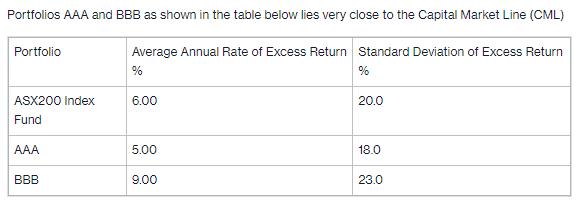

You are choosing one of the three portfolios by considering the Sharpe Ratio, Treynor Ration and Jensen-Alpha.

Question:

You are choosing one of the three portfolios by considering the Sharpe Ratio, Treynor Ration and Jensen-Alpha. Briefly discuss which one you would choose to optimise risk-adjusted return. Justify your choice by providing evidence using suitable performance measurement.

Briefly discuss two limitations of your choice.

In light of your answer in provide a better alternative portfolio evaluation index. Provide justifications for your choice.

You are going to combine portfolio AAA and portfolio BBB to form a portfolio CCC. Without doing any calculation, do you expect there will be any improvement in portfolio CCC in Sharpe Ratio, Treynor Ratio and Jensen-Alpha?

Expert Answer:

To optimize riskadjusted return among the given portfolios we can evaluate them using the Sharpe Ratio Treynor Ratio and Jensens Alpha 1 Sharpe Ratio ... View the full answer

Investment Analysis and Portfolio Management

ISBN: 978-1305262997

11th Edition

Authors: Frank K. Reilly, Keith C. Brown, Sanford J. Leeds