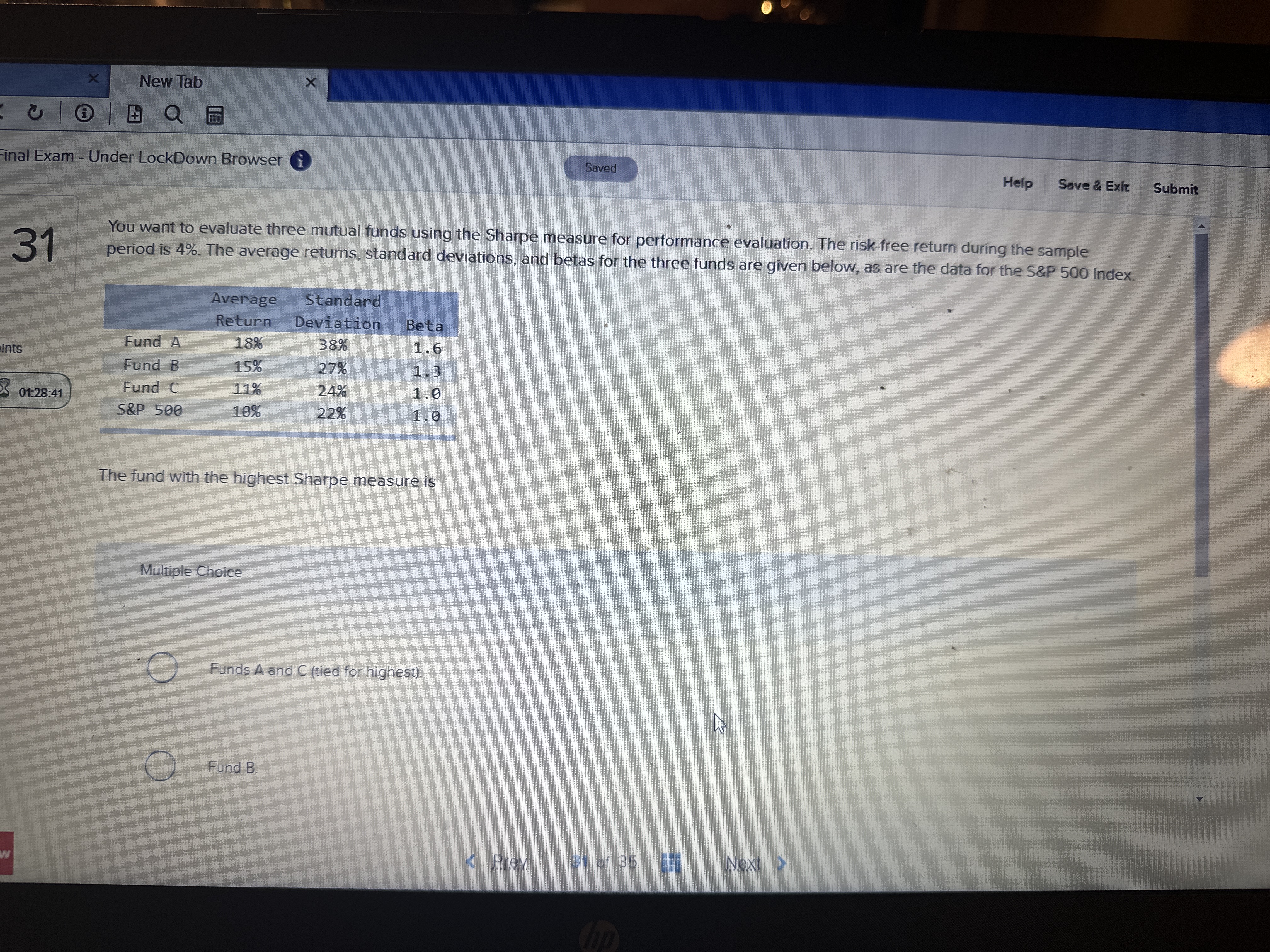

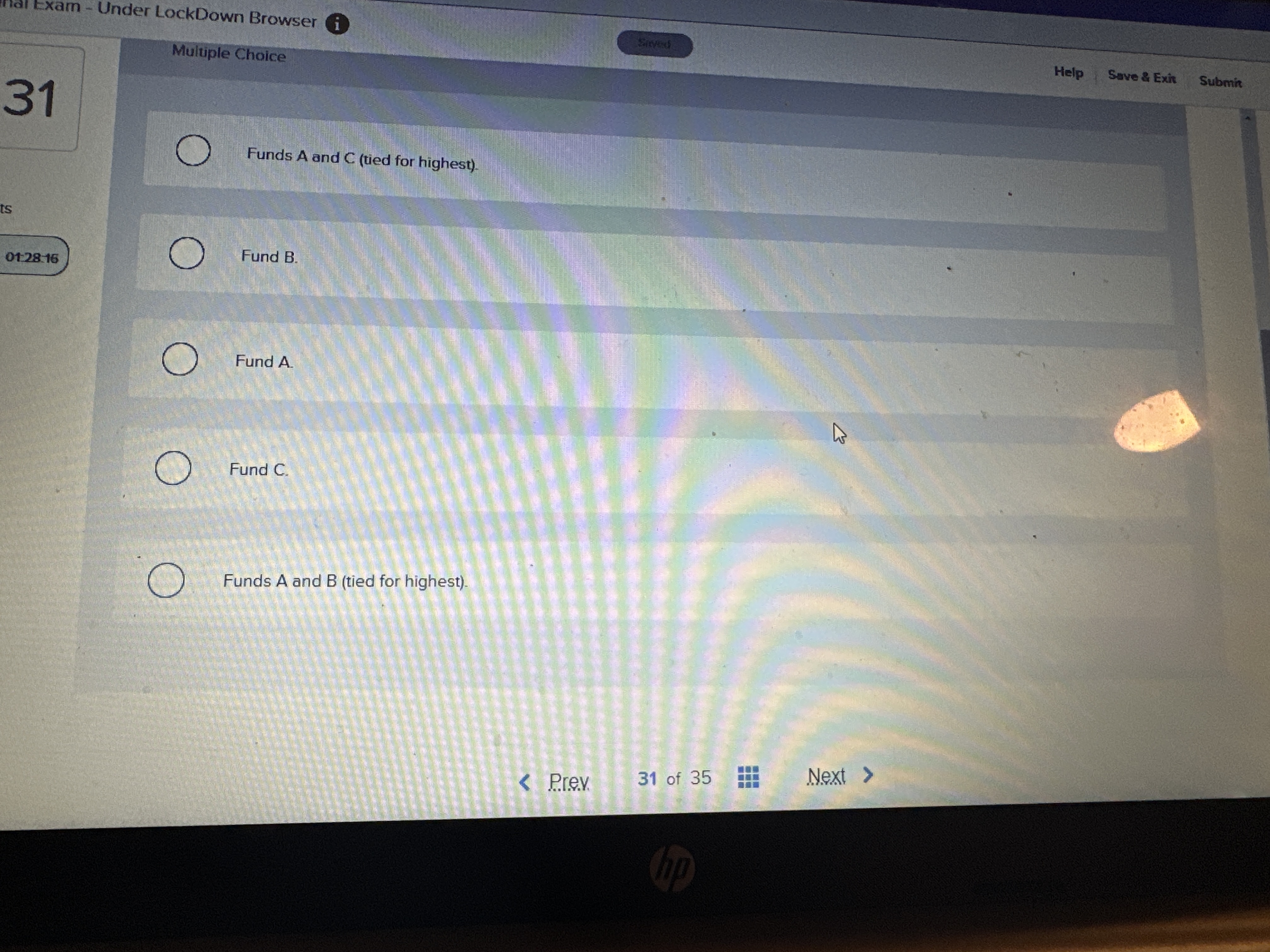

Question: X New Tab X Final Exam - Under LockDown Browser i Saved Help Save & Exit Submit You want to evaluate three mutual funds using

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts