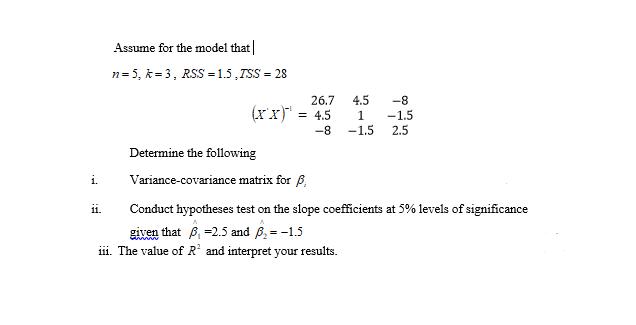

Question: i. Assume for the model that n = 5, k= 3, RSS = 1.5,ISS = 28 11. 26.7 = 4.5 4.5 1 -8 -1.5

i. Assume for the model that n = 5, k= 3, RSS = 1.5,ISS = 28 11. 26.7 = 4.5 4.5 1 -8 -1.5 -8 -1.5 2.5 Determine the following Variance-covariance matrix for p Conduct hypotheses test on the slope coefficients at 5% levels of significance given that 6, -2.5 and 6 = -1.5 iii. The value of R and interpret your results.

Step by Step Solution

3.44 Rating (157 Votes )

There are 3 Steps involved in it

SOLUTION i Variancecovariance matrix for B The variancecovariance matrix for the slope coefficients B is given by VarB RSSnk1XX1 where RSS is the residual sum of squares n is the sample size k is the ... View full answer

Get step-by-step solutions from verified subject matter experts