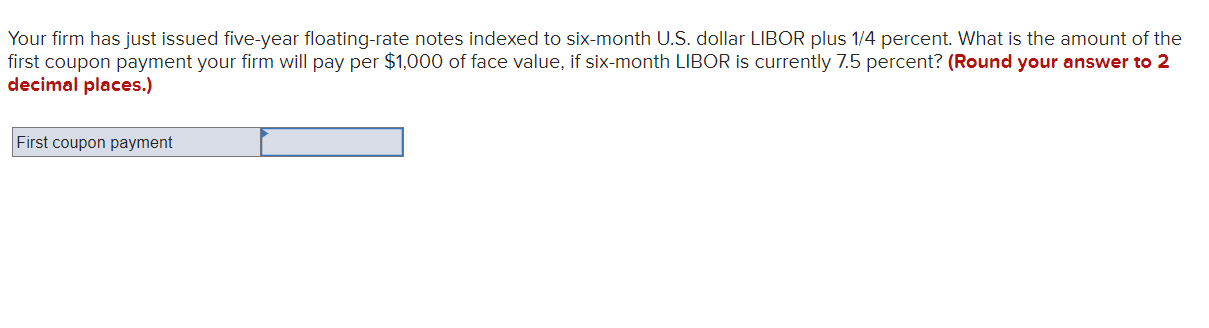

Question: Your firm has just issued five-year floating-rate notes indexed to six-month U.S. dollar LIBOR plus 1/4 percent. What is the amount of the first coupon

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts