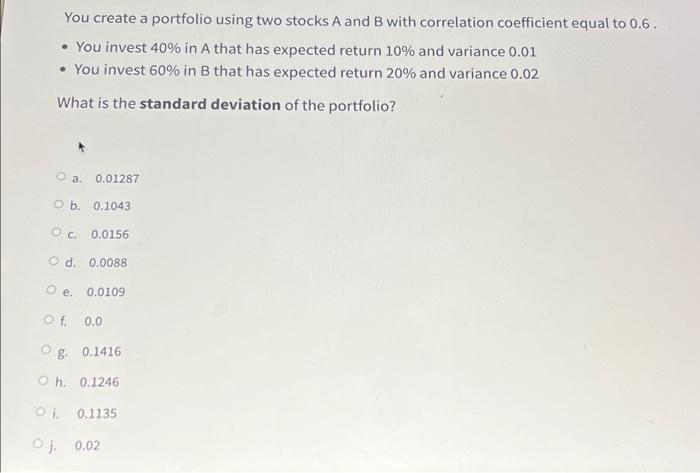

Question: You create a portfolio using two stocks A and B with correlation coefficient equal to 0.6 . - You invest 40% in A that has

You create a portfolio using two stocks A and B with correlation coefficient equal to 0.6 . - You invest 40% in A that has expected return 10% and variance 0.01 - You invest 60% in B that has expected return 20% and variance 0.02 What is the standard deviation of the portfolio? a. 0.01287 b. 0.1043 c. 0.0156 d. 0.0088 e. 0.0109 f. 0.0 g. 0.1416 h. 0.1246 i. 0.1135 i. 0.02

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock