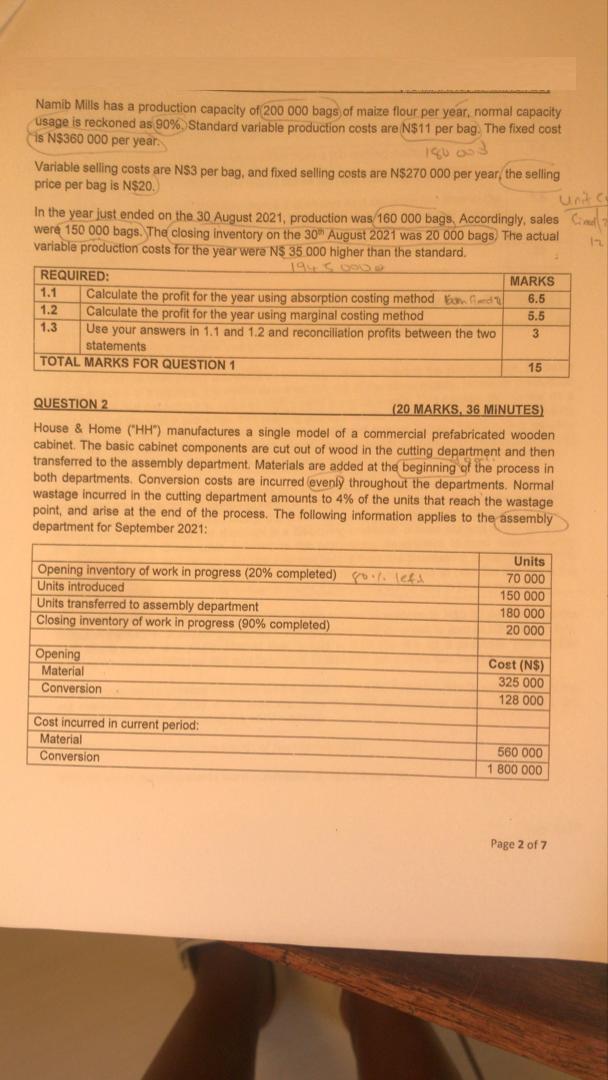

Namib Mills has a production capacity of 200 000 bags of maize flour per year, normal...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

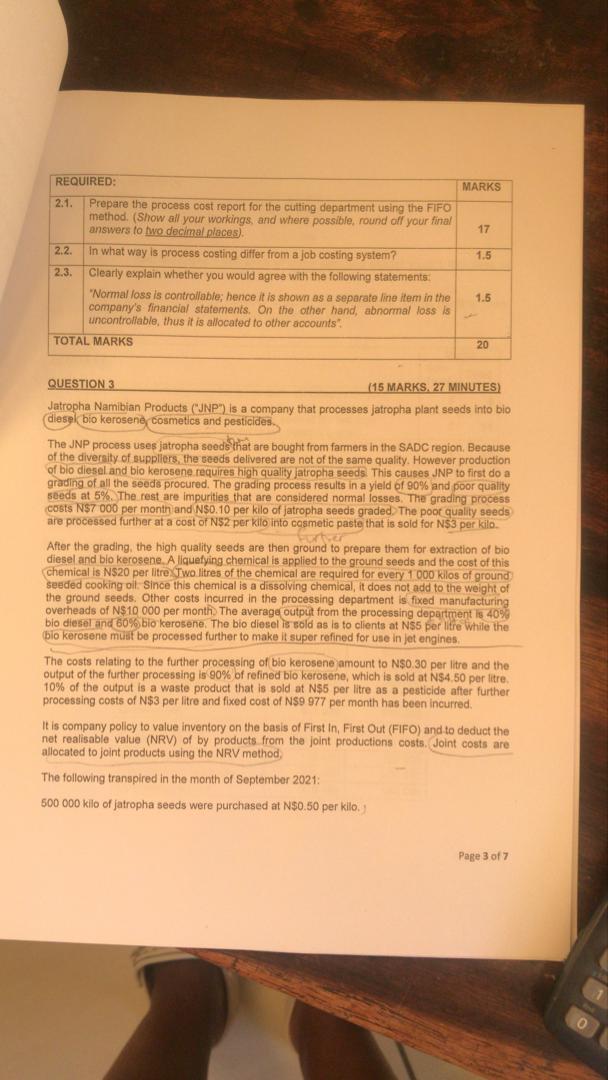

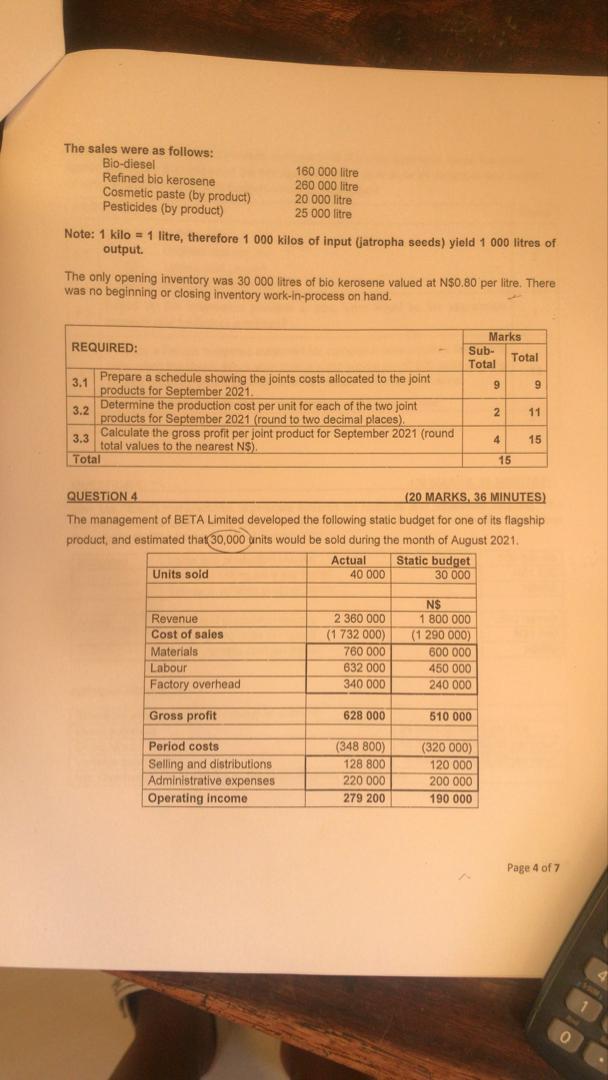

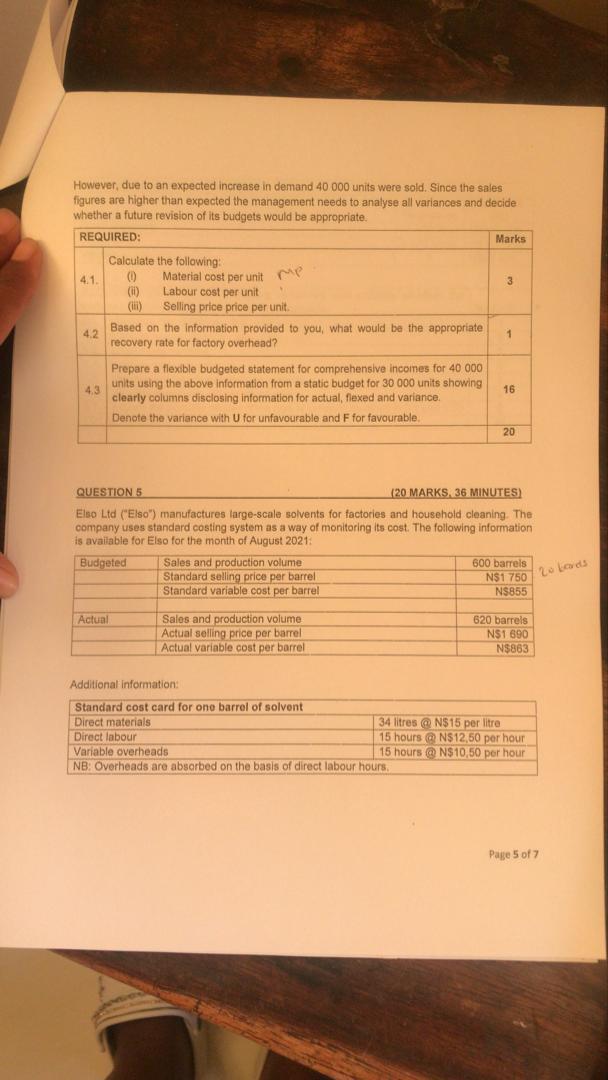

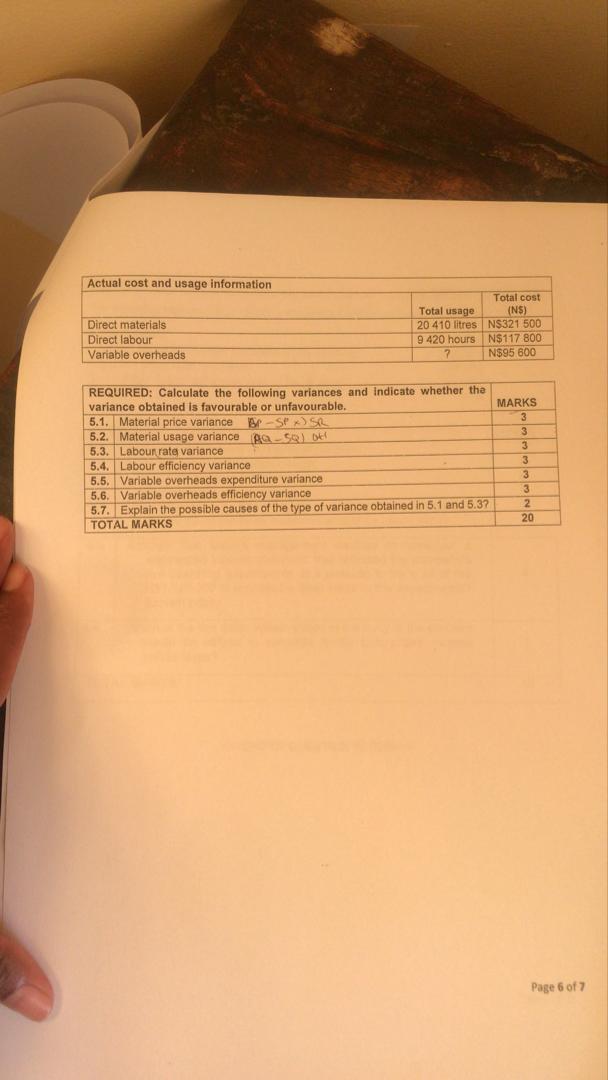

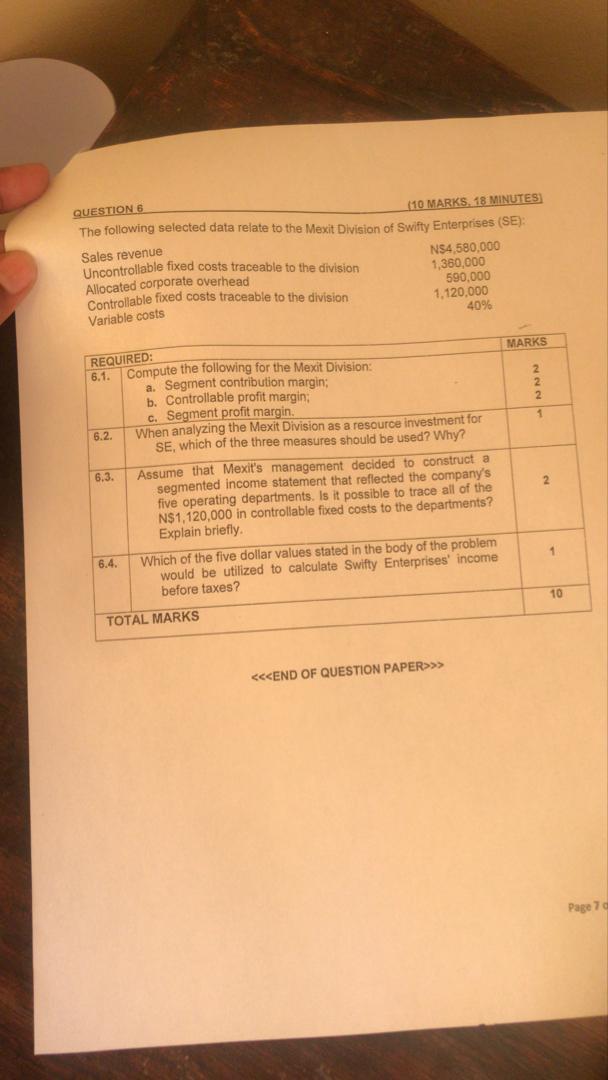

Namib Mills has a production capacity of 200 000 bags of maize flour per year, normal capacity usage is reckoned as 90% Standard variable production costs are N$11 per bag. The fixed cost is N$360 000 per year. 18083 Variable selling costs are NS3 per bag, and fixed selling costs are N$270 000 per year, the selling price per bag is N$20.) Unit ca In the year just ended on the 30 August 2021, production was 160 000 bags, Accordingly, sales C2 were 150 000 bags. The closing inventory on the 30th August 2021 was 20 000 bags. The actual variable production costs for the year were N$ 35 000 higher than the standard. 17 REQUIRED: Calculate the profit for the year using absorption costing method to find Calculate the profit for the year using marginal costing method Use your answers in 1.1 and 1.2 and reconciliation profits between the two statements TOTAL MARKS FOR QUESTION 1 1.1 1.2 1.3 Opening inventory of work in progress (20% completed) go.. left Units introduced Units transferred to assembly department Closing inventory of work in progress (90% completed) QUESTION 2 (20 MARKS, 36 MINUTES) House & Home (HH") manufactures a single model of a commercial prefabricated wooden cabinet. The basic cabinet components are cut out of wood in the cutting department and then transferred to the assembly department. Materials are added at the beginning of the process in both departments. Conversion costs are incurred evenly throughout the departments. Normal wastage incurred in the cutting department amounts to 4% of the units that reach the wastage point, and arise at the end of the process. The following information applies to the assembly department for September 2021: Opening Material Conversion MARKS 6.5 5.5 3 Cost incurred in current period: Material Conversion 15 Units 70 000 150 000 180 000 20 000 Cost (NS) 325 000 128 000 560 000 1 800 000 Page 2 of 7 REQUIRED: 2.1. Prepare the process cost report for the cutting department using the FIFO method. (Show all your workings, and where possible, round off your final answers to two decimal places). 2.2. In what way is process costing differ from a job costing system? 2.3. Clearly explain whether you would agree with the following statements: "Normal loss is controllable; hence it is shown as a separate line item in the company's financial statements. On the other hand, abnormal loss is uncontrollable, thus it is allocated to other accounts". TOTAL MARKS MARKS J 17 1.5 1.5 The following transpired in the month of September 2021: 500 000 kilo of jatropha seeds were purchased at N$0.50 per kilo. 20 QUESTION 3 (15 MARKS. 27 MINUTES) Jatropha Namibian Products ("JNP") is a company that processes jatropha plant seeds into bio (diesek bio kerosene cosmetics and pesticides. The JNP process uses jatropha seeds that are bought from farmers in the SADC region. Because of the diversity of suppliers, the seeds delivered are not of the same quality. However production of bio diesel and bio kerosene requires high quality jatropha seeds. This causes JNP to first do a grading of all the seeds procured. The grading process results in a yield of 90% and poor quality seeds at 5%. The rest are impurities that are considered normal losses. The grading process costs N$7 000 per month and NS0.10 per kilo of jatropha seeds graded. The poor quality seeds are processed further at a cost of N$2 per kilo into cosmetic paste that is sold for NS3 per kilo. ortver After the grading, the high quality seeds are then ground to prepare them for extraction of bio diesel and bio kerosene. A liquefying chemical is applied to the ground seeds and the cost of this chemical is NS20 per litre Two litres of the chemical are required for every 1 000 kilos of ground seeded cooking oil. Since this chemical is a dissolving chemical, it does not add to the weight of the ground seeds. Other costs incurred in the processing department is fixed manufacturing overheads of N$10 000 per month. The average output from the processing department is 40% bio diesel and 60% bio kerosene. The bio diesel is sold as is to clients at NS5 per litre while the (bio kerosene must be processed further to make it super refined for use in jet engines. The costs relating to the further processing of bio kerosene amount to N$0.30 per litre and the output of the further processing is 90% of refined bio kerosene, which is sold at N$4.50 per litre. 10% of the output is a waste product that is sold at N$5 per litre as a pesticide after further processing costs of N$3 per litre and fixed cost of NS9 977 per month has been incurred. It is company policy to value inventory on the basis of First In, First Out (FIFO) and to deduct the net realisable value (NRV) of by products from the joint productions costs. Joint costs are allocated to joint products using the NRV method, Page 3 of 7 0 The sales were as follows: Bio-diesel Refined bio kerosene Note: 1 kilo=1 litre, therefore 1 000 kilos of input (jatropha seeds) yield 1 000 litres of output. Cosmetic paste (by product) Pesticides (by product) The only opening inventory was 30 000 litres of bio kerosene valued at N$0.80 per litre. There was no beginning or closing inventory work-in-process on hand. REQUIRED: 3.1 3.2 Prepare a schedule showing the joints costs allocated to the joint products for September 2021. 3.3 Total Determine the production cost per unit for each of the two joint products for September 2021 (round to two decimal places). Calculate the gross profit per joint product for September 2021 (round total values to the nearest N$), 160 000 litre 260 000 litre 20 000 litre 25 000 litre Units sold Revenue Cost of sales Materials Labour Factory overhead Gross profit Period costs Selling and distributions Administrative expenses Operating income Actual 40 000 2 360 000 (1 732 000) 760 000 632 000 340 000 628 000 (348 800) 128 800 220 000 279 200 Sub- Total QUESTION 4 (20 MARKS, 36 MINUTES) The management of BETA Limited developed the following static budget for one of its flagship product, and estimated that 30,000 units would be sold during the month of August 2021. Static budget 30 000 N$ 1 800 000 (1 290 000) 600 000 450 000 240 000 Marks 510 000 (320 000) 120 000 200 000 190 000 9 2 4 Total 15 9 11 15 Page 4 of 7 However, due to an expected increase in demand 40 000 units were sold. Since the sales figures are higher than expected the management needs to analyse all variances and decide whether a future revision of its budgets would be appropriate. REQUIRED: 4.1. 4.2 4.3 Calculate the following: (0) (ii) (iii) Actual Material cost per unit mp Labour cost per unit Selling price price per unit. Based on the information provided to you, what would be the appropriate recovery rate for factory overhead? Prepare a flexible budgeted statement for comprehensive incomes for 40 000 units using the above information from a static budget for 30 000 units showing clearly columns disclosing information for actual, flexed and variance. Denote the variance with U for unfavourable and F for favourable. Sales and production volume Standard selling price per barrel Standard variable cost per barrel Sales and production volume. Actual selling price per barrel Actual variable cost per barrel Marks Additional information: Standard cost card for one barrel of solvent Direct materials Direct labour Variable overheads NB: Overheads are absorbed on the basis of direct labour hours. 3 QUESTION 5 (20 MARKS, 36 MINUTES) Elso Ltd ("Elso") manufactures large-scale solvents for factories and household cleaning. The company uses standard costing system as a way of monitoring its cost. The following information is available for Elso for the month of August 2021: Budgeted 1 16 20 600 barrels 20 N$1 750 2 kards N$855 620 barrels N$1 690 N$863 34 litres @ N$15 per litre 15 hours @ N$12,50 per hour 15 hours @ N$10,50 per hour Page 5 of 7 Actual cost and usage information Direct materials Direct labour Variable overheads Total usage 20 410 litres 9 420 hours REQUIRED: Calculate the following variances and indicate whether the variance obtained s favourable or unfavourable. 5.1. Material price variance BP-SP x) SR 5.2. Material usage variance a-5Q) off 5.3. Labour rate variance 5.4. Labour efficiency variance 5.5, Variable overheads expenditure variance Total cost (NS) N$321 500 N$117 800 N$95 600 5.6. Variable overheads efficiency variance 5.7. Explain the possible causes of the type of variance obtained in 5.1 and 5.37 TOTAL MARKS MARKS 3 3 3 3 3 2 20 Page 6 of 7 QUESTION 6 (10 MARKS, 18 MINUTES) The following selected data relate to the Mexit Division of Swifty Enterprises (SE): Sales revenue Uncontrollable fixed costs traceable to the division Allocated corporate overhead Controllable fixed costs traceable to the division Variable costs REQUIRED: 6.1. 6.2. 6.3. 6.4. Compute the following for the Mexit Division: a. Segment contribution margin: b. Controllable profit margin: N$4,580,000 1,360,000 590,000 1,120,000 40% c. Segment profit margin. When analyzing the Mexit Division as a resource investment for SE, which of the three measures should be used? Why? Assume that Mexit's management decided to construct a segmented income statement that reflected the company's five operating departments. Is it possible to trace all of the N$1,120,000 in controllable fixed costs to the departments? Explain briefly. Which of the five dollar values stated in the body of the problem would be utilized to calculate Swifty Enterprises' income before taxes? TOTAL MARKS <<<END OF QUESTION PAPER>>>> MARKS 2 1 2 1 10 Page 7 d Namib Mills has a production capacity of 200 000 bags of maize flour per year, normal capacity usage is reckoned as 90% Standard variable production costs are N$11 per bag. The fixed cost is N$360 000 per year. 18083 Variable selling costs are NS3 per bag, and fixed selling costs are N$270 000 per year, the selling price per bag is N$20.) Unit ca In the year just ended on the 30 August 2021, production was 160 000 bags, Accordingly, sales C2 were 150 000 bags. The closing inventory on the 30th August 2021 was 20 000 bags. The actual variable production costs for the year were N$ 35 000 higher than the standard. 17 REQUIRED: Calculate the profit for the year using absorption costing method to find Calculate the profit for the year using marginal costing method Use your answers in 1.1 and 1.2 and reconciliation profits between the two statements TOTAL MARKS FOR QUESTION 1 1.1 1.2 1.3 Opening inventory of work in progress (20% completed) go.. left Units introduced Units transferred to assembly department Closing inventory of work in progress (90% completed) QUESTION 2 (20 MARKS, 36 MINUTES) House & Home (HH") manufactures a single model of a commercial prefabricated wooden cabinet. The basic cabinet components are cut out of wood in the cutting department and then transferred to the assembly department. Materials are added at the beginning of the process in both departments. Conversion costs are incurred evenly throughout the departments. Normal wastage incurred in the cutting department amounts to 4% of the units that reach the wastage point, and arise at the end of the process. The following information applies to the assembly department for September 2021: Opening Material Conversion MARKS 6.5 5.5 3 Cost incurred in current period: Material Conversion 15 Units 70 000 150 000 180 000 20 000 Cost (NS) 325 000 128 000 560 000 1 800 000 Page 2 of 7 REQUIRED: 2.1. Prepare the process cost report for the cutting department using the FIFO method. (Show all your workings, and where possible, round off your final answers to two decimal places). 2.2. In what way is process costing differ from a job costing system? 2.3. Clearly explain whether you would agree with the following statements: "Normal loss is controllable; hence it is shown as a separate line item in the company's financial statements. On the other hand, abnormal loss is uncontrollable, thus it is allocated to other accounts". TOTAL MARKS MARKS J 17 1.5 1.5 The following transpired in the month of September 2021: 500 000 kilo of jatropha seeds were purchased at N$0.50 per kilo. 20 QUESTION 3 (15 MARKS. 27 MINUTES) Jatropha Namibian Products ("JNP") is a company that processes jatropha plant seeds into bio (diesek bio kerosene cosmetics and pesticides. The JNP process uses jatropha seeds that are bought from farmers in the SADC region. Because of the diversity of suppliers, the seeds delivered are not of the same quality. However production of bio diesel and bio kerosene requires high quality jatropha seeds. This causes JNP to first do a grading of all the seeds procured. The grading process results in a yield of 90% and poor quality seeds at 5%. The rest are impurities that are considered normal losses. The grading process costs N$7 000 per month and NS0.10 per kilo of jatropha seeds graded. The poor quality seeds are processed further at a cost of N$2 per kilo into cosmetic paste that is sold for NS3 per kilo. ortver After the grading, the high quality seeds are then ground to prepare them for extraction of bio diesel and bio kerosene. A liquefying chemical is applied to the ground seeds and the cost of this chemical is NS20 per litre Two litres of the chemical are required for every 1 000 kilos of ground seeded cooking oil. Since this chemical is a dissolving chemical, it does not add to the weight of the ground seeds. Other costs incurred in the processing department is fixed manufacturing overheads of N$10 000 per month. The average output from the processing department is 40% bio diesel and 60% bio kerosene. The bio diesel is sold as is to clients at NS5 per litre while the (bio kerosene must be processed further to make it super refined for use in jet engines. The costs relating to the further processing of bio kerosene amount to N$0.30 per litre and the output of the further processing is 90% of refined bio kerosene, which is sold at N$4.50 per litre. 10% of the output is a waste product that is sold at N$5 per litre as a pesticide after further processing costs of N$3 per litre and fixed cost of NS9 977 per month has been incurred. It is company policy to value inventory on the basis of First In, First Out (FIFO) and to deduct the net realisable value (NRV) of by products from the joint productions costs. Joint costs are allocated to joint products using the NRV method, Page 3 of 7 0 The sales were as follows: Bio-diesel Refined bio kerosene Note: 1 kilo=1 litre, therefore 1 000 kilos of input (jatropha seeds) yield 1 000 litres of output. Cosmetic paste (by product) Pesticides (by product) The only opening inventory was 30 000 litres of bio kerosene valued at N$0.80 per litre. There was no beginning or closing inventory work-in-process on hand. REQUIRED: 3.1 3.2 Prepare a schedule showing the joints costs allocated to the joint products for September 2021. 3.3 Total Determine the production cost per unit for each of the two joint products for September 2021 (round to two decimal places). Calculate the gross profit per joint product for September 2021 (round total values to the nearest N$), 160 000 litre 260 000 litre 20 000 litre 25 000 litre Units sold Revenue Cost of sales Materials Labour Factory overhead Gross profit Period costs Selling and distributions Administrative expenses Operating income Actual 40 000 2 360 000 (1 732 000) 760 000 632 000 340 000 628 000 (348 800) 128 800 220 000 279 200 Sub- Total QUESTION 4 (20 MARKS, 36 MINUTES) The management of BETA Limited developed the following static budget for one of its flagship product, and estimated that 30,000 units would be sold during the month of August 2021. Static budget 30 000 N$ 1 800 000 (1 290 000) 600 000 450 000 240 000 Marks 510 000 (320 000) 120 000 200 000 190 000 9 2 4 Total 15 9 11 15 Page 4 of 7 However, due to an expected increase in demand 40 000 units were sold. Since the sales figures are higher than expected the management needs to analyse all variances and decide whether a future revision of its budgets would be appropriate. REQUIRED: 4.1. 4.2 4.3 Calculate the following: (0) (ii) (iii) Actual Material cost per unit mp Labour cost per unit Selling price price per unit. Based on the information provided to you, what would be the appropriate recovery rate for factory overhead? Prepare a flexible budgeted statement for comprehensive incomes for 40 000 units using the above information from a static budget for 30 000 units showing clearly columns disclosing information for actual, flexed and variance. Denote the variance with U for unfavourable and F for favourable. Sales and production volume Standard selling price per barrel Standard variable cost per barrel Sales and production volume. Actual selling price per barrel Actual variable cost per barrel Marks Additional information: Standard cost card for one barrel of solvent Direct materials Direct labour Variable overheads NB: Overheads are absorbed on the basis of direct labour hours. 3 QUESTION 5 (20 MARKS, 36 MINUTES) Elso Ltd ("Elso") manufactures large-scale solvents for factories and household cleaning. The company uses standard costing system as a way of monitoring its cost. The following information is available for Elso for the month of August 2021: Budgeted 1 16 20 600 barrels 20 N$1 750 2 kards N$855 620 barrels N$1 690 N$863 34 litres @ N$15 per litre 15 hours @ N$12,50 per hour 15 hours @ N$10,50 per hour Page 5 of 7 Actual cost and usage information Direct materials Direct labour Variable overheads Total usage 20 410 litres 9 420 hours REQUIRED: Calculate the following variances and indicate whether the variance obtained s favourable or unfavourable. 5.1. Material price variance BP-SP x) SR 5.2. Material usage variance a-5Q) off 5.3. Labour rate variance 5.4. Labour efficiency variance 5.5, Variable overheads expenditure variance Total cost (NS) N$321 500 N$117 800 N$95 600 5.6. Variable overheads efficiency variance 5.7. Explain the possible causes of the type of variance obtained in 5.1 and 5.37 TOTAL MARKS MARKS 3 3 3 3 3 2 20 Page 6 of 7 QUESTION 6 (10 MARKS, 18 MINUTES) The following selected data relate to the Mexit Division of Swifty Enterprises (SE): Sales revenue Uncontrollable fixed costs traceable to the division Allocated corporate overhead Controllable fixed costs traceable to the division Variable costs REQUIRED: 6.1. 6.2. 6.3. 6.4. Compute the following for the Mexit Division: a. Segment contribution margin: b. Controllable profit margin: N$4,580,000 1,360,000 590,000 1,120,000 40% c. Segment profit margin. When analyzing the Mexit Division as a resource investment for SE, which of the three measures should be used? Why? Assume that Mexit's management decided to construct a segmented income statement that reflected the company's five operating departments. Is it possible to trace all of the N$1,120,000 in controllable fixed costs to the departments? Explain briefly. Which of the five dollar values stated in the body of the problem would be utilized to calculate Swifty Enterprises' income before taxes? TOTAL MARKS <<<END OF QUESTION PAPER>>>> MARKS 2 1 2 1 10 Page 7 d Namib Mills has a production capacity of 200 000 bags of maize flour per year, normal capacity usage is reckoned as 90% Standard variable production costs are N$11 per bag. The fixed cost is N$360 000 per year. 18083 Variable selling costs are NS3 per bag, and fixed selling costs are N$270 000 per year, the selling price per bag is N$20.) Unit ca In the year just ended on the 30 August 2021, production was 160 000 bags, Accordingly, sales C2 were 150 000 bags. The closing inventory on the 30th August 2021 was 20 000 bags. The actual variable production costs for the year were N$ 35 000 higher than the standard. 17 REQUIRED: Calculate the profit for the year using absorption costing method to find Calculate the profit for the year using marginal costing method Use your answers in 1.1 and 1.2 and reconciliation profits between the two statements TOTAL MARKS FOR QUESTION 1 1.1 1.2 1.3 Opening inventory of work in progress (20% completed) go.. left Units introduced Units transferred to assembly department Closing inventory of work in progress (90% completed) QUESTION 2 (20 MARKS, 36 MINUTES) House & Home (HH") manufactures a single model of a commercial prefabricated wooden cabinet. The basic cabinet components are cut out of wood in the cutting department and then transferred to the assembly department. Materials are added at the beginning of the process in both departments. Conversion costs are incurred evenly throughout the departments. Normal wastage incurred in the cutting department amounts to 4% of the units that reach the wastage point, and arise at the end of the process. The following information applies to the assembly department for September 2021: Opening Material Conversion MARKS 6.5 5.5 3 Cost incurred in current period: Material Conversion 15 Units 70 000 150 000 180 000 20 000 Cost (NS) 325 000 128 000 560 000 1 800 000 Page 2 of 7 REQUIRED: 2.1. Prepare the process cost report for the cutting department using the FIFO method. (Show all your workings, and where possible, round off your final answers to two decimal places). 2.2. In what way is process costing differ from a job costing system? 2.3. Clearly explain whether you would agree with the following statements: "Normal loss is controllable; hence it is shown as a separate line item in the company's financial statements. On the other hand, abnormal loss is uncontrollable, thus it is allocated to other accounts". TOTAL MARKS MARKS J 17 1.5 1.5 The following transpired in the month of September 2021: 500 000 kilo of jatropha seeds were purchased at N$0.50 per kilo. 20 QUESTION 3 (15 MARKS. 27 MINUTES) Jatropha Namibian Products ("JNP") is a company that processes jatropha plant seeds into bio (diesek bio kerosene cosmetics and pesticides. The JNP process uses jatropha seeds that are bought from farmers in the SADC region. Because of the diversity of suppliers, the seeds delivered are not of the same quality. However production of bio diesel and bio kerosene requires high quality jatropha seeds. This causes JNP to first do a grading of all the seeds procured. The grading process results in a yield of 90% and poor quality seeds at 5%. The rest are impurities that are considered normal losses. The grading process costs N$7 000 per month and NS0.10 per kilo of jatropha seeds graded. The poor quality seeds are processed further at a cost of N$2 per kilo into cosmetic paste that is sold for NS3 per kilo. ortver After the grading, the high quality seeds are then ground to prepare them for extraction of bio diesel and bio kerosene. A liquefying chemical is applied to the ground seeds and the cost of this chemical is NS20 per litre Two litres of the chemical are required for every 1 000 kilos of ground seeded cooking oil. Since this chemical is a dissolving chemical, it does not add to the weight of the ground seeds. Other costs incurred in the processing department is fixed manufacturing overheads of N$10 000 per month. The average output from the processing department is 40% bio diesel and 60% bio kerosene. The bio diesel is sold as is to clients at NS5 per litre while the (bio kerosene must be processed further to make it super refined for use in jet engines. The costs relating to the further processing of bio kerosene amount to N$0.30 per litre and the output of the further processing is 90% of refined bio kerosene, which is sold at N$4.50 per litre. 10% of the output is a waste product that is sold at N$5 per litre as a pesticide after further processing costs of N$3 per litre and fixed cost of NS9 977 per month has been incurred. It is company policy to value inventory on the basis of First In, First Out (FIFO) and to deduct the net realisable value (NRV) of by products from the joint productions costs. Joint costs are allocated to joint products using the NRV method, Page 3 of 7 0 The sales were as follows: Bio-diesel Refined bio kerosene Note: 1 kilo=1 litre, therefore 1 000 kilos of input (jatropha seeds) yield 1 000 litres of output. Cosmetic paste (by product) Pesticides (by product) The only opening inventory was 30 000 litres of bio kerosene valued at N$0.80 per litre. There was no beginning or closing inventory work-in-process on hand. REQUIRED: 3.1 3.2 Prepare a schedule showing the joints costs allocated to the joint products for September 2021. 3.3 Total Determine the production cost per unit for each of the two joint products for September 2021 (round to two decimal places). Calculate the gross profit per joint product for September 2021 (round total values to the nearest N$), 160 000 litre 260 000 litre 20 000 litre 25 000 litre Units sold Revenue Cost of sales Materials Labour Factory overhead Gross profit Period costs Selling and distributions Administrative expenses Operating income Actual 40 000 2 360 000 (1 732 000) 760 000 632 000 340 000 628 000 (348 800) 128 800 220 000 279 200 Sub- Total QUESTION 4 (20 MARKS, 36 MINUTES) The management of BETA Limited developed the following static budget for one of its flagship product, and estimated that 30,000 units would be sold during the month of August 2021. Static budget 30 000 N$ 1 800 000 (1 290 000) 600 000 450 000 240 000 Marks 510 000 (320 000) 120 000 200 000 190 000 9 2 4 Total 15 9 11 15 Page 4 of 7 However, due to an expected increase in demand 40 000 units were sold. Since the sales figures are higher than expected the management needs to analyse all variances and decide whether a future revision of its budgets would be appropriate. REQUIRED: 4.1. 4.2 4.3 Calculate the following: (0) (ii) (iii) Actual Material cost per unit mp Labour cost per unit Selling price price per unit. Based on the information provided to you, what would be the appropriate recovery rate for factory overhead? Prepare a flexible budgeted statement for comprehensive incomes for 40 000 units using the above information from a static budget for 30 000 units showing clearly columns disclosing information for actual, flexed and variance. Denote the variance with U for unfavourable and F for favourable. Sales and production volume Standard selling price per barrel Standard variable cost per barrel Sales and production volume. Actual selling price per barrel Actual variable cost per barrel Marks Additional information: Standard cost card for one barrel of solvent Direct materials Direct labour Variable overheads NB: Overheads are absorbed on the basis of direct labour hours. 3 QUESTION 5 (20 MARKS, 36 MINUTES) Elso Ltd ("Elso") manufactures large-scale solvents for factories and household cleaning. The company uses standard costing system as a way of monitoring its cost. The following information is available for Elso for the month of August 2021: Budgeted 1 16 20 600 barrels 20 N$1 750 2 kards N$855 620 barrels N$1 690 N$863 34 litres @ N$15 per litre 15 hours @ N$12,50 per hour 15 hours @ N$10,50 per hour Page 5 of 7 Actual cost and usage information Direct materials Direct labour Variable overheads Total usage 20 410 litres 9 420 hours REQUIRED: Calculate the following variances and indicate whether the variance obtained s favourable or unfavourable. 5.1. Material price variance BP-SP x) SR 5.2. Material usage variance a-5Q) off 5.3. Labour rate variance 5.4. Labour efficiency variance 5.5, Variable overheads expenditure variance Total cost (NS) N$321 500 N$117 800 N$95 600 5.6. Variable overheads efficiency variance 5.7. Explain the possible causes of the type of variance obtained in 5.1 and 5.37 TOTAL MARKS MARKS 3 3 3 3 3 2 20 Page 6 of 7 QUESTION 6 (10 MARKS, 18 MINUTES) The following selected data relate to the Mexit Division of Swifty Enterprises (SE): Sales revenue Uncontrollable fixed costs traceable to the division Allocated corporate overhead Controllable fixed costs traceable to the division Variable costs REQUIRED: 6.1. 6.2. 6.3. 6.4. Compute the following for the Mexit Division: a. Segment contribution margin: b. Controllable profit margin: N$4,580,000 1,360,000 590,000 1,120,000 40% c. Segment profit margin. When analyzing the Mexit Division as a resource investment for SE, which of the three measures should be used? Why? Assume that Mexit's management decided to construct a segmented income statement that reflected the company's five operating departments. Is it possible to trace all of the N$1,120,000 in controllable fixed costs to the departments? Explain briefly. Which of the five dollar values stated in the body of the problem would be utilized to calculate Swifty Enterprises' income before taxes? TOTAL MARKS <<<END OF QUESTION PAPER>>>> MARKS 2 1 2 1 10 Page 7 d Namib Mills has a production capacity of 200 000 bags of maize flour per year, normal capacity usage is reckoned as 90% Standard variable production costs are N$11 per bag. The fixed cost is N$360 000 per year. 18083 Variable selling costs are NS3 per bag, and fixed selling costs are N$270 000 per year, the selling price per bag is N$20.) Unit ca In the year just ended on the 30 August 2021, production was 160 000 bags, Accordingly, sales C2 were 150 000 bags. The closing inventory on the 30th August 2021 was 20 000 bags. The actual variable production costs for the year were N$ 35 000 higher than the standard. 17 REQUIRED: Calculate the profit for the year using absorption costing method to find Calculate the profit for the year using marginal costing method Use your answers in 1.1 and 1.2 and reconciliation profits between the two statements TOTAL MARKS FOR QUESTION 1 1.1 1.2 1.3 Opening inventory of work in progress (20% completed) go.. left Units introduced Units transferred to assembly department Closing inventory of work in progress (90% completed) QUESTION 2 (20 MARKS, 36 MINUTES) House & Home (HH") manufactures a single model of a commercial prefabricated wooden cabinet. The basic cabinet components are cut out of wood in the cutting department and then transferred to the assembly department. Materials are added at the beginning of the process in both departments. Conversion costs are incurred evenly throughout the departments. Normal wastage incurred in the cutting department amounts to 4% of the units that reach the wastage point, and arise at the end of the process. The following information applies to the assembly department for September 2021: Opening Material Conversion MARKS 6.5 5.5 3 Cost incurred in current period: Material Conversion 15 Units 70 000 150 000 180 000 20 000 Cost (NS) 325 000 128 000 560 000 1 800 000 Page 2 of 7 REQUIRED: 2.1. Prepare the process cost report for the cutting department using the FIFO method. (Show all your workings, and where possible, round off your final answers to two decimal places). 2.2. In what way is process costing differ from a job costing system? 2.3. Clearly explain whether you would agree with the following statements: "Normal loss is controllable; hence it is shown as a separate line item in the company's financial statements. On the other hand, abnormal loss is uncontrollable, thus it is allocated to other accounts". TOTAL MARKS MARKS J 17 1.5 1.5 The following transpired in the month of September 2021: 500 000 kilo of jatropha seeds were purchased at N$0.50 per kilo. 20 QUESTION 3 (15 MARKS. 27 MINUTES) Jatropha Namibian Products ("JNP") is a company that processes jatropha plant seeds into bio (diesek bio kerosene cosmetics and pesticides. The JNP process uses jatropha seeds that are bought from farmers in the SADC region. Because of the diversity of suppliers, the seeds delivered are not of the same quality. However production of bio diesel and bio kerosene requires high quality jatropha seeds. This causes JNP to first do a grading of all the seeds procured. The grading process results in a yield of 90% and poor quality seeds at 5%. The rest are impurities that are considered normal losses. The grading process costs N$7 000 per month and NS0.10 per kilo of jatropha seeds graded. The poor quality seeds are processed further at a cost of N$2 per kilo into cosmetic paste that is sold for NS3 per kilo. ortver After the grading, the high quality seeds are then ground to prepare them for extraction of bio diesel and bio kerosene. A liquefying chemical is applied to the ground seeds and the cost of this chemical is NS20 per litre Two litres of the chemical are required for every 1 000 kilos of ground seeded cooking oil. Since this chemical is a dissolving chemical, it does not add to the weight of the ground seeds. Other costs incurred in the processing department is fixed manufacturing overheads of N$10 000 per month. The average output from the processing department is 40% bio diesel and 60% bio kerosene. The bio diesel is sold as is to clients at NS5 per litre while the (bio kerosene must be processed further to make it super refined for use in jet engines. The costs relating to the further processing of bio kerosene amount to N$0.30 per litre and the output of the further processing is 90% of refined bio kerosene, which is sold at N$4.50 per litre. 10% of the output is a waste product that is sold at N$5 per litre as a pesticide after further processing costs of N$3 per litre and fixed cost of NS9 977 per month has been incurred. It is company policy to value inventory on the basis of First In, First Out (FIFO) and to deduct the net realisable value (NRV) of by products from the joint productions costs. Joint costs are allocated to joint products using the NRV method, Page 3 of 7 0 The sales were as follows: Bio-diesel Refined bio kerosene Note: 1 kilo=1 litre, therefore 1 000 kilos of input (jatropha seeds) yield 1 000 litres of output. Cosmetic paste (by product) Pesticides (by product) The only opening inventory was 30 000 litres of bio kerosene valued at N$0.80 per litre. There was no beginning or closing inventory work-in-process on hand. REQUIRED: 3.1 3.2 Prepare a schedule showing the joints costs allocated to the joint products for September 2021. 3.3 Total Determine the production cost per unit for each of the two joint products for September 2021 (round to two decimal places). Calculate the gross profit per joint product for September 2021 (round total values to the nearest N$), 160 000 litre 260 000 litre 20 000 litre 25 000 litre Units sold Revenue Cost of sales Materials Labour Factory overhead Gross profit Period costs Selling and distributions Administrative expenses Operating income Actual 40 000 2 360 000 (1 732 000) 760 000 632 000 340 000 628 000 (348 800) 128 800 220 000 279 200 Sub- Total QUESTION 4 (20 MARKS, 36 MINUTES) The management of BETA Limited developed the following static budget for one of its flagship product, and estimated that 30,000 units would be sold during the month of August 2021. Static budget 30 000 N$ 1 800 000 (1 290 000) 600 000 450 000 240 000 Marks 510 000 (320 000) 120 000 200 000 190 000 9 2 4 Total 15 9 11 15 Page 4 of 7 However, due to an expected increase in demand 40 000 units were sold. Since the sales figures are higher than expected the management needs to analyse all variances and decide whether a future revision of its budgets would be appropriate. REQUIRED: 4.1. 4.2 4.3 Calculate the following: (0) (ii) (iii) Actual Material cost per unit mp Labour cost per unit Selling price price per unit. Based on the information provided to you, what would be the appropriate recovery rate for factory overhead? Prepare a flexible budgeted statement for comprehensive incomes for 40 000 units using the above information from a static budget for 30 000 units showing clearly columns disclosing information for actual, flexed and variance. Denote the variance with U for unfavourable and F for favourable. Sales and production volume Standard selling price per barrel Standard variable cost per barrel Sales and production volume. Actual selling price per barrel Actual variable cost per barrel Marks Additional information: Standard cost card for one barrel of solvent Direct materials Direct labour Variable overheads NB: Overheads are absorbed on the basis of direct labour hours. 3 QUESTION 5 (20 MARKS, 36 MINUTES) Elso Ltd ("Elso") manufactures large-scale solvents for factories and household cleaning. The company uses standard costing system as a way of monitoring its cost. The following information is available for Elso for the month of August 2021: Budgeted 1 16 20 600 barrels 20 N$1 750 2 kards N$855 620 barrels N$1 690 N$863 34 litres @ N$15 per litre 15 hours @ N$12,50 per hour 15 hours @ N$10,50 per hour Page 5 of 7 Actual cost and usage information Direct materials Direct labour Variable overheads Total usage 20 410 litres 9 420 hours REQUIRED: Calculate the following variances and indicate whether the variance obtained s favourable or unfavourable. 5.1. Material price variance BP-SP x) SR 5.2. Material usage variance a-5Q) off 5.3. Labour rate variance 5.4. Labour efficiency variance 5.5, Variable overheads expenditure variance Total cost (NS) N$321 500 N$117 800 N$95 600 5.6. Variable overheads efficiency variance 5.7. Explain the possible causes of the type of variance obtained in 5.1 and 5.37 TOTAL MARKS MARKS 3 3 3 3 3 2 20 Page 6 of 7 QUESTION 6 (10 MARKS, 18 MINUTES) The following selected data relate to the Mexit Division of Swifty Enterprises (SE): Sales revenue Uncontrollable fixed costs traceable to the division Allocated corporate overhead Controllable fixed costs traceable to the division Variable costs REQUIRED: 6.1. 6.2. 6.3. 6.4. Compute the following for the Mexit Division: a. Segment contribution margin: b. Controllable profit margin: N$4,580,000 1,360,000 590,000 1,120,000 40% c. Segment profit margin. When analyzing the Mexit Division as a resource investment for SE, which of the three measures should be used? Why? Assume that Mexit's management decided to construct a segmented income statement that reflected the company's five operating departments. Is it possible to trace all of the N$1,120,000 in controllable fixed costs to the departments? Explain briefly. Which of the five dollar values stated in the body of the problem would be utilized to calculate Swifty Enterprises' income before taxes? TOTAL MARKS <<<END OF QUESTION PAPER>>>> MARKS 2 1 2 1 10 Page 7 d Namib Mills has a production capacity of 200 000 bags of maize flour per year, normal capacity usage is reckoned as 90% Standard variable production costs are N$11 per bag. The fixed cost is N$360 000 per year. 18083 Variable selling costs are NS3 per bag, and fixed selling costs are N$270 000 per year, the selling price per bag is N$20.) Unit ca In the year just ended on the 30 August 2021, production was 160 000 bags, Accordingly, sales C2 were 150 000 bags. The closing inventory on the 30th August 2021 was 20 000 bags. The actual variable production costs for the year were N$ 35 000 higher than the standard. 17 REQUIRED: Calculate the profit for the year using absorption costing method to find Calculate the profit for the year using marginal costing method Use your answers in 1.1 and 1.2 and reconciliation profits between the two statements TOTAL MARKS FOR QUESTION 1 1.1 1.2 1.3 Opening inventory of work in progress (20% completed) go.. left Units introduced Units transferred to assembly department Closing inventory of work in progress (90% completed) QUESTION 2 (20 MARKS, 36 MINUTES) House & Home (HH") manufactures a single model of a commercial prefabricated wooden cabinet. The basic cabinet components are cut out of wood in the cutting department and then transferred to the assembly department. Materials are added at the beginning of the process in both departments. Conversion costs are incurred evenly throughout the departments. Normal wastage incurred in the cutting department amounts to 4% of the units that reach the wastage point, and arise at the end of the process. The following information applies to the assembly department for September 2021: Opening Material Conversion MARKS 6.5 5.5 3 Cost incurred in current period: Material Conversion 15 Units 70 000 150 000 180 000 20 000 Cost (NS) 325 000 128 000 560 000 1 800 000 Page 2 of 7 REQUIRED: 2.1. Prepare the process cost report for the cutting department using the FIFO method. (Show all your workings, and where possible, round off your final answers to two decimal places). 2.2. In what way is process costing differ from a job costing system? 2.3. Clearly explain whether you would agree with the following statements: "Normal loss is controllable; hence it is shown as a separate line item in the company's financial statements. On the other hand, abnormal loss is uncontrollable, thus it is allocated to other accounts". TOTAL MARKS MARKS J 17 1.5 1.5 The following transpired in the month of September 2021: 500 000 kilo of jatropha seeds were purchased at N$0.50 per kilo. 20 QUESTION 3 (15 MARKS. 27 MINUTES) Jatropha Namibian Products ("JNP") is a company that processes jatropha plant seeds into bio (diesek bio kerosene cosmetics and pesticides. The JNP process uses jatropha seeds that are bought from farmers in the SADC region. Because of the diversity of suppliers, the seeds delivered are not of the same quality. However production of bio diesel and bio kerosene requires high quality jatropha seeds. This causes JNP to first do a grading of all the seeds procured. The grading process results in a yield of 90% and poor quality seeds at 5%. The rest are impurities that are considered normal losses. The grading process costs N$7 000 per month and NS0.10 per kilo of jatropha seeds graded. The poor quality seeds are processed further at a cost of N$2 per kilo into cosmetic paste that is sold for NS3 per kilo. ortver After the grading, the high quality seeds are then ground to prepare them for extraction of bio diesel and bio kerosene. A liquefying chemical is applied to the ground seeds and the cost of this chemical is NS20 per litre Two litres of the chemical are required for every 1 000 kilos of ground seeded cooking oil. Since this chemical is a dissolving chemical, it does not add to the weight of the ground seeds. Other costs incurred in the processing department is fixed manufacturing overheads of N$10 000 per month. The average output from the processing department is 40% bio diesel and 60% bio kerosene. The bio diesel is sold as is to clients at NS5 per litre while the (bio kerosene must be processed further to make it super refined for use in jet engines. The costs relating to the further processing of bio kerosene amount to N$0.30 per litre and the output of the further processing is 90% of refined bio kerosene, which is sold at N$4.50 per litre. 10% of the output is a waste product that is sold at N$5 per litre as a pesticide after further processing costs of N$3 per litre and fixed cost of NS9 977 per month has been incurred. It is company policy to value inventory on the basis of First In, First Out (FIFO) and to deduct the net realisable value (NRV) of by products from the joint productions costs. Joint costs are allocated to joint products using the NRV method, Page 3 of 7 0 The sales were as follows: Bio-diesel Refined bio kerosene Note: 1 kilo=1 litre, therefore 1 000 kilos of input (jatropha seeds) yield 1 000 litres of output. Cosmetic paste (by product) Pesticides (by product) The only opening inventory was 30 000 litres of bio kerosene valued at N$0.80 per litre. There was no beginning or closing inventory work-in-process on hand. REQUIRED: 3.1 3.2 Prepare a schedule showing the joints costs allocated to the joint products for September 2021. 3.3 Total Determine the production cost per unit for each of the two joint products for September 2021 (round to two decimal places). Calculate the gross profit per joint product for September 2021 (round total values to the nearest N$), 160 000 litre 260 000 litre 20 000 litre 25 000 litre Units sold Revenue Cost of sales Materials Labour Factory overhead Gross profit Period costs Selling and distributions Administrative expenses Operating income Actual 40 000 2 360 000 (1 732 000) 760 000 632 000 340 000 628 000 (348 800) 128 800 220 000 279 200 Sub- Total QUESTION 4 (20 MARKS, 36 MINUTES) The management of BETA Limited developed the following static budget for one of its flagship product, and estimated that 30,000 units would be sold during the month of August 2021. Static budget 30 000 N$ 1 800 000 (1 290 000) 600 000 450 000 240 000 Marks 510 000 (320 000) 120 000 200 000 190 000 9 2 4 Total 15 9 11 15 Page 4 of 7 However, due to an expected increase in demand 40 000 units were sold. Since the sales figures are higher than expected the management needs to analyse all variances and decide whether a future revision of its budgets would be appropriate. REQUIRED: 4.1. 4.2 4.3 Calculate the following: (0) (ii) (iii) Actual Material cost per unit mp Labour cost per unit Selling price price per unit. Based on the information provided to you, what would be the appropriate recovery rate for factory overhead? Prepare a flexible budgeted statement for comprehensive incomes for 40 000 units using the above information from a static budget for 30 000 units showing clearly columns disclosing information for actual, flexed and variance. Denote the variance with U for unfavourable and F for favourable. Sales and production volume Standard selling price per barrel Standard variable cost per barrel Sales and production volume. Actual selling price per barrel Actual variable cost per barrel Marks Additional information: Standard cost card for one barrel of solvent Direct materials Direct labour Variable overheads NB: Overheads are absorbed on the basis of direct labour hours. 3 QUESTION 5 (20 MARKS, 36 MINUTES) Elso Ltd ("Elso") manufactures large-scale solvents for factories and household cleaning. The company uses standard costing system as a way of monitoring its cost. The following information is available for Elso for the month of August 2021: Budgeted 1 16 20 600 barrels 20 N$1 750 2 kards N$855 620 barrels N$1 690 N$863 34 litres @ N$15 per litre 15 hours @ N$12,50 per hour 15 hours @ N$10,50 per hour Page 5 of 7 Actual cost and usage information Direct materials Direct labour Variable overheads Total usage 20 410 litres 9 420 hours REQUIRED: Calculate the following variances and indicate whether the variance obtained s favourable or unfavourable. 5.1. Material price variance BP-SP x) SR 5.2. Material usage variance a-5Q) off 5.3. Labour rate variance 5.4. Labour efficiency variance 5.5, Variable overheads expenditure variance Total cost (NS) N$321 500 N$117 800 N$95 600 5.6. Variable overheads efficiency variance 5.7. Explain the possible causes of the type of variance obtained in 5.1 and 5.37 TOTAL MARKS MARKS 3 3 3 3 3 2 20 Page 6 of 7 QUESTION 6 (10 MARKS, 18 MINUTES) The following selected data relate to the Mexit Division of Swifty Enterprises (SE): Sales revenue Uncontrollable fixed costs traceable to the division Allocated corporate overhead Controllable fixed costs traceable to the division Variable costs REQUIRED: 6.1. 6.2. 6.3. 6.4. Compute the following for the Mexit Division: a. Segment contribution margin: b. Controllable profit margin: N$4,580,000 1,360,000 590,000 1,120,000 40% c. Segment profit margin. When analyzing the Mexit Division as a resource investment for SE, which of the three measures should be used? Why? Assume that Mexit's management decided to construct a segmented income statement that reflected the company's five operating departments. Is it possible to trace all of the N$1,120,000 in controllable fixed costs to the departments? Explain briefly. Which of the five dollar values stated in the body of the problem would be utilized to calculate Swifty Enterprises' income before taxes? TOTAL MARKS <<<END OF QUESTION PAPER>>>> MARKS 2 1 2 1 10 Page 7 d Namib Mills has a production capacity of 200 000 bags of maize flour per year, normal capacity usage is reckoned as 90% Standard variable production costs are N$11 per bag. The fixed cost is N$360 000 per year. 18083 Variable selling costs are NS3 per bag, and fixed selling costs are N$270 000 per year, the selling price per bag is N$20.) Unit ca In the year just ended on the 30 August 2021, production was 160 000 bags, Accordingly, sales C2 were 150 000 bags. The closing inventory on the 30th August 2021 was 20 000 bags. The actual variable production costs for the year were N$ 35 000 higher than the standard. 17 REQUIRED: Calculate the profit for the year using absorption costing method to find Calculate the profit for the year using marginal costing method Use your answers in 1.1 and 1.2 and reconciliation profits between the two statements TOTAL MARKS FOR QUESTION 1 1.1 1.2 1.3 Opening inventory of work in progress (20% completed) go.. left Units introduced Units transferred to assembly department Closing inventory of work in progress (90% completed) QUESTION 2 (20 MARKS, 36 MINUTES) House & Home (HH") manufactures a single model of a commercial prefabricated wooden cabinet. The basic cabinet components are cut out of wood in the cutting department and then transferred to the assembly department. Materials are added at the beginning of the process in both departments. Conversion costs are incurred evenly throughout the departments. Normal wastage incurred in the cutting department amounts to 4% of the units that reach the wastage point, and arise at the end of the process. The following information applies to the assembly department for September 2021: Opening Material Conversion MARKS 6.5 5.5 3 Cost incurred in current period: Material Conversion 15 Units 70 000 150 000 180 000 20 000 Cost (NS) 325 000 128 000 560 000 1 800 000 Page 2 of 7 REQUIRED: 2.1. Prepare the process cost report for the cutting department using the FIFO method. (Show all your workings, and where possible, round off your final answers to two decimal places). 2.2. In what way is process costing differ from a job costing system? 2.3. Clearly explain whether you would agree with the following statements: "Normal loss is controllable; hence it is shown as a separate line item in the company's financial statements. On the other hand, abnormal loss is uncontrollable, thus it is allocated to other accounts". TOTAL MARKS MARKS J 17 1.5 1.5 The following transpired in the month of September 2021: 500 000 kilo of jatropha seeds were purchased at N$0.50 per kilo. 20 QUESTION 3 (15 MARKS. 27 MINUTES) Jatropha Namibian Products ("JNP") is a company that processes jatropha plant seeds into bio (diesek bio kerosene cosmetics and pesticides. The JNP process uses jatropha seeds that are bought from farmers in the SADC region. Because of the diversity of suppliers, the seeds delivered are not of the same quality. However production of bio diesel and bio kerosene requires high quality jatropha seeds. This causes JNP to first do a grading of all the seeds procured. The grading process results in a yield of 90% and poor quality seeds at 5%. The rest are impurities that are considered normal losses. The grading process costs N$7 000 per month and NS0.10 per kilo of jatropha seeds graded. The poor quality seeds are processed further at a cost of N$2 per kilo into cosmetic paste that is sold for NS3 per kilo. ortver After the grading, the high quality seeds are then ground to prepare them for extraction of bio diesel and bio kerosene. A liquefying chemical is applied to the ground seeds and the cost of this chemical is NS20 per litre Two litres of the chemical are required for every 1 000 kilos of ground seeded cooking oil. Since this chemical is a dissolving chemical, it does not add to the weight of the ground seeds. Other costs incurred in the processing department is fixed manufacturing overheads of N$10 000 per month. The average output from the processing department is 40% bio diesel and 60% bio kerosene. The bio diesel is sold as is to clients at NS5 per litre while the (bio kerosene must be processed further to make it super refined for use in jet engines. The costs relating to the further processing of bio kerosene amount to N$0.30 per litre and the output of the further processing is 90% of refined bio kerosene, which is sold at N$4.50 per litre. 10% of the output is a waste product that is sold at N$5 per litre as a pesticide after further processing costs of N$3 per litre and fixed cost of NS9 977 per month has been incurred. It is company policy to value inventory on the basis of First In, First Out (FIFO) and to deduct the net realisable value (NRV) of by products from the joint productions costs. Joint costs are allocated to joint products using the NRV method, Page 3 of 7 0 The sales were as follows: Bio-diesel Refined bio kerosene Note: 1 kilo=1 litre, therefore 1 000 kilos of input (jatropha seeds) yield 1 000 litres of output. Cosmetic paste (by product) Pesticides (by product) The only opening inventory was 30 000 litres of bio kerosene valued at N$0.80 per litre. There was no beginning or closing inventory work-in-process on hand. REQUIRED: 3.1 3.2 Prepare a schedule showing the joints costs allocated to the joint products for September 2021. 3.3 Total Determine the production cost per unit for each of the two joint products for September 2021 (round to two decimal places). Calculate the gross profit per joint product for September 2021 (round total values to the nearest N$), 160 000 litre 260 000 litre 20 000 litre 25 000 litre Units sold Revenue Cost of sales Materials Labour Factory overhead Gross profit Period costs Selling and distributions Administrative expenses Operating income Actual 40 000 2 360 000 (1 732 000) 760 000 632 000 340 000 628 000 (348 800) 128 800 220 000 279 200 Sub- Total QUESTION 4 (20 MARKS, 36 MINUTES) The management of BETA Limited developed the following static budget for one of its flagship product, and estimated that 30,000 units would be sold during the month of August 2021. Static budget 30 000 N$ 1 800 000 (1 290 000) 600 000 450 000 240 000 Marks 510 000 (320 000) 120 000 200 000 190 000 9 2 4 Total 15 9 11 15 Page 4 of 7 However, due to an expected increase in demand 40 000 units were sold. Since the sales figures are higher than expected the management needs to analyse all variances and decide whether a future revision of its budgets would be appropriate. REQUIRED: 4.1. 4.2 4.3 Calculate the following: (0) (ii) (iii) Actual Material cost per unit mp Labour cost per unit Selling price price per unit. Based on the information provided to you, what would be the appropriate recovery rate for factory overhead? Prepare a flexible budgeted statement for comprehensive incomes for 40 000 units using the above information from a static budget for 30 000 units showing clearly columns disclosing information for actual, flexed and variance. Denote the variance with U for unfavourable and F for favourable. Sales and production volume Standard selling price per barrel Standard variable cost per barrel Sales and production volume. Actual selling price per barrel Actual variable cost per barrel Marks Additional information: Standard cost card for one barrel of solvent Direct materials Direct labour Variable overheads NB: Overheads are absorbed on the basis of direct labour hours. 3 QUESTION 5 (20 MARKS, 36 MINUTES) Elso Ltd ("Elso") manufactures large-scale solvents for factories and household cleaning. The company uses standard costing system as a way of monitoring its cost. The following information is available for Elso for the month of August 2021: Budgeted 1 16 20 600 barrels 20 N$1 750 2 kards N$855 620 barrels N$1 690 N$863 34 litres @ N$15 per litre 15 hours @ N$12,50 per hour 15 hours @ N$10,50 per hour Page 5 of 7 Actual cost and usage information Direct materials Direct labour Variable overheads Total usage 20 410 litres 9 420 hours REQUIRED: Calculate the following variances and indicate whether the variance obtained s favourable or unfavourable. 5.1. Material price variance BP-SP x) SR 5.2. Material usage variance a-5Q) off 5.3. Labour rate variance 5.4. Labour efficiency variance 5.5, Variable overheads expenditure variance Total cost (NS) N$321 500 N$117 800 N$95 600 5.6. Variable overheads efficiency variance 5.7. Explain the possible causes of the type of variance obtained in 5.1 and 5.37 TOTAL MARKS MARKS 3 3 3 3 3 2 20 Page 6 of 7 QUESTION 6 (10 MARKS, 18 MINUTES) The following selected data relate to the Mexit Division of Swifty Enterprises (SE): Sales revenue Uncontrollable fixed costs traceable to the division Allocated corporate overhead Controllable fixed costs traceable to the division Variable costs REQUIRED: 6.1. 6.2. 6.3. 6.4. Compute the following for the Mexit Division: a. Segment contribution margin: b. Controllable profit margin: N$4,580,000 1,360,000 590,000 1,120,000 40% c. Segment profit margin. When analyzing the Mexit Division as a resource investment for SE, which of the three measures should be used? Why? Assume that Mexit's management decided to construct a segmented income statement that reflected the company's five operating departments. Is it possible to trace all of the N$1,120,000 in controllable fixed costs to the departments? Explain briefly. Which of the five dollar values stated in the body of the problem would be utilized to calculate Swifty Enterprises' income before taxes? TOTAL MARKS <<<END OF QUESTION PAPER>>>> MARKS 2 1 2 1 10 Page 7 d

Expert Answer:

Answer rating: 100% (QA)

Solution First we need to calculate working notes as follows under Production capacity Normal capaci... View the full answer

Related Book For

Fraud examination

ISBN: 978-0538470841

4th edition

Authors: Steve Albrecht, Chad Albrecht, Conan Albrecht, Mark zimbelma

Posted Date:

Students also viewed these accounting questions

-

You are hired as a marketing intern at Green Airport. It's your first week on the job and your boss just walked into your office announcing the recipients of the Air Service Development Fund (Warwick...

-

You have been hired as a marketing research analyst by a major industrial marketing company in the country. Your boss, the market research manager, is a high powered statistician who does not believe...

-

You have been hired as a marketing research analyst by a major consumer marketing company in the country. Your boss, the project director, is not well trained in statistical methods and wonders why...

-

Superior Gaming, a computer enhancement company, has three product lines: audio enhancers, video enhancers, and connection-speed accelerators. Common costs are allocated based on relative sales. A...

-

Discuss the relationship between attributes and entities.

-

Bob Forrester is retired and owns a home. He has these assets and liabilities. a. Calculate Bob's net worth. b. Two years ago, Bob's net worth was $650,000. Last year, his net worth as $740,500. What...

-

Refer to Samsungs financial statements in Appendix A. Compute its debt ratio as of December 31, 2015, and December 31, 2014. Data From Samsung Financial Statement Appendix A Samsung Electronics Co.,...

-

In the month of June, Jose Heberts Beauty Salon gave 4,000 haircuts, shampoos, and permanents at an average price of $30. During the month, fixed costs were $16,800 and variable costs were 75% of...

-

A beam of light travels from a vacuum into water at an angle of 45. The light has a frequency of 6.00 x 1014 Hz and travels at a speed of 2.26 x 108 m/s in water. The speed of light in a vacuum is...

-

An investor, wants to know how two portfolios are performing in the market: 7% Y (3%) 12% Probability Market portfolio 0.40 0.20 15% 0.40 Beta factor 10% 18% Portfolio X 1.30 10% 8% 4% 0.75 1 The...

-

Subject: Application of Integrals- Volumes of Solid of revolution Answer the following: Show complete solution and show each graph 1. Find the volume of solid generated by the are bounded by x =...

-

If a bridge with steel expansion joints expands 0.30 m on a hot day (T = 25C), what is the original length of the bridge? Convert your answer from meters to kilometers

-

The skier is going down a 3 0 - degree grade. His mass with his equipment is 8 9 kg . Using a drag coefficient of 0 . 7 8 , an area of 1 . 1 m 2 , and an air density of 0 . 8 4 kg / m 3 will be his...

-

Nuclear reactor uses 'moderator' materials such as graphite to to eliminate thermal neutrons to reduce the speed of fast neutrons increase the number of fast neutrons to cause -235 to split ?Explain

-

Melissa Jasmine is a Marketing Manager at Metro Prima Berhad (MPB) which is one of the best media and television services companies in Malaysia. She has more than 15 years of working experience in...

-

A photon collides with an initially stationary free particle. If the initial total energies of the photon and the particle are Ep and Ee , respectively, determine the minimum total energy ( in terms...

-

Forecasted Industry Growth Rate = 15% Companies Market Share Post Types 2019 Sales 40% Square $400 M 40% Round $400 M 20% Square $200 M 100% N/A $1 B A B C Totals 60% Post Innovations (a new entrant...

-

Diamond Walker sells homemade knit scarves for $25 each at local craft shows. Her contribution margin ratio is 60%. Currently, the craft show entrance fees cost Diamond $1,500 per year. The craft...

-

1. Fraud perpetrators: a. Look like other criminals. b. Have profiles that look like most honest people. c. Are usually very young. d. Are none of the above. 2. Which of the following is not one of...

-

(True and fasle) 1. Fraud perpetrators are often those who are least suspected and most trusted. 2. Unintentional errors in financial statements are a form of fraud. 3. Occupational fraud is fraud...

-

In what ways can organizations conduct proactive fraud auditing?

-

Data from the last nine decades for the broad U.S. equity market yield the following statistics: average excess return, 8.3%; standard deviation, 20.1%. a. To the extent that these averages...

-

Suppose that the risk premium on the market portfolio is estimated at 8% with a standard deviation of 22%. What is the risk premium on a portfolio invested 25% in Toyota and 75% in Ford if they have...

-

Stock XYZ has an expected return of 12% and risk of = 1. Stock ABC has expected return of 13% and = 1.5. The markets expected return is 11%, and rf = 5%. a. According to the CAPM, which stock is a...

Study smarter with the SolutionInn App