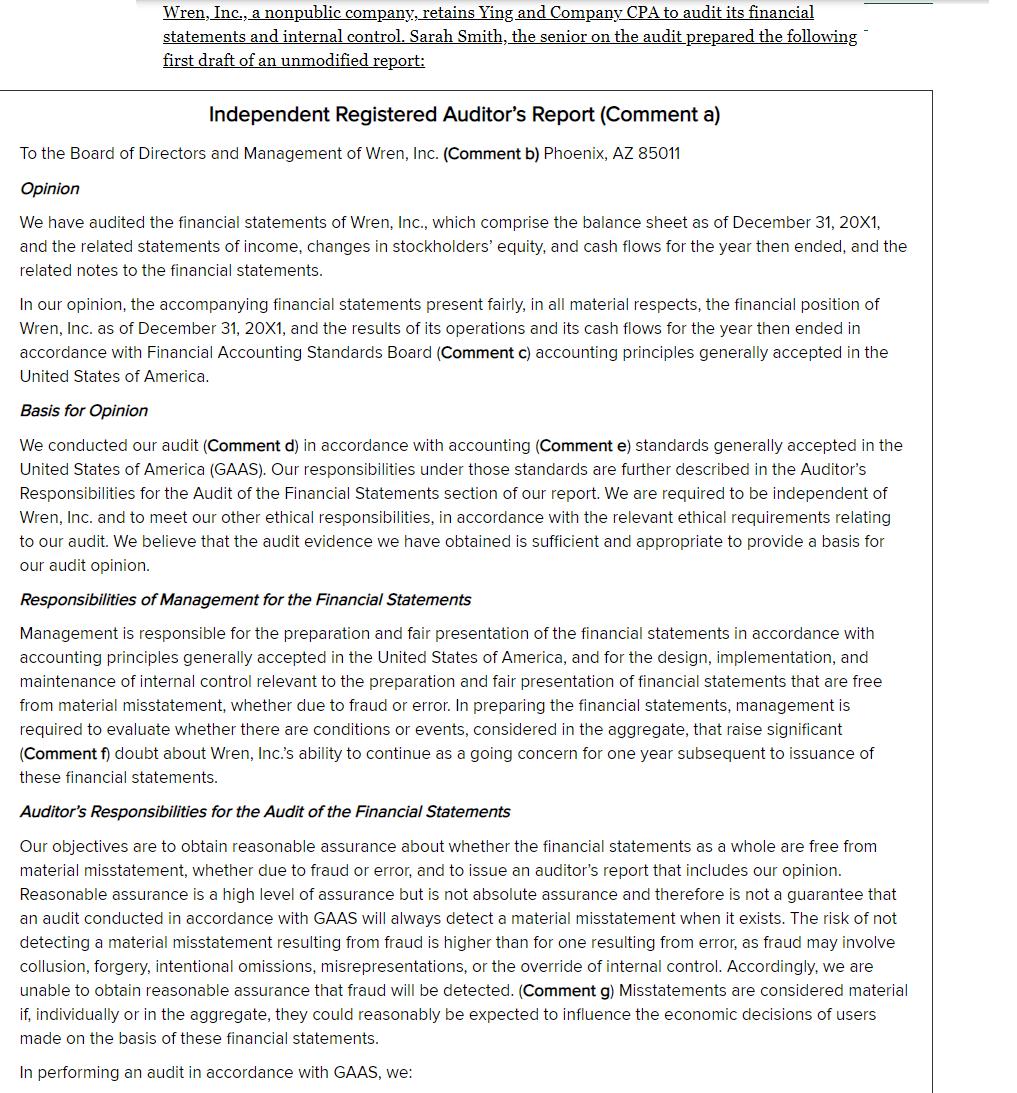

Wren, Inc., a nonpublic company, retains Ying and Company CPA to audit its financial statements and...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

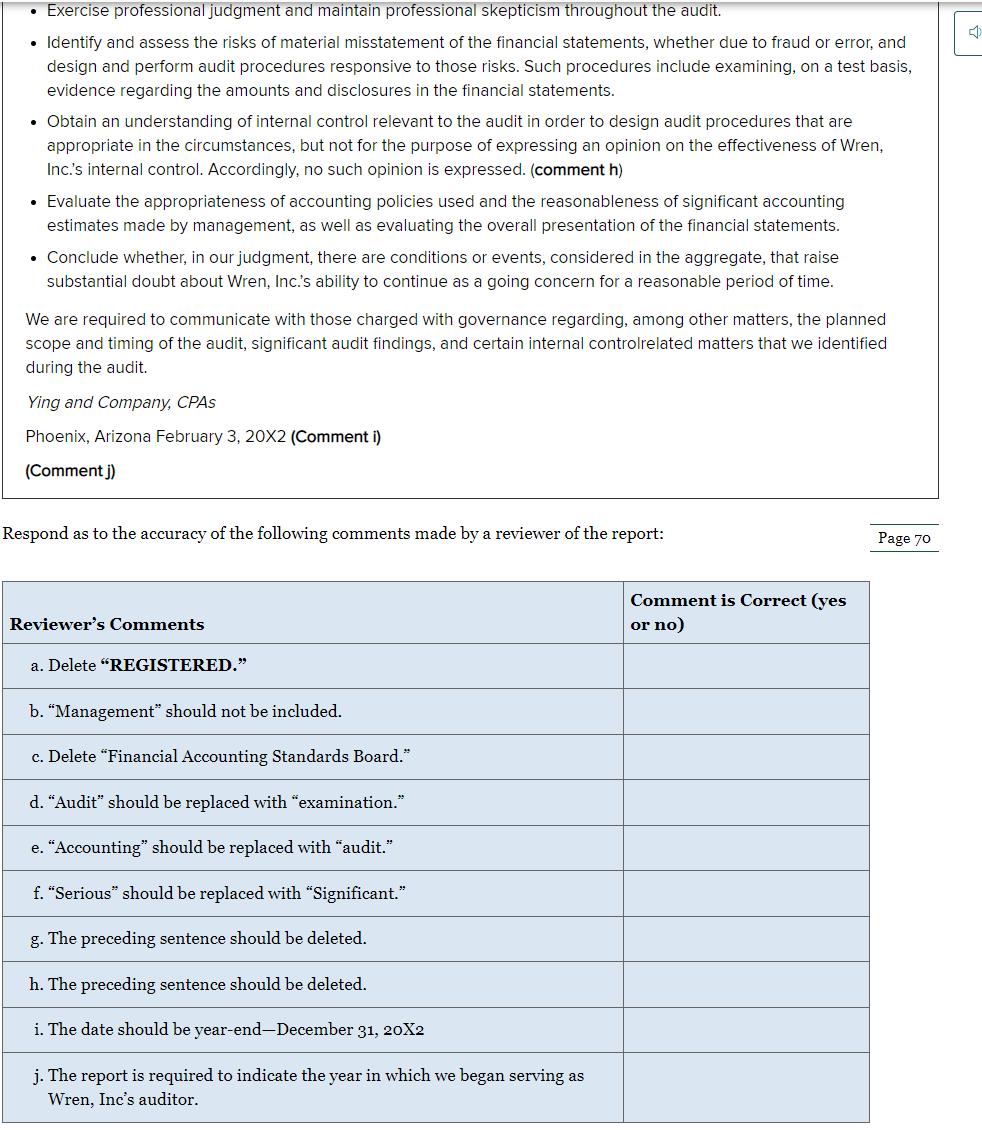

Wren, Inc., a nonpublic company, retains Ying and Company CPA to audit its financial statements and internal control. Sarah Smith, the senior on the audit prepared the following first draft of an unmodified report: Independent Registered Auditor's Report (Comment a) To the Board of Directors and Management of Wren, Inc. (Comment b) Phoenix, AZ 85011 Opinion We have audited the financial statements of Wren, Inc., which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of Wren, Inc. as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with Financial Accounting Standards Board (Comment c) accounting principles generally accepted in the United States of America. Basis for Opinion We conducted our audit (Comment d) in accordance with accounting (Comment e) standards generally accepted in the United States of America (GAAS). Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of Wren, Inc. and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements relating to our audit. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Responsibilities of Management for the Financial Statements Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America, and for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. In preparing the financial statements, management is required to evaluate whether there are conditions or events, considered in the aggregate, that raise significant (Comment f) doubt about Wren, Inc.'s ability to continue as a going concern for one year subsequent to issuance of these financial statements. Auditor's Responsibilities for the Audit of the Financial Statements Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with GAAS will always detect a material misstatement when it exists. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. Accordingly, we are unable to obtain reasonable assurance that fraud will be detected. (Comment g) Misstatements are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users made on the basis of these financial statements. In performing an audit in accordance with GAAS, we: • Exercise professional judgment and maintain professional skepticism throughout the audit. 4 • Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. • Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of Wren, Inc.'s internal control. Accordingly, no such opinion is expressed. (comment h) • Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. • Conclude whether, in our judgment, there are conditions or events, considered in the aggregate, that raise substantial doubt about Wren, Inc.'s ability to continue as a going concern for a reasonable period of time. We are required to communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit, significant audit findings, and certain internal controlrelated matters that we identified during the audit. Ying and Company, CPAS Phoenix, Arizona February 3, 20X2 (Comment i) (Comment j) Respond as to the accuracy of the following comments made by a reviewer of the report: Page 70 Reviewer's Comments a. Delete "REGISTERED." b. "Management" should not be included. c. Delete "Financial Accounting Standards Board." d. "Audit" should be replaced with "examination." e. "Accounting" should be replaced with "audit." f. "Serious" should be replaced with "Significant." g. The preceding sentence should be deleted. h. The preceding sentence should be deleted. i. The date should be year-end-December 31, 20X2 j. The report is required to indicate the year in which we began serving as Wren, Inc's auditor. Comment is Correct (yes or no) Wren, Inc., a nonpublic company, retains Ying and Company CPA to audit its financial statements and internal control. Sarah Smith, the senior on the audit prepared the following first draft of an unmodified report: Independent Registered Auditor's Report (Comment a) To the Board of Directors and Management of Wren, Inc. (Comment b) Phoenix, AZ 85011 Opinion We have audited the financial statements of Wren, Inc., which comprise the balance sheet as of December 31, 20X1, and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the related notes to the financial statements. In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of Wren, Inc. as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in accordance with Financial Accounting Standards Board (Comment c) accounting principles generally accepted in the United States of America. Basis for Opinion We conducted our audit (Comment d) in accordance with accounting (Comment e) standards generally accepted in the United States of America (GAAS). Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of Wren, Inc. and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements relating to our audit. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Responsibilities of Management for the Financial Statements Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America, and for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. In preparing the financial statements, management is required to evaluate whether there are conditions or events, considered in the aggregate, that raise significant (Comment f) doubt about Wren, Inc.'s ability to continue as a going concern for one year subsequent to issuance of these financial statements. Auditor's Responsibilities for the Audit of the Financial Statements Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with GAAS will always detect a material misstatement when it exists. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. Accordingly, we are unable to obtain reasonable assurance that fraud will be detected. (Comment g) Misstatements are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users made on the basis of these financial statements. In performing an audit in accordance with GAAS, we: • Exercise professional judgment and maintain professional skepticism throughout the audit. 4 • Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. • Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of Wren, Inc.'s internal control. Accordingly, no such opinion is expressed. (comment h) • Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. • Conclude whether, in our judgment, there are conditions or events, considered in the aggregate, that raise substantial doubt about Wren, Inc.'s ability to continue as a going concern for a reasonable period of time. We are required to communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit, significant audit findings, and certain internal controlrelated matters that we identified during the audit. Ying and Company, CPAS Phoenix, Arizona February 3, 20X2 (Comment i) (Comment j) Respond as to the accuracy of the following comments made by a reviewer of the report: Page 70 Reviewer's Comments a. Delete "REGISTERED." b. "Management" should not be included. c. Delete "Financial Accounting Standards Board." d. "Audit" should be replaced with "examination." e. "Accounting" should be replaced with "audit." f. "Serious" should be replaced with "Significant." g. The preceding sentence should be deleted. h. The preceding sentence should be deleted. i. The date should be year-end-December 31, 20X2 j. The report is required to indicate the year in which we began serving as Wren, Inc's auditor. Comment is Correct (yes or no)

Expert Answer:

Answer rating: 100% (QA)

Auditing Auditing is a procedure to examine and inspect the books of accounts along with the p... View the full answer

Related Book For

Principles of Auditing and Other Assurance Services

ISBN: 978-0078025617

19th edition

Authors: Ray Whittington, Kurt Pany

Posted Date:

Students also viewed these accounting questions

-

The Edwards Lake Community Hospital balance sheet as of December 31, 2019, follows. Required a. Record in general journal form the effect of the following transactions during the fiscal year ended...

-

If a combination of goods is located above an economy's production possibility curve and above its consumption possibility curve, then: this combination of goods is attainable regardless of whether...

-

The Vincent Community Hospital balance sheet as of December 31, 2013, follows. Required a. Record in general journal form the effect of the following transactions during the fiscal year ended...

-

Question 1: Presented below is information related to Al-Arab Company. Its capital structure consists of 80,000 ordinary shares. At December 31, 2020 an analysis of the accounts and discussions with...

-

Sally's Silk Screening produces specialty T-shirts that are primarily sold at special events. She is trying to decide how many toproduce for an upcoming event. During the event itself, which lasts...

-

Suppose that you meet three people Aaron, Bohan, and Crystal. Can you determine what Aaron, Bohan, and Crystal are if Aaron says "All of us are knaves" and Bohan says "Exactly one of us is a knave."?

-

Star \(\mathrm{Co}\). is considering the installation of new equipment for its warehouse. The equipment has an initial cost of \(\$ 600,000\) and an expected useful life of ten years. It is assumed...

-

Tri Designs, Inc. has the following data: Perform a vertical analysis of Tri Designss balance sheet for each year. TRI DESIGNS, INC. Comparative Balance Sheet December 31, 2016 and 2015 2016 2015...

-

What is the law of demand? A ) As the price of a good increases, its demand decreases B ) As the price of a good increases, its demand increases C ) Demand remains constant regardless of price...

-

Consider a two-date economy where there are three states of the world at date 1. There is a risky asset and a risk-free asset. The pay-off of the risky stock at date 1 will be $3, $6, or $4, and it...

-

This design uses just 3 JK flip-flops. The usual documents are required - the documents below, Karnaugh maps etc (looped), with a screenshot of your counter where M=1 and the Gray code = 101. Design...

-

What internal controls are applicable to a payroll bank account?

-

a. What is the objective and nature of a compilation service on historical financial statements? b. Indicate the content of the accountant's standard report on a compilation of historical financial...

-

Identify the tests of details that an auditor may use in auditing a payroll bank account.

-

a. How may a CPA be associated with unaudited financial statements? b. Describe the reporting and additional disclosure requirements when a CPA is associated with unaudited financial statements.

-

a. What is lapping? b. What circumstance is conducive to lapping?

-

Problem 2 Using the continuity equation u ov +=0 ox by along with the velocity distribution u u = 3y 1 y 26 26) and the expression for the boundary-layer thickness 4.64 x = Re derive an expression...

-

Calculate I, , and a for a 0.0175 m solution of Na 3 PO 4 at 298 K. Assume complete dissociation. How confident are you that your calculated results will agree with experimental results?

-

Morgan, CPA, is approached by a prospective audit client who wants to engage Morgan to perform an audit for the current year. In prior years, this prospective client was audited by another CPA....

-

How is the auditors understanding of the clients internal control documented in the audit working papers?

-

The mean of the audited values in a sample is $20. The accounts in that sample have a mean book value of $21, and the entire population of 10,000 accounts has an average book value of $19. Using...

-

Let \(h: \boldsymbol{x} \mapsto \mathbb{R}\) be a convex function and let \(\boldsymbol{X}\) be a random variable. Use the subgradient definition of convexity to prove Jensen's inequality: \[...

-

The purpose of this exercise is to prove the following Vapnik-Chernovenkis bound: for any finite class \(\mathscr{G}\) (containing only a finite number \(|\mathscr{G}|\) of possible functions) and a...

-

Using Jensen's inequality, show that the Kullback-Leibler divergence between probability densities \(f\) and \(g\) is always positive; that is, \[ \mathbb{E} \ln...

Study smarter with the SolutionInn App