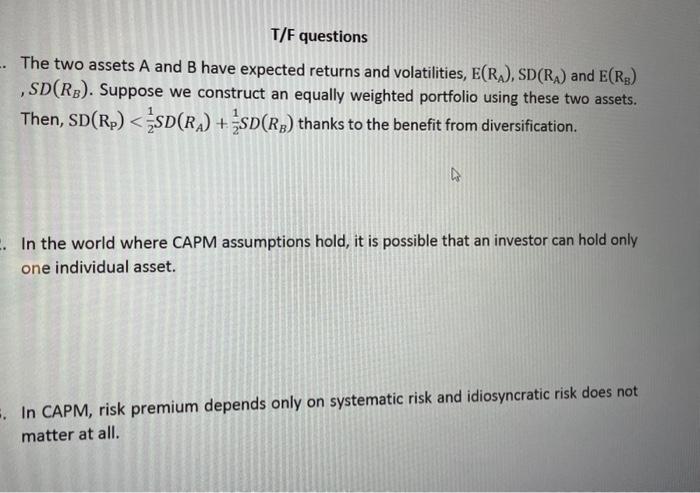

Question: write whether each is true or false and why The two assets A and B have expected returns and volatilities, E(RA),SD(RA) and E(RB) , SD(RB).

write whether each is true or false and why

The two assets A and B have expected returns and volatilities, E(RA),SD(RA) and E(RB) , SD(RB). Suppose we construct an equally weighted portfolio using these two assets. Then, SD(RP)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock