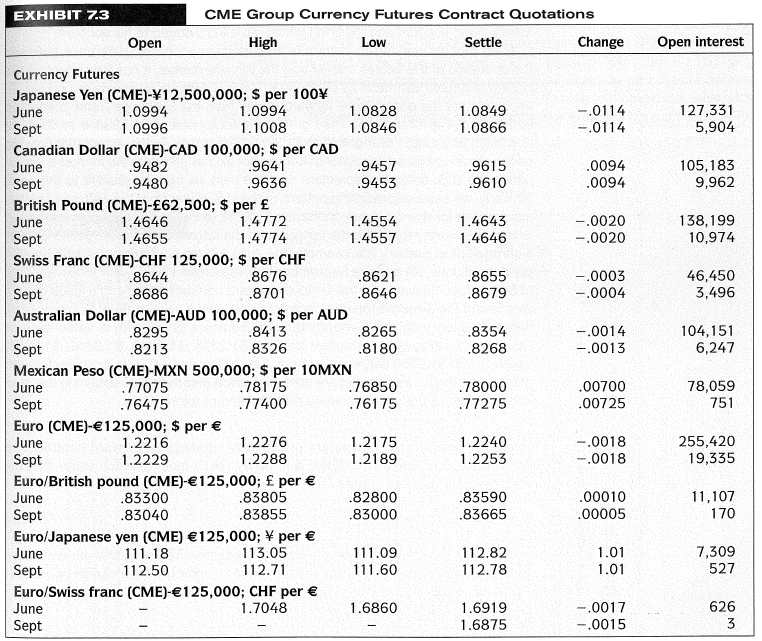

Question: Using the quotations in Exhibit 7.3, calculate the face value of the open interest in the September 2010 Swiss franc futures contract. Exhibit 7.3 CME

Using the quotations in Exhibit 7.3, calculate the face value of the open interest in the September 2010 Swiss franc futures contract.

Exhibit 7.3

CME Group Currency Futures Contract Quotations EXHIBIT 7.3 Change Open interest High Low Settle Open Currency Futures Japanese Yen (CME)-12,500,000; S per 100 June 1.0994 1.1008 127,331 5,904 1.0828 1.0849 -.0114 1.0994 1.0846 1.0866 -.0114 1.0996 Sept Canadian Dollar (CME)-CAD 100,000; $ per CAD .9482 .9457 .9615 .0094 105,183 9,962 .9641 June .9480 .9453 .9610 .0094 Sept British Pound (CME)-62,500; $ per June .9636 138,199 10,974 -.0020 1.4646 1.4772 1.4554 1.4643 1.4646 -.0020 Sept Swiss Franc (CME)-CHF 125,000; $ per CHF June Sept Australian Dollar (CME)-AUD 100,000; $ per AUD June 1.4655 1.4774 1.4557 -.0003 46,450 3,496 .8676 .8621 .8655 .8644 .8686 -.0004 .8701 .8646 .8679 104,151 6,247 .8413 .8265 .8354 -.0014 .8295 .8326 .8180 .8268 -.0013 Sept .8213 Mexican Peso (CME)-MXN 500,000; $ per 10MXN June .78000 .77275 78,059 751 .78175 .76850 .00700 .77075 .77400 .76175 .00725 Sept .76475 Euro (CME)-125,000; $ per June 1.2175 1.2240 -.0018 255,420 19,335 1.2216 1.2276 Sept Euro/British pound (CME)-125,000; per June 1.2229 1.2288 1.2189 1.2253 -.0018 .00010 11,107 170 .83300 .83805 .82800 .83590 .00005 Sept .83855 .83000 .83665 .83040 Euro/Japanese yen (CME) 125,000; per 113.05 112.71 1.01 1.01 112.82 112.78 7,309 527 June 111.09 111.18 Sept 112.50 111.60 Euro/Swiss franc (CME)-125,000; CHF per June 626 -.0017 -.0015 1.7048 1.6860 1.6919 3 1.6875 Sept

Step by Step Solution

3.50 Rating (163 Votes )

There are 3 Steps involved in it

3496 contracts x SF125000 SF437000000 ... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

97-B-F-I-F-M (112).docx

120 KBs Word File