Question: Suppose every time units a process either increases by the amount with probability p or decreases by the amount with probability

Suppose every time units a process either increases by the amount σ

√

with probability p or decreases by the amount σ

√

with probability 1 − p where

Show that as goes to 0, this process converges to a Brownian motion process with drift parameter μ and variance parameter σ2.

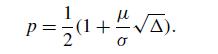

p= 1 + A).

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock