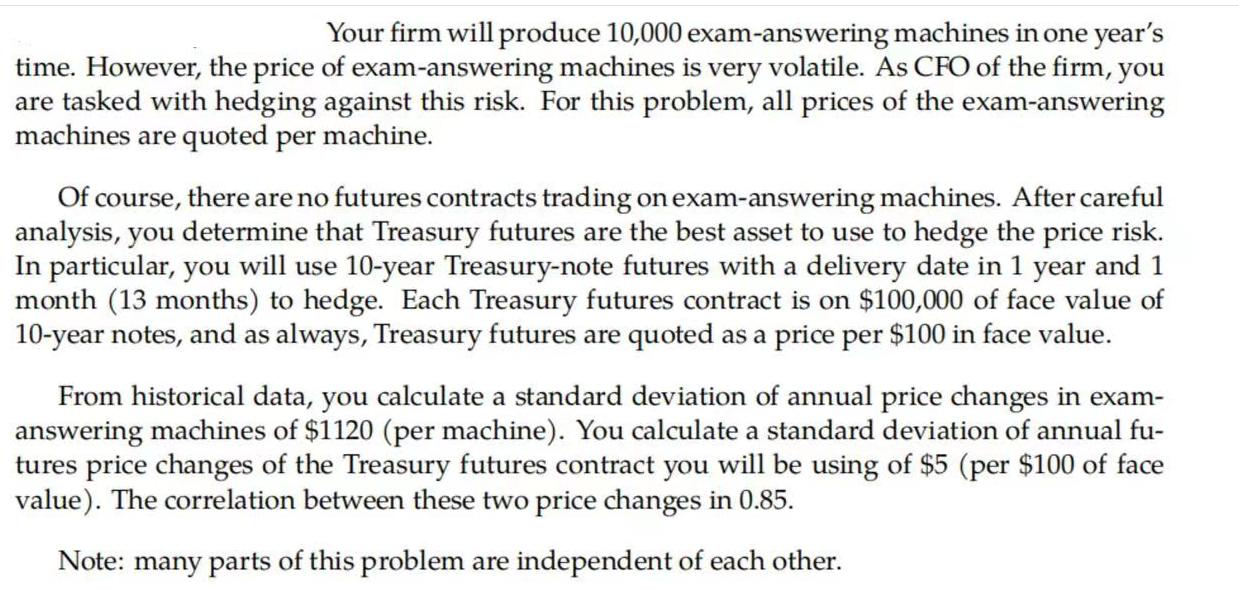

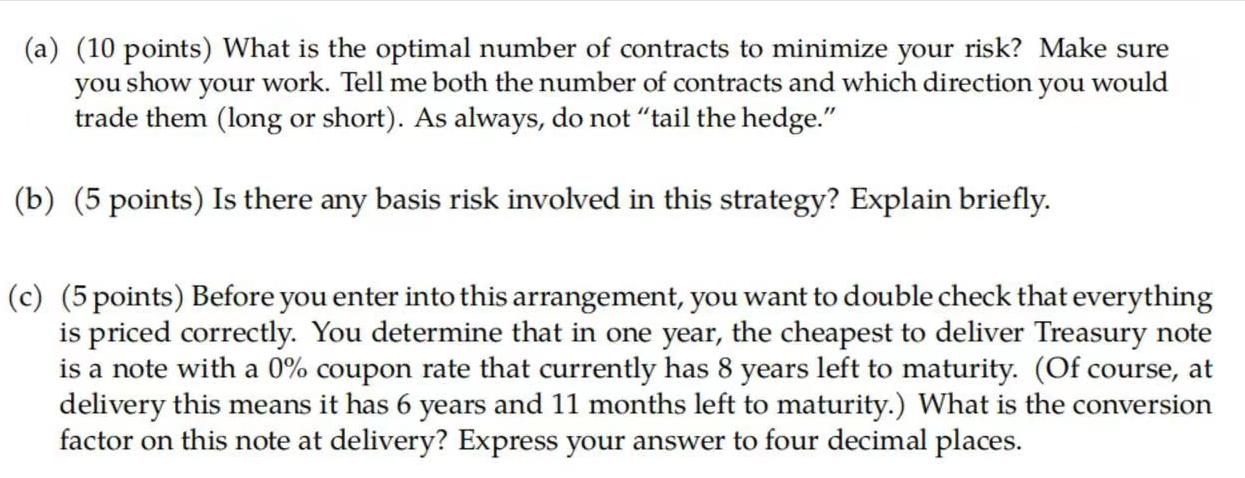

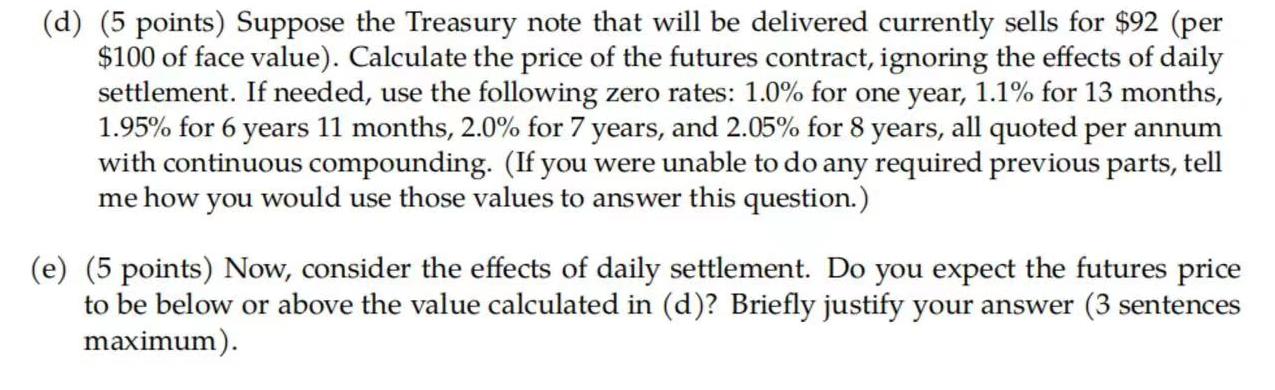

Your firm will produce 10,000 exam-answering machines in one year's time. However, the price of exam-answering...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Your firm will produce 10,000 exam-answering machines in one year's time. However, the price of exam-answering machines is very volatile. As CFO of the firm, you are tasked with hedging against this risk. For this problem, all prices of the exam-answering machines are quoted per machine. Of course, there are no futures contracts trading on exam-answering machines. After careful analysis, you determine that Treasury futures are the best asset to use to hedge the price risk. In particular, you will use 10-year Treasury-note futures with a delivery date in 1 year and 1 month (13 months) to hedge. Each Treasury futures contract is on $100,000 of face value of 10-year notes, and as always, Treasury futures are quoted as a price per $100 in face value. From historical data, you calculate a standard deviation of annual price changes in exam- answering machines of $1120 (per machine). You calculate a standard deviation of annual fu- tures price changes of the Treasury futures contract you will be using of $5 (per $100 of face value). The correlation between these two price changes in 0.85. Note: many parts of this problem are independent of each other. (a) (10 points) What is the optimal number of contracts to minimize your risk? Make sure you show your work. Tell me both the number of contracts and which direction you would trade them (long or short). As always, do not "tail the hedge." (b) (5 points) Is there any basis risk involved in this strategy? Explain briefly. (c) (5 points) Before you enter into this arrangement, you want to double check that everything is priced correctly. You determine that in one year, the cheapest to deliver Treasury note is a note with a 0% coupon rate that currently has 8 years left to maturity. (Of course, at delivery this means it has 6 years and 11 months left to maturity.) What is the conversion factor on this note at delivery? Express your answer to four decimal places. (d) (5 points) Suppose the Treasury note that will be delivered currently sells for $92 (per $100 of face value). Calculate the price of the futures contract, ignoring the effects of daily settlement. If needed, use the following zero rates: 1.0% for one year, 1.1% for 13 months, 1.95% for 6 years 11 months, 2.0% for 7 years, and 2.05% for 8 years, all quoted per annum with continuous compounding. (If you were unable to do any required previous parts, tell me how you would use those values to answer this question.) (e) (5 points) Now, consider the effects of daily settlement. Do you expect the futures price to be below or above the value calculated in (d)? Briefly justify your answer (3 sentences maximum). Your firm will produce 10,000 exam-answering machines in one year's time. However, the price of exam-answering machines is very volatile. As CFO of the firm, you are tasked with hedging against this risk. For this problem, all prices of the exam-answering machines are quoted per machine. Of course, there are no futures contracts trading on exam-answering machines. After careful analysis, you determine that Treasury futures are the best asset to use to hedge the price risk. In particular, you will use 10-year Treasury-note futures with a delivery date in 1 year and 1 month (13 months) to hedge. Each Treasury futures contract is on $100,000 of face value of 10-year notes, and as always, Treasury futures are quoted as a price per $100 in face value. From historical data, you calculate a standard deviation of annual price changes in exam- answering machines of $1120 (per machine). You calculate a standard deviation of annual fu- tures price changes of the Treasury futures contract you will be using of $5 (per $100 of face value). The correlation between these two price changes in 0.85. Note: many parts of this problem are independent of each other. (a) (10 points) What is the optimal number of contracts to minimize your risk? Make sure you show your work. Tell me both the number of contracts and which direction you would trade them (long or short). As always, do not "tail the hedge." (b) (5 points) Is there any basis risk involved in this strategy? Explain briefly. (c) (5 points) Before you enter into this arrangement, you want to double check that everything is priced correctly. You determine that in one year, the cheapest to deliver Treasury note is a note with a 0% coupon rate that currently has 8 years left to maturity. (Of course, at delivery this means it has 6 years and 11 months left to maturity.) What is the conversion factor on this note at delivery? Express your answer to four decimal places. (d) (5 points) Suppose the Treasury note that will be delivered currently sells for $92 (per $100 of face value). Calculate the price of the futures contract, ignoring the effects of daily settlement. If needed, use the following zero rates: 1.0% for one year, 1.1% for 13 months, 1.95% for 6 years 11 months, 2.0% for 7 years, and 2.05% for 8 years, all quoted per annum with continuous compounding. (If you were unable to do any required previous parts, tell me how you would use those values to answer this question.) (e) (5 points) Now, consider the effects of daily settlement. Do you expect the futures price to be below or above the value calculated in (d)? Briefly justify your answer (3 sentences maximum). Your firm will produce 10,000 exam-answering machines in one year's time. However, the price of exam-answering machines is very volatile. As CFO of the firm, you are tasked with hedging against this risk. For this problem, all prices of the exam-answering machines are quoted per machine. Of course, there are no futures contracts trading on exam-answering machines. After careful analysis, you determine that Treasury futures are the best asset to use to hedge the price risk. In particular, you will use 10-year Treasury-note futures with a delivery date in 1 year and 1 month (13 months) to hedge. Each Treasury futures contract is on $100,000 of face value of 10-year notes, and as always, Treasury futures are quoted as a price per $100 in face value. From historical data, you calculate a standard deviation of annual price changes in exam- answering machines of $1120 (per machine). You calculate a standard deviation of annual fu- tures price changes of the Treasury futures contract you will be using of $5 (per $100 of face value). The correlation between these two price changes in 0.85. Note: many parts of this problem are independent of each other. (a) (10 points) What is the optimal number of contracts to minimize your risk? Make sure you show your work. Tell me both the number of contracts and which direction you would trade them (long or short). As always, do not "tail the hedge." (b) (5 points) Is there any basis risk involved in this strategy? Explain briefly. (c) (5 points) Before you enter into this arrangement, you want to double check that everything is priced correctly. You determine that in one year, the cheapest to deliver Treasury note is a note with a 0% coupon rate that currently has 8 years left to maturity. (Of course, at delivery this means it has 6 years and 11 months left to maturity.) What is the conversion factor on this note at delivery? Express your answer to four decimal places. (d) (5 points) Suppose the Treasury note that will be delivered currently sells for $92 (per $100 of face value). Calculate the price of the futures contract, ignoring the effects of daily settlement. If needed, use the following zero rates: 1.0% for one year, 1.1% for 13 months, 1.95% for 6 years 11 months, 2.0% for 7 years, and 2.05% for 8 years, all quoted per annum with continuous compounding. (If you were unable to do any required previous parts, tell me how you would use those values to answer this question.) (e) (5 points) Now, consider the effects of daily settlement. Do you expect the futures price to be below or above the value calculated in (d)? Briefly justify your answer (3 sentences maximum). Your firm will produce 10,000 exam-answering machines in one year's time. However, the price of exam-answering machines is very volatile. As CFO of the firm, you are tasked with hedging against this risk. For this problem, all prices of the exam-answering machines are quoted per machine. Of course, there are no futures contracts trading on exam-answering machines. After careful analysis, you determine that Treasury futures are the best asset to use to hedge the price risk. In particular, you will use 10-year Treasury-note futures with a delivery date in 1 year and 1 month (13 months) to hedge. Each Treasury futures contract is on $100,000 of face value of 10-year notes, and as always, Treasury futures are quoted as a price per $100 in face value. From historical data, you calculate a standard deviation of annual price changes in exam- answering machines of $1120 (per machine). You calculate a standard deviation of annual fu- tures price changes of the Treasury futures contract you will be using of $5 (per $100 of face value). The correlation between these two price changes in 0.85. Note: many parts of this problem are independent of each other. (a) (10 points) What is the optimal number of contracts to minimize your risk? Make sure you show your work. Tell me both the number of contracts and which direction you would trade them (long or short). As always, do not "tail the hedge." (b) (5 points) Is there any basis risk involved in this strategy? Explain briefly. (c) (5 points) Before you enter into this arrangement, you want to double check that everything is priced correctly. You determine that in one year, the cheapest to deliver Treasury note is a note with a 0% coupon rate that currently has 8 years left to maturity. (Of course, at delivery this means it has 6 years and 11 months left to maturity.) What is the conversion factor on this note at delivery? Express your answer to four decimal places. (d) (5 points) Suppose the Treasury note that will be delivered currently sells for $92 (per $100 of face value). Calculate the price of the futures contract, ignoring the effects of daily settlement. If needed, use the following zero rates: 1.0% for one year, 1.1% for 13 months, 1.95% for 6 years 11 months, 2.0% for 7 years, and 2.05% for 8 years, all quoted per annum with continuous compounding. (If you were unable to do any required previous parts, tell me how you would use those values to answer this question.) (e) (5 points) Now, consider the effects of daily settlement. Do you expect the futures price to be below or above the value calculated in (d)? Briefly justify your answer (3 sentences maximum).

Expert Answer:

Answer rating: 100% (QA)

a To minimize risk we can use the following formula to calculate the optimal number of contracts N P 1 2 f F where N is the optimal number of contract... View the full answer

Related Book For

Accounting for Decision Making and Control

ISBN: 978-1259564550

9th edition

Authors: Jerold Zimmerman

Posted Date:

Students also viewed these finance questions

-

A company's net income for the current year was $480,000. Depreciation was $62,000. Accounts receivable and inventories decreased by $20,000 and $32,000, respectively. Prepaid expenses and salaries...

-

What refers to countries trying to gain independence from their reliance on another country for goods or services; an example of this is the U.S. and the microchip fabrication business with what?

-

Read the case study "Southwest Airlines," found in Part 2 of your textbook. Review the "Guide to Case Analysis" found on pp. CA1 - CA11 of your textbook. (This guide follows the last case in the...

-

In a recombinant protein expression process the host microorganism, Pichia pastoris needs to be separated from the culture supernatant after production. A pilot scale bioreactor with a working volume...

-

(a) Show that 1 Pa = 1 J/m3. (b) Show that the density in space of the translational kinetic energy of an ideal gas is 3P/2.

-

What are the annual payments on a loan of $350,000 to be repaid over 10 years at 8%?

-

Many consumers, particularly those in developing countries, are concerned about the cleanliness of municipal water for human consumption. For this reason, distilled water is widely available at work,...

-

A manufactured product has the following information for June. Compute the (1) Standard cost per unit (2) Total cost variance for June. Indicate whether the cost variance is favorable or unfavorable....

-

Selected current year-end financial statements of Cabot Corporation follow. (All sales were on credit; selected balance sheet amounts at December 31 of the prior year were inventory, $55,900; total...

-

Packer and Stringer were in partnership as retail traders sharing profits and losses: Packer 3/4, Stringer 1/4. The partners were credited annually with interest at the rate of 6% per annum on their...

-

Supermart Food Stores (SFS) has experienced net operating losses in its frozen food products line in the last few periods. Management believes that the store can improve its profitability if SFS...

-

According to Smith, where does the division of labor come from? What challenges stand in the way of economic growth, in Smith's view? What do you think Smith would say about economic inequality?

-

On September 25, Bramble provided services to two clients and billed the clients a total of $700. On October 15, both clients paid their invoice in full. Bramble's cost related to this sale was $430...

-

Discuss whether economies of scale have any relevance to such companies as Wal-Mart.

-

Suppose the spot exchange rates quoted by three banks located in three different countries are as follows: Bank A (Australia): 95/A$ Bank B (Germany): A$1.60/ Bank C (Japan.): 150/ Assume a German...

-

Discuss three habits or behaviors you think every "good" student should have. At least one of these habits must relate directly to students taking online classes.

-

Which of the following compounds is the (R) enantiomer of carvone, a ketone-containing compound that smells like spearmint? Hint: the prioritization for substituents is shown for choice (a). Your...

-

Which of the following is FALSE regarding the purchasing power parity (PPP). a. The PPP is a manifestation of the law of one price b. The PPP says that a country with a higher expected inflation can...

-

Polymtech uses advanced laser technology to manufacture polymers for a variety of applications. One of their processes produces four separate polymers (N200, HV87, HMT45, and V989) in one batch...

-

Palabora Mining owns and operates a copper mine. Besides producing copper, the mine also produces magnetite, vermiculite, and titanium dioxide. To extract the ore and to separate the four minerals...

-

Gino Potestio, owner of Napoli Pizzeria, is evaluating leasing an espresso/cappuccino machine. A number of patrons have inquired about espresso and cappuccino beverages. Napoli currently does not...

-

The following information has been extracted from the financial statements and the notes of Champigon Ltd. Required (a) Calculate the following for 2023 to one decimal place: i. current ratio ii....

-

Comparative figures from the statement of financial position for Warder Ltd are shown below. Required (a) Prepare common size statements for the company for both years, and comment on what this...

-

The following information has been extracted from the financial statements and notes thereto of Bass and Dide Ltd, consultants. Required (a) Calculate the following ratios for 2025: i. return on...

Study smarter with the SolutionInn App