New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

accounting

Intermediate Accounting 13th Edition Donald E. Kieso, Jerry J. Weygandt, And Terry D. Warfield - Solutions

Entries for Disposition of Assets On December 31, 2010, Chrysler Inc. has a machine with a book value of $940,000. The original cost and related accumulated depreciation at this date are as follows.Machine

Disposition of Assets On April 1, 2010, Pavlova Company received a condemnation award of $410,000 cash as compensation for the forced sale of the company’s land and building, which stood in the path of a new state highway. The land and building cost $60,000 and $280,000, respectively, when they

Classification of Acquisition and Other Asset Costs At December 31, 2009, certain accounts included in the property, plant, and equipment section of Reagan Company’s balance sheet had the following balances.Land

Classification of Acquisition Costs Selected accounts included in the property, plant, and equipment section of Lobo Corporation’s balance sheet at December 31, 2009, had the following balances.Land

Classification of Land and Building Costs Spitfire Company was incorporated on January 2, 2011, but was unable to begin manufacturing activities until July 1, 2011, because new factory facilities were not completed until that date. The Land and Building account reported the following items during

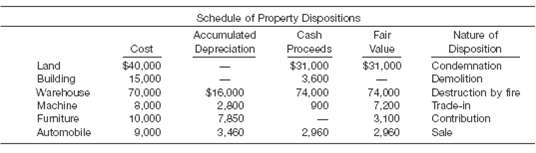

Dispositions, Including Condemnation, Demolition, and Trade-in Presented below are a schedule of property dispositions for Hollerith Co. The following additional information is available. Land On February 15, a condemnation award was received as consideration for unimproved land held primarily as

Classification of Costs and Interest Capitalization On January 1, 2010, Blair Corporation purchased for $500,000 a tract of land (site number 101) with a building. Blair paid a real estate broker’s commission of $36,000, legal fees of $6,000, and title guarantee insurance of $18,000. The closing

Interest during Construction Grieg Landscaping began construction of a new plant on December 1, 2010. On this date the company purchased a parcel of land for $139,000 in cash. In addition, it paid $2,000 in surveying costs and $4,000 for a title insurance policy. An old dwelling on the premises was

Capitalization of Interest Laserwords Inc. is a book distributor that had been operating in its original facility since 1985. The increase in certification programs and continuing education requirements in several professions has contributed to an annual growth rate of 15% for Laserwords since

Nonmonetary Exchanges Holyfield Corporation wishes to exchange a machine used in its operations. Holyfield has received the following offers from other companies in the industry.1. Dorsett Company offered to exchange a similar machine plus $23,000. (The exchange has commercial substance for both

Nonmonetary Exchanges on August 1, Hyde, Inc. exchanged productive assets with Wiggins, Inc. Hyde’s asset are referred to below as “Asset A,” and Wiggins’ is referred to as “Asset B.” The following facts pertain to these assets.

Nonmonetary Exchanges During the current year, Marshall Construction trades an old crane that has a book value of $90,000 (original cost $140,000 less accumulated depreciation $50,000) for a new crane from Brigham Manufacturing Co. The new crane cost Brigham $165,000 to manufacture and is

Purchases by Deferred Payment, Lump-Sum, and Nonmonetary Exchanges Klamath Company, a manufacturer of ballet shoes, is experiencing a period of sustained growth. In an effort to expand its production capacity to meet the increased demand for its product, the company recently made several

Acquisition, Improvements, and Sale of Realty Tonkawa Company purchased land for use as its corporate headquarters. A small factory that was on the land when it was purchased was torn down before construction of the office building began. Furthermore, a substantial amount of rock blasting and

Accounting for Self-Constructed Assets Troopers Medical Labs, Inc., began operations 5 years ago producing stetrics, a new type of instrument it hoped to sell to doctors, dentists, and hospitals. The demand for stetrics far exceeded initial expectations, and the company was unable to produce enough

Capitalization of Interest Langer Airline is converting from piston-type planes to jets. Delivery time for the jets is 3 years, during which substantial progress payments must be made. The multimillion-dollar cost of the planes cannot be financed from working capital; Langer must borrow funds for

Capitalization of Interest Vania Magazine Company started construction of a warehouse building for its own use at an estimated cost of $5,000,000 on January 1, 2009, and completed the building on December 31, 2009. During the construction period, Vania has the following debt obligations

Nonmonetary Exchanges You has two clients that are considering trading machinery with each other. Although the machines are different from each other, you believe that an assessment of expected cash flows on the exchanged assets will indicate the exchange lacks commercial substance. Your clients

Costs of Acquisition the invoice price of a machine is $50,000. Various other costs relating to the acquisition and installation of the machine including transportation, electrical wiring, and special base, and soon amount to $7,500 The machine has an estimated life of 10 years, with no residual

Cost of Land vs. Building—Ethics Tones Company purchased a warehouse in a downtown district where land values are rapidly increasing. Gerald Carter, controller, and Wilma Ankara, financial vice president, are trying to allocate the cost of the purchase between the land and the building. Noting

In recent years, the Wall Street Journal has indicated that many companies have changed their accounting principles. What are the major reasons why companies change accounting methods?

State how each of the following items is reflected in the financial statements.(a) Change from FIFO to LIFO method for inventory valuation purposes.(b) Charge for failure to record depreciation in a previous period.(c) Litigation won in current year, related to prior period.(d) Change in the

Discuss briefly the three approaches that have been suggested for reporting changes in accounting principles.

Identify and describe the approach the FASB requires for reporting changes in accounting principles.

What is the indirect effect of a change in accounting principle? Briefly describe the reporting of the indirect effects of a change in accounting principle.

Define a change in estimate and provide an illustration. When is a change in accounting estimate effected by a change in accounting principle?

Lenexa State Bank has followed the practice of capitalizing certain marketing costs and amortizing these costs over their expected life. In the current year, the bank determined that the future benefits from these costs were doubtful. Consequently, the bank adopted the policy of expensing these

Indicate how the following items are recorded in the accounting records in the current year of Coronet Co.(a) Impairment of goodwill.(b) A change in depreciating plant assets from accelerated to the straight-line method.(c) Large write-off of inventories because of obsolescence.(d) Change from the

Whittier Construction Co. had followed the practice of expensing all materials assigned to a construction job without recognizing any salvage inventory. On December 31, 2010, it was determined that salvage inventory should be valued at $52,000. Of this amount, $29,000 arose during the current year.

Parsons Inc. wishes to change from the completed-contract to the percentage-of-completion method for financial reporting purposes. The auditor indicates that a change would be permitted only if it is to a preferable method. What difficulties develop in assessing prefer ability?

Discuss how a change to the LIFO method of inventory valuation is handled when it is impracticable to determine previous LIFO inventory amounts.

How should consolidated financial statements be reported this year when statements of individual companies were presented last year?

Simms Corp. controlled four domestic subsidiaries and one foreign subsidiary. Prior to the current year, Simms Corp. had excluded the foreign subsidiary from consolidation. During the current year, the foreign subsidiary was included in the financial statements. How should this change in accounting

Distinguish between counterbalancing and non-counterbalancing errors. Give an example of each.

Discuss and illustrate how a correction of an error in previously issued financial statements should be handled.

Prior to 2010, Heberling Inc. excluded manufacturing overhead costs from work in process and finished goods inventory. These costs have been expensed as incurred. In 2010, the company decided to change its accounting methods for manufacturing inventories to full costing by including these costs as

Elliott Corp failed to record accrued salaries for 2009, $2,000; 2010, $2,100; and 2011, $3,900 what is the amount of the overstatement or understatement of Retained Earnings at December 31, 2012?

In January 2010, installation costs of $6,000 on new machinery were charged to Repair Expense. Other costs of this machinery of $30,000 were correctly recorded and have been depreciated using the straight-line method with an estimated life of 10 years and no salvage value. At December 31, 2011, it

On January 2, 2010, $100,000 of 11%, 10-year bonds were issued for $97,000. The $3,000 discount was charged to Interest Expense. The bookkeeper, Mark Landis, records interest only on the interest payment dates of January 1 and July 1. What is the effect on reported net income for 2010 of this

An entry to record Purchases and related Accounts Payable of $13,000 for merchandise purchased on December 23, 2011, was recorded in January 2012. This merchandise was not included in inventory at December 31, 2011. What effect does this error have on reported net income for 2011? What entry

Equipment was purchased on January 2, 2010, for $24,000, but no portion of the cost has been charged to depreciation. The corporation wishes to use the straight-line method for these assets, which have been estimated to have a life of 10 years and no salvage value. What effect does this error have

Where can authoritative iGAAP related to accounting changes be found?

Briefly describe some of the similarities and differences between U.S. GAAP and iGAAP with respect to reporting accounting changes.

How might differences in presentation of comparative data under U.S. and iGAAP affect adoption of iGAAP by U.S. companies?

Wertz Construction Company decided at the beginning of 2010 to change from the completed contract method to the percentage-of-completion method for financial reporting purposes. The company will continue to use the completed-contract method for tax purposes. For years prior to 2010, pre-tax income

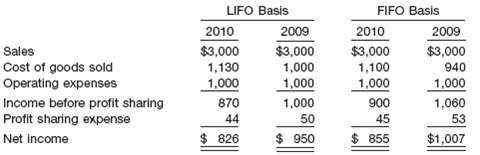

Refer to the accounting change by Wertz Construction Company in BE22-1. Wertz has a profit-sharing plan, which pays all employees a bonus at year-end based on 1% of pre-tax income. Compute the indirect effect of Wertz’s change in accounting principle that will be reported in the 2010 income

Shannon, Inc., changed from the LIFO cost flow assumption to the FIFO cost flow assumption in 2010. The increase in the prior year’s income before taxes is $1,200,000. The tax rate is 40%. Prepare Shannon’s 2010 journal entry to record the change in accounting principle.

Tedesco Company changed depreciation methods in 2010 from double-declining-balance to straight-line. depreciation prior to 2010 under double-declining-balance was $90,000, whereas straight line depreciation prior to 2010 would have been $50,000. Tedesco’s depreciable assets had a cost of $250,000

Sesame Company purchased a computer system for $74,000 on January 1, 2009. It was depreciated based on a 7-year life and an $18,000 salvage value. On January 1, 2011, Sesame revised these estimates to a total useful life of 4 years and a salvage value of $10,000. Prepare Sesame’s entry to record

In 2010, Bailey Corporation discovered that equipment purchased on January 1, 2008, for $50,000 was expensed at that time. The equipment should have been depreciated over 5 years, with no salvage value. The effective tax rate is 30%. Prepare Bailey’s 2010 journal entry to correct the error.

At January 1, 2010, Beidler Company reported retained earnings of $2,000,000. In 2010, Beidler discovered that 2009 depreciation expense was understated by $400,000. In 2010, net income was $900,000 and dividends declared were $250,000. The tax rate is 40%. Prepare a 2010 retained earnings

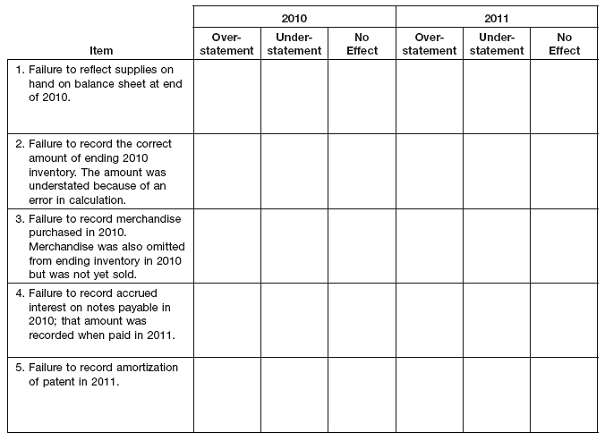

Indicate the effect—Understate, Overstate, No Effect—that each of the following errors has on 2010 net income and 2011 net income.

Round tree Manufacturing Co. is preparing its year-end financial statements and is considering the accounting for the following items.1. The vice president of sales had indicated that one product line has lost its customer appeal and will be phased out over the next 3 years. Therefore, a decision

Palmer Co. is evaluating the appropriate accounting for the following items.1. Management has decided to switch from the FIFO inventory valuation method to the LIFO inventory valuation method for all inventories.2. When the year-end physical inventory adjustment was made for the current year, the

Simmons Corporation owns stock of Armstrong, Inc prior to 2010 the investment was accounted for using the equity method. In early 2010, Simmons sold part of its investment in Armstrong, and began using the fair value method. In 2010, Armstrong earned net income of $80,000 and paid dividends of

Oliver Corporation has owned stock of Conrad Corporation since 2007. At December 31, 2010, its balances related to this investment were: Available-for-Sale Securities $185,000 Securities Fair Value Adj (AFS) 34,000 Dr. Unrealized Holding Gain or Loss—Equity 34,000 Cr. On January 1, 2011, Oliver

Change in Principle—Long-Term Contracts Cherokee Construction Company changed from the completed-contract to the percentage-of-completion method of accounting for long-term construction contracts during 2010. For tax purposes, the company employs the completed-contract method and will continue

Change in Principle—Inventory Methods Whitman Company began operations on January 1, 2008, and uses the average cost method of pricing inventory. Management is contemplating a change in inventory methods for 2011. The following information is available for the years 2008–2010. (Ignore all tax

Accounting Change Ramirez Co. decides at the beginning of 2010 to adopt the FIFO method of inventory valuation. Ramirez had used the LIFO method for financial reporting since its inception on January 1, 2008, and had maintained records adequate to apply the FIFO method retrospectively. Ramirez

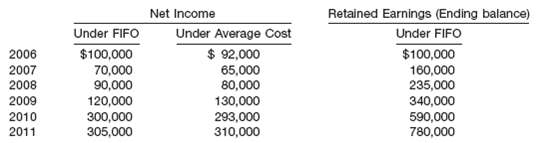

Accounting Change Linden Company started operations on January 1, 2006, and has used the FIFO method of inventory valuation since its inception. In 2012, it decides to switch to the average cost method. You are provided with the following information. (a) What is the beginning retained earnings

Accounting Change Presented are income statements prepared on a LIFO and FIFO basis for Carlton Company, which started operations on January 1, 2009. The company presently uses the LIFO method of pricing its inventory and has decided to switch to the FIFO method in 2010. The FIFO income statement

Accounting Changes—Depreciation Robillard Inc. acquired the following assets in January of 2007.Equipment estimated service life, 5 years; salvage value, $15,000 $465,000Building, estimated service life, 30 years; no salvage value

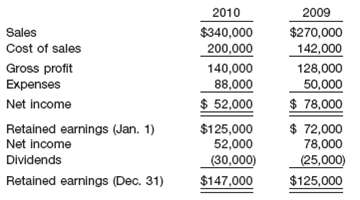

Change in Estimate and Error; Financial Statements Presented below are the comparative income statements for Pannebecker Inc. for the years 2009 and 2010. The following additional information is provided: 1. In 2010, Pannebecker Inc. decided to switch its depreciation method from

Accounting for Accounting Changes and Errors Listed below are various types of accounting changes and errors.______ 1. Change from FIFO to average cost inventory method.______ 2. Change due to overstatement of inventory.______ 3. Change from sum-of-the-years’-digits to straight-line method of

Error and Change in Estimate—Depreciation Tarkington Co. purchased a machine on January 1, 2007, for $440,000. At that time it was estimated that the machine would have a 10-year life and no salvage value. On December 31, 2010, the firm’s accountant found that the entry for Depreciation expense

Depreciation Changes On January 1, 2006, McElroy Company purchased a building and equipment that have the following useful lives, salvage values, and costs.Building, 40-year estimated useful life, $50,000 salvage value, $1,200,000 costEquipment, 12-year estimated useful life, $10,000 salvage value,

Change in Estimate—Depreciation Thurber Co. purchased equipment for $710,000 which was estimated to have a useful life of 10 years with a salvage value of $10,000 at the end of that time. Depreciation has been entered for 7 years on a straight-line basis. In 2011, it is determined that the total

Change in Estimate—Depreciation Frederick Industries changed from the double-declining balance to the straight-line method in 2010 on all its plant assets. There was no change in the assets’ salvage values or useful lives. Plant assets, acquired on January 2, 2007, had an original cost of

Change in Principle?Long-Term Contracts Bryant Construction Company changed from the completed-contract to the percentage-of-completion method of accounting for long-term construction contracts during 2010. For tax purposes, the company employs the completed-contract method and will continue this

Various Changes in Principle—Inventory Methods Below is the net income of Benchley Instrument Co., a private corporation, computed under the three inventory methods using a periodic system.

Error Correction Entries the first audit of the books of Fennimore Company was made for the year ended December 31, 2010. In examining the books, the auditor found that certain items had been overlooked or incorrectly handled in the last 3 years. These items are:1. At the beginning of 2008, the

Error Analysis and Correcting Entry You have been engaged to review the financial statements of Longfellow Corporation. In the course of your examination you conclude that the bookkeeper hired during the current year is not doing a good job. You notice a number of irregularities as follows.1.

Error Analysis and Correcting Entry the reported net incomes for the first 2 years of Sinclair Products, Inc., were as follows: 2010, $147,000; 2011, $185,000. Early in 2012, the following errors were discovered.1. Depreciation of equipment for 2010 was overstated $19,000.2. Depreciation of

Error Analysis Emerson Tool Company’s December 31 year-end financial statements contained the following errors.

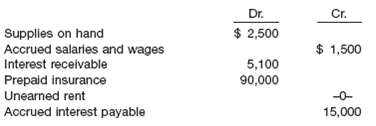

Error Analysis and Correcting Entries A partial trial balance of Dickinson Corporation is as follows on December 31, 2010. Additional adjusting data: 1. A physical count of supplies on hand on December 31, 2010, totaled $1,100. 2. Through oversight, the Accrued Salaries and Wages account was not

Error Analysis The before-tax income for Fitzgerald Co. for 2010 was $101,000 and $77,400 for 2011. However, the accountant noted that the following errors had been made:1. Sales for 2010 included amounts of $38,200 which had been received in cash during 2010, but for which the related products

Error Analysis when the records of Archibald Corporation were reviewed at the close of 2011, the errors listed below was discovered. For each item indicate by a check mark in the appropriate column whether the error resulted in an overstatement, an understatement, or had no effect on net income for

Change from Fair Value to Equity On January 1, 2010, Sandburg Co. purchased 25,000 shares (a 10% interest) in Yevette Corp. for $1,400,000. At the time, the book value and the fair value of Yevette’s net identifiable assets were $13,000,000. On July 1, 2011, Sandburg paid $3,040,000 for 50,000

Change from Equity to Fair Value Gamble Corp. was a 30% owner of Sabrina Company, holding 210,000 shares of Sabrina?s common stock on December 31, 2010. The investment account had the following entries. On January 2, 2011, Gamble sold 126,000 shares of Sabrina for $3,440,000, thereby losing its

Change in Estimate and Error Correction Holtzman Company is in the process of preparing its financial statements for 2010. Assume that no entries for depreciation have been recorded in 2010. The following information related to depreciation of fixed assets is provided to you:1. Holtzman purchased

Comprehensive Accounting Change and Error Analysis Problem Botticelli Inc. were organized in late 2008 to manufacture and sell hosiery. At the end of its fourth year of operation, the company has been fairly successful, as indicated by the following reported net incomes. 2008

Error Corrections and Accounting Changes Penn Company is in the process of adjusting and correcting its books at the end of 2010. In reviewing its records, the following information is compiled. 1. Penn has failed to accrue sales commissions payable at the end of each of the last 2 years, as

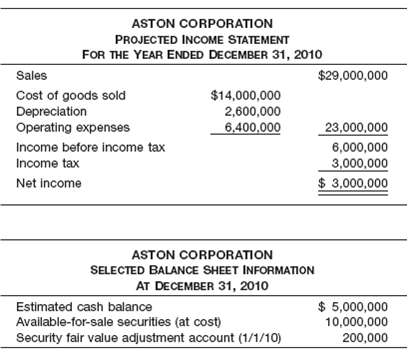

Accounting Changes Aston Corporation performs year-end planning in November of each year before their calendar year ends in December. The preliminary estimated net income is $3 million. The CFO, Rita Warren, meets with the company president, J. B. Aston, to review the projected numbers. She

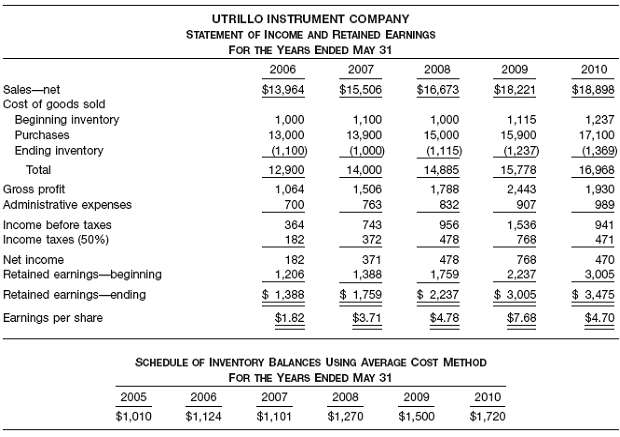

Change in Principle?Inventory?Periodic the management of Utrillo Instrument Company had concluded, with the concurrence of its independent auditors, that results of operations would be more fairly presented if Utrillo changed its method of pricing inventory from last-in, first-out (LIFO) to average

Accounting Change and Error Analysis on December 31, 2010, before the books were closed, the management and accountants of Madras a Inc. made the following determinations about three depreciable assets.1. Depreciable asset A was purchased January 2, 2007. It originally cost $540,000 and, for

Error Corrections you have been assigned to examine the financial statements of Zarle Company for the year ended December 31, 2010. You discover the following situations.1. Depreciation of $3,200 for 2010 on delivery vehicles was not recorded.2. The physical inventory count on December 31, 2009,

Comprehensive Error Analysis on March 5, 2011, you were hired by Hemingway Inc., a closely held company, as a staff member of its newly created internal auditing department. While reviewing the company?s records for 2009 and 2010, you discover that no adjustments have yet been made for the items

Error Analysis Lowell Corporation has used the accrual basis of accounting for several years. A review of the records, however, indicates that some expenses and revenues have been handled on a cash basis because of errors made by an inexperienced bookkeeper. Income statements prepared by the

Fair Value to Equity Method with Goodwill On January 1, 2010, Millay Inc. paid$700,000 for 10,000 shares of Genso Company’s voting common stock, which was a 10% interest in Genso. At that date the net assets of Genso totaled $6,000,000. The fair values of all of Genso’s identifiable assets and

Change from Fair Value to Equity Method On January 3, 2009, Martin Company purchased for $500,000 cash a 10% interest in Renner Corp. On that date the net assets of Renner had a book value of $3,700,000. The excess of cost over the underlying equity in net assets is attributable to undervalued

(Analysis of Various Accounting Changes and Errors) Joblonsky Inc. has recently hired a new independent auditor, Karen Ogleby, who says she wants “to get everything straightened out.” Consequently, she has proposed the accounting changes in connection with Joblonsky Inc.’s 2010 financial

Analysis of Various Accounting Changes and Errors Various types of accounting changes can affect the financial statements of a business enterprise differently. Assume that the following list describes changes that have a material effect on the financial statements for the current year of your

Analysis of Three Accounting Changes and Errors listed below are three independent, unrelated sets of facts relating to accounting changes.Situation 1Sanford Company is in the process of having its first audit. The company has used the cash basis of accounting for revenue recognition. Sanford

Analysis of Various Accounting Changes and Errors Katherine Irving, controller of Lotan Corp., is aware that a pronouncement on accounting changes has been issued. After reading the pronouncement, she is confused about what action should be taken on the following items related to Lotan Corp. for

Change in Principle, Estimate As a certified public accountant you have been contacted by Joe Davison, CEO of Sports-Pro Athletics, Inc., a manufacturer of a variety of athletic equipment. He has asked you how to account for the following changes.1. Sports-Pro appropriately changed its depreciation

Change in Estimate Mike Crane is an audit senior of a large public accounting firm who has just been assigned to the Frost Corporation’s annual audit engagement. Frost has been a client of Crane’s firm for many years. Frost is a fast-growing business in the commercial construction industry. In

Explain the current environment regarding revenue recognition.

When is revenue conventionally recognized? What conditions should exist for the recognition at date of sale of all or part of the revenue of any sale transaction?

When is revenue recognized in the following situations?(a) Revenue from selling products?(b) Revenue from services rendered?(c) Revenue from permitting others to use enterprise assets?(d) Revenue from disposing of assets other than products?

Identify several types of sales transactions and indicate the types of business for which that type of transaction is common.

Showing 1600 - 1700

of 107766

First

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

Last

Step by Step Answers