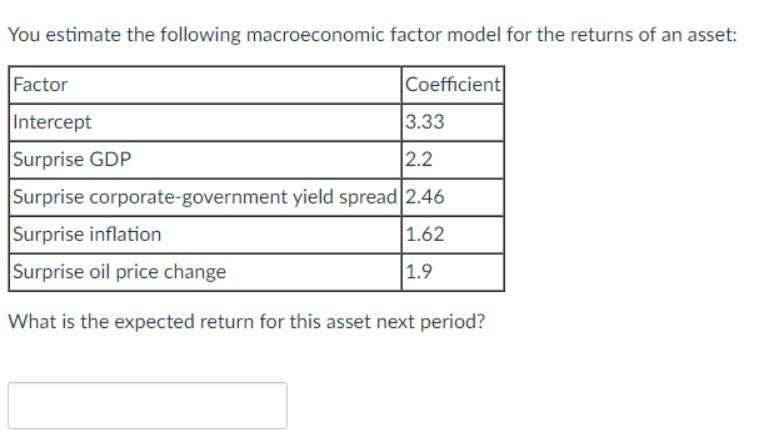

Question: You estimate the following macroeconomic factor model for the returns of an asset: Coefficient Factor Intercept 3.33 Surprise GDP 2.2 Surprise corporate-government yield spread

You estimate the following macroeconomic factor model for the returns of an asset: Coefficient Factor Intercept 3.33 Surprise GDP 2.2 Surprise corporate-government yield spread 2.46 Surprise inflation 1.62 Surprise oil price change 1.9 What is the expected return for this asset next period?

Step by Step Solution

★★★★★

3.38 Rating (145 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

To calculate the expected return for the asset next period using th... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock