Question: Support-department cost allocation: direct and step-down methods. Phoenix Partners provides management consulting services to government and corporate clients. Phoenix has two support departmentsAdministrative Services (AS)

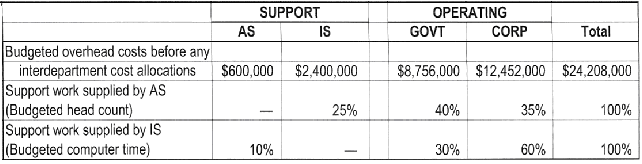

Support-department cost allocation: direct and step-down methods. Phoenix Partners provides management consulting services to government and corporate clients. Phoenix has two support departments—Administrative Services (AS) and Information Systems (IS)—and two operating departments— Government Consulting (GOVT) and Corporate Consulting (CORP). For the first quarter of 2009, Phoenix’s cost records indicate the following:

1. Allocate the two support departments’ costs to the two operating departments using the following methods:

a. Direct method

b. Step-down method (allocate AS first)

c. Step-down method (allocate IS first)

2. Compare and explain differences in the support-department costs allocated to each operating department.

3. What approaches might be used to decide the sequence in which to allocate support departments when using the step-down method?

SUPPORT OPERATING Total AS IS GOVT CORP Budgeted overhead costs before any interdepartment cost allocations Support work supplied by AS (Budgeted head count) Support work supplied by IS (Budgeted computer time) $600,000 $8,756,000 $12,452,000 $24,208,000 $2,400,000 35% 25% 100% 40% 10% 30% 60% 100%

Step by Step Solution

3.34 Rating (166 Votes )

There are 3 Steps involved in it

Support department cost allocation direct and stepdown methods 1 2 GOVT CORP Direct method 1120000 1880000 Stepdown AS first 1090000 1910000 Stepdown ... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

24-B-C-A-C-A (73).docx

120 KBs Word File