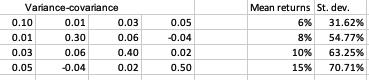

You are given the variance-covariance for four assets, their returns and standard deviations. Perform the following analysis.

Fantastic news! We've Found the answer you've been seeking!

Question:

You are given the variance-covariance for four assets, their returns and standard deviations. Perform the following analysis.

a. For constant c = 0 and c = 0.05, find the efficient portfolios for each case;

b. Let the efficient portfolio for c = 0 as portfolio 1 and the other as portfolio 2, use Data Table to find the efficient frontier for portfolio 1 weight ranging from -1.4 to 2.85 with 0.25 increment;

c. Impose no short sale on portfolio 2. Find the efficient frontier with no short sale;

Data for this question:

Expert Answer:

Related Book For

Fundamentals of Investments Valuation and Management

ISBN: 978-0077283292

5th edition

Authors: Bradford D. Jordan, Thomas W. Miller

Posted Date: