New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing

Auditing a risk based approach to conducting a quality audit 9th edition Karla Johnstone, Audrey Gramling, Larry Rittenberg - Solutions

The SEC has criticized the auditing profession for not looking at significant changes in accounting estimates. For example, a reserve (liability estimate) may be estimated very high one year and then very low the next year. Explain how an accounting estimate might not be materially misstated for

Auditors make materiality judgments during the planning phase of the audit in order to be sure they ultimately gather sufficient evidence during the audit to provide reasonable assurance that the financial statements are free of material misstatements. The lower the materiality threshold that an

The audit report provides reasonable assurance that the financial statements are free from material misstatements. The auditor is put in a difficult situation because materiality is defined from a user's viewpoint, but the auditor must assess materiality in planning the audit to ensure that

Define the terms inherent risk, control risk, audit risk, and detection risk. Refer to Exhibit and explain how these risks relate to each other.

Describe factors that would lead the auditor to assess inherent risk at the assertion level at a higher level.

Inherent risk at the financial statement level relates to (a) business and operating-related risks and (b) financial reporting risks. The Professional Judgment in Context feature, "Risks Associated with Financial Statement Misstatements," summarizes various risks from ISA 315; that list is

Refer to the Auditing in Practice feature, "Pfizer Pharmaceuticals Risk Disclosures as an Example of Inherent Risk at the Financial Statement Level." Summarize the risks that Pfizer is disclosing. Comment on why these risks might be of concern to the auditor.

List the various resources that the auditor can access to learn about inherent risk relating to the operations of a company.

List the factors that would lead auditors to assess control risk at a higher level. Discuss the techniques that the auditor uses to understand management's risk assessment and other internal control components.

Explain how ratio analysis and industry comparisons can be useful to the auditor in identifying potential risk of material misstatement on an audit engagement. How can such analysis also help the auditor plan the audit?

Brainstorming is a group discussion designed to encourage auditors to creatively assess client risks, particularly those relevant to fraud.a. When does brainstorming typically occur?b. Who attends the brainstorming session? Who leads it?c. Besides encouraging auditors to creatively assess client

The following information shows the past two periods of results for a fictional company, Jones Manufacturing, and a comparison with industry data for the same period:ANALYTICAL DATA FOR JONES MANUFACTURINGa. From the preceding data, identify potential risk areas and explain why they represent

The auditor for a fictional company, ABC Wholesaling, has just begun to perform preliminary analytical procedures as part of planning the audit for the coming year. ABC Wholesaling is in a competitive industry, selling products such as STP Brand products and Ortho Grow products to companies such as

Refer to Exhibit 7.3 and consider the audit risk model, whereby Audit Risk = Inherent Risk × Control Risk × Detection Risk. Complete the boxes in the table below. Describe generalizations about the relationships among the four components of the audit risk model that you

What are examples of how an auditor might change(a) The nature of risk response,(b) The timing of risk response,(c) The extent of risk response?

How can an auditor introduce unpredictability into audit procedures?

On May 22, 2012, the audit firm of Brock, Schechter & Polakoff LLP (hereafter BSP) was censured and fined $20,000 by the PCAOB in relation to its audits of public companies located in Taiwan and China. These public companies were listed on U.S. stock exchanges. James Waggoner, BSP's Director of

The following is a description of various factors that affected the operations of Lincoln Federal Savings and Loan, a California savings and loan (S&L). It was a subsidiary of American Continental Company, a real estate development company run by Charles Keating.Lincoln Federal Savings &

Important factors that lead auditors to assess inherent risk relating to financial reporting at a higher level relate to analyst following, including a history of exactly meeting analyst estimates, analysts having high earnings growth expectations, and a situation in which the company is unable to

The Auditing in Practice feature, "Application of Accounting Principles and Related Disclosures," discusses guidance from AS 12 regarding the auditor's responsibilities to understand management's application of accounting principles and related disclosures. Locate AS 12 on the PCAOB Web site, read

Exhibit provides examples of questions that an auditor should ask when assessing inherent risk relating to financial reporting.The first question asks, "What are the significant judgment areas (reserves, contingencies, asset values, note disclosures) that affect the current year financial

Refer to the Auditing in Practice feature, "Lack of Oversight as a Control Weakness Leads to Embezzlement," and the Auditing in Practice feature, "The City of Dixon, Illinois Sues Its Auditor for $50 Million Related to the Rita Crundwell Embezzlement." The situation described in these features

Locate and read the article listed below and answer the following questions.Johnstone, K. 2000. Client-Acceptance Decisions: Simultaneous Effects of Client Business Risk, Audit Risk, Auditor Business Risk, and Risk Adaptation. Auditing: A Journal of Practice & Theory. 19 (1): 1—25.a. What is

Locate and read the article listed below and answer the following questions.Bowlin, K. 2011. Risk-Based Auditing, Strategic Prompts, and Auditor Sensitivity to the Strategic Risk of Fraud. The Accounting Review 86 (4): 1231-1253.a. What is the issue being addressed in the paper?b. What are the

Ford 10-K 1. Describe the primary risks facing Ford.Toyota 20-F 2. Describe the primary risks facing Toyota.3. Compare the risks of Ford and Toyota.4. Why would an auditor be concerned with these risks?

What is the directional relationship between the risks of material misstatement (inherent and control risk) and both audit risk and detection risk? In other words, if the risks of material misstatement increase or decrease, how are audit risk and detection risk affected?

Distinguish between a controls reliance audit and a substantive audit. Which approach should an auditor consider to be most effective?

What audit procedures can be completed only at or after period end?

TRUE-FALSE QUESTIONS1. Sampling can be used for both tests of controls and direct tests of account balances and assertions.2. Audit procedures such as inquiry, observation, and analytical procedures are the primary audit procedures involving audit sampling.3. Sampling risk is the risk that the

TRUE-FALSE QUESTIONS1. In attributes sampling, the attribute of interest is an individual dollar amount in the population.2. Factual misstatements are those that are the auditor's best estimate of misstatements in a given population based on sample results.3. The division of a population into two

MULTIPLE-CHOICE QUESTIONS1. For which of the following auditing procedures would sampling be most appropriate?a. Examining documents.b. Inquiring of management.c. Observing controls being completed.d. Conducting analytical procedures.2. Which of the following activities would be most likely to be

MULTIPLE-CHOICE QUESTIONS1. Refer to Exhibit. Assume a 5% risk of overreliance, a tolerable deviation rate of 8%, a sample size of 100, and that the number of deviations is 5. What is the upper limit of the possible deviation rate, and what does it mean?a. 10.3%. The auditor is 95% confident that

Describe how auditors use sampling and GAS for gathering audit evidence.

Refer to Exhibit. Describe at least one auditing procedure for each financial statement assertion for sampling andGAS.

Refer to Exhibits.a. Define the following risks:● Risk of incorrect acceptance of internal control reliability● Risk of incorrect rejection of internal control reliability● Risk of incorrect acceptance of book value● Risk of incorrect rejection of book valueb. Explain which of these risks

Refer to Exhibit and compare and contrast statistical sampling and nonstatistical sampling on the following dimensions: sample size determination, sample selection, evaluation, costs, andbenefits.

Define the terms attributes sampling and attribute. Give an example of an attribute of interest to an auditor. Give an example of a control failure.

Define the term tolerable rate of deviation in formal terms (in other words, in the manner in which the AICPA’s 2012 Audit Sampling guide formally defines it) and in more practical terms.

Practice calculating the sample size and the number of expected errors in attributes sampling by using the tables in Exhibit and the following combinations ofinputs:

Using the tables in Exhibit, work backward to explain at least one set of assumptions that the auditor would have to make to justify the following samplesizes:

Define the following terms:(a) Simple random sampling,(b) Systematic sampling,(c) Systematic random sampling,(d) Haphazard sampling,(e) Block sampling.

Practice evaluating the results of attributes sampling by using the tables in Exhibit 8.6 and the following combinations of inputs.Assume the tolerable deviation rate is 12%. For each item labeleda. through f. below, state your interpretation of the result, including the appropriate conclusion

When evaluating an attributes sample, why is the focus on the upper limit of deviations in the sample? If the upper limit of deviation exceeds the tolerable deviation rate in attributes sampling, what alternative courses of action are available to the auditor?

Assume that you are using attribute sampling to test the controls over revenue recognition of the Packet Corporation, a public company, and will use the results as part of the evidence on which to base your opinion on its internal controls and to determine what additional auditing procedures should

Define the following terms:(a) Misstatement,(b) Factual misstatement,(c) Projected misstatement,(d) Tolerable misstatement,(e) Expected misstatement.

When using nonstatistical sampling as a test of an account balance, how does the auditor do the following?a. Determine the sample size.b. Select the sample.c. Evaluate the sample results.

The following information relates to a nonstatistical sample used for a price test of inventory:a. What is the best estimate of the total misstatement?b. Are these results acceptable, assuming tolerable misstatement is $25,000? Explain.c. If the results are not acceptable, what possible courses of

What are the strengths of MUS? Provide at least three examples in which MUS might be used.

Practice calculating the sample size in a MUS sample using Exhibit with the following combinations ofinputs.

Calculate the sampling interval for cases a. through h. in Problem, assuming a population size of $8,500,000. Recall that sampling interval = population size ÷ sample size. Round the value of the interval down to the nearest $1,000 or $10,000 to ensure that the sample size is

Assume you are planning the confirmation of accounts receivable. There are 2,000 customer accounts with a total book value of $5,643,200. Tolerable misstatement is set at $200,000, and expected misstatement is $40,000. The risk of incorrect acceptance is 30%. The ratio of expected to tolerable

Based on the information in Problem 8-56, assume that your sampling interval is $100,000.a. What is your statistical conclusion if no misstatements are found in the sample? Is the account balance acceptable? Explain.b. Calculate the total estimated misstatement assuming the following misstatements

Assume that you are auditing the inventory of Husky Manufacturing Company for the year ended December 31, 2013, and you are using MUS. The book value is $8,124,998.66. The risk of incorrect acceptance is 10% (90% confidence level). The tolerable misstatement is $275,000, and expected misstatement

Assume that the auditor is auditing accounts receivable for a long-time client. The auditor has assessed the risk of incorrect acceptance at 10%. The client's book value in accounts receivable is $8,425,000. Tolerable misstatement is $200,000, and expected misstatement is $40,000. Therefore, the

What courses of action should the auditor consider pursuing when the results of the MUS sample are unacceptable, in other words, when the total estimated misstatement exceeds the tolerable misstatement?

Respond to the ethical judgments required based on the following scenarios.Scenario 1. Assume you have collected a sample using MUS and that you have evaluated that sample to calculate a total estimated misstatement of $213,500. Prior to sampling, you set tolerable misstatement at $215,000. What is

The following are typical tasks performed by GAS. For each task, provide an example of how GAS could be used to accomplish that task.a. Analyze a fileb. Select transactions based on logical identifiersc. Select samplesd. Evaluate samplese. Print confirmationsf. Analyze overall file validityg.

List the advantages of using GAS.

Locate and read the article listed below and answer the following questions. Hall, T. W., J. E. Hunton, and B. J. Pierce. 2002. Sampling practices of auditors in public accounting, industry and government. Accounting Horizons 16 (2): 125–136.a. What is the issue being addressed in the paper?b.

Define the terms sampling units and population, and describe how these two concepts relate to each other.

What four critical questions must the auditor answer when sampling?

Distinguish between the terms sampling risk and nonsampling risk.

List the factors that the auditor should address when defining the population in attributes sampling.

What is the sampling unit when gathering evidence about misstatements in account balances and associated assertions? Provide examples of sampling units in the context of accounts receivable.

What is stratification? Distinguish between top-stratum items and lower-stratum items.

What are the difficulties that the auditor may experience in using MUS?

The sample size in a MUS sample is a function of what three factors?

TRUE-FALSE QUESTIONS1. Auditors should expect clients to have only one revenue process in place.2. The revenue cycle begins when the goods are shipped to a customer.3. An important inherent risk in the revenue cycle is that revenue will be recorded prior to when it has been earned.4. Determining

TRUE-FALSE QUESTIONS1. The auditor might believe a heightened risk of fraud exists if the preliminary analytical procedures indicate increases in revenue and net income, but negative cash flow from operations.2. When performing preliminary analytical procedures, the auditor could perform trend

MULTIPLE-CHOICE QUESTIONS1. Which of the following statements is true regarding assertions in the revenue cycle?a. It is typical that all five assertions for revenue are equally important.b. If a client has an incentive to overstate revenues, the existence assertion would be more relevant than the

MULTIPLE-CHOICE QUESTIONS1. Which of the following statements is false regarding preliminary analytical procedures in the revenue cycle?a. Since revenue is typically regarded as a high-risk account, preliminary analytical procedures related to revenue are not required.b. Auditors completing

Refer to Exhibit. Which accounts are typically affected by transactions in the revenue cycle? Identify the relationships among them.

For accounts receivable, what are the more relevant assertions? Why should an auditor identify which assertions are more relevant?

Refer to Exhibit 9.2. What are the major activities involved in generating and recording a sales transaction? What are the major documents generated as a part of each activity?Exhibit Overview of the SalesProcess

An important task in the audit of the revenue cycle is determining whether a client has appropriately recognized revenue.a. In assessing the risks associated with revenue recognition, the auditor of U.S. companies will likely consult criteria provided by the SEC. What general criteria has the SEC

What are some examples of sales transactions that involve product delivery that might have a high level of inherent risk?

Refer to Exhibit and to the Auditing in Practice features “Channel Stuffing at ArthroCare—The Importance of Professional Skepticism” and “The Importance of Professional Skepticism in Auditing Revenue at Tvia.” What methods have been used to fraudulently inflate revenue? How can auditors

What are a control risk assessment questionnaire and a controls matrix? How are these documents used by the auditor?

Why are monthly customer statement considered a control? Why is it important to separate the duties of responding to customer complaints from the accounts receivable and cash collection functions?

Refer to the Auditing in Practice feature "Risks Associated with Sales Returns: The Case of Medicis and Ernst & Young." What problems can occur if controls related to sales returns and allowances are not designed and operating effectively?

Identify preliminary analytical procedures that can help auditors identify areas of potential material misstatements in the revenue cycle.

Consider an audit client that manufactures fishing boats and sells them all over the country. Boats are sold to dealers who finance their purchases with their banks. The banks usually pay your client within two weeks of shipment. The company's profits have been increasing over the past several

Describe the differences in the planned audit approaches for Clients A and B and the reasons for such differences.

Read the following description of Drea Tech Company and identify the elements of inherent risk associated with the revenue cycle. Determine the appropriate audit response (audit procedure) to address the risks.Drea Tech Company has been growing rapidly and has recently engaged your firm as its

When assessing whether the controls are operating effectively, does the auditor need to reperform the control? For example, if personnel check the correctness of computations on an invoice and initial the bottom of a document to indicate that the control has been performed, does the auditor need to

The following is a list of controls (numbered 1 through 7 below) typically implemented in the revenue cycle.a. For each control identified, briefly indicate the financial misstatement that could occur if the control is not implemented effectively.b. Identify a test of control that the auditor can

Most accounting systems have the ability to generate exception reports that immediately identify control procedure failures or transactions that are out of the norm so that management can determine whether any special action is needed.a. Identify how the auditor might use each of the following four

Assume the auditor wishes to test controls over the shipment and recording of sales transactions. Identify the controls that the auditor would expect to find to achieve the objective that all transactions are recorded correctly, and in the correct time period. For each control identified indicate

Refer to the Auditing in Practice feature "Performing Appropriate Substantive Procedures in the Revenue Cycle: The Case of Kyoto Audit Corporation." What substantive procedures did Kyoto not perform appropriately? If such procedures are not performed appropriately, will the client's financial

a. What are typical substantive procedures in the revenue cycle, and how are these procedures related to management assertions?b. For the following procedures (numbered 1 through 6), indicate the assertion that is being tested.1. Take a block of shipping orders and account for the invoicing of all

What is an aged trial balance of accounts receivable? How does an auditor use it? How does an auditor determine that it is correctly aged?

Distinguish between the positive and negative forms of accounts receivable confirmations.Which confirmation type, positive or negative, is considered the more reliable? Why?

Identify potential fraud risk factors in the revenue cycle. What substantive audit procedures could be used to help determine if fraud has occurred in the revenue cycle?

Address the following questions about the confirmation of customers' accounts receivable.a. Why do confirmations not typically provide reliable evidence about the completeness assertion?b. What is a confirmation exception, and why is it important to investigate a confirmation exception?c. When

Read the following scenario about Strang Corporation and identify the substantive procedures that the CPA (Stanley) should perform to determine whether lapping exists. Do not discuss deficiencies in the system of internal control.During the year, Strang Corporation began to encounter cash flow

Your audit client, Madison, Inc., has a computerized accounts receivable system. There are two master files, a customer data file and an unpaid invoice file. The customer data file contains the customer's name, billing address, shipping address, identification number, phone number, purchase and

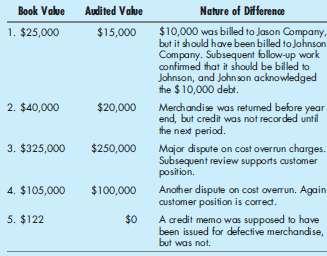

You have sent confirmations to 40 customers of Berg Shovick Express, a long-time audit client experiencing some financial difficulty. The company sells specialized high-technology goods. You have received confirmations from 32 of the 40 positive confirmations sent. A few minor errors were noted on

Refer to the Professional Judgment in Context feature "How to Account for Virtual Sales at Zynga." Answer the following questions:a. What are the inherent risks associated with the revenue transactions at Zynga?b. What are management's incentives to misstate revenue transactions?c. What controls

An Auditing in Practice feature presented in the chapter discussed the SEC's complaint against Benjamin Silva III, Tvia's vice president of worldwide sales. The complaint alleges a number of actions taken by Silva. For each of the following actions, indicate the accounting and/or auditing issue

Read the following case about MiniScribe and answer the following questions.a. How did MiniScribe inflate its financial statements?b. What are some of the factors that led to the inflated financial statements?c. What red flags should have raised the auditor’s suspicions about phony sales and

Showing 2100 - 2200

of 10291

First

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

Last

Step by Step Answers

.png)

.png)

.png)

-1.png)

-2.png)

-3.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

-1.png)

-2.png)

.png)

.png)

.png)

.png)