Question: YOUR BANK is thinking to issue a regular coupon bond (debenture) with following particulars: Maturity =3 years, Coupon rate =7.000%, Face value =$1,000.00, Coupon payments

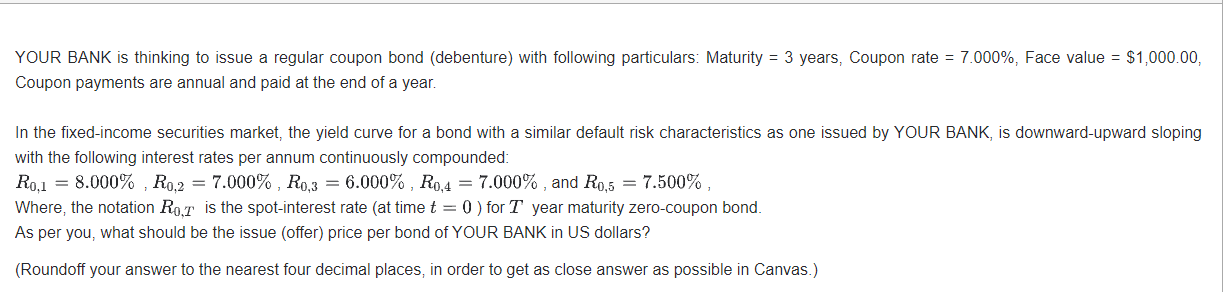

YOUR BANK is thinking to issue a regular coupon bond (debenture) with following particulars: Maturity =3 years, Coupon rate =7.000%, Face value =$1,000.00, Coupon payments are annual and paid at the end of a year. In the fixed-income securities market, the yield curve for a bond with a similar default risk characteristics as one issued by YOUR BANK, is downward-upward sloping with the following interest rates per annum continuously compounded: R0,1=8.000%,R0,2=7.000%,R0,3=6.000%,R0,4=7.000%, and R0,5=7.500%, Where, the notation R0,T is the spot-interest rate (at time t=0 ) for T year maturity zero-coupon bond. As per you, what should be the issue (offer) price per bond of YOUR BANK in US dollars? (Roundoff your answer to the nearest four decimal places, in order to get as close answer as possible in Canvas.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts