You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

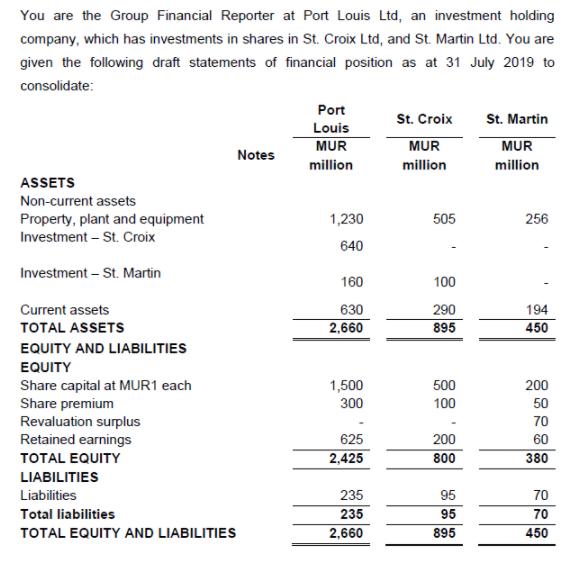

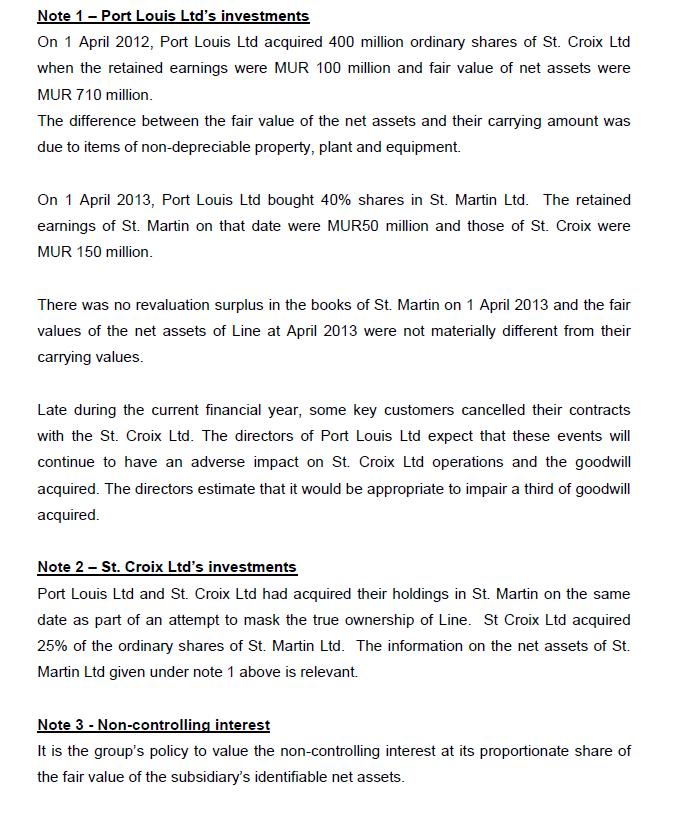

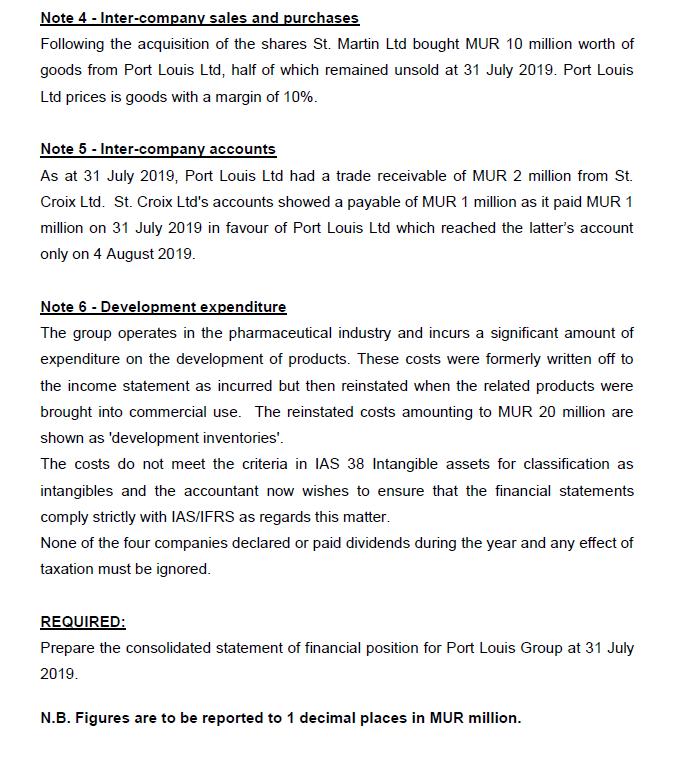

You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and St. Martin Ltd. You are given the following draft statements of financial position as at 31 July 2019 to consolidate: Port St. Croix St. Martin Louis MUR MUR MUR Notes million million million ASSETS Non-current assets Property, plant and equipment Investment – St. Croix 1,230 505 256 640 Investment – St. Martin 160 100 Current assets 630 290 194 TOTAL ASSETS 2,660 895 450 EQUITY AND LIABILITIES EQUITY 1,500 Share capital at MUR1 each Share premium Revaluation surplus Retained earnings 500 200 300 100 50 70 625 200 60 TOTAL EQUITY 2,425 800 380 LIABILITIES Liabilities 235 95 70 Total liabilities 235 95 70 TOTAL EQUITY AND LIABILITIES 2,660 895 450 Note 1- Port Louis Ltd's investments On 1 April 2012, Port Louis Ltd acquired 400 million ordinary shares of St. Croix Ltd when the retained earnings were MUR 100 million and fair value of net assets were MUR 710 million. The difference between the fair value of the net assets and their carrying amount was due to items of non-depreciable property, plant and equipment. On 1 April 2013, Port Louis Ltd bought 40% shares in St. Martin Ltd. The retained earnings of St. Martin on that date were MUR50 million and those of St. Croix were MUR 150 million. There was no revaluation surplus in the books of St. Martin on 1 April 2013 and the fair values of the net assets of Line at April 2013 were not materially different from their carrying values. Late during the current financial year, some key customers cancelled their contracts with the St. Croix Ltd. The directors of Port Louis Ltd expect that these events will continue to have an adverse impact on St. Croix Ltd operations and the goodwill acquired. The directors estimate that it would be appropriate to impair a third of goodwill acquired. Note 2 - St. Croix Ltd's investments Port Louis Ltd and St. Croix Ltd had acquired their holdings in St. Martin on the same date as part of an attempt to mask the true ownership of Line. St Croix Ltd acquired 25% of the ordinary shares of St. Martin Ltd. The information on the net assets of St. Martin Ltd given under note 1 above is relevant. Note 3 - Non-controlling interest It is the group's policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary's identifiable net assets. Note 4 - Inter-company sales and purchases Following the acquisition of the shares St. Martin Ltd bought MUR 10 million worth of goods from Port Louis Ltd, half of which remained unsold at 31 July 2019. Port Louis Ltd prices is goods with a margin of 10%. Note 5 - Inter-company accounts As at 31 July 2019, Port Louis Ltd had a trade receivable of MUR 2 million from St. Croix Ltd. St. Croix Ltd's accounts showed a payable of MUR 1 million as it paid MUR 1 million on 31 July 2019 in favour of Port Louis Ltd which reached the latter's account only on 4 August 2019. Note 6 - Development expenditure The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs amounting to MUR 20 million are shown as 'development inventories'. The costs do not meet the criteria in IAS 38 Intangible assets for classification as intangibles and the accountant now wishes to ensure that the financial statements comply strictly with IAS/IFRS as regards this matter. None of the four companies declared or paid dividends during the year and any effect of taxation must be ignored. REQUIRED: Prepare the consolidated statement of financial position for Port Louis Group at 31 July 2019. N.B. Figures are to be reported to 1 decimal places in MUR million. You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and St. Martin Ltd. You are given the following draft statements of financial position as at 31 July 2019 to consolidate: Port St. Croix St. Martin Louis MUR MUR MUR Notes million million million ASSETS Non-current assets Property, plant and equipment Investment – St. Croix 1,230 505 256 640 Investment – St. Martin 160 100 Current assets 630 290 194 TOTAL ASSETS 2,660 895 450 EQUITY AND LIABILITIES EQUITY 1,500 Share capital at MUR1 each Share premium Revaluation surplus Retained earnings 500 200 300 100 50 70 625 200 60 TOTAL EQUITY 2,425 800 380 LIABILITIES Liabilities 235 95 70 Total liabilities 235 95 70 TOTAL EQUITY AND LIABILITIES 2,660 895 450 Note 1- Port Louis Ltd's investments On 1 April 2012, Port Louis Ltd acquired 400 million ordinary shares of St. Croix Ltd when the retained earnings were MUR 100 million and fair value of net assets were MUR 710 million. The difference between the fair value of the net assets and their carrying amount was due to items of non-depreciable property, plant and equipment. On 1 April 2013, Port Louis Ltd bought 40% shares in St. Martin Ltd. The retained earnings of St. Martin on that date were MUR50 million and those of St. Croix were MUR 150 million. There was no revaluation surplus in the books of St. Martin on 1 April 2013 and the fair values of the net assets of Line at April 2013 were not materially different from their carrying values. Late during the current financial year, some key customers cancelled their contracts with the St. Croix Ltd. The directors of Port Louis Ltd expect that these events will continue to have an adverse impact on St. Croix Ltd operations and the goodwill acquired. The directors estimate that it would be appropriate to impair a third of goodwill acquired. Note 2 - St. Croix Ltd's investments Port Louis Ltd and St. Croix Ltd had acquired their holdings in St. Martin on the same date as part of an attempt to mask the true ownership of Line. St Croix Ltd acquired 25% of the ordinary shares of St. Martin Ltd. The information on the net assets of St. Martin Ltd given under note 1 above is relevant. Note 3 - Non-controlling interest It is the group's policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary's identifiable net assets. Note 4 - Inter-company sales and purchases Following the acquisition of the shares St. Martin Ltd bought MUR 10 million worth of goods from Port Louis Ltd, half of which remained unsold at 31 July 2019. Port Louis Ltd prices is goods with a margin of 10%. Note 5 - Inter-company accounts As at 31 July 2019, Port Louis Ltd had a trade receivable of MUR 2 million from St. Croix Ltd. St. Croix Ltd's accounts showed a payable of MUR 1 million as it paid MUR 1 million on 31 July 2019 in favour of Port Louis Ltd which reached the latter's account only on 4 August 2019. Note 6 - Development expenditure The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs amounting to MUR 20 million are shown as 'development inventories'. The costs do not meet the criteria in IAS 38 Intangible assets for classification as intangibles and the accountant now wishes to ensure that the financial statements comply strictly with IAS/IFRS as regards this matter. None of the four companies declared or paid dividends during the year and any effect of taxation must be ignored. REQUIRED: Prepare the consolidated statement of financial position for Port Louis Group at 31 July 2019. N.B. Figures are to be reported to 1 decimal places in MUR million. You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and St. Martin Ltd. You are given the following draft statements of financial position as at 31 July 2019 to consolidate: Port St. Croix St. Martin Louis MUR MUR MUR Notes million million million ASSETS Non-current assets Property, plant and equipment Investment – St. Croix 1,230 505 256 640 Investment – St. Martin 160 100 Current assets 630 290 194 TOTAL ASSETS 2,660 895 450 EQUITY AND LIABILITIES EQUITY 1,500 Share capital at MUR1 each Share premium Revaluation surplus Retained earnings 500 200 300 100 50 70 625 200 60 TOTAL EQUITY 2,425 800 380 LIABILITIES Liabilities 235 95 70 Total liabilities 235 95 70 TOTAL EQUITY AND LIABILITIES 2,660 895 450 Note 1- Port Louis Ltd's investments On 1 April 2012, Port Louis Ltd acquired 400 million ordinary shares of St. Croix Ltd when the retained earnings were MUR 100 million and fair value of net assets were MUR 710 million. The difference between the fair value of the net assets and their carrying amount was due to items of non-depreciable property, plant and equipment. On 1 April 2013, Port Louis Ltd bought 40% shares in St. Martin Ltd. The retained earnings of St. Martin on that date were MUR50 million and those of St. Croix were MUR 150 million. There was no revaluation surplus in the books of St. Martin on 1 April 2013 and the fair values of the net assets of Line at April 2013 were not materially different from their carrying values. Late during the current financial year, some key customers cancelled their contracts with the St. Croix Ltd. The directors of Port Louis Ltd expect that these events will continue to have an adverse impact on St. Croix Ltd operations and the goodwill acquired. The directors estimate that it would be appropriate to impair a third of goodwill acquired. Note 2 - St. Croix Ltd's investments Port Louis Ltd and St. Croix Ltd had acquired their holdings in St. Martin on the same date as part of an attempt to mask the true ownership of Line. St Croix Ltd acquired 25% of the ordinary shares of St. Martin Ltd. The information on the net assets of St. Martin Ltd given under note 1 above is relevant. Note 3 - Non-controlling interest It is the group's policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary's identifiable net assets. Note 4 - Inter-company sales and purchases Following the acquisition of the shares St. Martin Ltd bought MUR 10 million worth of goods from Port Louis Ltd, half of which remained unsold at 31 July 2019. Port Louis Ltd prices is goods with a margin of 10%. Note 5 - Inter-company accounts As at 31 July 2019, Port Louis Ltd had a trade receivable of MUR 2 million from St. Croix Ltd. St. Croix Ltd's accounts showed a payable of MUR 1 million as it paid MUR 1 million on 31 July 2019 in favour of Port Louis Ltd which reached the latter's account only on 4 August 2019. Note 6 - Development expenditure The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs amounting to MUR 20 million are shown as 'development inventories'. The costs do not meet the criteria in IAS 38 Intangible assets for classification as intangibles and the accountant now wishes to ensure that the financial statements comply strictly with IAS/IFRS as regards this matter. None of the four companies declared or paid dividends during the year and any effect of taxation must be ignored. REQUIRED: Prepare the consolidated statement of financial position for Port Louis Group at 31 July 2019. N.B. Figures are to be reported to 1 decimal places in MUR million. You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and St. Martin Ltd. You are given the following draft statements of financial position as at 31 July 2019 to consolidate: Port St. Croix St. Martin Louis MUR MUR MUR Notes million million million ASSETS Non-current assets Property, plant and equipment Investment – St. Croix 1,230 505 256 640 Investment – St. Martin 160 100 Current assets 630 290 194 TOTAL ASSETS 2,660 895 450 EQUITY AND LIABILITIES EQUITY 1,500 Share capital at MUR1 each Share premium Revaluation surplus Retained earnings 500 200 300 100 50 70 625 200 60 TOTAL EQUITY 2,425 800 380 LIABILITIES Liabilities 235 95 70 Total liabilities 235 95 70 TOTAL EQUITY AND LIABILITIES 2,660 895 450 Note 1- Port Louis Ltd's investments On 1 April 2012, Port Louis Ltd acquired 400 million ordinary shares of St. Croix Ltd when the retained earnings were MUR 100 million and fair value of net assets were MUR 710 million. The difference between the fair value of the net assets and their carrying amount was due to items of non-depreciable property, plant and equipment. On 1 April 2013, Port Louis Ltd bought 40% shares in St. Martin Ltd. The retained earnings of St. Martin on that date were MUR50 million and those of St. Croix were MUR 150 million. There was no revaluation surplus in the books of St. Martin on 1 April 2013 and the fair values of the net assets of Line at April 2013 were not materially different from their carrying values. Late during the current financial year, some key customers cancelled their contracts with the St. Croix Ltd. The directors of Port Louis Ltd expect that these events will continue to have an adverse impact on St. Croix Ltd operations and the goodwill acquired. The directors estimate that it would be appropriate to impair a third of goodwill acquired. Note 2 - St. Croix Ltd's investments Port Louis Ltd and St. Croix Ltd had acquired their holdings in St. Martin on the same date as part of an attempt to mask the true ownership of Line. St Croix Ltd acquired 25% of the ordinary shares of St. Martin Ltd. The information on the net assets of St. Martin Ltd given under note 1 above is relevant. Note 3 - Non-controlling interest It is the group's policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary's identifiable net assets. Note 4 - Inter-company sales and purchases Following the acquisition of the shares St. Martin Ltd bought MUR 10 million worth of goods from Port Louis Ltd, half of which remained unsold at 31 July 2019. Port Louis Ltd prices is goods with a margin of 10%. Note 5 - Inter-company accounts As at 31 July 2019, Port Louis Ltd had a trade receivable of MUR 2 million from St. Croix Ltd. St. Croix Ltd's accounts showed a payable of MUR 1 million as it paid MUR 1 million on 31 July 2019 in favour of Port Louis Ltd which reached the latter's account only on 4 August 2019. Note 6 - Development expenditure The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs amounting to MUR 20 million are shown as 'development inventories'. The costs do not meet the criteria in IAS 38 Intangible assets for classification as intangibles and the accountant now wishes to ensure that the financial statements comply strictly with IAS/IFRS as regards this matter. None of the four companies declared or paid dividends during the year and any effect of taxation must be ignored. REQUIRED: Prepare the consolidated statement of financial position for Port Louis Group at 31 July 2019. N.B. Figures are to be reported to 1 decimal places in MUR million. You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and St. Martin Ltd. You are given the following draft statements of financial position as at 31 July 2019 to consolidate: Port St. Croix St. Martin Louis MUR MUR MUR Notes million million million ASSETS Non-current assets Property, plant and equipment Investment – St. Croix 1,230 505 256 640 Investment – St. Martin 160 100 Current assets 630 290 194 TOTAL ASSETS 2,660 895 450 EQUITY AND LIABILITIES EQUITY 1,500 Share capital at MUR1 each Share premium Revaluation surplus Retained earnings 500 200 300 100 50 70 625 200 60 TOTAL EQUITY 2,425 800 380 LIABILITIES Liabilities 235 95 70 Total liabilities 235 95 70 TOTAL EQUITY AND LIABILITIES 2,660 895 450 Note 1- Port Louis Ltd's investments On 1 April 2012, Port Louis Ltd acquired 400 million ordinary shares of St. Croix Ltd when the retained earnings were MUR 100 million and fair value of net assets were MUR 710 million. The difference between the fair value of the net assets and their carrying amount was due to items of non-depreciable property, plant and equipment. On 1 April 2013, Port Louis Ltd bought 40% shares in St. Martin Ltd. The retained earnings of St. Martin on that date were MUR50 million and those of St. Croix were MUR 150 million. There was no revaluation surplus in the books of St. Martin on 1 April 2013 and the fair values of the net assets of Line at April 2013 were not materially different from their carrying values. Late during the current financial year, some key customers cancelled their contracts with the St. Croix Ltd. The directors of Port Louis Ltd expect that these events will continue to have an adverse impact on St. Croix Ltd operations and the goodwill acquired. The directors estimate that it would be appropriate to impair a third of goodwill acquired. Note 2 - St. Croix Ltd's investments Port Louis Ltd and St. Croix Ltd had acquired their holdings in St. Martin on the same date as part of an attempt to mask the true ownership of Line. St Croix Ltd acquired 25% of the ordinary shares of St. Martin Ltd. The information on the net assets of St. Martin Ltd given under note 1 above is relevant. Note 3 - Non-controlling interest It is the group's policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary's identifiable net assets. Note 4 - Inter-company sales and purchases Following the acquisition of the shares St. Martin Ltd bought MUR 10 million worth of goods from Port Louis Ltd, half of which remained unsold at 31 July 2019. Port Louis Ltd prices is goods with a margin of 10%. Note 5 - Inter-company accounts As at 31 July 2019, Port Louis Ltd had a trade receivable of MUR 2 million from St. Croix Ltd. St. Croix Ltd's accounts showed a payable of MUR 1 million as it paid MUR 1 million on 31 July 2019 in favour of Port Louis Ltd which reached the latter's account only on 4 August 2019. Note 6 - Development expenditure The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs amounting to MUR 20 million are shown as 'development inventories'. The costs do not meet the criteria in IAS 38 Intangible assets for classification as intangibles and the accountant now wishes to ensure that the financial statements comply strictly with IAS/IFRS as regards this matter. None of the four companies declared or paid dividends during the year and any effect of taxation must be ignored. REQUIRED: Prepare the consolidated statement of financial position for Port Louis Group at 31 July 2019. N.B. Figures are to be reported to 1 decimal places in MUR million. You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and St. Martin Ltd. You are given the following draft statements of financial position as at 31 July 2019 to consolidate: Port St. Croix St. Martin Louis MUR MUR MUR Notes million million million ASSETS Non-current assets Property, plant and equipment Investment – St. Croix 1,230 505 256 640 Investment – St. Martin 160 100 Current assets 630 290 194 TOTAL ASSETS 2,660 895 450 EQUITY AND LIABILITIES EQUITY 1,500 Share capital at MUR1 each Share premium Revaluation surplus Retained earnings 500 200 300 100 50 70 625 200 60 TOTAL EQUITY 2,425 800 380 LIABILITIES Liabilities 235 95 70 Total liabilities 235 95 70 TOTAL EQUITY AND LIABILITIES 2,660 895 450 Note 1- Port Louis Ltd's investments On 1 April 2012, Port Louis Ltd acquired 400 million ordinary shares of St. Croix Ltd when the retained earnings were MUR 100 million and fair value of net assets were MUR 710 million. The difference between the fair value of the net assets and their carrying amount was due to items of non-depreciable property, plant and equipment. On 1 April 2013, Port Louis Ltd bought 40% shares in St. Martin Ltd. The retained earnings of St. Martin on that date were MUR50 million and those of St. Croix were MUR 150 million. There was no revaluation surplus in the books of St. Martin on 1 April 2013 and the fair values of the net assets of Line at April 2013 were not materially different from their carrying values. Late during the current financial year, some key customers cancelled their contracts with the St. Croix Ltd. The directors of Port Louis Ltd expect that these events will continue to have an adverse impact on St. Croix Ltd operations and the goodwill acquired. The directors estimate that it would be appropriate to impair a third of goodwill acquired. Note 2 - St. Croix Ltd's investments Port Louis Ltd and St. Croix Ltd had acquired their holdings in St. Martin on the same date as part of an attempt to mask the true ownership of Line. St Croix Ltd acquired 25% of the ordinary shares of St. Martin Ltd. The information on the net assets of St. Martin Ltd given under note 1 above is relevant. Note 3 - Non-controlling interest It is the group's policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary's identifiable net assets. Note 4 - Inter-company sales and purchases Following the acquisition of the shares St. Martin Ltd bought MUR 10 million worth of goods from Port Louis Ltd, half of which remained unsold at 31 July 2019. Port Louis Ltd prices is goods with a margin of 10%. Note 5 - Inter-company accounts As at 31 July 2019, Port Louis Ltd had a trade receivable of MUR 2 million from St. Croix Ltd. St. Croix Ltd's accounts showed a payable of MUR 1 million as it paid MUR 1 million on 31 July 2019 in favour of Port Louis Ltd which reached the latter's account only on 4 August 2019. Note 6 - Development expenditure The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs amounting to MUR 20 million are shown as 'development inventories'. The costs do not meet the criteria in IAS 38 Intangible assets for classification as intangibles and the accountant now wishes to ensure that the financial statements comply strictly with IAS/IFRS as regards this matter. None of the four companies declared or paid dividends during the year and any effect of taxation must be ignored. REQUIRED: Prepare the consolidated statement of financial position for Port Louis Group at 31 July 2019. N.B. Figures are to be reported to 1 decimal places in MUR million. You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and St. Martin Ltd. You are given the following draft statements of financial position as at 31 July 2019 to consolidate: Port St. Croix St. Martin Louis MUR MUR MUR Notes million million million ASSETS Non-current assets Property, plant and equipment Investment – St. Croix 1,230 505 256 640 Investment – St. Martin 160 100 Current assets 630 290 194 TOTAL ASSETS 2,660 895 450 EQUITY AND LIABILITIES EQUITY 1,500 Share capital at MUR1 each Share premium Revaluation surplus Retained earnings 500 200 300 100 50 70 625 200 60 TOTAL EQUITY 2,425 800 380 LIABILITIES Liabilities 235 95 70 Total liabilities 235 95 70 TOTAL EQUITY AND LIABILITIES 2,660 895 450 Note 1- Port Louis Ltd's investments On 1 April 2012, Port Louis Ltd acquired 400 million ordinary shares of St. Croix Ltd when the retained earnings were MUR 100 million and fair value of net assets were MUR 710 million. The difference between the fair value of the net assets and their carrying amount was due to items of non-depreciable property, plant and equipment. On 1 April 2013, Port Louis Ltd bought 40% shares in St. Martin Ltd. The retained earnings of St. Martin on that date were MUR50 million and those of St. Croix were MUR 150 million. There was no revaluation surplus in the books of St. Martin on 1 April 2013 and the fair values of the net assets of Line at April 2013 were not materially different from their carrying values. Late during the current financial year, some key customers cancelled their contracts with the St. Croix Ltd. The directors of Port Louis Ltd expect that these events will continue to have an adverse impact on St. Croix Ltd operations and the goodwill acquired. The directors estimate that it would be appropriate to impair a third of goodwill acquired. Note 2 - St. Croix Ltd's investments Port Louis Ltd and St. Croix Ltd had acquired their holdings in St. Martin on the same date as part of an attempt to mask the true ownership of Line. St Croix Ltd acquired 25% of the ordinary shares of St. Martin Ltd. The information on the net assets of St. Martin Ltd given under note 1 above is relevant. Note 3 - Non-controlling interest It is the group's policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary's identifiable net assets. Note 4 - Inter-company sales and purchases Following the acquisition of the shares St. Martin Ltd bought MUR 10 million worth of goods from Port Louis Ltd, half of which remained unsold at 31 July 2019. Port Louis Ltd prices is goods with a margin of 10%. Note 5 - Inter-company accounts As at 31 July 2019, Port Louis Ltd had a trade receivable of MUR 2 million from St. Croix Ltd. St. Croix Ltd's accounts showed a payable of MUR 1 million as it paid MUR 1 million on 31 July 2019 in favour of Port Louis Ltd which reached the latter's account only on 4 August 2019. Note 6 - Development expenditure The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs amounting to MUR 20 million are shown as 'development inventories'. The costs do not meet the criteria in IAS 38 Intangible assets for classification as intangibles and the accountant now wishes to ensure that the financial statements comply strictly with IAS/IFRS as regards this matter. None of the four companies declared or paid dividends during the year and any effect of taxation must be ignored. REQUIRED: Prepare the consolidated statement of financial position for Port Louis Group at 31 July 2019. N.B. Figures are to be reported to 1 decimal places in MUR million. You are the Group Financial Reporter at Port Louis Ltd, an investment holding company, which has investments in shares in St. Croix Ltd, and St. Martin Ltd. You are given the following draft statements of financial position as at 31 July 2019 to consolidate: Port St. Croix St. Martin Louis MUR MUR MUR Notes million million million ASSETS Non-current assets Property, plant and equipment Investment – St. Croix 1,230 505 256 640 Investment – St. Martin 160 100 Current assets 630 290 194 TOTAL ASSETS 2,660 895 450 EQUITY AND LIABILITIES EQUITY 1,500 Share capital at MUR1 each Share premium Revaluation surplus Retained earnings 500 200 300 100 50 70 625 200 60 TOTAL EQUITY 2,425 800 380 LIABILITIES Liabilities 235 95 70 Total liabilities 235 95 70 TOTAL EQUITY AND LIABILITIES 2,660 895 450 Note 1- Port Louis Ltd's investments On 1 April 2012, Port Louis Ltd acquired 400 million ordinary shares of St. Croix Ltd when the retained earnings were MUR 100 million and fair value of net assets were MUR 710 million. The difference between the fair value of the net assets and their carrying amount was due to items of non-depreciable property, plant and equipment. On 1 April 2013, Port Louis Ltd bought 40% shares in St. Martin Ltd. The retained earnings of St. Martin on that date were MUR50 million and those of St. Croix were MUR 150 million. There was no revaluation surplus in the books of St. Martin on 1 April 2013 and the fair values of the net assets of Line at April 2013 were not materially different from their carrying values. Late during the current financial year, some key customers cancelled their contracts with the St. Croix Ltd. The directors of Port Louis Ltd expect that these events will continue to have an adverse impact on St. Croix Ltd operations and the goodwill acquired. The directors estimate that it would be appropriate to impair a third of goodwill acquired. Note 2 - St. Croix Ltd's investments Port Louis Ltd and St. Croix Ltd had acquired their holdings in St. Martin on the same date as part of an attempt to mask the true ownership of Line. St Croix Ltd acquired 25% of the ordinary shares of St. Martin Ltd. The information on the net assets of St. Martin Ltd given under note 1 above is relevant. Note 3 - Non-controlling interest It is the group's policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary's identifiable net assets. Note 4 - Inter-company sales and purchases Following the acquisition of the shares St. Martin Ltd bought MUR 10 million worth of goods from Port Louis Ltd, half of which remained unsold at 31 July 2019. Port Louis Ltd prices is goods with a margin of 10%. Note 5 - Inter-company accounts As at 31 July 2019, Port Louis Ltd had a trade receivable of MUR 2 million from St. Croix Ltd. St. Croix Ltd's accounts showed a payable of MUR 1 million as it paid MUR 1 million on 31 July 2019 in favour of Port Louis Ltd which reached the latter's account only on 4 August 2019. Note 6 - Development expenditure The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs amounting to MUR 20 million are shown as 'development inventories'. The costs do not meet the criteria in IAS 38 Intangible assets for classification as intangibles and the accountant now wishes to ensure that the financial statements comply strictly with IAS/IFRS as regards this matter. None of the four companies declared or paid dividends during the year and any effect of taxation must be ignored. REQUIRED: Prepare the consolidated statement of financial position for Port Louis Group at 31 July 2019. N.B. Figures are to be reported to 1 decimal places in MUR million.

Expert Answer:

Answer rating: 100% (QA)

PgNo1 Consolidated Statement of financial Position for Post Louis Gsup at 31071... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

The summarized statements of financial position as at 31 March 20X1 and 31 March 20X2 of Higher Ltd are as follows: Additional information 1. Non-current assets Non-current assets disposed of during...

-

The statement of financial position as at 31 December 20X2 of Zoom Products Ltd included: Trade receivables...............................85,360 The financial statements for the year ended 31...

-

+ The following are statements of financial position as at 31 December 20X7: Pascal Bhd. (RM) Assets Non-current assets: Property, plant and equipment Investments in Saville Sdn. Bhd: 720,00 units...

-

Perhaps more surprising to Mr. Pitkin was a proposal by the VP of Marketing to make a major investment in market share by increasing promotional expenditures by $2.5 million during 1998-2000. Sales...

-

Consider the following hypotheses: H 0 : = 140 H 1 : 140 Given that x = 148.1, s = 37.5, n = 20, and = 0.02, answer the following questions: a. What conclusion should be drawn? b. Use PHStat to...

-

Wine These data give ratings and prices of 257 red and white wines that appeared in Wine Spectator in 2009. For this analysis, we are interested in how the rating given to a wine is associated with...

-

Given that \(f(x)=\frac{k}{2^{x}}\) is a probability distribution for a random variable that can take on the values \(x=\) \(0,1,2,3\), and 4 , find \(k\).

-

Identifying suitable market segments and selecting targets are critical to the success of any marketing plan. As Jane Melodys assistant, youre responsible for market segmentation and targeting. Look...

-

Image transcription text FILE NUMBER : . . . . . . . . . . .. . ...' J.W. & D.B. Craig . . . . . . . . . . ... .... GRADE NOTE: USE WITH NEXT THREE PAGES. PROB A NOTE: SKETCH PROB B PROBLEM...

-

Calculate the molar volume of saturated liquid and the molar volume of saturated vapor by the Redlich/Kwong equation for one of the following and compare results with values found by suitable...

-

A speculator thinks that the British pound will be at around $1.32/ (spot rate) by June 25. She notices that the put premium per British pound is $0.04 on January 1 (today), with a strike price of...

-

Presented below are selected ledger accounts of Woods Corporation at December 31, 2015. Cash $ 185,000 Salaries and wages expense (sales) $284,000 Inventory (beginning) 535,000 Salaries and wages...

-

The title of an article in The Wall Street Journal was Pricing of Products Is Still an Art, Often Having Little Link to Costs. In the article, the following cases were cited: Vodka pricing: All...

-

PharMerger is a pharmaceutical company with significant global presence in six continents and premises in 45 countries. The UK has two research and development sites, one of which is the subject of...

-

The International Labor Organization estimates that 250 million children in developing countries between the ages of 5 and 14 are working either full- or part-time. The estimate of the percentage of...

-

Lilikoi Corporation began business in 2015. Lilikoi earned taxable income of $40,000 in 2015 and $120,000 in 2016. For 2017, Lilikoi Corporation has a net operating loss of $50,000 and decides to...

-

Talk with three people to get their opinions on federal spending on energy, education, and defense. You may ask friends, family members, and other trusted adults. Ask them to rank the programs listed...

-

In Exercises delete part of the domain so that the function that remains is one-to-one. Find the inverse function of the remaining function and give the domain of the inverse function. f(x) = 16x4 -3...

-

Data You are employed as the assistant management accountant in the group accountant's office of Hampstead plc. Hampstead recently acquired Finchley Ltd, a small company making a specialist product...

-

(a) Flopro plc make and sell two products A and B, each of which passes through the same automated production operations. The following estimated information is available for period 1: (i) (ii)...

-

XY Limited commenced trading on 1 February with fully paid issued share capital of 500 000, Fixed Assets of 275 000 and Cash at Bank of 225 000. By the end of April, the following transactions had...

-

Maribel Ortiz is puzzled. Her company had a profit margin of 10% in 2025. She feels that this is an indication that the company is doing well. Gordon Liddy, her accountant, says that more information...

-

At December 31, 2025, the fair value of non-trading securities is 41,300 and the cost is 39,800. At January 1, 2025, there was a credit balance of 900 in the Fair Value Adjustment Non-Trading...

-

On January 1, 2025, Lennon Enterprises acquires 100% of Ono Ltd. for 220,000 in cash. The condensed statements of financial position of the two companies immediately following the acquisition are as...

Study smarter with the SolutionInn App