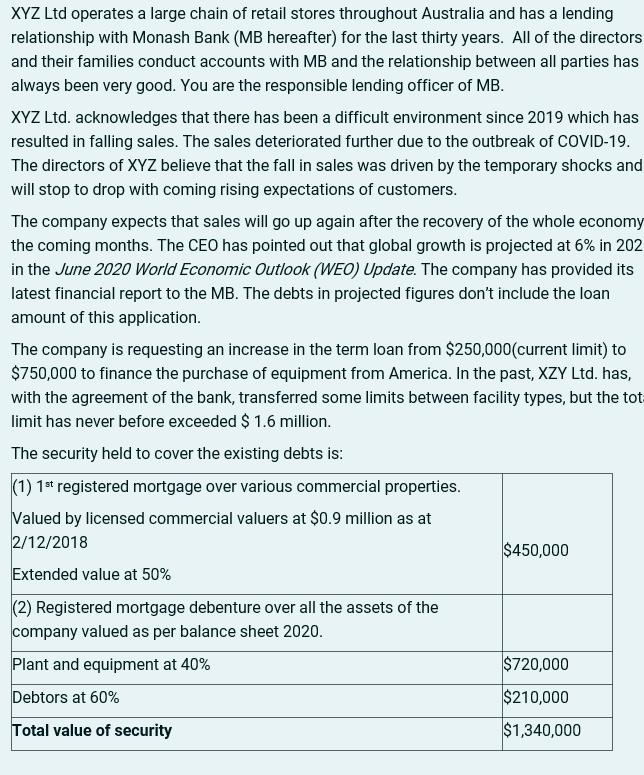

XYZ Ltd operates a large chain of retail stores throughout Australia and has a lending relationship...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

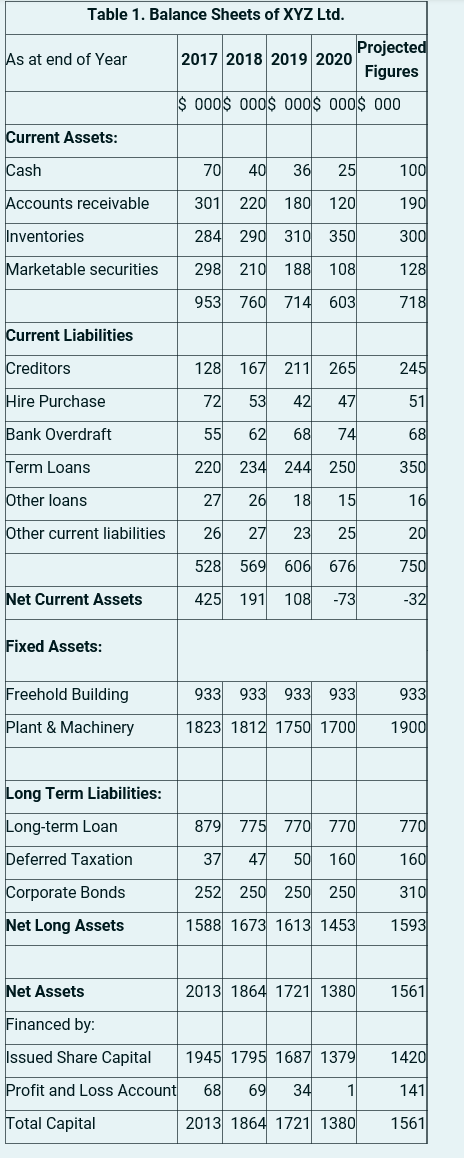

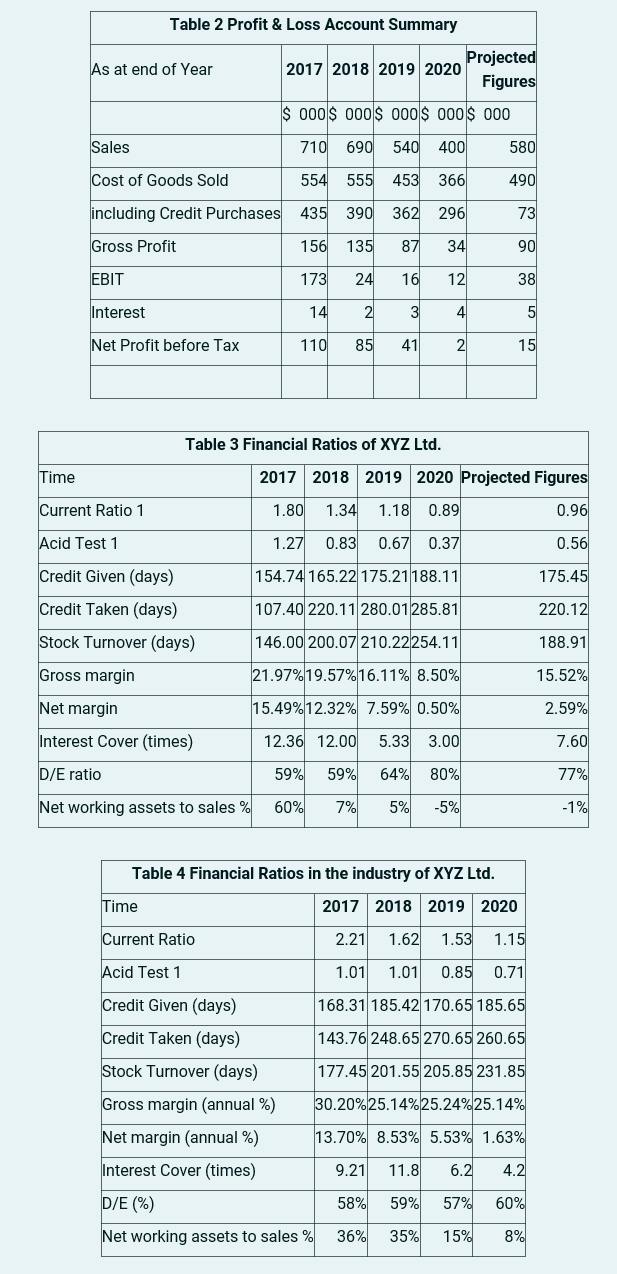

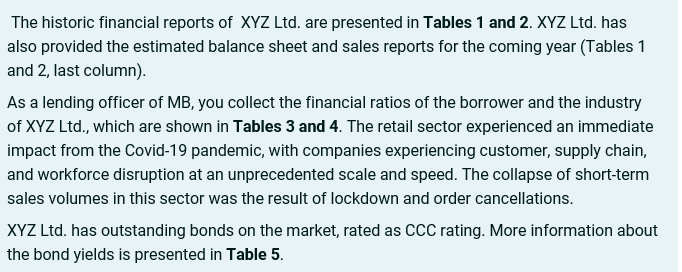

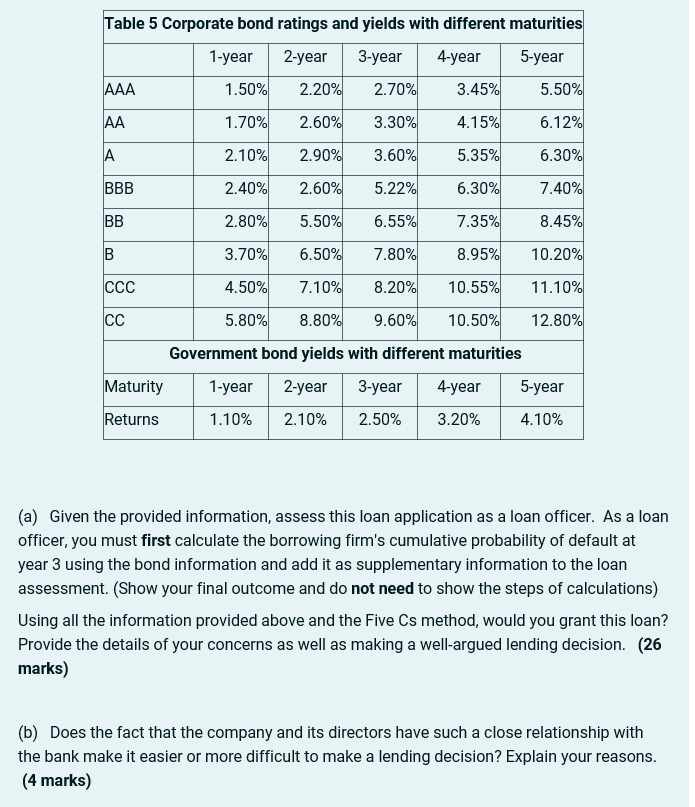

XYZ Ltd operates a large chain of retail stores throughout Australia and has a lending relationship with Monash Bank (MB hereafter) for the last thirty years. All of the directors and their families conduct accounts with MB and the relationship between all parties has always been very good. You are the responsible lending officer of MB. XYZ Ltd. acknowledges that there has been a difficult environment since 2019 which has resulted in falling sales. The sales deteriorated further due to the outbreak of COVID-19. The directors of XYZ believe that the fall in sales was driven by the temporary shocks and will stop to drop with coming rising expectations of customers. The company expects that sales will go up again after the recovery of the whole economy the coming months. The CEO has pointed out that global growth is projected at 6% in 202 in the June 2020 World Economic Outlook (WEO) Update. The company has provided its latest financial report to the MB. The debts in projected figures don't include the loan amount of this application. The company is requesting an increase in the term loan from $250,000(current limit) to $750,000 to finance the purchase of equipment from America. In the past, XZY Ltd. has, with the agreement of the bank, transferred some limits between facility types, but the tot limit has never before exceeded $ 1.6 million. The security held to cover the existing debts is: (1) 1st registered mortgage over various commercial properties. Valued by licensed commercial valuers at $0.9 million as at 2/12/2018 $450,000 Extended value at 50% (2) Registered mortgage debenture over all the assets of the company valued as per balance sheet 2020. Plant and equipment at 40% $720,000 Debtors at 60% Total value of security $210,000 $1,340,000 Table 1. Balance Sheets of XYZ Ltd. As at end of Year 2017 2018 2019 2020 Projected Figures $ 000$ 000$ 000$ 000$ 000 Current Assets: Cash 70 40 36 25 100 Accounts receivable 301 220 180 120 190 Inventories 284 290 310 350 Marketable securities 298 210 188 108 953 760 714 603 300 128 718 Current Liabilities Creditors 128 167 211 265 245 Hire Purchase 72 53 42 47 51 Bank Overdraft 55 62 68 74 68 Term Loans 220 234 244 250 350 Other loans 27 26 18 15 16 Other current liabilities 26 27 23 25 20 528 569 606 676 750 Net Current Assets 425 191 108 -73 -32 Fixed Assets: Freehold Building Plant & Machinery 933 933 933 933 1823 1812 1750 1700 933 1900 Long Term Liabilities: Long-term Loan 879 775 770 770 770 Deferred Taxation 37 47 50 160 160 Corporate Bonds 252 250 250 250 310 Net Long Assets 1588 1673 1613 1453 1593 Net Assets Financed by: 2013 1864 1721 1380 1561 Issued Share Capital 1945 1795 1687 1379 1420 Profit and Loss Account 68 69 34 1 141 Total Capital 2013 1864 1721 1380 1561 Table 2 Profit & Loss Account Summary As at end of Year 2017 2018 2019 2020 Projected Figures $ 000$ 000$ 000 $ 000$ 000 Sales 710 690 540 400 580 Cost of Goods Sold 554 555 453 366 490 including Credit Purchases 435 390 362 296 73 Gross Profit 156 135 87 34 90 EBIT 173 24 16 12 38 Interest 14 2 3 4 5 Net Profit before Tax 110 85 41 2 15 Time Table 3 Financial Ratios of XYZ Ltd. 2017 2018 2019 2020 Projected Figures Current Ratio 1 1.80 1.34 1.18 0.89 0.96 Acid Test 1 1.27 0.83 0.67 0.37 0.56 Credit Given (days) 154.74 165.22 175.21 188.11 175.45 Credit Taken (days) 107.40 220.11 280.01 285.81 220.12 Stock Turnover (days) 146.00 200.07 210.22254.11 188.91 Gross margin 21.97% 19.57% 16.11% 8.50% 15.52% Net margin 15.49% 12.32% 7.59% 0.50% 2.59% Interest Cover (times) 12.36 12.00 5.33 3.00 7.60 D/E ratio Net working assets to sales% 59% 59% 64% 80% 60% 77% 7% 5% -5% -1% Time Table 4 Financial Ratios in the industry of XYZ Ltd. Current Ratio 2017 2018 2019 2020 2.21 1.62 1.53 1.15 Acid Test 1 1.01 1.01 0.85 0.71 Credit Given (days) Credit Taken (days) Stock Turnover (days) Gross margin (annual %) 168.31 185.42 170.65 185.65 143.76 248.65 270.65 260.65 177.45 201.55 205.85 231.85 30.20% 25.14% 25.24% 25.14% Net margin (annual %) 13.70% 8.53% 5.53% 1.63% Interest Cover (times) D/E (%) Net working assets to sales% 9.21 11.8 6.2 4.2 58% 59% 57% 60% 36% 35% 15% 8% The historic financial reports of XYZ Ltd. are presented in Tables 1 and 2. XYZ Ltd. has also provided the estimated balance sheet and sales reports for the coming year (Tables 1 and 2, last column). As a lending officer of MB, you collect the financial ratios of the borrower and the industry of XYZ Ltd., which are shown in Tables 3 and 4. The retail sector experienced an immediate impact from the Covid-19 pandemic, with companies experiencing customer, supply chain, and workforce disruption at an unprecedented scale and speed. The collapse of short-term sales volumes in this sector was the result of lockdown and order cancellations. XYZ Ltd. has outstanding bonds on the market, rated as CCC rating. More information about the bond yields is presented in Table 5. Table 5 Corporate bond ratings and yields with different maturities 1-year 2-year 3-year 4-year 5-year AAA 1.50% 2.20% 2.70% 3.45% 5.50% AA 1.70% 2.60% 3.30% 4.15% 6.12% A 2.10% 2.90% 3.60% 5.35% 6.30% BBB 2.40% 2.60% 5.22% 6.30% 7.40% BB 2.80% 5.50% 6.55% 7.35% 8.45% B 3.70% 6.50% 7.80% 8.95% 10.20% CCC 4.50% 7.10% 8.20% 10.55% 11.10% CC 5.80% 8.80% 9.60% 10.50% 12.80% Government bond yields with different maturities Maturity 1-year 2-year 3-year 4-year 5-year Returns 1.10% 2.10% 2.50% 3.20% 4.10% (a) Given the provided information, assess this loan application as a loan officer. As a loan officer, you must first calculate the borrowing firm's cumulative probability of default at year 3 using the bond information and add it as supplementary information to the loan assessment. (Show your final outcome and do not need to show the steps of calculations) Using all the information provided above and the Five Cs method, would you grant this loan? Provide the details of your concerns as well as making a well-argued lending decision. (26 marks) (b) Does the fact that the company and its directors have such a close relationship with the bank make it easier or more difficult to make a lending decision? Explain your reasons. (4 marks) XYZ Ltd operates a large chain of retail stores throughout Australia and has a lending relationship with Monash Bank (MB hereafter) for the last thirty years. All of the directors and their families conduct accounts with MB and the relationship between all parties has always been very good. You are the responsible lending officer of MB. XYZ Ltd. acknowledges that there has been a difficult environment since 2019 which has resulted in falling sales. The sales deteriorated further due to the outbreak of COVID-19. The directors of XYZ believe that the fall in sales was driven by the temporary shocks and will stop to drop with coming rising expectations of customers. The company expects that sales will go up again after the recovery of the whole economy the coming months. The CEO has pointed out that global growth is projected at 6% in 202 in the June 2020 World Economic Outlook (WEO) Update. The company has provided its latest financial report to the MB. The debts in projected figures don't include the loan amount of this application. The company is requesting an increase in the term loan from $250,000(current limit) to $750,000 to finance the purchase of equipment from America. In the past, XZY Ltd. has, with the agreement of the bank, transferred some limits between facility types, but the tot limit has never before exceeded $ 1.6 million. The security held to cover the existing debts is: (1) 1st registered mortgage over various commercial properties. Valued by licensed commercial valuers at $0.9 million as at 2/12/2018 $450,000 Extended value at 50% (2) Registered mortgage debenture over all the assets of the company valued as per balance sheet 2020. Plant and equipment at 40% $720,000 Debtors at 60% Total value of security $210,000 $1,340,000 Table 1. Balance Sheets of XYZ Ltd. As at end of Year 2017 2018 2019 2020 Projected Figures $ 000$ 000$ 000$ 000$ 000 Current Assets: Cash 70 40 36 25 100 Accounts receivable 301 220 180 120 190 Inventories 284 290 310 350 Marketable securities 298 210 188 108 953 760 714 603 300 128 718 Current Liabilities Creditors 128 167 211 265 245 Hire Purchase 72 53 42 47 51 Bank Overdraft 55 62 68 74 68 Term Loans 220 234 244 250 350 Other loans 27 26 18 15 16 Other current liabilities 26 27 23 25 20 528 569 606 676 750 Net Current Assets 425 191 108 -73 -32 Fixed Assets: Freehold Building Plant & Machinery 933 933 933 933 1823 1812 1750 1700 933 1900 Long Term Liabilities: Long-term Loan 879 775 770 770 770 Deferred Taxation 37 47 50 160 160 Corporate Bonds 252 250 250 250 310 Net Long Assets 1588 1673 1613 1453 1593 Net Assets Financed by: 2013 1864 1721 1380 1561 Issued Share Capital 1945 1795 1687 1379 1420 Profit and Loss Account 68 69 34 1 141 Total Capital 2013 1864 1721 1380 1561 Table 2 Profit & Loss Account Summary As at end of Year 2017 2018 2019 2020 Projected Figures $ 000$ 000$ 000 $ 000$ 000 Sales 710 690 540 400 580 Cost of Goods Sold 554 555 453 366 490 including Credit Purchases 435 390 362 296 73 Gross Profit 156 135 87 34 90 EBIT 173 24 16 12 38 Interest 14 2 3 4 5 Net Profit before Tax 110 85 41 2 15 Time Table 3 Financial Ratios of XYZ Ltd. 2017 2018 2019 2020 Projected Figures Current Ratio 1 1.80 1.34 1.18 0.89 0.96 Acid Test 1 1.27 0.83 0.67 0.37 0.56 Credit Given (days) 154.74 165.22 175.21 188.11 175.45 Credit Taken (days) 107.40 220.11 280.01 285.81 220.12 Stock Turnover (days) 146.00 200.07 210.22254.11 188.91 Gross margin 21.97% 19.57% 16.11% 8.50% 15.52% Net margin 15.49% 12.32% 7.59% 0.50% 2.59% Interest Cover (times) 12.36 12.00 5.33 3.00 7.60 D/E ratio Net working assets to sales% 59% 59% 64% 80% 60% 77% 7% 5% -5% -1% Time Table 4 Financial Ratios in the industry of XYZ Ltd. Current Ratio 2017 2018 2019 2020 2.21 1.62 1.53 1.15 Acid Test 1 1.01 1.01 0.85 0.71 Credit Given (days) Credit Taken (days) Stock Turnover (days) Gross margin (annual %) 168.31 185.42 170.65 185.65 143.76 248.65 270.65 260.65 177.45 201.55 205.85 231.85 30.20% 25.14% 25.24% 25.14% Net margin (annual %) 13.70% 8.53% 5.53% 1.63% Interest Cover (times) D/E (%) Net working assets to sales% 9.21 11.8 6.2 4.2 58% 59% 57% 60% 36% 35% 15% 8% The historic financial reports of XYZ Ltd. are presented in Tables 1 and 2. XYZ Ltd. has also provided the estimated balance sheet and sales reports for the coming year (Tables 1 and 2, last column). As a lending officer of MB, you collect the financial ratios of the borrower and the industry of XYZ Ltd., which are shown in Tables 3 and 4. The retail sector experienced an immediate impact from the Covid-19 pandemic, with companies experiencing customer, supply chain, and workforce disruption at an unprecedented scale and speed. The collapse of short-term sales volumes in this sector was the result of lockdown and order cancellations. XYZ Ltd. has outstanding bonds on the market, rated as CCC rating. More information about the bond yields is presented in Table 5. Table 5 Corporate bond ratings and yields with different maturities 1-year 2-year 3-year 4-year 5-year AAA 1.50% 2.20% 2.70% 3.45% 5.50% AA 1.70% 2.60% 3.30% 4.15% 6.12% A 2.10% 2.90% 3.60% 5.35% 6.30% BBB 2.40% 2.60% 5.22% 6.30% 7.40% BB 2.80% 5.50% 6.55% 7.35% 8.45% B 3.70% 6.50% 7.80% 8.95% 10.20% CCC 4.50% 7.10% 8.20% 10.55% 11.10% CC 5.80% 8.80% 9.60% 10.50% 12.80% Government bond yields with different maturities Maturity 1-year 2-year 3-year 4-year 5-year Returns 1.10% 2.10% 2.50% 3.20% 4.10% (a) Given the provided information, assess this loan application as a loan officer. As a loan officer, you must first calculate the borrowing firm's cumulative probability of default at year 3 using the bond information and add it as supplementary information to the loan assessment. (Show your final outcome and do not need to show the steps of calculations) Using all the information provided above and the Five Cs method, would you grant this loan? Provide the details of your concerns as well as making a well-argued lending decision. (26 marks) (b) Does the fact that the company and its directors have such a close relationship with the bank make it easier or more difficult to make a lending decision? Explain your reasons. (4 marks)

Expert Answer:

Posted Date:

Students also viewed these finance questions

-

Find the time required for an investment of 5000 dollars to grow to 7000 dollars at an interest rate of 7.5 percent per year, compounded quarterly. The answer is t= _____________ years.

-

ASHTON HOTEL GROUP BACKGROUND AND BRIEF HISTORY Ashton Hotel Group (AHG) commenced operation in 1967, marking its entry into the bustling Sydney hotel market. Initially operating three hotels, AHG...

-

Question: What as the average weekly safety inventory level of refined sugar from the beginning January 2022 to the end of July 2022? A. 512,465.9691 metric tons per week B. 316,002.1474 metric tons...

-

Suppose that a client performs an intermixed sequence of push and pop operations on a pushdown stack. The push operations insert the integers 0 through 9 in order onto the stack; the pop operations...

-

Consider a 40-strike call with 91 days to expiration. Graph the results from the following calculations. a. Compute the actual price with 90 days to expiration at $1 intervals from $30 to $50. b....

-

Determine the speed of the boat with respect to the shore in Example 3-11.

-

Because of the complexity of human behavior, economists must _________ to focus on the most important components of a particular problem.

-

Under Section 11 of the Securities Act of 1933 and Section 10(b), Rule 10b-5, of the Securities Exchange Act of 1934, a CPA may be sued by a purchaser of registered securities. The following items...

-

Imagine that a researcher randomly selected 10 girls from a high school and measured their weights and heights and then calculated Body Mass Index (BMI). It is calculated by the weight in kg divided...

-

Jackson County Senior Services is a nonprofit organization devoted to providing essential services to seniors who live in their own homes within the Jackson County area. Three services are provided...

-

17. Which of the following is an active transport mechanism? a. Osmosis b. Facilitated diffusion c. Filtration d. Pinocytosis 18. Which of the following transport mechanisms transports water across...

-

Solve the system using either Gaussian elimination with back-substitution or Gauss-Jordan elimination. z, and w in terms of the parameters t and s.) 4x+12y7z - 20w = 28 3x + 9y5z28w = 36

-

Managing diversity is different from valuing diversity because it addresses the organizational processes that can reinforce - or hinder - the ability to establish an environment that values...

-

24. The compound that enters the Krebs cycle and combines with oxaloacetic acid is a. citric acid. b. pyruvic acid. c. acetyl-CoA. d. phosphoglyceraldehyde. 25. Formic acid is a fermentation product...

-

4. Bacterial replication is accomplished primarily by a. mitosis. b. meiosis. c. cytokinesis. d. binary fission. 5. Bacteria that use oxygen, but only at low concentration, are classified as a....

-

A medical researcher says that less than 80% of adults in a certain country think that healthy children should be required to be vaccinated. In a random sample of 600 adults in that country, 76%...

-

Banner Company acquires an 80% interest in Roller Company for $640,000 cash on January 1, 2013. The NCI has a fair value of $160,000. Any excess of cost over book value is attributed to goodwill. To...

-

What is a planning horizon? How will it differ between strategic planning and operational planning?

-

Which of the following budgets will typically have the longest budget period? a. Capital expenditures budget b. Cash budget c. Sales budget d. Budgeted income statement

-

Which of the following budgets should be prepared before all of the others listed below? a. Cash budget b. Direct materials budget c. Manufacturing overhead budget d. Production budget

Study smarter with the SolutionInn App