You are employed by an audit firm as audit assistant. You have been seconded to PJ...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

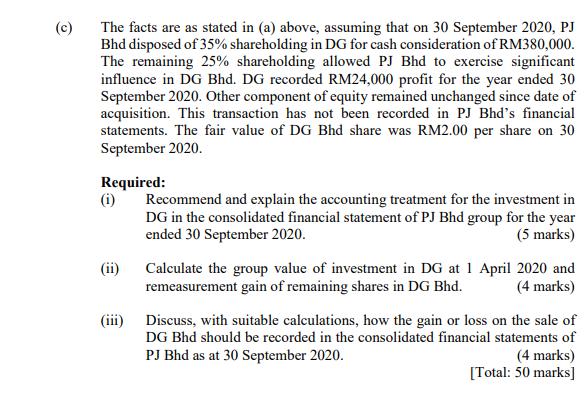

You are employed by an audit firm as audit assistant. You have been seconded to PJ Bhd, a trading and manufacturing company, to help with the preparation of their consolidated financial statements for the year ended 30 September 2020. At 1 October 2019, PJ Bhd had investments in two subsidiaries, KK Bhd and DG Bhd, as well as a number of other small investments. The draft summarised statements of financial position for PJ Bhd and its two subsidiaries at 30 September 2020 are shown below: PJ КК DG ASSETS RM RM RM Non-current assets 533,000 369,000 390,000 Property, plant and equipment Investments 554,000 Current assets Inventories 75,300 53,700 35,900 Trade and other receivables 98,600 39,600 29,000 5,400 2.700 2.300 Cash and cash equivalents Total assets 1.266.300 465.000 457,200 EQUITY AND LIABILITIES Equity Ordinary share capital 650,000 210,000 250,000 Other components of equity (OCE) 150,000 25,000 Retained earnings 132,300 147,000 123,000 Non-current liabilities Deferred consideration 121,000 Current liabilities 112,000 51,000 38,200 Trade and other payables Income tax 101,000 32.000 46.000 Total equity and liabilities 1.266.300 465.000 457.200 Number of ordinary shares 650,000 210,000 250,000 Additional information: (1) On 1 October 2019 PJ Bhd acquired 80% of KK Bhd for RM261,000 when KK Bhd's retained earnings were RM112,500. RM140,000 was paid immediately and the remaining RM121,000 is payable on 1 October 2021. The full RM261,000 was recognized by PJ Bhd as a non-current asset investment and a liability was set up for the deferred consideration. The fair values of KK Bhd's assets and liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, a contingent liability which had been reliably measured at a fair value of RM32,000 was disclosed, but not recognised, in KK Bhd's financial statements for the year ended 30 September 2020. This amount was subsequently settled at the estimated fair value. Question 1 (Continued) A reassessment of KK Bhd's assets, liabilities and consideration transferred took place following acquisition and no adjustments were necessary. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the fair value method. The fair value of the non-controlling interest in KK Bhd on 1 October 2019 was estimated at RM65,000. (2) PJ Bhd acquired 60% of DG Bhd on 1 October 2014 when DG Bhd's retained earnings were RM83,450. The consideration consisted of RM180,000 in cash paid at the date of acquisition and 50,000 newly issued RM1 ordinary shares in PJ Bhd. The market value of each share in PJ Bhd at 1 October 2014 was RM1.65. The issue of shares was correctly accounted for. The fair values of DG Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, DG Bhd has some internally generated brands which it does not recognise in its own financial statements. On 1 October 2014 these were valued by an independent expert at RM45,000 and were estimated as having an eight year useful life. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the proportionate method. (3) On 1 January 2020 PJ Bhd acquired a 25% shareholding in JNV Bhd, a joint venture, for RM28,000. The fair values of JNV Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. JNV Bhd's profit for the year ended 30 September 2020, accruing evenly over the year, was RM62,000. (4) In July 2020 PJ Bhd sold goods to JNV Bhd for RM10,000, earning a 15% gross margin. In addition, DG Bhd sold goods to KK Bhd for RM18,000 at a markup of 20%. At 30 September 2020 all of these goods were still held by both JNV Bhd and KK Bhd and the invoices remained unpaid. (5) PJ Bhd has undertaken its annual impairment review of goodwill and identified that an impairment of RM3,000 needs to be recognised at 30 September 2020 in relation to goodwill arising on the acquisition of DG Bhd. Cumulative impairments of goodwill arising on the acquisition of DG Bhd of RM5,000 were recognised at 30 September 2019. An appropriate discount rate is 10% pa. (6) On 30 September 2020, PJ acquired an additional 20% of the ordinary shares of DG from the non-controlling interest of DG for a cash consideration of RM80,000. PJ has not accounted for this in its books. (c) The facts are as stated in (a) above, assuming that on 30 September 2020, PJ Bhd disposed of 35% shareholding in DG for cash consideration of RM380,000. The remaining 25% shareholding allowed PJ Bhd to exercise significant influence in DG Bhd. DG recorded RM24,000 profit for the year ended 30 September 2020. Other component of equity remained unchanged since date of acquisition. This transaction has not been recorded in PJ Bhd's financial statements. The fair value of DG Bhd share was RM2.00 per share on 30 September 2020. Required: (i) Recommend and explain the accounting treatment for the investment in DG in the consolidated financial statement of PJ Bhd group for the year ended 30 September 2020. (5 marks) (ii) Calculate the group value of investment in DG at 1 April 2020 and remeasurement gain of remaining shares in DG Bhd. (4 marks) (iii) Discuss, with suitable calculations, how the gain or loss on the sale of DG Bhd should be recorded in the consolidated financial statements of PJ Bhd as at 30 September 2020. (4 marks) [Total: 50 marks] You are employed by an audit firm as audit assistant. You have been seconded to PJ Bhd, a trading and manufacturing company, to help with the preparation of their consolidated financial statements for the year ended 30 September 2020. At 1 October 2019, PJ Bhd had investments in two subsidiaries, KK Bhd and DG Bhd, as well as a number of other small investments. The draft summarised statements of financial position for PJ Bhd and its two subsidiaries at 30 September 2020 are shown below: PJ КК DG ASSETS RM RM RM Non-current assets 533,000 369,000 390,000 Property, plant and equipment Investments 554,000 Current assets Inventories 75,300 53,700 35,900 Trade and other receivables 98,600 39,600 29,000 5,400 2.700 2.300 Cash and cash equivalents Total assets 1.266.300 465.000 457,200 EQUITY AND LIABILITIES Equity Ordinary share capital 650,000 210,000 250,000 Other components of equity (OCE) 150,000 25,000 Retained earnings 132,300 147,000 123,000 Non-current liabilities Deferred consideration 121,000 Current liabilities 112,000 51,000 38,200 Trade and other payables Income tax 101,000 32.000 46.000 Total equity and liabilities 1.266.300 465.000 457.200 Number of ordinary shares 650,000 210,000 250,000 Additional information: (1) On 1 October 2019 PJ Bhd acquired 80% of KK Bhd for RM261,000 when KK Bhd's retained earnings were RM112,500. RM140,000 was paid immediately and the remaining RM121,000 is payable on 1 October 2021. The full RM261,000 was recognized by PJ Bhd as a non-current asset investment and a liability was set up for the deferred consideration. The fair values of KK Bhd's assets and liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, a contingent liability which had been reliably measured at a fair value of RM32,000 was disclosed, but not recognised, in KK Bhd's financial statements for the year ended 30 September 2020. This amount was subsequently settled at the estimated fair value. Question 1 (Continued) A reassessment of KK Bhd's assets, liabilities and consideration transferred took place following acquisition and no adjustments were necessary. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the fair value method. The fair value of the non-controlling interest in KK Bhd on 1 October 2019 was estimated at RM65,000. (2) PJ Bhd acquired 60% of DG Bhd on 1 October 2014 when DG Bhd's retained earnings were RM83,450. The consideration consisted of RM180,000 in cash paid at the date of acquisition and 50,000 newly issued RM1 ordinary shares in PJ Bhd. The market value of each share in PJ Bhd at 1 October 2014 was RM1.65. The issue of shares was correctly accounted for. The fair values of DG Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, DG Bhd has some internally generated brands which it does not recognise in its own financial statements. On 1 October 2014 these were valued by an independent expert at RM45,000 and were estimated as having an eight year useful life. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the proportionate method. (3) On 1 January 2020 PJ Bhd acquired a 25% shareholding in JNV Bhd, a joint venture, for RM28,000. The fair values of JNV Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. JNV Bhd's profit for the year ended 30 September 2020, accruing evenly over the year, was RM62,000. (4) In July 2020 PJ Bhd sold goods to JNV Bhd for RM10,000, earning a 15% gross margin. In addition, DG Bhd sold goods to KK Bhd for RM18,000 at a markup of 20%. At 30 September 2020 all of these goods were still held by both JNV Bhd and KK Bhd and the invoices remained unpaid. (5) PJ Bhd has undertaken its annual impairment review of goodwill and identified that an impairment of RM3,000 needs to be recognised at 30 September 2020 in relation to goodwill arising on the acquisition of DG Bhd. Cumulative impairments of goodwill arising on the acquisition of DG Bhd of RM5,000 were recognised at 30 September 2019. An appropriate discount rate is 10% pa. (6) On 30 September 2020, PJ acquired an additional 20% of the ordinary shares of DG from the non-controlling interest of DG for a cash consideration of RM80,000. PJ has not accounted for this in its books. (c) The facts are as stated in (a) above, assuming that on 30 September 2020, PJ Bhd disposed of 35% shareholding in DG for cash consideration of RM380,000. The remaining 25% shareholding allowed PJ Bhd to exercise significant influence in DG Bhd. DG recorded RM24,000 profit for the year ended 30 September 2020. Other component of equity remained unchanged since date of acquisition. This transaction has not been recorded in PJ Bhd's financial statements. The fair value of DG Bhd share was RM2.00 per share on 30 September 2020. Required: (i) Recommend and explain the accounting treatment for the investment in DG in the consolidated financial statement of PJ Bhd group for the year ended 30 September 2020. (5 marks) (ii) Calculate the group value of investment in DG at 1 April 2020 and remeasurement gain of remaining shares in DG Bhd. (4 marks) (iii) Discuss, with suitable calculations, how the gain or loss on the sale of DG Bhd should be recorded in the consolidated financial statements of PJ Bhd as at 30 September 2020. (4 marks) [Total: 50 marks] You are employed by an audit firm as audit assistant. You have been seconded to PJ Bhd, a trading and manufacturing company, to help with the preparation of their consolidated financial statements for the year ended 30 September 2020. At 1 October 2019, PJ Bhd had investments in two subsidiaries, KK Bhd and DG Bhd, as well as a number of other small investments. The draft summarised statements of financial position for PJ Bhd and its two subsidiaries at 30 September 2020 are shown below: PJ КК DG ASSETS RM RM RM Non-current assets 533,000 369,000 390,000 Property, plant and equipment Investments 554,000 Current assets Inventories 75,300 53,700 35,900 Trade and other receivables 98,600 39,600 29,000 5,400 2.700 2.300 Cash and cash equivalents Total assets 1.266.300 465.000 457,200 EQUITY AND LIABILITIES Equity Ordinary share capital 650,000 210,000 250,000 Other components of equity (OCE) 150,000 25,000 Retained earnings 132,300 147,000 123,000 Non-current liabilities Deferred consideration 121,000 Current liabilities 112,000 51,000 38,200 Trade and other payables Income tax 101,000 32.000 46.000 Total equity and liabilities 1.266.300 465.000 457.200 Number of ordinary shares 650,000 210,000 250,000 Additional information: (1) On 1 October 2019 PJ Bhd acquired 80% of KK Bhd for RM261,000 when KK Bhd's retained earnings were RM112,500. RM140,000 was paid immediately and the remaining RM121,000 is payable on 1 October 2021. The full RM261,000 was recognized by PJ Bhd as a non-current asset investment and a liability was set up for the deferred consideration. The fair values of KK Bhd's assets and liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, a contingent liability which had been reliably measured at a fair value of RM32,000 was disclosed, but not recognised, in KK Bhd's financial statements for the year ended 30 September 2020. This amount was subsequently settled at the estimated fair value. Question 1 (Continued) A reassessment of KK Bhd's assets, liabilities and consideration transferred took place following acquisition and no adjustments were necessary. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the fair value method. The fair value of the non-controlling interest in KK Bhd on 1 October 2019 was estimated at RM65,000. (2) PJ Bhd acquired 60% of DG Bhd on 1 October 2014 when DG Bhd's retained earnings were RM83,450. The consideration consisted of RM180,000 in cash paid at the date of acquisition and 50,000 newly issued RM1 ordinary shares in PJ Bhd. The market value of each share in PJ Bhd at 1 October 2014 was RM1.65. The issue of shares was correctly accounted for. The fair values of DG Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, DG Bhd has some internally generated brands which it does not recognise in its own financial statements. On 1 October 2014 these were valued by an independent expert at RM45,000 and were estimated as having an eight year useful life. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the proportionate method. (3) On 1 January 2020 PJ Bhd acquired a 25% shareholding in JNV Bhd, a joint venture, for RM28,000. The fair values of JNV Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. JNV Bhd's profit for the year ended 30 September 2020, accruing evenly over the year, was RM62,000. (4) In July 2020 PJ Bhd sold goods to JNV Bhd for RM10,000, earning a 15% gross margin. In addition, DG Bhd sold goods to KK Bhd for RM18,000 at a markup of 20%. At 30 September 2020 all of these goods were still held by both JNV Bhd and KK Bhd and the invoices remained unpaid. (5) PJ Bhd has undertaken its annual impairment review of goodwill and identified that an impairment of RM3,000 needs to be recognised at 30 September 2020 in relation to goodwill arising on the acquisition of DG Bhd. Cumulative impairments of goodwill arising on the acquisition of DG Bhd of RM5,000 were recognised at 30 September 2019. An appropriate discount rate is 10% pa. (6) On 30 September 2020, PJ acquired an additional 20% of the ordinary shares of DG from the non-controlling interest of DG for a cash consideration of RM80,000. PJ has not accounted for this in its books. (c) The facts are as stated in (a) above, assuming that on 30 September 2020, PJ Bhd disposed of 35% shareholding in DG for cash consideration of RM380,000. The remaining 25% shareholding allowed PJ Bhd to exercise significant influence in DG Bhd. DG recorded RM24,000 profit for the year ended 30 September 2020. Other component of equity remained unchanged since date of acquisition. This transaction has not been recorded in PJ Bhd's financial statements. The fair value of DG Bhd share was RM2.00 per share on 30 September 2020. Required: (i) Recommend and explain the accounting treatment for the investment in DG in the consolidated financial statement of PJ Bhd group for the year ended 30 September 2020. (5 marks) (ii) Calculate the group value of investment in DG at 1 April 2020 and remeasurement gain of remaining shares in DG Bhd. (4 marks) (iii) Discuss, with suitable calculations, how the gain or loss on the sale of DG Bhd should be recorded in the consolidated financial statements of PJ Bhd as at 30 September 2020. (4 marks) [Total: 50 marks] You are employed by an audit firm as audit assistant. You have been seconded to PJ Bhd, a trading and manufacturing company, to help with the preparation of their consolidated financial statements for the year ended 30 September 2020. At 1 October 2019, PJ Bhd had investments in two subsidiaries, KK Bhd and DG Bhd, as well as a number of other small investments. The draft summarised statements of financial position for PJ Bhd and its two subsidiaries at 30 September 2020 are shown below: PJ КК DG ASSETS RM RM RM Non-current assets 533,000 369,000 390,000 Property, plant and equipment Investments 554,000 Current assets Inventories 75,300 53,700 35,900 Trade and other receivables 98,600 39,600 29,000 5,400 2.700 2.300 Cash and cash equivalents Total assets 1.266.300 465.000 457,200 EQUITY AND LIABILITIES Equity Ordinary share capital 650,000 210,000 250,000 Other components of equity (OCE) 150,000 25,000 Retained earnings 132,300 147,000 123,000 Non-current liabilities Deferred consideration 121,000 Current liabilities 112,000 51,000 38,200 Trade and other payables Income tax 101,000 32.000 46.000 Total equity and liabilities 1.266.300 465.000 457.200 Number of ordinary shares 650,000 210,000 250,000 Additional information: (1) On 1 October 2019 PJ Bhd acquired 80% of KK Bhd for RM261,000 when KK Bhd's retained earnings were RM112,500. RM140,000 was paid immediately and the remaining RM121,000 is payable on 1 October 2021. The full RM261,000 was recognized by PJ Bhd as a non-current asset investment and a liability was set up for the deferred consideration. The fair values of KK Bhd's assets and liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, a contingent liability which had been reliably measured at a fair value of RM32,000 was disclosed, but not recognised, in KK Bhd's financial statements for the year ended 30 September 2020. This amount was subsequently settled at the estimated fair value. Question 1 (Continued) A reassessment of KK Bhd's assets, liabilities and consideration transferred took place following acquisition and no adjustments were necessary. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the fair value method. The fair value of the non-controlling interest in KK Bhd on 1 October 2019 was estimated at RM65,000. (2) PJ Bhd acquired 60% of DG Bhd on 1 October 2014 when DG Bhd's retained earnings were RM83,450. The consideration consisted of RM180,000 in cash paid at the date of acquisition and 50,000 newly issued RM1 ordinary shares in PJ Bhd. The market value of each share in PJ Bhd at 1 October 2014 was RM1.65. The issue of shares was correctly accounted for. The fair values of DG Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, DG Bhd has some internally generated brands which it does not recognise in its own financial statements. On 1 October 2014 these were valued by an independent expert at RM45,000 and were estimated as having an eight year useful life. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the proportionate method. (3) On 1 January 2020 PJ Bhd acquired a 25% shareholding in JNV Bhd, a joint venture, for RM28,000. The fair values of JNV Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. JNV Bhd's profit for the year ended 30 September 2020, accruing evenly over the year, was RM62,000. (4) In July 2020 PJ Bhd sold goods to JNV Bhd for RM10,000, earning a 15% gross margin. In addition, DG Bhd sold goods to KK Bhd for RM18,000 at a markup of 20%. At 30 September 2020 all of these goods were still held by both JNV Bhd and KK Bhd and the invoices remained unpaid. (5) PJ Bhd has undertaken its annual impairment review of goodwill and identified that an impairment of RM3,000 needs to be recognised at 30 September 2020 in relation to goodwill arising on the acquisition of DG Bhd. Cumulative impairments of goodwill arising on the acquisition of DG Bhd of RM5,000 were recognised at 30 September 2019. An appropriate discount rate is 10% pa. (6) On 30 September 2020, PJ acquired an additional 20% of the ordinary shares of DG from the non-controlling interest of DG for a cash consideration of RM80,000. PJ has not accounted for this in its books. (c) The facts are as stated in (a) above, assuming that on 30 September 2020, PJ Bhd disposed of 35% shareholding in DG for cash consideration of RM380,000. The remaining 25% shareholding allowed PJ Bhd to exercise significant influence in DG Bhd. DG recorded RM24,000 profit for the year ended 30 September 2020. Other component of equity remained unchanged since date of acquisition. This transaction has not been recorded in PJ Bhd's financial statements. The fair value of DG Bhd share was RM2.00 per share on 30 September 2020. Required: (i) Recommend and explain the accounting treatment for the investment in DG in the consolidated financial statement of PJ Bhd group for the year ended 30 September 2020. (5 marks) (ii) Calculate the group value of investment in DG at 1 April 2020 and remeasurement gain of remaining shares in DG Bhd. (4 marks) (iii) Discuss, with suitable calculations, how the gain or loss on the sale of DG Bhd should be recorded in the consolidated financial statements of PJ Bhd as at 30 September 2020. (4 marks) [Total: 50 marks] You are employed by an audit firm as audit assistant. You have been seconded to PJ Bhd, a trading and manufacturing company, to help with the preparation of their consolidated financial statements for the year ended 30 September 2020. At 1 October 2019, PJ Bhd had investments in two subsidiaries, KK Bhd and DG Bhd, as well as a number of other small investments. The draft summarised statements of financial position for PJ Bhd and its two subsidiaries at 30 September 2020 are shown below: PJ КК DG ASSETS RM RM RM Non-current assets 533,000 369,000 390,000 Property, plant and equipment Investments 554,000 Current assets Inventories 75,300 53,700 35,900 Trade and other receivables 98,600 39,600 29,000 5,400 2.700 2.300 Cash and cash equivalents Total assets 1.266.300 465.000 457,200 EQUITY AND LIABILITIES Equity Ordinary share capital 650,000 210,000 250,000 Other components of equity (OCE) 150,000 25,000 Retained earnings 132,300 147,000 123,000 Non-current liabilities Deferred consideration 121,000 Current liabilities 112,000 51,000 38,200 Trade and other payables Income tax 101,000 32.000 46.000 Total equity and liabilities 1.266.300 465.000 457.200 Number of ordinary shares 650,000 210,000 250,000 Additional information: (1) On 1 October 2019 PJ Bhd acquired 80% of KK Bhd for RM261,000 when KK Bhd's retained earnings were RM112,500. RM140,000 was paid immediately and the remaining RM121,000 is payable on 1 October 2021. The full RM261,000 was recognized by PJ Bhd as a non-current asset investment and a liability was set up for the deferred consideration. The fair values of KK Bhd's assets and liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, a contingent liability which had been reliably measured at a fair value of RM32,000 was disclosed, but not recognised, in KK Bhd's financial statements for the year ended 30 September 2020. This amount was subsequently settled at the estimated fair value. Question 1 (Continued) A reassessment of KK Bhd's assets, liabilities and consideration transferred took place following acquisition and no adjustments were necessary. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the fair value method. The fair value of the non-controlling interest in KK Bhd on 1 October 2019 was estimated at RM65,000. (2) PJ Bhd acquired 60% of DG Bhd on 1 October 2014 when DG Bhd's retained earnings were RM83,450. The consideration consisted of RM180,000 in cash paid at the date of acquisition and 50,000 newly issued RM1 ordinary shares in PJ Bhd. The market value of each share in PJ Bhd at 1 October 2014 was RM1.65. The issue of shares was correctly accounted for. The fair values of DG Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, DG Bhd has some internally generated brands which it does not recognise in its own financial statements. On 1 October 2014 these were valued by an independent expert at RM45,000 and were estimated as having an eight year useful life. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the proportionate method. (3) On 1 January 2020 PJ Bhd acquired a 25% shareholding in JNV Bhd, a joint venture, for RM28,000. The fair values of JNV Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. JNV Bhd's profit for the year ended 30 September 2020, accruing evenly over the year, was RM62,000. (4) In July 2020 PJ Bhd sold goods to JNV Bhd for RM10,000, earning a 15% gross margin. In addition, DG Bhd sold goods to KK Bhd for RM18,000 at a markup of 20%. At 30 September 2020 all of these goods were still held by both JNV Bhd and KK Bhd and the invoices remained unpaid. (5) PJ Bhd has undertaken its annual impairment review of goodwill and identified that an impairment of RM3,000 needs to be recognised at 30 September 2020 in relation to goodwill arising on the acquisition of DG Bhd. Cumulative impairments of goodwill arising on the acquisition of DG Bhd of RM5,000 were recognised at 30 September 2019. An appropriate discount rate is 10% pa. (6) On 30 September 2020, PJ acquired an additional 20% of the ordinary shares of DG from the non-controlling interest of DG for a cash consideration of RM80,000. PJ has not accounted for this in its books. (c) The facts are as stated in (a) above, assuming that on 30 September 2020, PJ Bhd disposed of 35% shareholding in DG for cash consideration of RM380,000. The remaining 25% shareholding allowed PJ Bhd to exercise significant influence in DG Bhd. DG recorded RM24,000 profit for the year ended 30 September 2020. Other component of equity remained unchanged since date of acquisition. This transaction has not been recorded in PJ Bhd's financial statements. The fair value of DG Bhd share was RM2.00 per share on 30 September 2020. Required: (i) Recommend and explain the accounting treatment for the investment in DG in the consolidated financial statement of PJ Bhd group for the year ended 30 September 2020. (5 marks) (ii) Calculate the group value of investment in DG at 1 April 2020 and remeasurement gain of remaining shares in DG Bhd. (4 marks) (iii) Discuss, with suitable calculations, how the gain or loss on the sale of DG Bhd should be recorded in the consolidated financial statements of PJ Bhd as at 30 September 2020. (4 marks) [Total: 50 marks] You are employed by an audit firm as audit assistant. You have been seconded to PJ Bhd, a trading and manufacturing company, to help with the preparation of their consolidated financial statements for the year ended 30 September 2020. At 1 October 2019, PJ Bhd had investments in two subsidiaries, KK Bhd and DG Bhd, as well as a number of other small investments. The draft summarised statements of financial position for PJ Bhd and its two subsidiaries at 30 September 2020 are shown below: PJ КК DG ASSETS RM RM RM Non-current assets 533,000 369,000 390,000 Property, plant and equipment Investments 554,000 Current assets Inventories 75,300 53,700 35,900 Trade and other receivables 98,600 39,600 29,000 5,400 2.700 2.300 Cash and cash equivalents Total assets 1.266.300 465.000 457,200 EQUITY AND LIABILITIES Equity Ordinary share capital 650,000 210,000 250,000 Other components of equity (OCE) 150,000 25,000 Retained earnings 132,300 147,000 123,000 Non-current liabilities Deferred consideration 121,000 Current liabilities 112,000 51,000 38,200 Trade and other payables Income tax 101,000 32.000 46.000 Total equity and liabilities 1.266.300 465.000 457.200 Number of ordinary shares 650,000 210,000 250,000 Additional information: (1) On 1 October 2019 PJ Bhd acquired 80% of KK Bhd for RM261,000 when KK Bhd's retained earnings were RM112,500. RM140,000 was paid immediately and the remaining RM121,000 is payable on 1 October 2021. The full RM261,000 was recognized by PJ Bhd as a non-current asset investment and a liability was set up for the deferred consideration. The fair values of KK Bhd's assets and liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, a contingent liability which had been reliably measured at a fair value of RM32,000 was disclosed, but not recognised, in KK Bhd's financial statements for the year ended 30 September 2020. This amount was subsequently settled at the estimated fair value. Question 1 (Continued) A reassessment of KK Bhd's assets, liabilities and consideration transferred took place following acquisition and no adjustments were necessary. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the fair value method. The fair value of the non-controlling interest in KK Bhd on 1 October 2019 was estimated at RM65,000. (2) PJ Bhd acquired 60% of DG Bhd on 1 October 2014 when DG Bhd's retained earnings were RM83,450. The consideration consisted of RM180,000 in cash paid at the date of acquisition and 50,000 newly issued RM1 ordinary shares in PJ Bhd. The market value of each share in PJ Bhd at 1 October 2014 was RM1.65. The issue of shares was correctly accounted for. The fair values of DG Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, DG Bhd has some internally generated brands which it does not recognise in its own financial statements. On 1 October 2014 these were valued by an independent expert at RM45,000 and were estimated as having an eight year useful life. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the proportionate method. (3) On 1 January 2020 PJ Bhd acquired a 25% shareholding in JNV Bhd, a joint venture, for RM28,000. The fair values of JNV Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. JNV Bhd's profit for the year ended 30 September 2020, accruing evenly over the year, was RM62,000. (4) In July 2020 PJ Bhd sold goods to JNV Bhd for RM10,000, earning a 15% gross margin. In addition, DG Bhd sold goods to KK Bhd for RM18,000 at a markup of 20%. At 30 September 2020 all of these goods were still held by both JNV Bhd and KK Bhd and the invoices remained unpaid. (5) PJ Bhd has undertaken its annual impairment review of goodwill and identified that an impairment of RM3,000 needs to be recognised at 30 September 2020 in relation to goodwill arising on the acquisition of DG Bhd. Cumulative impairments of goodwill arising on the acquisition of DG Bhd of RM5,000 were recognised at 30 September 2019. An appropriate discount rate is 10% pa. (6) On 30 September 2020, PJ acquired an additional 20% of the ordinary shares of DG from the non-controlling interest of DG for a cash consideration of RM80,000. PJ has not accounted for this in its books. (c) The facts are as stated in (a) above, assuming that on 30 September 2020, PJ Bhd disposed of 35% shareholding in DG for cash consideration of RM380,000. The remaining 25% shareholding allowed PJ Bhd to exercise significant influence in DG Bhd. DG recorded RM24,000 profit for the year ended 30 September 2020. Other component of equity remained unchanged since date of acquisition. This transaction has not been recorded in PJ Bhd's financial statements. The fair value of DG Bhd share was RM2.00 per share on 30 September 2020. Required: (i) Recommend and explain the accounting treatment for the investment in DG in the consolidated financial statement of PJ Bhd group for the year ended 30 September 2020. (5 marks) (ii) Calculate the group value of investment in DG at 1 April 2020 and remeasurement gain of remaining shares in DG Bhd. (4 marks) (iii) Discuss, with suitable calculations, how the gain or loss on the sale of DG Bhd should be recorded in the consolidated financial statements of PJ Bhd as at 30 September 2020. (4 marks) [Total: 50 marks] You are employed by an audit firm as audit assistant. You have been seconded to PJ Bhd, a trading and manufacturing company, to help with the preparation of their consolidated financial statements for the year ended 30 September 2020. At 1 October 2019, PJ Bhd had investments in two subsidiaries, KK Bhd and DG Bhd, as well as a number of other small investments. The draft summarised statements of financial position for PJ Bhd and its two subsidiaries at 30 September 2020 are shown below: PJ КК DG ASSETS RM RM RM Non-current assets 533,000 369,000 390,000 Property, plant and equipment Investments 554,000 Current assets Inventories 75,300 53,700 35,900 Trade and other receivables 98,600 39,600 29,000 5,400 2.700 2.300 Cash and cash equivalents Total assets 1.266.300 465.000 457,200 EQUITY AND LIABILITIES Equity Ordinary share capital 650,000 210,000 250,000 Other components of equity (OCE) 150,000 25,000 Retained earnings 132,300 147,000 123,000 Non-current liabilities Deferred consideration 121,000 Current liabilities 112,000 51,000 38,200 Trade and other payables Income tax 101,000 32.000 46.000 Total equity and liabilities 1.266.300 465.000 457.200 Number of ordinary shares 650,000 210,000 250,000 Additional information: (1) On 1 October 2019 PJ Bhd acquired 80% of KK Bhd for RM261,000 when KK Bhd's retained earnings were RM112,500. RM140,000 was paid immediately and the remaining RM121,000 is payable on 1 October 2021. The full RM261,000 was recognized by PJ Bhd as a non-current asset investment and a liability was set up for the deferred consideration. The fair values of KK Bhd's assets and liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, a contingent liability which had been reliably measured at a fair value of RM32,000 was disclosed, but not recognised, in KK Bhd's financial statements for the year ended 30 September 2020. This amount was subsequently settled at the estimated fair value. Question 1 (Continued) A reassessment of KK Bhd's assets, liabilities and consideration transferred took place following acquisition and no adjustments were necessary. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the fair value method. The fair value of the non-controlling interest in KK Bhd on 1 October 2019 was estimated at RM65,000. (2) PJ Bhd acquired 60% of DG Bhd on 1 October 2014 when DG Bhd's retained earnings were RM83,450. The consideration consisted of RM180,000 in cash paid at the date of acquisition and 50,000 newly issued RM1 ordinary shares in PJ Bhd. The market value of each share in PJ Bhd at 1 October 2014 was RM1.65. The issue of shares was correctly accounted for. The fair values of DG Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, DG Bhd has some internally generated brands which it does not recognise in its own financial statements. On 1 October 2014 these were valued by an independent expert at RM45,000 and were estimated as having an eight year useful life. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the proportionate method. (3) On 1 January 2020 PJ Bhd acquired a 25% shareholding in JNV Bhd, a joint venture, for RM28,000. The fair values of JNV Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. JNV Bhd's profit for the year ended 30 September 2020, accruing evenly over the year, was RM62,000. (4) In July 2020 PJ Bhd sold goods to JNV Bhd for RM10,000, earning a 15% gross margin. In addition, DG Bhd sold goods to KK Bhd for RM18,000 at a markup of 20%. At 30 September 2020 all of these goods were still held by both JNV Bhd and KK Bhd and the invoices remained unpaid. (5) PJ Bhd has undertaken its annual impairment review of goodwill and identified that an impairment of RM3,000 needs to be recognised at 30 September 2020 in relation to goodwill arising on the acquisition of DG Bhd. Cumulative impairments of goodwill arising on the acquisition of DG Bhd of RM5,000 were recognised at 30 September 2019. An appropriate discount rate is 10% pa. (6) On 30 September 2020, PJ acquired an additional 20% of the ordinary shares of DG from the non-controlling interest of DG for a cash consideration of RM80,000. PJ has not accounted for this in its books. (c) The facts are as stated in (a) above, assuming that on 30 September 2020, PJ Bhd disposed of 35% shareholding in DG for cash consideration of RM380,000. The remaining 25% shareholding allowed PJ Bhd to exercise significant influence in DG Bhd. DG recorded RM24,000 profit for the year ended 30 September 2020. Other component of equity remained unchanged since date of acquisition. This transaction has not been recorded in PJ Bhd's financial statements. The fair value of DG Bhd share was RM2.00 per share on 30 September 2020. Required: (i) Recommend and explain the accounting treatment for the investment in DG in the consolidated financial statement of PJ Bhd group for the year ended 30 September 2020. (5 marks) (ii) Calculate the group value of investment in DG at 1 April 2020 and remeasurement gain of remaining shares in DG Bhd. (4 marks) (iii) Discuss, with suitable calculations, how the gain or loss on the sale of DG Bhd should be recorded in the consolidated financial statements of PJ Bhd as at 30 September 2020. (4 marks) [Total: 50 marks] You are employed by an audit firm as audit assistant. You have been seconded to PJ Bhd, a trading and manufacturing company, to help with the preparation of their consolidated financial statements for the year ended 30 September 2020. At 1 October 2019, PJ Bhd had investments in two subsidiaries, KK Bhd and DG Bhd, as well as a number of other small investments. The draft summarised statements of financial position for PJ Bhd and its two subsidiaries at 30 September 2020 are shown below: PJ КК DG ASSETS RM RM RM Non-current assets 533,000 369,000 390,000 Property, plant and equipment Investments 554,000 Current assets Inventories 75,300 53,700 35,900 Trade and other receivables 98,600 39,600 29,000 5,400 2.700 2.300 Cash and cash equivalents Total assets 1.266.300 465.000 457,200 EQUITY AND LIABILITIES Equity Ordinary share capital 650,000 210,000 250,000 Other components of equity (OCE) 150,000 25,000 Retained earnings 132,300 147,000 123,000 Non-current liabilities Deferred consideration 121,000 Current liabilities 112,000 51,000 38,200 Trade and other payables Income tax 101,000 32.000 46.000 Total equity and liabilities 1.266.300 465.000 457.200 Number of ordinary shares 650,000 210,000 250,000 Additional information: (1) On 1 October 2019 PJ Bhd acquired 80% of KK Bhd for RM261,000 when KK Bhd's retained earnings were RM112,500. RM140,000 was paid immediately and the remaining RM121,000 is payable on 1 October 2021. The full RM261,000 was recognized by PJ Bhd as a non-current asset investment and a liability was set up for the deferred consideration. The fair values of KK Bhd's assets and liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, a contingent liability which had been reliably measured at a fair value of RM32,000 was disclosed, but not recognised, in KK Bhd's financial statements for the year ended 30 September 2020. This amount was subsequently settled at the estimated fair value. Question 1 (Continued) A reassessment of KK Bhd's assets, liabilities and consideration transferred took place following acquisition and no adjustments were necessary. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the fair value method. The fair value of the non-controlling interest in KK Bhd on 1 October 2019 was estimated at RM65,000. (2) PJ Bhd acquired 60% of DG Bhd on 1 October 2014 when DG Bhd's retained earnings were RM83,450. The consideration consisted of RM180,000 in cash paid at the date of acquisition and 50,000 newly issued RM1 ordinary shares in PJ Bhd. The market value of each share in PJ Bhd at 1 October 2014 was RM1.65. The issue of shares was correctly accounted for. The fair values of DG Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. In addition, DG Bhd has some internally generated brands which it does not recognise in its own financial statements. On 1 October 2014 these were valued by an independent expert at RM45,000 and were estimated as having an eight year useful life. PJ Bhd recognised the goodwill and non-controlling interest on this acquisition using the proportionate method. (3) On 1 January 2020 PJ Bhd acquired a 25% shareholding in JNV Bhd, a joint venture, for RM28,000. The fair values of JNV Bhd's assets, liabilities and contingent liabilities at the date of acquisition by PJ Bhd were equal to their carrying amounts. JNV Bhd's profit for the year ended 30 September 2020, accruing evenly over the year, was RM62,000. (4) In July 2020 PJ Bhd sold goods to JNV Bhd for RM10,000, earning a 15% gross margin. In addition, DG Bhd sold goods to KK Bhd for RM18,000 at a markup of 20%. At 30 September 2020 all of these goods were still held by both JNV Bhd and KK Bhd and the invoices remained unpaid. (5) PJ Bhd has undertaken its annual impairment review of goodwill and identified that an impairment of RM3,000 needs to be recognised at 30 September 2020 in relation to goodwill arising on the acquisition of DG Bhd. Cumulative impairments of goodwill arising on the acquisition of DG Bhd of RM5,000 were recognised at 30 September 2019. An appropriate discount rate is 10% pa. (6) On 30 September 2020, PJ acquired an additional 20% of the ordinary shares of DG from the non-controlling interest of DG for a cash consideration of RM80,000. PJ has not accounted for this in its books. (c) The facts are as stated in (a) above, assuming that on 30 September 2020, PJ Bhd disposed of 35% shareholding in DG for cash consideration of RM380,000. The remaining 25% shareholding allowed PJ Bhd to exercise significant influence in DG Bhd. DG recorded RM24,000 profit for the year ended 30 September 2020. Other component of equity remained unchanged since date of acquisition. This transaction has not been recorded in PJ Bhd's financial statements. The fair value of DG Bhd share was RM2.00 per share on 30 September 2020. Required: (i) Recommend and explain the accounting treatment for the investment in DG in the consolidated financial statement of PJ Bhd group for the year ended 30 September 2020. (5 marks) (ii) Calculate the group value of investment in DG at 1 April 2020 and remeasurement gain of remaining shares in DG Bhd. (4 marks) (iii) Discuss, with suitable calculations, how the gain or loss on the sale of DG Bhd should be recorded in the consolidated financial statements of PJ Bhd as at 30 September 2020. (4 marks) [Total: 50 marks]

Expert Answer:

Answer rating: 100% (QA)

i The accounting treatment for the investment in DG On 1 Oct 2012 PJ acquired 60 equity interest in ... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

You have been recently employed by an audit firm You are to understudy and assist one of the experienced partners in the audit firm to conduct an audit of a client with whom they have recently signed...

-

In preparing the financial statements for the year ended 30 June 2018 the accountant of Windsor Ltd, a tobacco manufacturer and wholesaler, has come to you with the following information and request...

-

The Magna International Inc. financial statements for the year ended December 31, 2011, can be found on SEDAR (www.sedar.com). Instructions (a) The company has many different types of shares...

-

THE iterative software development method. Just read the case thoroughly and answer the below-mentioned 3 questions. Here are the three questions to be answered: 1. What are the two choices Lalonde...

-

Winfield Co. has 1,000 units in process in Forming at the beginning of the month with a transferred cost of $21,200 from Blanking. During the month, 5,000 units with a total cost of $100,000 are...

-

Ms. Ray is age 46 and single. Her employer made a $2,895 contribution to her qualified profit-sharing plan account, and she made the maximum contribution to her traditional IRA. Compute her IRA...

-

A fractional extraction system (Figure 13-5) is separating abietic acid from other acids. Solvent 1 , heptane, enters at \(\mathrm{E}-=1000 \mathrm{~kg} / \mathrm{h}\) and is pure. Solvent 2,...

-

Jane has just been appointed as purchasing manager of Tacoma Technologies Corp. The previous purchasing manager, who recently retired, was known for his winner-take-all approach to suppliers. He...

-

Here is a case where the police were actually sued: Castle Rock v. Gonzales , 545 U.S. 748 (2005). Tell us about the case. Why were the police sued? Did the plaintiff win? What is the rationale for...

-

An older man has just lost his job after repeated warnings to come to work sober and seek help for his alcohol addiction. He has decided that he should get help now. Too little, too late, he says...

-

In the dynamic and expanding urban environment of "Slothsberg", a new highway ("Snailpace Highway") is to be constructed over the existing "Dillydally Highway". The following conditions apply to the...

-

Michele has undertaken an inventory of the electrical appliances throughout her business and discovers that some require cleaning and repair. Michele takes the appliances to Rolando the repairer,...

-

Using accrual accounting rules, ABC Co . delivers $ 1 , 0 0 0 worth of window washing services in January 2 0 2 2 and bills the client, who pays for the services in February 2 0 2 2 . How much in...

-

How should an employer considered the personal needs and development of employees when creating messaging? Supported your response by using a scholarly source(s) .

-

Explain the difference between journaling file systems and non-journaling file systems. What are the benefits and trade-offs of each approach in terms of data integrity and performance ?

-

On January 1, 2022, ABC Company purchased 1,000 of ZYX Company's common shares (15% of common shares outstanding) for $4,000, and paid transaction costs of $400. On February 1, 2022, ZYX paid a...

-

Suppose a textual representation of an HTA description of vacuum cleaning. Present the same information in a diagrammatic form. What is speech act theory? Describe positive and negative issues that...

-

Complete the following acid-base reactions: (a) HCCH + NaH

-

Dudas Inc. sold a division of its business in 2017. Pertinent details follow: Required: Prepare the journal entry to record the sale of the assets assuming that Dudas Inc. uses the net method to...

-

Hinton Property Management Company (HPMC) owns several properties that it rents to major hotel chains such as The Westin and Holiday Inn. HPMC does not operate the hotels but instead simply provides...

-

You are employed by McDowell and Partners, Chartered Accountants (M&P). A new client, Community Finance Corporation (CFC), approached M&P for assistance. Enviro Ltd. (Enviro) has asked CFC for a loan...

-

This question considers the impact of different degrees of truncation in the Tobit model. (a) Generate 200 draws of a latent variable y = k + 3 x + u , where u N [ 0 , 3 ] and the regressor x ...

-

Consider a latent variable modeled by y i = x i + i with i N [ 0 , 2 ] . Suppose y i is censored from above so that we observe y i = y i if y i < U i and y i = U i if y i U i , where the...

-

Suppose \(y=\mathbf{x}^{\prime} \boldsymbol{\beta}+u\), where \(u \sim \mathcal{N}\left[0, \sigma^{2} ight]\), with parameter vector \(\theta=\left[\boldsymbol{\beta}^{\prime}, \sigma^{2}...

Study smarter with the SolutionInn App