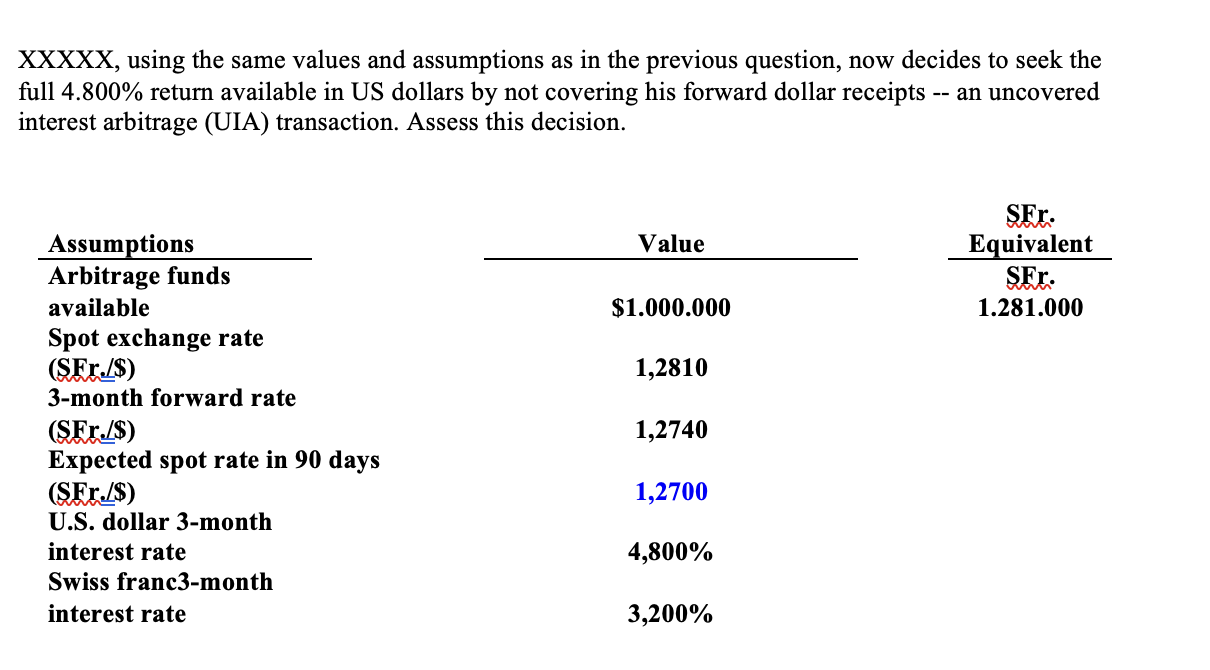

Question: XXXXX, using the same values and assumptions as in the previous question, now decides to seek the full 4.800% return available in US dollars by

XXXXX, using the same values and assumptions as in the previous question, now decides to seek the full 4.800% return available in US dollars by not covering his forward dollar receipts -- an uncovered interest arbitrage (UIA) transaction. Assess this decision. Value Ser: Equivalent SFr. 1.281.000 $1.000.000 1,2810 Assumptions Arbitrage funds available Spot exchange rate (SFr./$) 3-month forward rate (SFr./$) Expected spot rate in 90 days (SFr./$) U.S. dollar 3-month interest rate Swiss franc3-month interest rate 1,2740 1,2700 4,800% 3,200%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock