Question: Prove Theorem 6.4 for the continuous case. THEOREM 6.4 If X and Y are independent random variables, then E(XY) = E(X)E(Y) Proof of Theorem 6.4

Prove Theorem 6.4 for the continuous case.

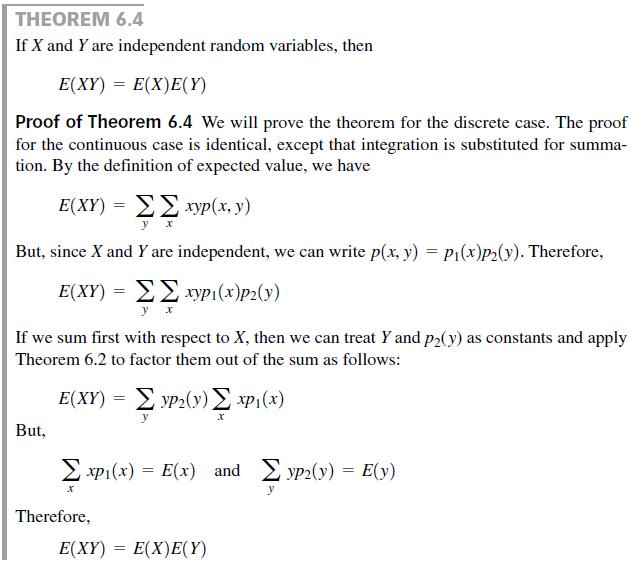

THEOREM 6.4 If X and Y are independent random variables, then E(XY) = E(X)E(Y) Proof of Theorem 6.4 We will prove the theorem for the discrete case. The proof for the continuous case is identical, except that integration is substituted for summa- tion. By the definition of expected value, we have E(XY) = EE xyp(x, y) y x But, since X and Y are independent, we can write p(x, y) = P1(x)p2(y). Therefore, E(XY) = E> xyp1(x)p2(y) y x If we sum first with respect to X, then we can treat Y and pP2(y) as constants and apply Theorem 6.2 to factor them out of the sum as follows: E(XY) = E yP2(y)E xP1(x) But, 2 xp1(x) = E(x) and yp2(y) = E(y) y Therefore, E(XY) = E(X)E(Y) %3D

Step by Step Solution

3.49 Rating (159 Votes )

There are 3 Steps involved in it

answer To prove Theorem 64 for the continuous case we need to show that if X and Y are in... View full answer

Get step-by-step solutions from verified subject matter experts