New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

accounting

Intermediate Accounting 13th Edition Donald E. Kieso, Jerry J. Weygandt, And Terry D. Warfield - Solutions

(Issuance of Bonds with Warrants) Prior Inc. has decided to raise additional capital by issuing $175,000 face value of bonds with a coupon rate of 10%. In discussions with investment bankers, it was determined that to help the sale of the bonds, detachable stock warrants should be issued at the

(Issuance of Bonds with Detachable Warrants) On September 1, 2010, Jacob Company sold at 104 (plus accrued interest) 3,000 of its 8%, 10-year, $1,000 face value, nonconvertible bonds with detachable stock warrants. Each bond carried two detachable warrants. Each warrant was for one share of common

(Issuance of Bonds with Stock Warrants) On May 1, 2010, Barkley Company issued 3,000 $1,000 bonds at 102. Each bond was issued with one detachable stock warrant. Shortly after issuance, the bonds were selling at 98, but the market value of the warrants cannot be determined.(a) Prepare the entry to

(Issuance and Exercise of Stock Options) On November 1, 2009, Olympic Company adopted a stock-option plan that granted options to key executives to purchase 40,000 shares of the company’s $10 par value common stock. The options were granted on January 2, 2010, and were exercisable 2 years after

(Issuance, Exercise, and Termination of Stock Options) On January 1, 2010, Magilla Inc. granted stock options to officers and key employees for the purchase of 20,000 shares of the company’s $10 par common stock at $25 per share. The options were exercisable within a 5-year period beginning

(Issuance, Exercise, and Termination of Stock Options) On January 1, 2009, Scooby Corporation granted 10,000 options to key executives. Each option allows the executive to purchase one share of Scooby’s $5 par value common stock at a price of $20 per share. The options were exercisable within a

(Accounting for Restricted Stock) Derrick Company issues 4,000 shares of restricted stock to its CFO, Dane Yapping, on January 1, 2010. The stock has a fair value of $120,000 on this date. The service period related to this restricted stock is 4 years. Vesting occurs if Yapping stays with the

(Accounting for Restricted Stock) Tweedie Company issues 10,000 shares of restricted stock to its CFO, Mary Tokar, on January 1, 2010. The stock has a fair value of $500,000 on this date. The service period related to this restricted stock is 5 years. Vesting occurs if Tokar stays with the company

(Weighted-Average Number of Shares) Gogean Inc. uses a calendar year for financial reporting. The company is authorized to issue 9,000,000 shares of $10 par common stock. At no time has Gogean issued any potentially dilutive securities. Listed below is a summary of Gogean’s common stock

(EPS: Simple Capital Structure) On January 1, 2010, Chang Corp. had 480,000 shares of common stock outstanding. During 2010, it had the following transactions that affected the common stock account. February 1 Issued 120,000 sharesMarch 1

(EPS: Simple Capital Structure) Ott Company had 210,000 shares of common stock outstanding on December 31, 2010. During the year 2011 the company issued 8,000 shares on May 1 and retired 14,000 shares on October 31. For the year 2011 Ott Company reported net income of $229,690 after a casualty loss

(EPS: Simple Capital Structure) Kendall Inc. presented the following data.Net income

(EPS: Simple Capital Structure) A portion of the statement of income and retained earnings of Pierson Inc. for the current year follows. Note 1 during the year, Pierson Inc. suffered a major casualty loss of $1,340,000 after applicable income tax reduction of $1,200,000. At the end of the current

(EPS: Simple Capital Structure) On January 1, 2010, Bailey Industries had stock outstanding as follows.6% Cumulative preferred stock, $100 par value, issued and outstanding 10,000 shares ………… $1,000,000Common stock, $10 par value, issued

(EPS: Simple Capital Structure) At January 1, 2010, Cameron Company’s outstanding shares included the following.280,000 shares of $50 par value, 7% cumulative preferred stock800,000 shares of $1 par value common stockNet income for 2010 was $2,830,000. No cash dividends were declared or paid

(EPS with Convertible Bonds, Various Situations) In 2010 Buraka Enterprises issued, at par, 75 $1,000, 8% bonds, each convertible into 100 shares of common stock. Buraka had revenues of $17,500 and expenses other than interest and taxes of $8,400 for 2011. (Assume that the tax rate is 40%)

(EPS with Convertible Bonds) On June 1, 2009, Bluhm Company and Amanar Company merged to form Davenport Inc. A total of 800,000 shares were issued to complete the merger. The new corporation reports on a calendar-year basis. On April 1, 2011, the company issued an additional 600,000 shares of stock

(EPS with Convertible Bonds and Preferred Stock) The Ottey Corporation issued 10-year, $4,000,000 par, 7% callable convertible subordinated debentures on January 2, 2010. The bonds have a par value of $1,000, with interest payable annually. The current conversion ratio is 14 : 1, and in 2 years it

(EPS with Convertible Bonds and Preferred Stock) On January 1, 2010, Lindsey Company issued 10-year, $3,000,000 face value, 6% bonds, at par. Each $1,000 bond is convertible into 15 shares of Lindsey common stock. Lindsey’s net income in 2011 was $240,000, and its tax rate was 40%. The company

(EPS with Options, Various Situations) Zambrano Company’s net income for 2010 is $40,000. The only potentially dilutive securities outstanding were 1,000 options issued during 2009, each exercisable for one share at $8. None has been exercised, and 10,000 shares of common were outstanding during

(EPS with Contingent Issuance Agreement) Brooks Inc. recently purchased Donovan Corp., a large mid western home Painting Corporation. One of the terms of the merger was that if Donovan’s income for 2011 was $110,000 or more, 10,000 additional shares would be issued to Donovan’s stockholders in

(EPS with Warrants) Worth Corporation earned $260,000 during a period when it had an average of 100,000 shares of common stock outstanding. The common stock sold at an average market price of $15 per share during the period. Also outstanding were 30,000 warrants that could be exercised to purchase

(Stock-Appreciation Rights) On December 31, 2007, Flessel Company issues 120,000 stock appreciation rights to its officers entitling them to receive cash for the difference between the market price of its stock and a pre-established price of $10. The fair value of the SARs is estimated to be $4 per

(Stock-Appreciation Rights) Derrick Company establishes a stock-appreciation rights program that entitles its new president Dan Scott to receive cash for the difference between the market price of the stock and a pre-established price of $30 (also market price) on December 31, 2008, on 40,000 SARs.

(Entries for Various Dilutive Securities) The stockholders’ equity section of Martino Inc. at the beginning of the current year appears below.Common stock, $10 par value, authorized 1,000,000shares, 300,000 shares issued and outstanding $3,000,000Paid-in

(Entries for Conversion, Amortization, and Interest of Bonds) Volker Inc. issued $2,500,000 of convertible 10-year bonds on July 1, 2010. The bonds provide for 12% interest payable semiannually on January 1 and July 1. The discount in connection with the issue was $54,000, which is being amortized

(Stock-Option Plan) Berg Company adopted a stock-option plan on November 30, 2009, that provided that 70,000 shares of $5 par value stock be designated as available for the granting of options to officers of the corporation at a price of $9 a share. The market value was $12 a share on November 30,

(Stock-Based Compensation) Assume that Amazon has a stock-option plan for top management. Each stock option represents the right to purchase a share of Amazon $1 par value common stock in the future at a price equal to the fair value of the stock at the date of the grant. Amazon has 5,000 stock

(EPS with Complex Capital Structure) Amy Dyken, controller at Fitzgerald Pharmaceutical Industries, a public company, is currently preparing the calculation for basic and diluted earnings per share and the related disclosure for Fitzgerald's financial statements. Below is selected financial

(Basic EPS: Two-Year Presentation) Melton Corporation is preparing the comparative financial statements for the annual report to its shareholders for fiscal years ended May 31, 2010, and May 31, 2011. The income from operations for each year was $1,800,000 and $2,500,000, respectively. In both

(Computation of Basic and Diluted EPS) Charles Austin of the controller’s office of Thompson Corporation was given the assignment of determining the basic and diluted earnings per share values for the year ending December 31, 2011. Austin has compiled the information listed below.1. The

(Computation of Basic and Diluted EPS) The information below pertains to Barkley Company for 2010.Net income for the year.................................................................$1,200,0008% convertible bonds issued at par ($1,000 per bond).Each bond is convertible into 30 shares of common

(EPS with Stock Dividend and Extraordinary Items) Agassi Corporation is preparing the comparative financial statements to be included in the annual report to stockholders. Agassi employs a fiscal year ending May 31. Income from operations before income taxes for Agassi was $1,400,000 and $660,000,

Explain the difference between pretax financial income and taxable income.

What are the two objectives of accounting for income taxes?

Interest on municipal bonds is referred to as a permanent difference when determining the proper amount to report for deferred taxes. Explain the meaning of permanent differences, and give two other examples.

Explain the meaning of a temporary difference as it relates to deferred tax computations, and give three examples.

Differentiate between an originating temporary difference and a reversing difference.

The book basis of depreciable assets for Erwin Co. is $900,000, and the tax basis is $700,000 at the end of 2011. The enacted tax rate is 34% for all periods. Determine the amount of deferred taxes to be reported on the balance sheet at the end of 2011.

Roth Inc. has a deferred tax liability of $68,000 at the beginning of 2011. At the end of 2011, it reports accounts receivable on the books at $90,000 and the tax basis at zero (its only temporary difference). If the enacted tax rate is 34% for all periods, and income tax payable for the period is

What is the difference between a future taxable amount and a future deductible amount? When is it appropriate to record a valuation account for a deferred tax asset?

Pretax financial income for Lake Inc. is $300,000, and its taxable income is $100,000 for 2011. Its only temporary difference at the end of the period relates to a $70,000 difference due to excess depreciation for tax purposes. If the tax rate is 40% for all periods, compute the amount of income

How are deferred tax assets and deferred tax liabilities reported on the balance sheet?

Describe the procedures involved in segregating various deferred tax amounts into current and noncurrent categories.

How is it determined whether deferred tax amounts are considered to be “related” to specific asset or liability amounts?

At the end of the year, Falabella Co. has pretax financial income of $550,000. Included in the $550,000 is $70,000 interest income on municipal bonds, $25,000 fine for dumping hazardous waste, and depreciation of $60,000. depreciation for tax purposes is $45,000. Compute income taxes payable,

Addison Co. has one temporary difference at the beginning of 2010 of $500,000. The deferred tax liability established for this amount is $150,000, based on a tax rate of 30%. The temporary difference will provide the following taxable amounts: $100,000 in 2011; $200,000 in 2012, and $200,000 in

What are some of the reasons that the components of income tax expense should be disclosed and reconciliation between the effective tax rate and the statutory tax rate be provided?

Differentiate between “loss carry back” and “loss carry forward.” Which can be accounted for with the greater certainty when it arises? Why?

What are the possible treatments for tax purposes of a net operating loss? What are the circumstances that determine the option to be applied? What is the proper treatment of a net operating loss for financial reporting purposes?

What controversy relates to the accounting for net operating loss carry forwards?

What is an uncertain tax position, and what are the general guidelines for accounting for uncertain tax positions?

Where can authoritative iGAAP related to the accounting for taxes be found?

Briefly describe some of the similarities and differences between U.S. GAAP and iGAAP with respect to income tax accounting.

Describe the current convergence efforts of the FASB and IASB in the area of accounting for taxes.

In 2010, Amir ante Corporation had pretax financial income of $168,000 and taxable income of $120,000. The difference is due to the use of different depreciation methods for tax and accounting purposes. The effective tax rate is 40%. Compute the amount to be reported as income taxes payable at

Oxford Corporation began operations in 2010 and reported pretax financial income of $225,000 for the year. Oxford’s tax depreciation exceeded its book depreciation by $40,000. Oxford’s tax rate for 2010 and years thereafter is 30%. In its December 31, 2010 balance sheet, what amount of deferred

Using the information from BE19-2, assume this is the only difference between Oxford’s pretax financial income and taxable income. Prepare the journal entry to record the income tax expense, deferred income taxes, and income tax payable, and show how the deferred tax liability will be classified

At December 31, 2010, Appaloosa Corporation had a deferred tax liability of $25,000. At December 31, 2011, the deferred tax liability is $42,000. The corporation’s 2011 current tax expense is $48,000.What amount should Appaloosa report as total 2011 tax expense?

At December 31, 2010, Suffolk Corporation had an estimated warranty liability of $105,000 for accounting purposes and $0 for tax purposes. (The warranty costs are not deductible until paid.) The effective tax rate is 40%. Compute the amount Suffolk should report as a deferred tax asset at December

At December 31, 2010, Percheron Inc. had a deferred tax asset of $30,000. At December 31, 2011, the deferred tax asset is $59,000. The corporation’s 2011 current tax expense is $61,000. What amount should Percheron report as total 2011 tax expense?

At December 31, 2010, Hill yard Corporation has a deferred tax asset of $200,000. After a careful review of all available evidence, it is determined that it is more likely than not that $60,000 of this deferred tax asset will not be realized, prepare the necessary journal entry.

Mitchell Corporation had income before income taxes of $195,000 in 2010. Mitchell’s current income tax expense is $48,000, and deferred income tax expense is $30,000. Prepare Mitchell’s 2010 income statement, beginning with income before income taxes.

Shetland Inc. had pretax financial income of $154,000 in 2010. Included in the computation of that amount is insurance expense of $4,000 which is not deductible for tax purposes. In addition, depreciation for tax purposes exceeds accounting depreciation by $10,000. Prepare Shetland’s journal

Clydesdale Corporation has a cumulative temporary difference related to depreciation of $580,000 at December 31, 2010. This difference will reverse as follows: 2011, $42,000; 2012, $244,000; and 2013, $294,000. Enacted tax rates are 34% for 2011 and 2012, and 40% for 2013. Compute the amount

At December 31, 2010, Fell Corporation had a deferred tax liability of $680,000, resulting from future taxable amounts of $2,000,000 and an enacted tax rate of 34%. In May 2011, a new income tax act is signed into law that raises the tax rate to 40% for 2011 and future years. Prepare the journal

Conlin Corporation had the following tax information. In 2011 Conlin suffered a net operating loss of $480,000, which it elected to carry back. The 2011 enacted tax rate is 29%. Prepare Conlin's entry to record the effect of the loss carry back.

Rode Inc. incurred a net operating loss of $500,000 in 2010. Combined income for 2008 and 2009 was $350,000. The tax rate for all years is 40%. Rode elects the carry back option. Prepare the journal entries to record the benefits of the loss carry back and the loss carry forward.

Use the information for Rode Inc. given in BE19-13. Assume that it is more likely than not that the entire net operating loss carry forward will not be realized in future years. Prepare all the journal entries necessary at the end of 2010.

Youngman Corporation has temporary differences at December 31, 2010, that result in the following deferred taxes.Deferred tax liability—current...........................$38,000Deferred tax asset—current............................$(62,000)Deferred tax

Access the glossary (“Master Glossary”) to answer the following.(a) What is a deferred tax asset?(b) What is taxable income?(c) What is the definition of valuation allowance?(d) What is a deferred tax liability?

What are the two basic requirements applied to the measurement of current and deferred income taxes at the date of the financial statements?

A company wishes to conduct business in a foreign country that attracts businesses by granting “holidays” from income taxes for a certain period of time. Would the company have to disclose this “holiday” to the SEC? If so, what information must be disclosed?

When is a company allowed to initially recognize the financial statement effects of a tax position?

(One Temporary Difference, Future Taxable Amounts, One Rate, No Beginning Deferred Taxes) Starfleet Corporation has one temporary difference at the end of 2010 that will reverse and cause taxable amounts of $55,000 in 2011, $60,000 in 2012, and $75,000 in 2013. Starfleet’s pretax financial income

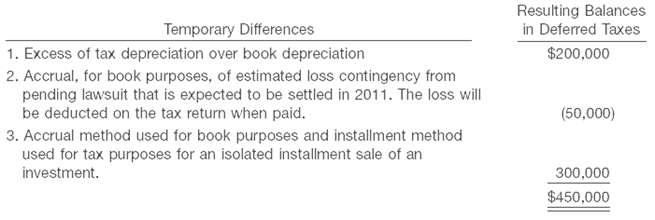

(Two Differences, No Beginning Deferred Taxes, Tracked through 2 Years) The following information is available for McKee Corporation for 2010.1. Excess of tax depreciation over book depreciation, $40,000. This $40,000 difference will reverse equally over the years 2011–2014.2. Deferral, for book

(One Temporary Difference, Future Taxable Amounts, One Rate, Beginning Deferred Taxes) Brennan Corporation began 2010 with a $90,000 balance in the Deferred Tax Liability account. At the end of 2010, the related cumulative temporary difference amounts to $350,000 and it will reverse evenly over the

(Three Differences, Compute Taxable Income, Entry for Taxes) Havaci Company reports pretax financial income of $80,000 for 2010. The following items cause taxable income to be different than pretax financial income.1. Depreciation on the tax return is greater than Depreciation on the income

(Two Temporary Differences, One Rate, Beginning Deferred Taxes) The following facts relate to Alschuler Corporation.1. Deferred tax liability, January 1, 2010, $40,000.2. Deferred tax asset, January 1, 2010, $0.3. Taxable income for 2010, $115,000.4. Pretax financial income for 2010, $200,000.5.

(Identify Temporary or Permanent Differences) Listed below are items that are commonly accounted for differently for financial reporting purposes than they are for tax purposes.For each item below, indicate whether it involves:(1) A temporary difference that will result in future deductible amounts

(Terminology, Relationships, Computations, Entries)Complete the following statements by filling in the blanks.(a) In a period in which a taxable temporary difference reverses, the reversal will cause taxable income to be _______ (less than, greater than) pretax financial income.(b) If a $68,000

(Two Temporary Differences, One Rate, 3 Years) Gordon Company has two temporary differences between its income tax expense and income taxes payable. The information is shown below. The income tax rate for all years is 40%. (a) Prepare the journal entry to record income tax expense, deferred income

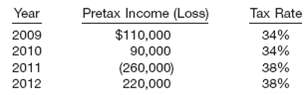

(Carry back and Carry forward of NOL, No Valuation Account, No Temporary Differences) The pretax financial income (or loss) figures for Synergetic Company are as

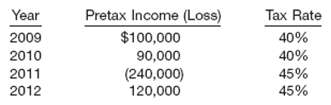

(Two NOLs, No Temporary Differences, No Valuation Account, Entries and Income Statement) Lanier Corporation has pretax financial income (or loss) equal to taxable income (or loss) from 2003 through 2011 as follows. Pretax financial income (loss) and taxable income (loss) were the same for all years

(Three Differences, Classify Deferred Taxes) At December 31, 2010, Cascade Company had a net deferred tax liability of $450,000. An explanation of the items that compose this balance is as follows. Indicate the manner in which deferred taxes should be presented on Cascade Company's December 31,

(Two Temporary Differences, One Rate, Beginning Deferred Taxes, Compute Pretax Financial Income) The following facts relate to Mc Kane Corporation.1. Deferred tax liability, January 1, 2010, $60,000.2. Deferred tax asset, January 1, 2010, $20,000.3. Taxable income for 2010, $115,000.4. Cumulative

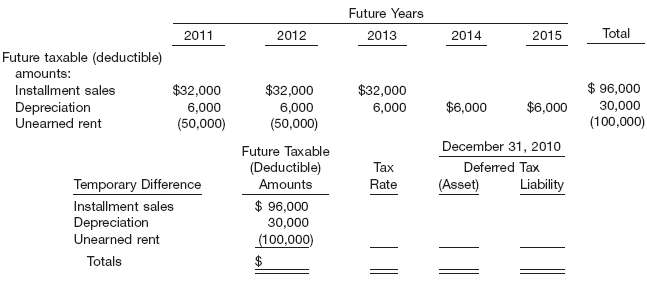

(One Difference, Multiple Rates, Effect of Beginning Balance versus No Beginning Deferred Taxes) At the end of 2010, Wasicsko Company has $180,000 of cumulative temporary differences that will result in reporting future taxable amounts as follows.2011.......................................$

(Deferred Tax Asset with and without Valuation Account) Callaway Corp. has a deferred tax asset account with a balance of $150,000 at the end of 2010 due to a single cumulative temporary difference of $375,000. At the end of 2011 this same temporary difference has increased to a cumulative amount

(Deferred Tax Asset with Previous Valuation Account) Assume the same information as E19-14, except that at the end of 2010, Callaway Corp. had a valuation account related to its deferred tax asset of $40,000.(a) Record income tax expense, deferred income taxes, and income taxes payable for 2011,

(Deferred Tax Liability, Change in Tax Rate, Prepare Section of Income Statement) Sharer Inc.’s only temporary difference at the beginning and end of 2010 is caused by a $2 million deferred gain for tax purposes for an installment sale of a plant asset, and the related receivable (only one-half

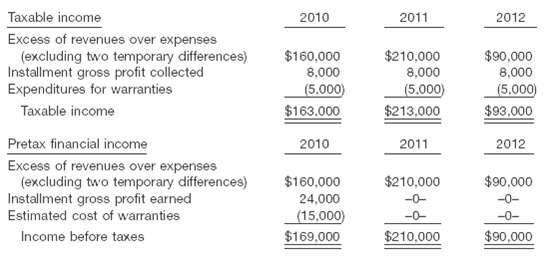

(Two Temporary Differences, Tracked through 3 Years, Multiple Rates) Taxable income and pretax financial income would be identical for Jones Co. except for its treatments of gross profit on installment sales and estimated costs of warranties. The following income computations have been prepared.

(Three Differences, Multiple Rates, Future Taxable Income) During 2010, Graham Co.'s first year of operations, the company reports pretax financial income of $250,000. Graham's enacted tax rate is 40% for 2010 and 35% for all later years. Graham expects to have taxable income in each of the next 5

(Two Differences, One Rate, Beginning Deferred Balance, Compute Pretax Financial Income) Shamess Co. establishes a $90 million liability at the end of 2010 for the estimated litigation settlement for manufacturing defects. All related costs will be paid and deducted on the tax return in 2011. Also,

(Two Differences, No Beginning Deferred Taxes, Multiple Rates) Macinski Inc., in its first year of operations, has the following differences between the book basis and tax basis of its assets and liabilities at the end of 2010.It is estimated that the warranty liability will be settled in 2011. The

(Two Temporary Differences, Multiple Rates, Future Taxable Income) Flynn Inc. has two temporary differences at the end of 2010. The first difference stems from installment sales, and the second one results from the accrual of a loss contingency. Flynn's accounting department has developed a

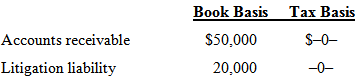

(Two Differences, One Rate, First Year) The differences between the book basis and tax basis of the assets and liabilities of Morgan Corporation at the end of 2010 are presented below.It is estimated that the litigation liability will be settled in 2011. The difference in accounts receivable will

(NOL Carry back and Carry forward, Valuation Account versus No Valuation Account) Sondgeroth Inc. reports the following pretax income (loss) for both financial reporting purposes and tax purposes. (Assume the carry back provision is used for a net operating loss.) The tax rates listed were all

(NOL Carry back and Carry forward, Valuation Account Needed) Nielson Inc. reports the following pretax income (loss) for both book and tax purposes. (Assume the carry back provision is used where possible for a net operating loss.) The tax rates listed were all enacted by the beginning of 2009. (a)

(NOL Carry back and Carry forward, Valuation Account Needed) Hayes Co. reported the following pretax financial income (loss) for the years

(Objectives and Principles for Accounting for Income Taxes) The amount of income taxes due to the government for a period of time is rarely the amount reported on the income statement for that period as income tax expense.(a) Explain the objectives of accounting for income taxes in general purpose

Showing 600 - 700

of 107766

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers