New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

accounting

Intermediate Accounting 13th Edition Donald E. Kieso, Jerry J. Weygandt, And Terry D. Warfield - Solutions

(Basic Accounting for Temporary Differences) Dexter Company appropriately uses the asset liability method to record deferred income taxes. Dexter reports depreciation expense for certain machinery purchased this year using the modified accelerated cost recovery system (MACRS) for income tax

(Identify Temporary Differences and Classification Criteria) The asset-liability approach for recording deferred income taxes is an integral part of generally accepted accounting principles.(a) Indicate whether each of the following independent situations should be treated as a temporary difference

(Accounting and Classification of Deferred Income Taxes)Part AThis year Gumowski Company has each of the following items in its income statement.1. Gross profits on installment sales.2. Revenues on long-term construction contracts.3. Estimated costs of product warranty contracts.4. Premiums on

(Explain Computation of Deferred Tax Liability for Multiple Tax Rates) At December 31, 2010, Higley Corporation has one temporary difference which will reverse and cause taxable amounts in 2011. In 2010 a new tax act set taxes equal to 45% for 2010, 40% for 2011, and 34% for 2012 and years

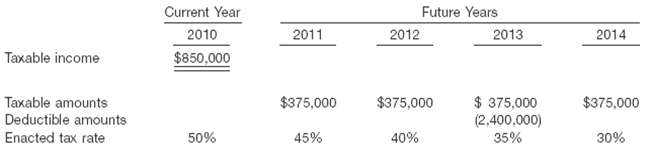

(Explain Future Taxable and Deductible Amounts, How Carry back and Carry forward Affects Deferred Taxes) Maria Rodriquez and Lynette Kingston are discussing accounting for income taxes. They are currently studying a schedule of taxable and deductible amounts that will arise in the future as a

(Deferred Taxes, Income Effects) Stephanie Delaney, CPA, is the newly hired director of corporate taxation for Acme Incorporated, which is a publicly traded corporation. Ms. Delaney’s first job with Acme was the review of the company’s accounting practices on deferred income taxes. In doing her

Refer to P&G’s financial statements and the accompanying notes to answer the following questions.(a) What amounts relative to income taxes does P&G report in it’s:(1) 2007 income statement?(2) June 30, 2007, balance sheet?(3) 2007 statement of cash flows?(b) P&G’s provision for

Go to the book’s companion website and use information found there to answer the following questions related to The Coca-Cola Company and PepsiCo, Inc.(a) What are the amounts of Coca-Cola’s and PepsiCo’s provision for income taxes for the year 2007? Of each company’s 2007 provision for

Home stake Mining Company is a 120-year-old international gold mining company with substantial gold mining operations and exploration in the United States, Canada, and Australia. At year-end, Home stake reported the following items related to income taxes (thousands of dollars).Total current

(Three Differences, No Beginning Deferred Taxes, Multiple Rates) The following information is available for Rammers Corporation for 2010.1. Depreciation reported on the tax return exceeded Depreciation reported on the income statement by $120,000. This difference will reverse in equal amounts of

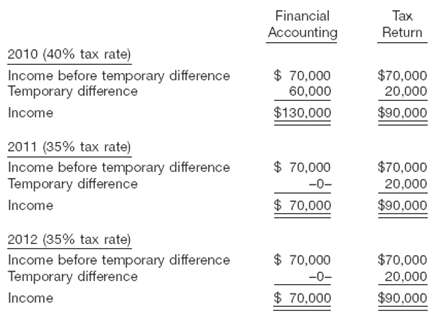

(One Temporary Difference, Tracked for 4 Years, One Permanent Difference, Change in Rate) The pretax financial income of Truttman Company differs from its taxable income throughout each of 4 years as follows. Pretax financial income for each year includes a nondeductible expense of $30,000 (never

(Second Year of Depreciation Difference, Two Differences, Single Rate, Extraordinary Item) The following information has been obtained for the Gocker Corporation.1. Prior to 2010, taxable income and pretax financial income were identical.2. Pretax financial income is $1,700,000 in 2010 and

(Permanent and Temporary Differences, One Rate) The accounting records of Shinault Inc. show the following data for 2010.1. Life insurance expense on officers was $9,000.2. Equipment was acquired in early January for $300,000. Straight-line depreciation over a 5-year life is used, with no salvage

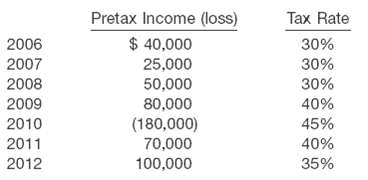

(NOL without Valuation Account) Jennings Inc. reported the following pretax income (loss) and related tax rates during the years 2006' ?2012. Pretax financial income (loss) and taxable income (loss) were the same for all years since Jennings began business. The tax rates from 2009' ?2012 were

Two Differences, Two Rates, Future Income Expected) Presented below are two independent situations related to future taxable and deductible amounts resulting from temporary differences existing at December 31, 2010. 1. Mooney Co. has developed the following schedule of future taxable and deductible

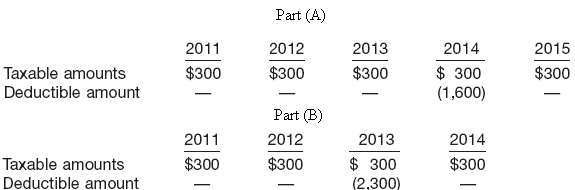

(One Temporary Difference, Tracked 3 Years, Change in Rates, Income Statement Presentation) Crosley Corp. sold an investment on an installment basis. The total gain of $60,000 was reported for financial reporting purposes in the period of sale. The company qualifies to use the installment-sales

Two Differences, 2 Years, Compute Taxable Income and Pretax Financial Income) The following information was disclosed during the audit of Elbert Inc. 2. On January 1, 2010, equipment costing $600,000 is purchased. For financial reporting purposes, the company uses straight-line depreciation over a

(Five Differences, Compute Taxable Income and Deferred Taxes, Draft Income Statement) Wise Company began operations at the beginning of 2011. The following information pertains to this company.1. Pretax financial income for 2011 is $100,000.2. The tax rate enacted for 2011 and future years is

What is a private pension plan? How does a contributory pension plan differ from a noncontributory plan?

Differentiate between a defined-contribution pension plan and a defined-benefit pension plan. Explain how the employer’s obligation differs between the two types of plans.

Differentiate between “accounting for the employer” and “accounting for the pension fund.”

The meaning of the term “fund” depends on the context in which it is used. Explain its meaning when used as a noun. Explain its meaning when it is used as a verb.

What is the role of an actuary relative to pension plans what are actuarial assumptions?

What factors must be considered by the actuary in measuring the amount of pension benefits under a defined benefit plan?

Name three approaches to measuring benefit obligations from a pension plan and explain how they differ.

Explain how cash-basis accounting for pension plans differs from accrual-basis accounting for pension plans. Why is cash-basis accounting generally considered unacceptable for pension plan accounting?

Identify the five components that comprise pension expense. Briefly explain the nature of each component.

What is service cost, and what is the basis of its measurement?

In computing the interest component of pension expense, what interest rates may be used?

Explain the difference between service cost and prior service cost.

What is meant by “prior service cost”? When is prior service cost recognized as pension expense?

What are “liability gains and losses,” and how are they accounted for?

If pension expense recognized in a period exceeds the current amount funded by the employer, what kind of account arises, and how should it be reported in the financial statements? If the reverse occurs—that is, current funding by the employer exceeds the amount recognized as pension

Given the items and amounts shown on page 1094, compute the actual return on plan assets: fair value of plan assets at the beginning of the period $9,500,000; benefits paid during the period $1,400,000; contributions made during the period $1,000,000; and fair value of the plan assets at the end of

How does an “asset gain or loss” develop in pension accounting? How does a “liability gain or loss” develop in pension accounting?

What is the meaning of “corridor amortization”?

At the end of the current period, Agler Inc. had a projected benefit obligation of $400,000 and pension plan assets (at fair value) of $350,000. What are the accounts and amounts that will be reported on the company’s balance sheet as pension assets or pension liabilities?

At the end of the current year, Pociek Co. has prior service cost of $9,150,000. Where should the prior service cost be reported on the balance sheet?

Describe the accounting for actuarial gains and losses.

Boey Company reported net income of $25,000 in 2011. It had the following amounts related to its pension plan in 2011: Actuarial liability gain $10,000; Unexpected asset loss $14,000; Accumulated other comprehensive income (G/L) (beginning balance), zero. Determine for 2011(a) Boey’s other

Describe the reporting of pension plans for a company with multiple plans, some of which are underfunded and some of which are overfunded.

Determine the meaning of the following terms.(a) Contributory plan.(b) Vested benefits.(c) Retroactive benefits.(d) Years-of-service method.

A headline in the Wall Street Journal stated, “Firms Increasingly Tap Their Pension Funds to Use Excess Assets.” What is the accounting issue related to the use of these “excess assets” by companies?

Where can authoritative iGAAP related to the accounting for pensions be found?

Briefly describe some of the similarities and differences between U.S. GAAP and iGAAP with respect to the accounting for pensions.

Cadbury Company, which uses iGAAP, has a postretirement benefit plan. During 2010 Cadbury recognized $30,000 unexpected asset gains in income. Just $10,000 of the gains exceeded the corridor, and the average remaining service lives of Cadbury’s employees is 10 years. Discuss how Cadbury’s

Briefly discuss the IASB/FASB convergence efforts in the area of postretirement-benefit accounting.

What are postretirement benefits other than pensions?

Why didn’t the FASB cover both types of postretirement benefits—pensions and healthcare—in the earlier pension accounting rules?

What are the major differences between postretirement healthcare benefits and pension benefits?

What is the difference between the APBO and the EPBO? What are the components of postretirement expense?

Access the glossary (“Master Glossary”) to answer the following.(a) What is an accumulated benefit obligation?(b) What is a defined benefit postretirement plan?(c) What is the definition of “actuarial present value”?(d) What is a prior service cost?

In general, how can an employer choose an appropriate discount rate for its pension plan? What information could an employer use in choosing a discount rate?

If an employer has a defined-benefit pension plan, what components would make up its net periodic pension cost?

What information about its pension plan must a publicly traded company disclose in its interim financial statements?

AMR Corporation (parent company of American Airlines) reported the following for 2007 (in millions).Service cost.................................................$370Interest on P.B.O.........................................672Return on plan assets.................................747Amortization of

For Warren Corporation, year-end plan assets were $2,000,000. At the beginning of the year, plan assets were $1,780,000. During the year, contributions to the pension fund were $120,000, and benefits paid were $200,000. Compute Warren’s actual return on plan assets.

At January 1, 2010, Beatty Company had plan assets of $280,000 and a projected benefit obligation of the same amount. During 2010, service cost was $27,500, the settlement rate was 10%, actual and expected return on plan assets were $25,000, contributions were $20,000, and benefits paid were

For 2007, Campbell Soup Company had pension expense of $32 million and contributed $32 million to the pension fund. Prepare Campbell Soup Company’s journal entry to record pension expense and funding.

Mancuso Corporation amended its pension plan on January 1, 2010, and granted $160,000 of prior service costs to its employees. The employees are expected to provide 2,000 service years in the future, with 350 service years in 2010. Compute prior service cost amortization for 2010.

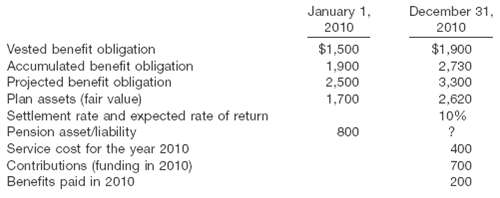

At December 31, 2010, Besler Corporation had a projected benefit obligation of $560,000, plan assets of $322,000, and prior service cost of $127,000 in accumulated other comprehensive income. Determine the pension asset/liability at December 31, 2010.

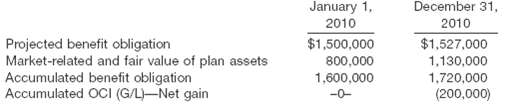

Shin Corporation had a projected benefit obligation of $3,100,000 and plan assets of $3,300,000 at January 1, 2010. Shin also had a net actuarial loss of $465,000 in accumulated OCI at January 1, 2010. The average remaining service period of Shin’s employees is 7.5 years. Compute Shin’s minimum

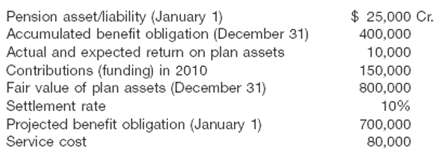

Hawkins Corporation has the following balances at December 31, 2010.Projected benefit obligation $2,600,000Plan assets at fair value 2,000,000Accumulated

Norton Co. had the following amounts related to its pension plan in 2010. Actuarial liability loss for 2010

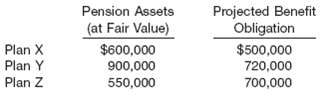

Lahey Corp. has three defined-benefit pension plans as follows. How will Lahey report these multiple plans in its financial statements?

Manno Corporation has the following information available concerning its postretirement benefit plan for 2010.Service cost

For 2010, Sampsell Inc. computed its annual postretirement expense as $240,900. Sampsell’s contribution to the plan during 2010 was $180,000. Prepare Sampsell’s 2010 entry to record postretirement expense.

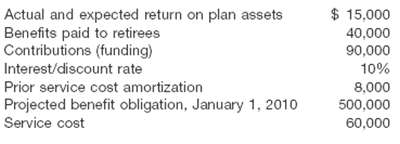

(Pension Expense, Journal Entries) The following information is available for the pension plan of Brady Company for the year 2010. (a) Compute pension expense for the year 2010. (b) Prepare the journal entry to record pension expense and the employer's contribution to the pension plan in 2010.

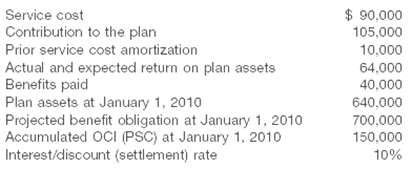

(Computation of Pension Expense) Bickner Company provides the following information about its defined-benefit pension plan for the year 2010. Compute the pension expense for the year 2010.

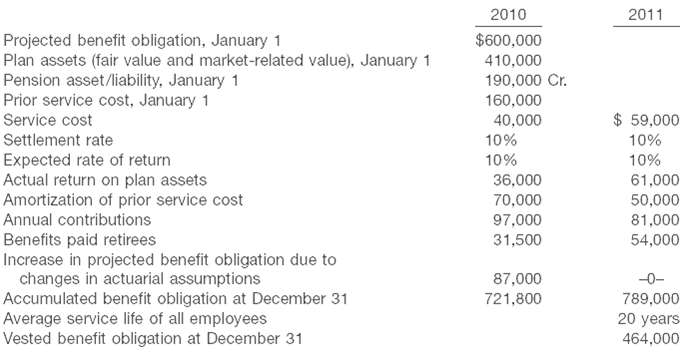

(Preparation of Pension Worksheet) Using the information in E20-2 prepare a pension worksheet inserting January 1, 2010, balances, showing December 31, 2010, balances, and the journal entry recording pension expense.

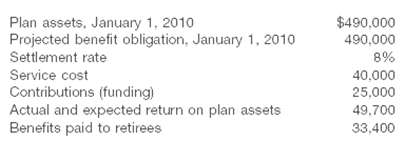

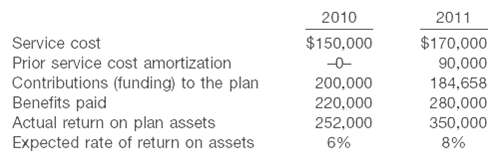

(Basic Pension Worksheet) The following facts apply to the pension plan of Boudreau Inc. for the year 2010. Using the preceding data, compute pension expense for the year 2010, as part of your solution, prepare a pension worksheet that shows the journal entry for pension expense for 2010 and the

(Application of Years-of-Service Method) Andrews Company has five employees participating in its defined-benefit pension plan. Expected years of future service for these employees at the beginning of 2010 are as follows. On January 1, 2010, the company amended its pension plan increasing its

(Computation of Actual Return) Gingrich Importers provides the following pension plan information. Fair value of pension plan assets, January 1, 2010 $2,400,000Fair value of pension plan assets, December 31, 2010

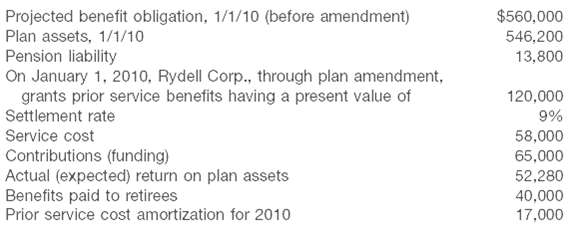

(Basic Pension Worksheet) The following defined pension data of Rydell Corp. apply to the year 2010. For 2010, prepare a pension worksheet for Rydell Corp. that shows the journal entry for pension expense and the year-end balances in the related pension accounts.

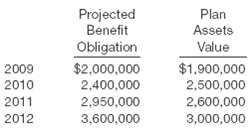

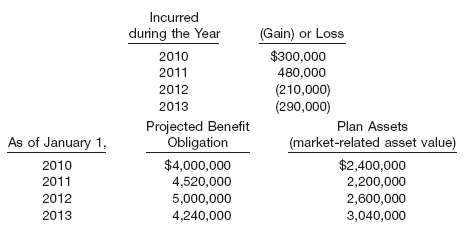

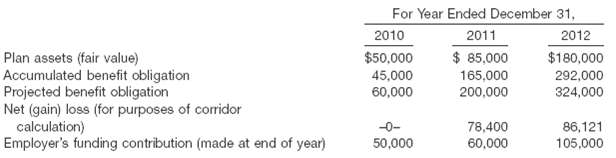

(Application of the Corridor Approach) Kensett Corp. has the following beginning-of-the-year present values for its projected benefit obligation and market-related values for its pension plan assets. The average remaining service life per employee in 2009 and 2010 is 10 years and in 2011 and 2012

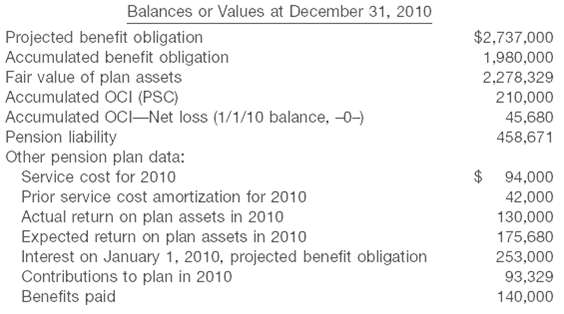

(Disclosures: Pension Expense and Other Comprehensive Income) Tavares Enterprises provides the following information relative to its defined benefit pension plan. (a) Prepare the note disclosing the components of pension expense for the year 2010. (b) Determine the amounts of other comprehensive

(Pension Worksheet) Webb Corp. sponsors a defined-benefit pension plan for its employees. On January 1, 2010, the following balances relate to this plan.Plan assets

(Pension Expense, Journal Entries, Statement Presentation) Henning Company sponsors a defined benefit pension plan for its employees. The following data relate to the operation of the plan for the year 2010 in which no benefits were paid.1. The actuarial present value of future benefits earned by

(Pension Expense, Journal Entries, Statement Presentation) Ferrari Company received the following selected information from its pension plan trustee concerning the operation of the company's defined benefit pension plan for the year ended December 31, 2010. The service cost component of pension

(Computation of Actual Return, Gains and Losses, Corridor Test, and Pension Expense) Erickson Company sponsors a defined benefit pension plan. The corporation's actuary provides the following information about the plan. (a) Compute the actual return on the plan assets in 2010. (b) Compute the

(Worksheet for E20-13) Using the information in E20-13 about Erickson Company’s defined benefit pension plan, prepare a 2010 pension worksheet with supplementary schedules of computations. Prepare the journal entries at December 31, 2010, to record pension expense and related pension

(Pension Expense, Journal Entries) Latoya Company provides the following selected information related to its defined-benefit pension plan for 2010. (a) Compute pension expense and prepare the journal entry to record pension expense and the employer's contribution to the pension plan in 2010.

(Amortization of Accumulated OCI (G/L), Corridor Approach, Pension Expense Computation) The actuary for the pension plan of Gustafson Inc. calculated the following net gains and losses. Other information about the company's pension obligation and plan assets is as follows. Gustafson Inc. has a

(Amortization of Accumulated OCI Balances) Keeton Company sponsors a defined-benefit pension plan for its 600 employees. The company's actuary provided the following information about the plan. The average remaining service life per employee is 10.5 years. The service cost component of net periodic

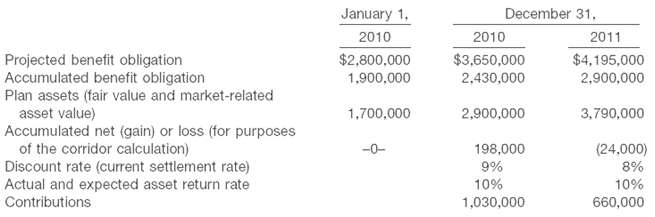

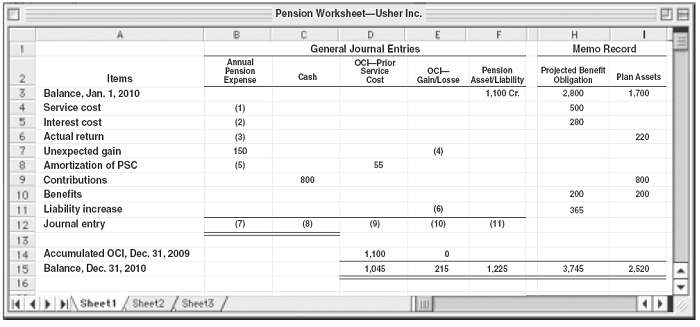

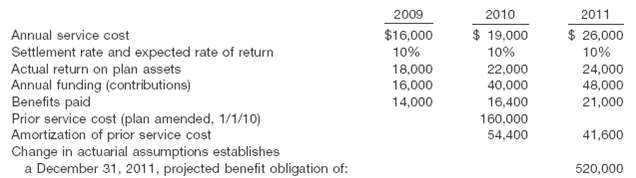

(Pension Worksheet?Missing Amounts) The accounting staff of Usher Inc. has prepared the following pension worksheet. Unfortunately, several entries in the worksheet are not decipherable. The company has asked your assistance in completing the worksheet and completing the accounting tasks related to

(Postretirement Benefit Expense Computation) Kreter Co. provides the following information about its postretirement benefit plan for the year 2010. Compute the postretirement benefit expense for 2010.

(Postretirement Benefit Worksheet) Using the information in *E20-19, prepare a worksheet inserting January 1, 2010, balances, and showing December 31, 2010, balances. Prepare the journal entry recording postretirement benefit expense.

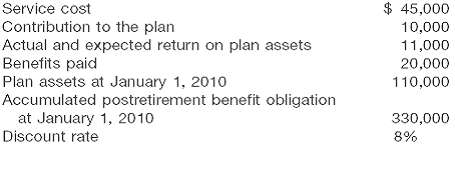

(Postretirement Benefit Expense Computation) Garner Inc. provides the following information related to its postretirement benefits for the year 2010.Accumulated postretirement benefit obligation at January 1, 2010 $710,000Actual and expected

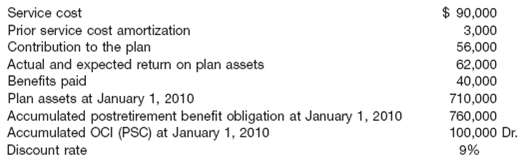

(Postretirement Benefit Expense Computation) Engle hart Co. provides the following information about its postretirement benefit plan for the year 2010. Compute the postretirement benefit expense for2010.

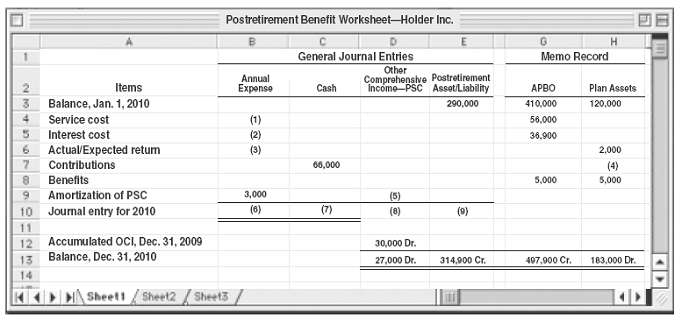

(Postretirement Benefit Worksheet—Missing Amounts) The accounting staff of Holder Inc. has prepared the postretirement benefit worksheet on page 1102. Unfortunately, several entries in the worksheet are not decipherable. The company has asked your assistance in completing the worksheet and

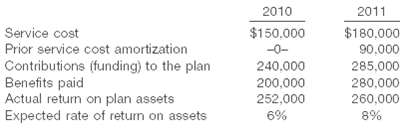

(Postretirement Benefit Worksheet) Using the information in *E20-22, prepare a worksheet inserting January 1, 2010, balances, showing December 31, 2010, balances, and the journal entry recording postretirement benefit expense. (a) Determine the missing amounts in the 2010 postretirement worksheet,

(2-Year Worksheet) On January 1, 2010, Cunningham Company has the following defined benefit pension plan balances.? Projected benefit obligation ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ?$4,500,000 Fair value of plan assets? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ?4,200,000 The interest

(3-Year Worksheet, Journal Entries, and Reporting) Jackson Company adopts acceptable accounting for its defined-benefit pension plan on January 1, 2009, with the following beginning balances: plan assets $200,000; projected benefit obligation $250,000. Other data relating to 3 years' operation of

(Pension Expense, Journal Entries, Amortization of Loss) Gottschalk Company sponsors a defined benefit plan for its 100 employees. On January 1, 2010, the company’s actuary provided the following information.Accumulated other comprehensive loss (PSC)

(Pension Expense, Journal Entries for 2 Years) Gordon Company sponsors a defined benefit pension plan. The following information related to the pension plan is available for 2010 and 2011. (a) Compute pension expense for 2010 and 2011. (b) Prepare the journal entries to record the pension expense

(Computation of Pension Expense, Amortization of Net Gain or Loss???Corridor Approach, Journal Entries for 3 Years) Hiatt Toothpaste Company initiates a defined-benefit pension plan for its 50 employees on January 1, 2010. The insurance company which administers the pension plan provided the

(Computation of Prior Service Cost Amortization, Pension Expense, Journal Entries, and Net Gain or Loss) Aykroyd Inc. has sponsored a noncontributory-defined benefit pension plan for its employees since 1987. Prior to 2010, cumulative net pension expense recognized equaled cumulative contributions

(Pension Worksheet) Hanson Corp. sponsors a defined-benefit pension plan for its employees. On January 1, 2010, the following balances related to this plan.Plan assets (market-related value) $520,000Projected benefit obligation

(Comprehensive 2-Year Worksheet) Lemke Company sponsors a defined-benefit pension plan for its employees. The following data relate to the operation of the plan for the years 2010 and 2011. (a) Prepare a pension worksheet presenting both years 2010 and 2011 and accompanying computations and

(Comprehensive 2-Year Worksheet) Hobbs Co. has the following defined-benefit pension plan balances on January 1, 2010. Projected benefit obligation? ? ? ? ? ? ? ? ? ? ? ? ? ??$4,600,000 Fair value of plan assets? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ? ?4,600,000 The interest (settlement) rate applicable

Showing 700 - 800

of 107766

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers