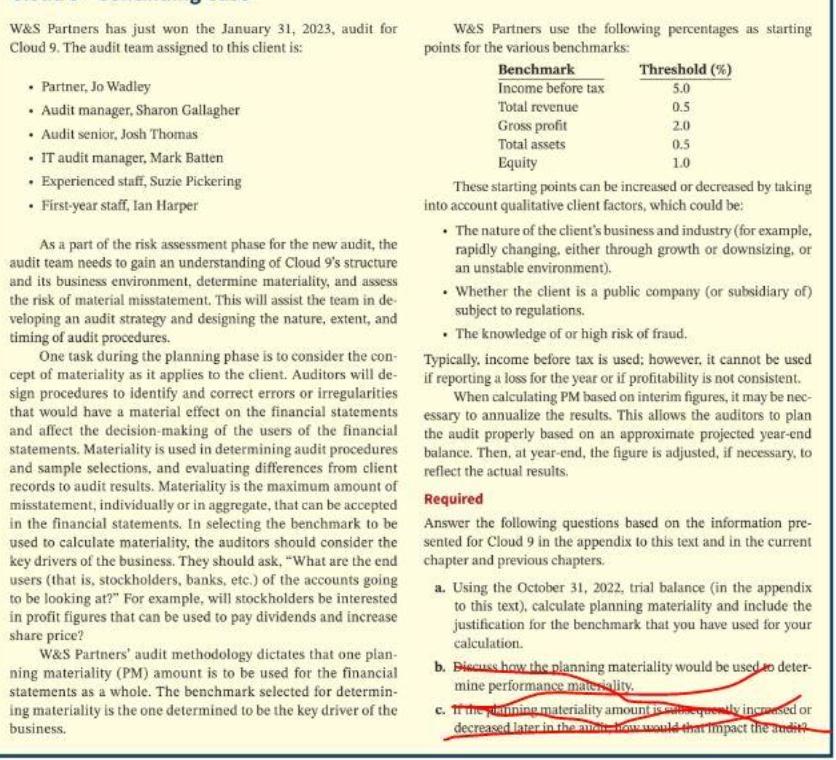

W&S Partners has just won the January 31, 2023, audit for Cloud 9. The audit team...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

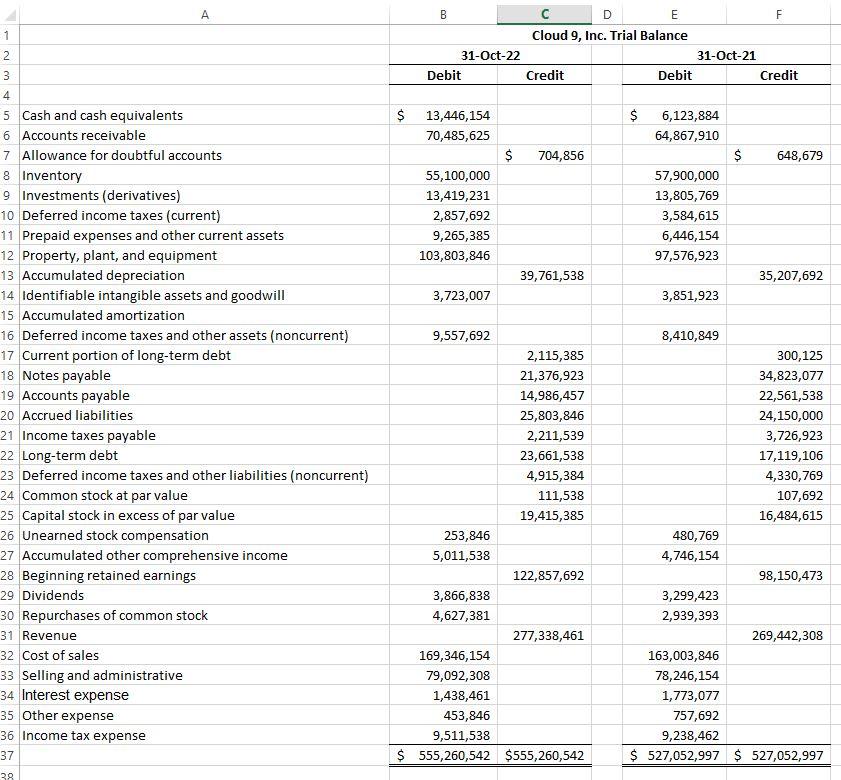

W&S Partners has just won the January 31, 2023, audit for Cloud 9. The audit team assigned to this client is: W&S Partners use the following percentages as starting points for the various benchmarks: Benchmark Threshold (%) 5.0 0.5 • Partner, Jo Wadley • Audit manager, Sharon Gallagher • Audit senior, Josh Thomas • IT audit manager, Mark Batten • Experienced staff, Suzie Pickering • First-year staff, lan Harper Income before tax Total revenue Gross profit Total assets 2.0 0.5 Equity 1.0 These starting points can be increased or decreased by taking into account qualitative client factors, which could be: As a part of the risk assessment phase for the new audit, the audit team needs to gain an understanding of Cloud 9's structure • The nature of the client's business and industry (for example, rapidly changing, either through growth or downsizing, or an unstable environment). and its business environment, determine materiality, and assess • Whether the client is a public company (or subsidiary of) subject to regulations. the risk of material misstatement. This will assist the team in de- veloping an audit strategy and designing the nature, extent, and timing of audit procedures. One task during the planning phase is to consider the con- cept of materiality as it applies to the client. Auditors will de- sign procedures to identify and correct errors or irregularities that would have a material effect on the financial statements essary to annualize the results. This allows the auditors to plan and affect the decision-making of the users of the financial the audit properly based on an approximate projected year-end statements. Materiality is used in determining audit procedures balance. Then, at year-end, the figure is adjusted, if necessary, to and sample selections, and evaluating differences from client records to audit results. Materiality is the maximum amount of misstatement, individually or in aggregate, that can be accepted in the financial statements. In selecting the benchmark to be Answer the following questions based on the information pre- used to calculate materiality, the auditors should consider the key drivers of the business. They should ask, "What are the end users (that is, stockholders, banks, etc.) of the accounts going to be looking at?" For example, will stockholders be interested in profit figures that can be used to pay dividends and increase share price? w&S Partners' audit methodology dictates that one plan- ning materiality (PM) amount is to be used for the financial statements as a whole. The benchmark selected for determin- • The knowledge of or high risk of fraud. Typically, income before tax is used; however, it cannot be used if reporting a loss for the year or if profitability is not consistent. When calculating PM based on interim figures, it may be nec- reflect the actual results. Required sented for Cloud 9 in the appendix to this text and in the current chapter and previous chapters. a. Using the October 31, 2022, trial balance (in the appendix to this text), calculate planning materiality and include the justification for the benchmark that you have used for your calculation. b. Biscuss how the planning materiality would be used eo deter- mine performance materiality. c. . The nning materiality amount iscquently incrsed or decreased later in the a owwauld thnt mpact the andit ing materiality is the one determined to be the key driver of the business. A B Cloud 9, Inc. Trial Balance 31-Oct-22 31-Oct-21 Debit Credit Debit Credit 5 Cash and cash equivalents 6 Accounts receivable 7 Allowance for doubtful accounts $ 13,446,154 $ 6,123,884 70,485,625 64,867,910 2$ 704,856 648,679 8 Inventory 55,100,000 57,900,000 9 Investments (derivatives) 10 Deferred income taxes (current) 11 Prepaid expenses and other current assets 12 Property, plant, and equipment 13,419,231 13,805,769 2,857,692 3,584,615 9,265,385 6,446,154 103,803,846 97,576,923 13 Accumulated depreciation 14 Identifiable intangible assets and goodwill 15 Accumulated amortization 16 Deferred income taxes and other assets (noncurrent) 17 Current portion of long-term debt 18 Notes payable 19 Accounts payable 20 Accrued liabilities 21 Income taxes payable 22 Long-term debt 39,761,538 35,207,692 3,723,007 3,851,923 9,557,692 8,410,849 2,115,385 300,125 21,376,923 34,823,077 14,986,457 22,561,538 25,803,846 24,150,000 2,211,539 3,726,923 23,661,538 17,119,106 23 Deferred income taxes and other liabilities (noncurrent) 4,915,384 4,330,769 24 Common stock at par value 111,538 107,692 25 Capital stock in excess of par value 26 Unearned stock compensation 19,415,385 16,484,615 253,846 480,769 27 Accumulated other comprehensive income 28 Beginning retained earnings 29 Dividends 5,011,538 4,746,154 122,857,692 98,150,473 3,866,838 3,299,423 30 Repurchases of common stock 31 Revenue 4,627,381 2,939,393 277,338,461 269,442,308 32 Cost of sales 169,346,154 163,003,846 33 Selling and administrative 34 Interest expense 79,092,308 78,246,154 1,438,461 1,773,077 35 Other expense 453,846 757,692 36 Income tax expense 9,511,538 9,238,462 $ 555,260,542 $555,260,542 $ 527,052,997 $ 527,052,997 37 38 %24 W&S Partners has just won the January 31, 2023, audit for Cloud 9. The audit team assigned to this client is: W&S Partners use the following percentages as starting points for the various benchmarks: Benchmark Threshold (%) 5.0 0.5 • Partner, Jo Wadley • Audit manager, Sharon Gallagher • Audit senior, Josh Thomas • IT audit manager, Mark Batten • Experienced staff, Suzie Pickering • First-year staff, lan Harper Income before tax Total revenue Gross profit Total assets 2.0 0.5 Equity 1.0 These starting points can be increased or decreased by taking into account qualitative client factors, which could be: As a part of the risk assessment phase for the new audit, the audit team needs to gain an understanding of Cloud 9's structure • The nature of the client's business and industry (for example, rapidly changing, either through growth or downsizing, or an unstable environment). and its business environment, determine materiality, and assess • Whether the client is a public company (or subsidiary of) subject to regulations. the risk of material misstatement. This will assist the team in de- veloping an audit strategy and designing the nature, extent, and timing of audit procedures. One task during the planning phase is to consider the con- cept of materiality as it applies to the client. Auditors will de- sign procedures to identify and correct errors or irregularities that would have a material effect on the financial statements essary to annualize the results. This allows the auditors to plan and affect the decision-making of the users of the financial the audit properly based on an approximate projected year-end statements. Materiality is used in determining audit procedures balance. Then, at year-end, the figure is adjusted, if necessary, to and sample selections, and evaluating differences from client records to audit results. Materiality is the maximum amount of misstatement, individually or in aggregate, that can be accepted in the financial statements. In selecting the benchmark to be Answer the following questions based on the information pre- used to calculate materiality, the auditors should consider the key drivers of the business. They should ask, "What are the end users (that is, stockholders, banks, etc.) of the accounts going to be looking at?" For example, will stockholders be interested in profit figures that can be used to pay dividends and increase share price? w&S Partners' audit methodology dictates that one plan- ning materiality (PM) amount is to be used for the financial statements as a whole. The benchmark selected for determin- • The knowledge of or high risk of fraud. Typically, income before tax is used; however, it cannot be used if reporting a loss for the year or if profitability is not consistent. When calculating PM based on interim figures, it may be nec- reflect the actual results. Required sented for Cloud 9 in the appendix to this text and in the current chapter and previous chapters. a. Using the October 31, 2022, trial balance (in the appendix to this text), calculate planning materiality and include the justification for the benchmark that you have used for your calculation. b. Biscuss how the planning materiality would be used eo deter- mine performance materiality. c. . The nning materiality amount iscquently incrsed or decreased later in the a owwauld thnt mpact the andit ing materiality is the one determined to be the key driver of the business. A B Cloud 9, Inc. Trial Balance 31-Oct-22 31-Oct-21 Debit Credit Debit Credit 5 Cash and cash equivalents 6 Accounts receivable 7 Allowance for doubtful accounts $ 13,446,154 $ 6,123,884 70,485,625 64,867,910 2$ 704,856 648,679 8 Inventory 55,100,000 57,900,000 9 Investments (derivatives) 10 Deferred income taxes (current) 11 Prepaid expenses and other current assets 12 Property, plant, and equipment 13,419,231 13,805,769 2,857,692 3,584,615 9,265,385 6,446,154 103,803,846 97,576,923 13 Accumulated depreciation 14 Identifiable intangible assets and goodwill 15 Accumulated amortization 16 Deferred income taxes and other assets (noncurrent) 17 Current portion of long-term debt 18 Notes payable 19 Accounts payable 20 Accrued liabilities 21 Income taxes payable 22 Long-term debt 39,761,538 35,207,692 3,723,007 3,851,923 9,557,692 8,410,849 2,115,385 300,125 21,376,923 34,823,077 14,986,457 22,561,538 25,803,846 24,150,000 2,211,539 3,726,923 23,661,538 17,119,106 23 Deferred income taxes and other liabilities (noncurrent) 4,915,384 4,330,769 24 Common stock at par value 111,538 107,692 25 Capital stock in excess of par value 26 Unearned stock compensation 19,415,385 16,484,615 253,846 480,769 27 Accumulated other comprehensive income 28 Beginning retained earnings 29 Dividends 5,011,538 4,746,154 122,857,692 98,150,473 3,866,838 3,299,423 30 Repurchases of common stock 31 Revenue 4,627,381 2,939,393 277,338,461 269,442,308 32 Cost of sales 169,346,154 163,003,846 33 Selling and administrative 34 Interest expense 79,092,308 78,246,154 1,438,461 1,773,077 35 Other expense 453,846 757,692 36 Income tax expense 9,511,538 9,238,462 $ 555,260,542 $555,260,542 $ 527,052,997 $ 527,052,997 37 38 %24

Expert Answer:

Answer rating: 100% (QA)

WS Partners commenced planning the Cloud 9 audit by gaining an understanding of theclients structure and its business environment A major task is to consider the concept ofmateriality as it applies to ... View the full answer

Related Book For

College Physics

ISBN: 978-0495113690

7th Edition

Authors: Raymond A. Serway, Jerry S. Faughn, Chris Vuille, Charles A. Bennett

Posted Date:

Students also viewed these civil engineering questions

-

The following information is to be used for the next three questions: Downward Inc. manufactures and sells a product, Z30. The per unit, standards for the direct costs of product Z30 are as follows:...

-

The following information is to be used for the next three questions: Downward Inc. manufactures and sells a product, Z30. The per unit, standards for the direct costs of product Z30 are as follows:...

-

for flood control? LOI/PLO (10) Q4: Compute the stream flow (in m/s) for the measurement data given in Table 1. Take the current meter rating with a = 0.05 and b = 0.35 for water velocity (in m/sec)...

-

Cindy Bagnal, the manager of Cayce Printing Service, has provided you with the following aging schedule for Cayce's accounts receivable: Cindy indicates that the $126,700 of accounts receivable...

-

A specialized retailer has a selection of five products. The following is information relating to these products. The company estimates selling costs to be 10% of selling price, primarily for sales...

-

Each of the following formulas for determining shareholders? required rate of return can be right or wrong depending on the circumstances: For each formula construct a simple numerical example...

-

Mrs. Clarks Foods was an Iowa company engaged in the business of distributing juice beverages. International Suntrade and Miller & Smith Foods were Canadian companies that acted as brokers...

-

Sanderson Manufacturing produces ornate, decorative wood frame doors and windows. Each item produced goes through 3 manufacturing processes: cutting, sanding, and finishing. Each door produced...

-

A car traveling 87.0 km/h is 1500 m behind a truck traveling at 74.0 km/h. How far from its initial position does the car have to travel to catch up to the truck.

-

Thriller Corporation has one class of voting common stock, of which 1,000 shares are issued and outstanding. The shares are owned as follows: Joe Jackson ......................................... 400...

-

Solve the integral equation f(t) + 4 f (t-T) f(7) dr = 3t for f(t). Recall the convolution theorem: L{f* g} = L{f(t)} L{g(t)}.

-

Why are FSNCs dependent on passengers traveling for business for profitability?

-

Innovation Company is thinking about marketing a new software product. Upfront costs to market and develop the product are $5,100,000. The product is expected to generate profits of $1,000,000 per...

-

Why is the pairing development process critical to an airlines cost control?

-

Bruges Corporations Memorandum of Association authorizes issuance of 3,000,000 shares of common stock. Currently, Bruges has 2,200,000 million authorized and paid up shares and holds 500,000 shares...

-

Use the Airline Product Design model to compare two airlines from different categories.

-

400-SMC-1011.1.2 (F101: Strategic Change) 400-SMC-1011.1.4 (F103: Developing Army Organizational capability) 400-SMC-1011.1.5 (F104: Planning, Programming, Budgeting, and Execution (PPBE) Process and...

-

Suppose the index goes to 18 percent in year 5. What is the effective cost of the unrestricted ARM?

-

A certain toaster has a heating element made of Nichrome resistance wire. When the toaster is first connected to a 120-V source of potential difference (and the wire is at a temperature of 20.0C),...

-

A room contains air in which the speed of sound is 343 m/s. The walls of the room are made of concrete, in which the speed of sound is 1 850 m/s. (a) Find the critical angle for total internal...

-

How is it possible that a complete circle of a rainbow can sometimes be seen from an airplane?

-

Cruz Manufacturing Ltds sales slumped badly in 2019. For the first time in its history, it operated at a loss. The companys income statement showed the following results from selling 600 000 units of...

-

The following are emails from various students to Dr. Destiny Sands, who is a professor in the English Department. These students are wondering if Dr. Sands would let them register for her...

-

What are some flawed assumptions about workplace communication? What is the reality for each myth?

Study smarter with the SolutionInn App