Question: Your client, Sandra is considering three assets: a bond mutual fund, a cryptocurrency ETF, and US Treasury bills. The annualized T-bill rate is 2%. The

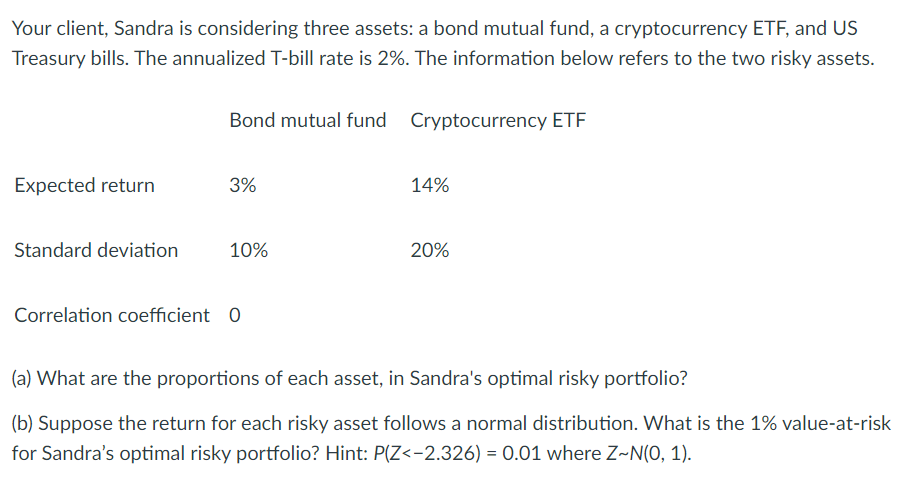

Your client, Sandra is considering three assets: a bond mutual fund, a cryptocurrency ETF, and US Treasury bills. The annualized T-bill rate is 2%. The information below refers to the two risky assets. Correlation coefficient 0 (a) What are the proportions of each asset, in Sandra's optimal risky portfolio? (b) Suppose the return for each risky asset follows a normal distribution. What is the 1% value-at-risk for Sandra's optimal risky portfolio? Hint: P(Z

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock