Question: You are using attribute estimation sampling to test the controls over revenue recognition of the Packet Corporation, a public company, and will use the results

You are using attribute estimation sampling to test the controls over revenue recognition of the Packet Corporation, a public company, and will use the results as part of the evidence on which to base your opinion on its internal controls and to determine what additional audit procedures should be performed on revenue and accounts receivable. You have decided to test the following controls and have set sampling risk at 5%, the tolerable failure rate at 5%, and the expected failure rate of 1%. A sample size of 100 is used. The results of your testing are as indicated.

Required

a. Determine the upper limit of control failures for each of the controls.

b. What impact do these results have for the type of opinion to be given on the client’s internal controls?

c. Indicate the potential misstatements that could be the result of the control failures?

d. Determine what substantive audit procedures should be performed in response to each of the control failures identified above.

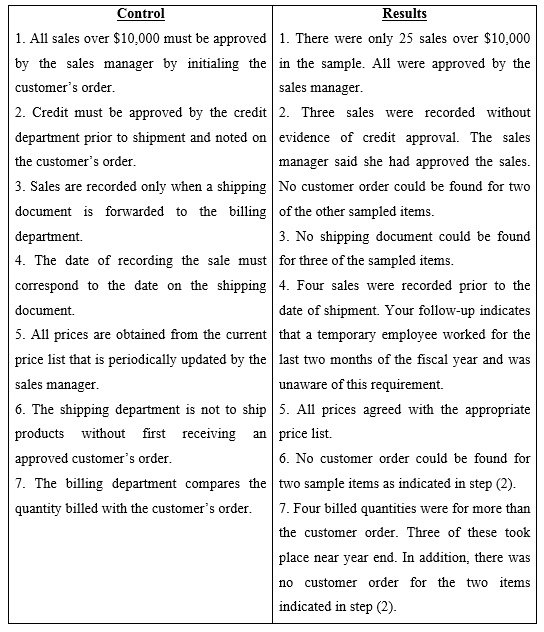

Results Control 1. All sales over $10,000 must be approved 1. There were only 25 sales over $10,000 by the sales manager by initialing the in the sample. All were approved by the customer's order. sales manager. 2. Credit must be approved by the credit 2. Three sales were recorded without department prior to shipment and noted on evidence of credit approval. The sales the customer's order. manager said she had approved the sales. 3. Sales are recorded only when a shipping No customer order could be found for two document is forwarded to the billing of the other sampled items. department. 3. No shipping document could be found 4. The date of recording the sale must for three of the sampled items. correspond to the date on the shipping 4. Four sales were recorded prior to the document. date of shipment. Your follow-up indicates 5. All prices are obtained from the current that a temporary employee worked for the price list that is periodically updated by the last two months of the fiscal year and was unaware of this requirement. sales manager. 6. The shipping department is not to ship 5. All prices agreed with the appropriate without first receiving an price list. products 6. No customer order could be found for approved customer's order. 7. The billing department compares the two sample items as indicated in step (2). 7. Four billed quantities were for more than quantity billed with the customer's order. the customer order. Three of these took place near year end. In addition, there was customer order for the two items no indicated in step (2).

Step by Step Solution

3.34 Rating (178 Votes )

There are 3 Steps involved in it

a Control Upper Limit of Control Failures 1 Only 25 of the 100 sales tested were over 10000 and all were properly approved The auditor should use hish... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

222-B-A-A-B-R (455).docx

120 KBs Word File