Question: You need to form a portfolio using two risky assets. The correlation coefficient between Asset A and Asset B is 0 . 2 5 If

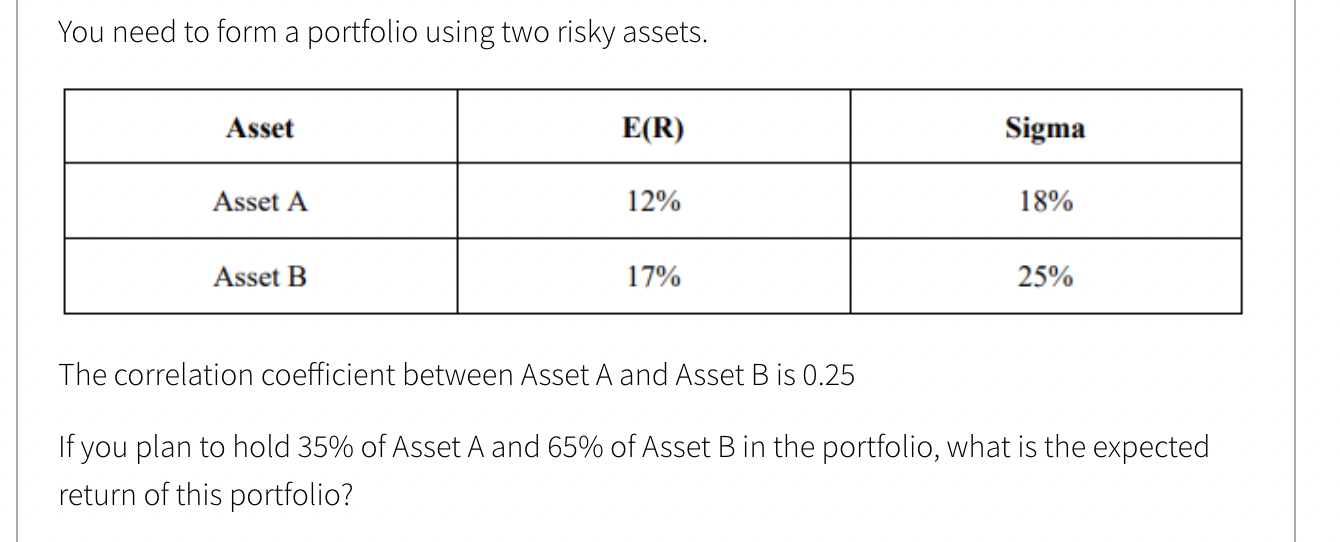

You need to form a portfolio using two risky assets.

The correlation coefficient between Asset A and Asset B is

If you plan to hold of Asset A and of Asset B in the portfolio,. Assume that riskfree rate is and your

degree of riskaversion is Now in addition to investing in these two risky assets, you can

also invest in the riskfree asset. What is the weight of each asset Asset A Asset B and the

riskfree asset in the optimal portfolio which gives you the highest utility?

Your utility function is

;;

;;

;;

;;

;;

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock