Question: You are going to create a portfolio which is a combination of the stock Zelda Corp, and a treasury bill. The rate on the treasury

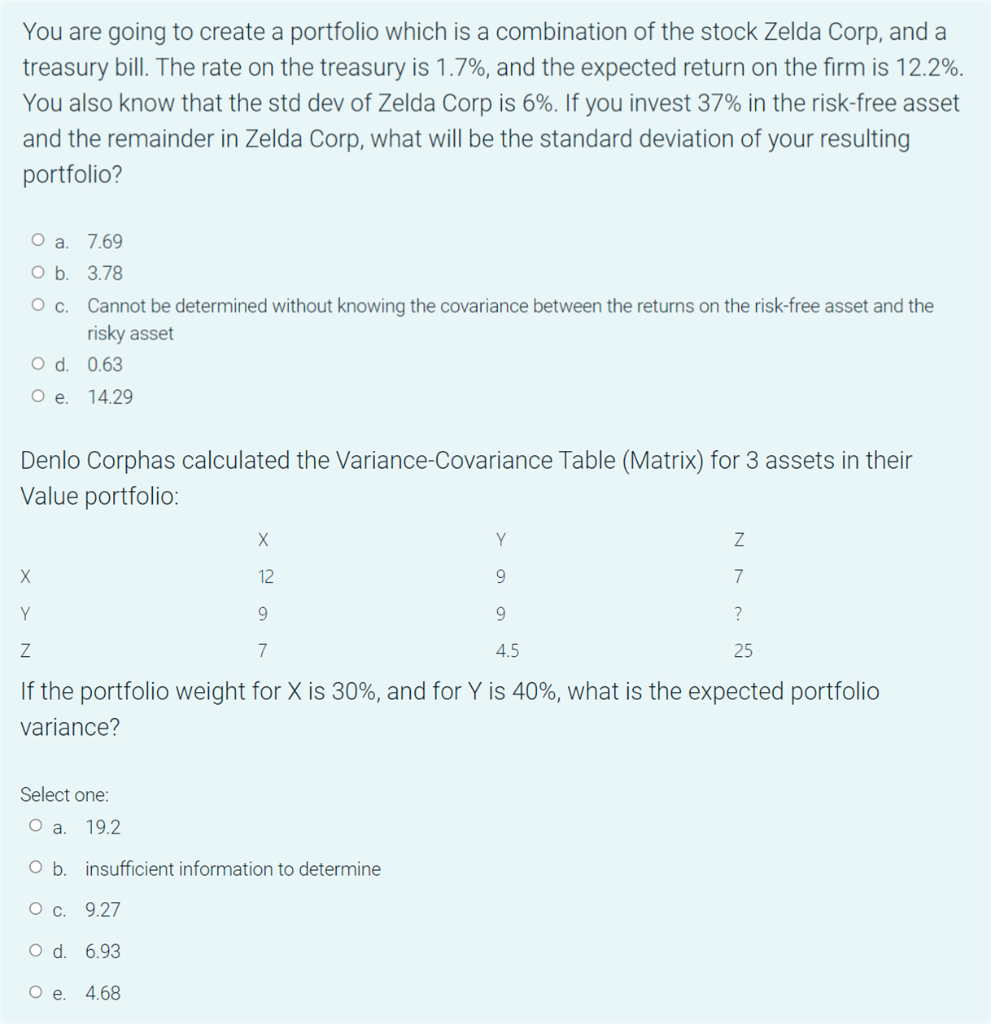

You are going to create a portfolio which is a combination of the stock Zelda Corp, and a treasury bill. The rate on the treasury is 1.7%, and the expected return on the firm is 12.2%. You also know that the std dev of Zelda Corp is 6%. If you invest 37% in the risk-free asset and the remainder in Zelda Corp, what will be the standard deviation of your resulting portfolio? O a. 7.69 O b. 3.78 O c. Cannot be determined without knowing the covariance between the returns on the risk-free asset and the risky asset Od 0.63 O e. 14.29 Matrix) for 3 assets in their Denlo Corphas calculated the Variance-Covariance Table Value portfolio: X Y Z X 12 9 7 Y 9 9 ? z 7 4.5 25 If the portfolio weight for X is 30%, and for Y is 40%, what is the expected portfolio variance? Select one: 19.2 . O b. insufficient information to determine O c. 9.27 O d. 6.93 O e. 4.68

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts