New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing

Auditing and Assurance Services A Systematic Approach 9th edition William Messier, Steven Glover, Douglas Prawitt - Solutions

Distinguish between factual, judgmental, and projected misstatements.

Distinguish between errors and fraud. Give three examples of each.

What steps should an auditor perform to identify the risk of material misstatement due to fraud?

Why would a company institute a control policy that required mandatory vacations?

Marv Jackal, CPA, determines that a number of risks of material misstatement are pervasive to the overall Financial statements. How should Jackal respond to such pervasive risks?

Multiple Choice1. Which of the following concepts are pervasive in the application of generally accepted auditing standards, particularly the standards of field work and reporting?a. Internal control.b. Expected misstatement.c. Control risk.d. Materiality and audit risk.2. The existence of audit

The auditor should consider audit risk when planning and performing an examination of financial statements in accordance with generally accepted auditing standards. Audit risk should also be considered together in deter-mining the nature, timing, and extent of auditing procedures and in evaluating

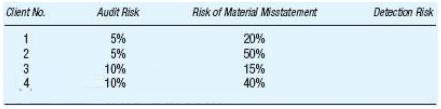

The CPA firm of Lumley & Lu uses a quantitative approach to implementing the audit risk model. Calculate detection risk for each of the following hypo thetical clients.

The CPA firm of Quigley & Associates uses a qualitative approach to implementing the audit risk model. Audit risk is categorized using two terms: very low and low. The risk of material misstatement and detection risk are categorized using three terms: low, moderate, and high. Calculate detection

You are considering acceptable audit risk at the financial statement level. For each of the following independent scenarios, based only on the information provided, indicate the effect on acceptable audit risk compared to a typical private company audit.a. LVD is a pharmaceutical company that has

When planning a financial statement audit, a CPA must understand audit risk and its components. The firm of Pack & Peck evaluates the risk of material misstatement (RMM) by disaggregating RMM into its two components: inherent risk and control risk.Required:For each illustration, select the

For each of the following situations, explain how risk of material misstatement should be assessed and what effect that assessment will have on detection risk.a. Johnson, Inc., is a fast- growing trucking company operating in the south-eastern part of the United States. The company is publicly

Management fraud (e. g., fraudulent financial reporting) is a relatively rare event. However, when it does occur, the frauds (e. g., Enron and WorldCom) can have a significant effect on shareholders, employees, and other parties. AU 240, Consideration of Fraud in a Financial Statement Audit,

In developing an understanding of the entity and its environment, the auditor can obtain information from numerous sources, such as knowledge from prior audits and discussions with management. List five additional potential sources (internal or external) of information about the entity and its

Industry conditions can be a source of business risks for an entity. Describe how each of the following industry conditions can result in business risks.a. The entity’s market characteristics (e. g., demand, capacity, etc.) and competition.b. The cyclical or seasonal activity in the entity’s

Assume that your firm is considering accepting NewSkin Pharma as a new audit client. NewSkin is a start- up biotech firm that has publicly traded stock on NASDAQ. Your audit partner has asked you to perform some prelim nary work for the firm’s client acceptance process.Required:a. Prepare a list

CarProof is a public company founded in 2002 to manufacture and sell specialty auto products mainly relating to paint protec-tion and rustproofing. By 2011, the CarProof board of directors felt that the company’s products had fully matured and that it needed to diversify. Car- Proof aggressively

Auditors are required to obtain and support an understanding of the entity and its environment in order to identify business risks. Much of the information needed to identify the risks can be obtained from the company’s annual report, 10K, and proxy materials. Many companies publish these

Explain why the auditor divides the financial statements into components or segments in order to test management’s assertions.

How do management assertions relate to the financial statements?

List and define the assertions about classes of transactions and events for the period under audit.

List and define the assertions about account balances at the period end.

Define audit evidence. Provide an example of evidence from accounting records and other information.

Explain why in most instances audit evidence is persuasive rather than convincing.

List and define the audit procedures for obtaining audit evidence.

In a situation that uses inspection of records and documents as a type of evidence, distinguish between vouching and tracing in terms of the direction of testing and the assertions being tested.

Why is it necessary to obtain corroborating evidence for inquiry and for observation?

Discuss the relative reliability of the different types of audit procedures.

Why does the “audit testing hierarchy” begin with tests of controls and substantive analytical procedures?

Consider the “assurance bucket” analogy. Why are some of the buckets larger than others for particular assertions or accounts?

Why are indexing and cross- referencing important to the documentation of audit working papers?

When discussing the use of analytical procedures, what is meant by the “precision of the expectation”? In applying this notion to an analytical procedure, how might an auditor calculate a tolerable difference?

Significant differences between the auditor’s expectation and the entity’s book value require explanation through quantification, corroboration, and evaluation. Explain each of these terms.

List and discuss the four categories of financial ratios that are presented in the chapter.

Multiple Choice1. Which of the following procedures would an auditor most likely rely on to verify management’s assertion of completeness? a. Reviewing standard bank confirmations for indications of cash manipulations. b. Comparing a sample of shipping documents to related sales invoices. c.

Management makes assertions about components of the financial statements. Match the management assertions shown in the left- hand column with the proper description of the assertion shown in the right- hand column.Management Assertion Description a. Existence or occurrence 1. The

Management assertions about classes of transactions area. Occurrence. b. Completeness. c. Authorization. d. Accuracy. e. Cutoff. f. Classification. For each management assertion, indicate an example of a misstatement that could occur for revenue transactions.

For each of the following specific audit procedures, indicate the type of audit procedure it represents: (1) Inspection of records or documents, (2) Inspection of tangible assets, (3) Observation, (4) Inquiry, (5) Confirmation, (6) Recalculation, (7) Re-performance, (8) Analytical procedures, and

For each of the audit procedures listed in Problem 5- 32, identify the category (assertions about classes of transactions and events or assertions about account balances) and the primary assertion being tested.In Problem 5- 32(1) Inspection of records or documents,(2) Inspection of tangible

Evidence comes in various types and has different degrees of reliability. Following are some statements that compare various types of evidence. a. A bank confirmation versus observation of the segregation of duties between cash receipts and recording payment in the accounts receivable subsidiary

Inspection of records and documents relates to the auditor’s examination of entity accounting records and other information. One issue that affects the reliability of documentary evidence is whether the documents are internal or external. Following are examples of documentary evidence:1.

The confirmation process is defined as the process of obtaining and evaluating a direct communication from a third party in response to a request for information about a particular item affecting financial statement assertions.Required:a. List the factors that affect the reliability of

Audit documentation is the auditor’s record of work performed and conclusions reached on an audit engagement.Required:a. What are the functions of audit documentation?b. List and describe the various types of audit documents.c. What factors affect the auditor’s judgment about the form, content,

At December 31, 2013, EarthWear has $ 5,890,000 in a liability account labeled “Reserve for returns.†The footnotes to the financial statements contain the following policy: “At the time of sale, the company provides a reserve equal to the gross profit on projected merchandise

Arthur, CPA, is auditing The Home Improvement Store as of December 31, 2014. As with all audit engagements, Arthur’s initial procedures are to analyze the entity’s financial data by reviewing trends in significant ratios and comparing the company’s performance with the industry

Part I. Lernout & Hauspie (L& H) was the world’s leading provider of speech and language technology products, solutions, and services to businesses and individuals worldwide. Both Microsoft and Intel invested millions in L& H. However, accounting scandals and fraud allegations sent

The auditors for Weston University are conducting their audit for the fiscal year ended December 31, 2013. Specifically, the audit firm is now focusing on the audit of revenue from this season’s home football games. While planning the audit of sales of football tickets, one of their newer staff

Bentley Bros. Book Company publishes more than 250 fiction and nonfiction titles. Most of the company’s books are written by southern authors and typically focus on subjects popular in the region. The company sells most of its books to major retail stores such as Waldenbooks and B. Dalton. Your

Use an Internet browser to search for the following terms: • Electronic data interchange (EDI). • Image-processing systems. Prepare a memo describing EDI and image- processing systems. Discuss the implications of each for the auditor’s consideration of audit evidence.

What are management’s incentives for establishing and maintaining strong internal control? What are the auditor’s main concerns with internal control?

What are the potential benefits and risks to an entity’s internal control from information technology?

Describe the five components of internal control.

What are the factors that affect the control environment?

What are the major differences between a substantive strategy and a reliance strategy when the auditor considers internal control in planning an audit?

Why must the auditor obtain an understanding of internal control?

What is meant by the concept of reasonable assurance in terms of internal control? What are the inherent limitations of internal control?

List the tools that can document the understanding of internal control.

What are the requirements under auditing standards for documenting the assessed level of control risk?

What factors should the auditor consider when substantive procedures are to be completed at an interim date? If the auditor conducts substantive procedures at an interim date, what audit procedures would normally be completed for the remaining period?

What is the auditor’s responsibility for communicating control deficiencies that are severe enough to be considered significant deficiencies or material weaknesses?

Multiple Choice 1. An auditor’s primary consideration regarding an entity’s internal controls is whether they a. Prevent management override. b. Relate to the control environment. c. Reflect management’s philosophy and operating style. d. Affect the financial statement assertions. 2. Which

An auditor is required to obtain sufficient understanding of each component of an entity’s internal control system to plan the audit of the entity’s financial statements and to assess control risk for the assertions embodied in the account balance, transaction class, and disclosure components

Johnson, CPA, has been engaged to audit the financial statements of Rose, Inc., a publicly held retailing company. Before assessing control risk, Johnson is required to obtain an understanding of Rose’s control environment.Required:a. Identify additional control environment factors (excluding the

Assume that you are an audit senior in charge of planning the audit of an entity that your firm has audited for the previous four years. During the audit planning meeting with the manager and partner in charge of the engagement, the partner noted that the entity recently adopted an IT- based

Auditors use various tools to document their understanding of an entity’s internal control system, including narrative descriptions, internal control questionnaires, and flowcharts. Required: a. Identify the relative strengths of each tool. b. Briefly describe how the complexity of an entity’s

The Audit Committee of a small manufacturing company that sells its products globally has directed internal audit to perform specific annual reviews to monitor manual journal entries, with a particular focus on potential management override activities. Internal audit’s review includes basic

Cook, CPA, has been engaged to audit the financial statements of General Department Stores, Inc., a continuing audit entity, which is a chain of medium- sized retail stores. General’s fiscal year will end on June 30, 2013, and General’s management has asked Cook to issue the auditor’s report

Ken Smith, the partner in charge of the audit of Houghton Enterprises, identified the following significant deficiencies during the audit of the December 31, 2013, financial statements:1. Controls for granting credit to new customers were not adequate. In particular, the credit department did not

Preview Company, a diversified manufacturer, has five divisions that operate throughout the United States and Mexico. Preview has historically allowed its divisions to operate autonomously. Corporate intervention occurred only when planned results were not obtained. Corporate management has high

Briefly summarize management’s and the auditor’s basic responsibilities under Section 404 of the Sarbanes- Oxley Act of 2002.

Discuss how the terms likelihood and magnitude play a role in evaluating the significance of a control deficiency.

The first element in management’s process for assessing the effectiveness of internal control is determining which controls should be tested. Identify the controls that would typically be tested by management.

Describe how management and the auditor decide on which locations or business units to test.

Management must document its assessment of internal control. What would such documentation include?

List the steps in the auditor’s process for an audit of ICFR.

How does the auditor evaluate the objectivity and competence of others who perform work for management?

Describe the steps in obtaining an understanding of ICFR using a top- down, risk- based approach.

The period- end financial reporting process controls are always important. What are those controls, and what should the auditor’s evaluation of those controls include?

A walkthrough involves tracing a transaction through the information system. What types of evidence does a walkthrough provide to the auditor?

AS5 indicates that certain circumstances are indicators of a material weakness. What are these circumstances, and why do you think the PCAOB assessed them as being of such importance?

Describe what is meant when management remediates a material weakness. If a material weakness is remediated and sufficiently tested before the “as of” date, what can management assert about ICFR?

What are the auditor’s documentation requirements for an audit of ICFR?

What are the types of reports that an auditor can issue for an audit of ICFR? Briefly identify the circumstances justifying each type of report.

Under what circumstances would an auditor give an adverse opinion on the effectiveness of an entity’s ICFR?

Under what circumstances would an auditor disclaim an opinion on the effectiveness of an entity’s ICFR?

What should the auditor do when a significant period of time has elapsed between the service organization auditor’s report and the date of management’s assessment?

Distinguish between generalized and custom audit software. List the functions that can be performed by generalized audit software.

Multiple- Choice1. The Sarbanes- Oxley Act of 2002 requires management to include a report on the effectiveness of ICFR in the entity’s annual report. It also requires auditors to report on the effectiveness of ICFR. Which of the following statements concerning these requirements is false? a. The

Following are three examples of controls for accounts that you have deter-mined are significant for the audit of ICFR. For each control, determine the nature, timing, and extent of testing of the design and operating effectiveness. Refer to Exhibit 7– 3 for a way to format your answer.Control 1.

Following are examples of control deficiencies that may represent significant deficiencies or material weaknesses. For each control deficiency, indicate whether it is a significant deficiency or material weakness. Justify your decision. a. The entity uses a standard sales contract for most

Following are examples of control deficiencies that may represent significant deficiencies or material weaknesses. For each of the following scenarios, indicate whether the deficiency is a significant deficiency or material weakness. Justify your decision. a. During its assessment of ICFR, the

For each of the following cases, indicate why management and the auditors determined that the control deficiency was a material weakness.Case 1: In our assessment of the effectiveness of internal control over financial reporting as of December 31, 2013, we identified a material weakness over the

For each of the following independent situations, indicate the type of report on ICFR you would issue. Justify your report choice. a. Hansen, Inc., has restated previously issued financial statements to reflect the correction of a misstatement. b. Shu & Han Engineering does not have effective

For each of the following independent situations relating to the audit of ICFR, indicate the reason for and the type of audit report you would issue. a. During the audit of Wood Pharmaceuticals, you are surprised to find several control deficiencies in the entity’s internal control. You

For each of the following independent situations, indicate the type of report on ICFR you would issue. Justify your report choice. a. The management’s report on ICFR issued by Graham Granary, Inc., includes disclosures about corrective actions taken by the entity after the date of management’s

Assume that scenario (a) in Problem 7- 36 is a material weakness. Prepare a draft of the auditor’s report for an audit of ICFR. Assume that Lorenz’s auditor is issuing a separate report on internal control.

Assume that scenario (b) in Problem 7- 36 is a material weakness. Prepare a draft of the auditor’s report for an audit of ICFR. Assume that First Coast’s auditor is issuing a combined report for the financial statement audit and audit of internal control.

The following audit report was drafted by a junior staff accountant of Lipske & Griffin, CPAs, at the completion of the audit of Douglas Company’s ICFR. The report was submitted to the engagement partner, who reviewed matters thoroughly and properly concluded that there was a material

Auditors use various audit techniques to gather evidence when an entity’s accounting information is processed using IT. Select the audit procedure from the following list and enter it in the appropriate place on the grid.Audit procedure: 1. Test data method.2. Custom audit software.3.

Brown, CPA, is auditing the financial statements of Big Z Wholesaling, Inc., a continuing audit client, for the year ended January 31, 2013. On January 5, 2013, Brown observed the tagging and counting of Big Z’s physical inventory and made appropriate test counts. These test counts have been

Showing 2600 - 2700

of 10291

First

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

Last

Step by Step Answers

.png)

.png)

.png)

.png)