Your firm has been the external auditor of Habib Plastics Ltd (Habib) for five years. On 1

Question:

Your firm has been the external auditor of Habib Plastics Ltd (Habib) for five years. On 1 January 20X9, Ismail Habib sold his 100% shareholding in Habib to Ikram PLC (Ikram). Ikram immediately appointed a new board of directors. Your firm has accepted the new board's offer of reappointment as the auditor of Habib for the year ended 31 July 20X9.

You are the audit senior responsible for planning the audit of Habib. The engagement partner asked you to consider the following three key areas of audit risk:

(1) Land and buildings

(2) Plant and machinery

(3) Related party transactions

Habib manufactures disposable plastic products, such as cutlery, plates and straws. It sells its products to European distributors operating in the catering industry. In 20X8 the EU announced that it would ban a range of plastic items, such as those manufactured by Habib. The ban is expected to come into effect in 20Y1. In response to the announcement,

Habib invested in the development of a new range of disposable products made from materials which degrade quickly when disposed of. Habib believes that its new range will not be subject to the EU ban.

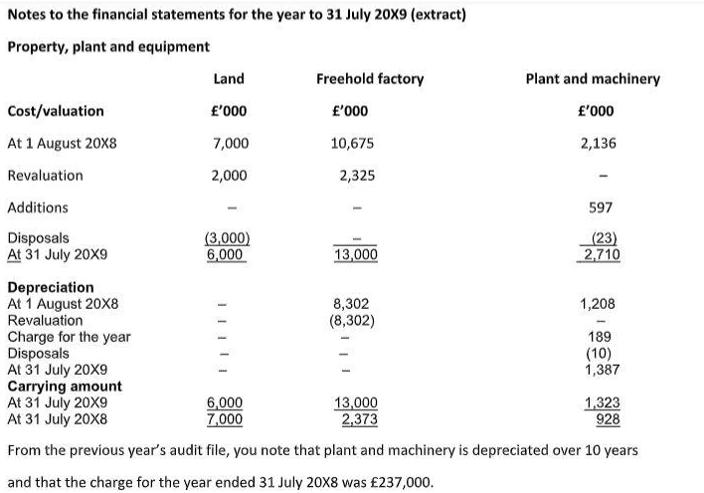

As part of your planning for the audit of the financial statements for the year ended 31 July 20X9, you met with Habib's new finance director, Angie, who provided you with the following

information:

⢠On 31 March 20X9, Habib sold part of the land where its factory is located to Neway Ltd (Neway). Habib's new chief executive is the majority shareholder of Neway.

⢠Habib's freehold factory and remaining land was revalued for the first time at 31 July 20X9 to make Habib's accounting policy consistent with that of Ikram. Angie obtained a valuation from ABC Associates, a firm of chartered surveyors where his wife, Olivia, is a partner. Habib has recognised this valuation in the financial statements for the year ended 31 July 20X9.

⢠To enable the manufacture of the new range of disposable products, Habib made several modifications to its production plant. Some components of the existing machinery were replaced. Habib has included the cost of the new components in plant and machinery. These components were purchased, in euros, from suppliers in Europe. The labour costs associated with making the modifications have also been included in plant and machinery.

⢠Habib's board has received a report from the Ikram's internal audit team, which recently conducted an audit of Habib's internal controls. The report identified the following internal control deficiencies:

(1) Several contracts negotiated with new customers during 20X9 have terms of trade which are more favourable to the customer than Habib's standard terms.

(2) Instances of management override were found in respect of the approval process for the purchase of machinery components. This included transactions with suppliers that are not on Habib's list of approved suppliers. Angie also provided you with the following financial information:

Â Â

Â

Ikram is audited by a different firm, Sahir & Co. Habib is a significant component of Ikram and financial information relating to Habib will be included in the Ikram group financial statements for the year ended 31 July 20X9. Your firm is required to cooperate with Sahir & Co.

Â

Requirements

(a) Describe the steps that your firm should have performed before accepting the board's request to continue as Habib's external auditor.

(b)Outline the potential consequences of each of the internal control deficiencies (a) and (b) above.

(c) List the requirements and information that you expect Sahir&Co, the external auditor of Ikram PLC, to include in its communication to your firm

Expert Answer:

SOLUTION a Steps that your firm should have performed before accepting the boards request to continue as Habibs external auditor Evaluate Independence Your firm should have assessed its independence t... View the full answer

Advanced Financial Accounting

ISBN: 978-0137030385

6th edition

Authors: Thomas Beechy, Umashanker Trivedi, Kenneth MacAulay