New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing

Principles of Auditing and Other Assurance Services 19th edition Ray Whittington, Kurt Pany - Solutions

Describe the audit implications of the Check Clearing for the 21st Century Act.

During your audit of a small manufacturing firm, you find numerous checks for large amounts drawn payable to the treasurer and charged to the Miscellaneous Expense account. Does this require any action by the auditor? Explain.

Prepare an example of lapping of cash receipts, showing actual transactions and the cash receipts journal entries.

During your reconciliation of bank accounts in an audit, you find that a number of checks for small amounts have been outstanding for more than a year. Does this situation call for any action by the auditor? Explain.

What action should be taken by the auditors when the count of cash on hand discloses a shortage?

Explain the objectives of each of the following audit procedures for cash:a. Obtain a cutoff bank statement subsequent to the balance sheet date.b. Compare paid checks returned with the bank statement to the list of outstanding checks in the previous reconciliation.c. Trace all bank transfers

Explain two procedures by which auditors may verify the client’s cutoff of cash receipts.

What is the meaning of the term window dressing when used in connection with year-end financial statements? How might the term be related to the making of loans by a corporation to one or more of its executives?

An audit client that has never before invested in securities recently acquired more than a million dollars in cash from the sale of real estate no longer used in operations. The president intends to invest this money in marketable securities until such time as the opportunity arises for

Salvador Corporation made an investment in Letter.com, Inc., in exchange for 100,000 options to purchase Letter.com’s stock at $20 per share. Since the stock options are not marketable, Salvador’s management has this derivative valued by a security appraiser. The appraiser uses an

In what ways can the audit of financial investments present special risks requiring specialized skill and knowledge?

If a security or derivative is not marketable, how do the auditors typically obtain evidence about the fair value of the instrument?

Fluid Controls, Inc., a manufacturing company, has retained you to perform an audit for the year ended December 31. Prior to the year-end, you begin to obtain an understanding of the new client’s controls over business processes related to the cash account.You find that nearly all the company’s

Henry Mills is responsible for preparing checks, recording cash disbursements, and preparing bank reconciliations for Signet Corporation. While reconciling the October bank statement, Mills noticed that several checks totaling $937 had been outstanding for more than one year.Concluding that these

During the first few months of the year, John Smith, the cashier in a small company, was engaged in lapping operations. However, he was able to restore the amount of cash “borrowed” by March 31, and he refrained from any fraudulent acts after that date. Will the year-end audit probably lead to

An assistant auditor received the following instructions from her supervisor: “Here is a cutoff bank statement covering the first seven business days of January. Compare the paid checks returned with the statement and dated December 31 or earlier with the list of checks outstanding at December

“When auditors are verifying a client’s bank reconciliation, they are particularly concerned with the possibility that the list of outstanding checks may include a nonexistent or fictitious check, and they also are concerned with the possibility of omission from the reconciliation of a deposit

In the audit of a client with a fiscal year ending December 31, the CPAs obtain a January 10 bank statement directly from the bank. Explain how this cutoff bank statement will be used:a. In the review of the December 31 bank reconciliation.b. To obtain other audit information.

In the audit of Wheat, Inc., for the year ended December 31, you discover that the client had been drawing checks as creditors’ invoices became due but had not been mailing the checks immediately. Because of a working capital shortage, some checks have been held for two or three weeks.The

Explain how each of the following items would appear in a four-column proof of cash for the month of November. Assume the format of the proof of cash begins with bank balances and ends with the unadjusted balances per the accounting records.a. Outstanding checks at November 30.b.

During the current year, the management of Hanover, Inc., entered into a futures contract to hedge the price of silver that will be needed for next year’s production. The contract, which is held by Hanover’s commodity broker, is marketable and exchanged on the CME Globex Exchange.a. Describe

During your audit of Miles Company, you prepared the following bank transfer schedule:a. Describe the purpose of a bank transfer schedule.b. Identify those transfers that should be investigated and explain thereason.

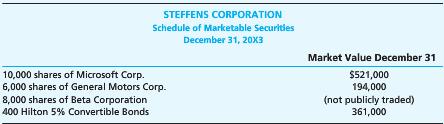

You are the auditor in charge of the audit of Steffens Corporation. In the audit of investments, you have just been given the following list of securities held by Steffens Corporation at December 31, 20X3.a. Identify the potential audit problems that may be indicated by the schedule.b. To value the

Multiple Choice QuestionsSelect the best answer for each of the following situations and give reasons for your choice.a. Which of the following controls would most likely reduce the risk of diversion of customer receipts by a client’s employees?(1) A bank lockbox system.(2) Prenumbered remittance

You are working on your firm’s fifth audit of SSC. The previous audits have all resulted in standard unqualified audit reports. Read the following write-up from your audit files concerning SSC and its industry, and then reply to the questions that follow.Company InformationIn 20X1, Gary Sherwood

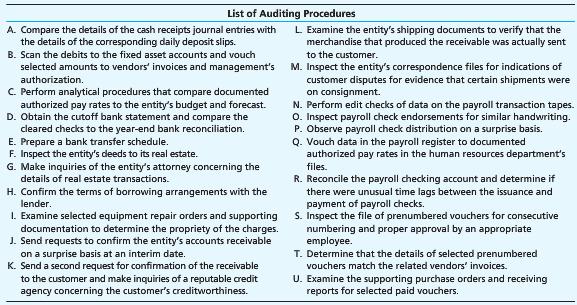

Items a through l represent possible errors and fraud that you suspect may be present at Rex Company. The accompanying List of Auditing Procedures represents procedures that the auditor would consider performing to gather evidence concerning possible errors and fraud. For each item, select one or

Items 1 through 6 represent the items that an auditor ordinarily would find on a client-prepared bank reconciliation. The accompanying List of Auditing Procedures represents substantive auditing procedures. For each item, select one or more procedures, as indicated, that the auditor most likely

For each substantive procedure below, identify its primary objective or indicate that the procedure serves no purpose.Substantive Procedures:a. Prepare a bank transfer schedule.b. Prepare a four-column proof of cash.c. Use a standard confirmation form to confirm account balance information.d.

During your audit of Carla Pang Inc. you prepared the following bank transfer schedule.Fill out the table below indicating the most likely situation as it relates to cash at year-end.Indicate the situation using one of the following:1. Year-end total cash is properly stated.2. Year-end total cash

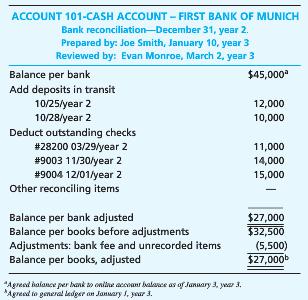

The auditor of Cubs obtained the following client-prepared bank reconciliation:The auditor for Cubs Co. has obtained the client-prepared bank reconciliation.The following information is available:• Evan Monroe was promoted to controller on December 15, year 2; his former position was assistant

Following are typical questions that might appear on an internal control questionnaire for investments in marketable securities.1. Is custody of investment securities maintained by an employee who does not maintain the detailed records of the securities?2. Are securities registered in the company

You are the senior auditor-in-charge of the July 31, 20X0, audit of Reliable Auto Parts, Inc. Your newly hired staff assistant reports to you that she is unable to complete the four-column proof of cash for the month of April 20X0, which you instructed her to do as part of the consideration of

During the audit of Sunset Building Supply, you are given the following year-end bank reconciliation prepared by the client:SUNSET BUILDING SUPPLYBank ReconciliationDecember 31Balance per 12/31 bank statement ...... $48,734Add: Deposits in transit ........... 4,467

In your audit of Ginko Company, you have received a cash confirmation and a cutoff statement from the bank on Ginko’s one bank account. Prepare an audit program of substantive procedures for Ginko’s cash.

Listed below are eight interbank cash transfers for Steven Smith Co., indicated by the letters a through h, for late December 20X1 and early January 20X2.For each of the transfers a through h, (1) indicate whether cash is understated, overstated, or correct as a result of the transfer; and (2)

An improper cutoff of transactions around year-end occurs when journal entries are recorded in the wrong year. In this case, you are to determine the effects of various cutoff misstatements relating to recording cash receipts received on accounts receivable and the recording of credit sales. To

On October 21, Rand & Brink, a CPA firm, was retained by Suncraft Appliance Corporation to perform an audit for the year ended December 31. A month later, James Minor, president of the corporation, invited the CPA firm’s partners, George Rand and Alice Brink, to attend a meeting of all

Today you had lunch with your friend Sarah Teasdale. Sarah has worked with Zaird & Associates, CPAs, for about two years. You’ve been with Zaird for only nine months. You discussed with her your difficulties in getting jobs done in the budgeted number of hours. Sarah said, “Yeah, that’s a

Describe circumstances that might cause the auditors to identify understatement of assets as a significant audit risk.

It is sometimes said that audit work on cash is facilitated by the existence of two independent records of the client’s cash transactions, which are available for comparison by the auditors. Identify these two independent records.

Explain how a lockbox system contributes to internal control over cash receipts.

The auditors’ work on cash may include preparing a description of controls and performing tests of controls. Which of these two steps should be performed first? What is the purpose of tests of controls?

A well-financed audit client of your CPA firm invests large amounts in marketable securities. As part of its internal control, the company uses a monthly report of securities transactions. The report is prepared by the controller and presented to the investment committee of the board of directors.

What information should be noted by the auditors during their inspection of securities on hand?

A summary of the controls for the revenue and cash receipts cycle of Keystone Computers & Networks, Inc., appears on pages 479–492.a. For the following three controls over sales, indicate one type of error or fraud that the control serves to prevent or detect. Organize your solution as

As indicated on the control risk assessment working paper on page 490, the auditors identified two weaknesses in internal control over the revenue cycle of KCN. Describe the implications of each of the two weaknesses in terms of the type of errors or fraud that could result.

As indicated on the working paper on page 490, the auditors decided to apply audit sampling to three controls for the revenue and cash receipts cycle.a. Describe the characteristic that a control must possess in order to be tested with audit sampling.b. Assume that the auditors decided to use audit

In Part III (Appendix 11B) of the audit case, the audit staff of Adams, Barnes & Co. identified specific revenue risks on working paper RA-12 (page 494). However, the “Summary of Audit Approach” section is incomplete (in process) for risks 2 and 3.Review the audit program (working paper

Assume that you have been assigned to the audit of Keystone after audit planning has occurred. Review the planning information on pages 235–242 and the audit program for the accounts receivable and revenue (B-6 on pages 495–496). The manager on the engagement has given you the task of

Keystone Computers & Networks, Inc. (KCN), has 933 accounts receivable, with a total book value of $10,235,457. From that population, Adams, Barnes & Co. (ABC), CPAs, selected a sample of 260 accounts (142 unique accounts) for confirmation for the year ended December 31, 20X5, as

Explain why the audit of revenue and receivables may present the auditors with significant audit risk.

The controller of a new client operating a medium-size manufacturing business complains to you that he believes the company has sustained significant losses on several occasions because certain sales invoices were misplaced and never recorded as accounts receivable. What control can you suggest to

The accounts receivable section of the accounting department in Wind Power, Inc., maintains subsidiary ledgers that are posted from copies of the sales invoices transmitted daily from the billing department. How may the accounts receivable section be sure that it receives promptly a copy of each

Among specific procedures that contribute to good internal control over the business processes related to accounts receivable are (a) the approval of uncollectible account write-offs and credit memoranda by an executive and (b) the sending of monthly statements to all customers.State three other

Your review of notes receivable from officers, directors, stockholders, and affiliated companies discloses that several notes of small amounts were written off to the allowance for uncollectible notes during the year. Have these transactions any special significance? Explain.

State briefly the audit objectives that are addressed by the following audit procedure: “Confirm accounts receivable and notes receivable by direct communication with debtors.”

Several accounts receivable confirmations have been returned with the notation, “Verification of vendors’ statements are no longer possible because of our data processing system.” What alternative auditing procedures could be used to verify these accounts receivable?

What alternative auditing procedures may be undertaken in connection with the confirmation of accounts receivable where customers having substantial balances fail to reply after second request forms have been mailed directly to them?

A CPA firm wishes to test the client’s sales cutoff at June 30, 20X0. Describe the steps that the auditors should include in this test.

In your first audit of Hydro Manufacturing Company, a manufacturer of outboard motors, you discover that an unusually large number of sales transactions were recorded just before the end of the fiscal year. What significance would you attach to this unusual volume?

In connection with an audit, what are the purposes of a review of sales returns and allowances subsequent to the balance sheet date?

Cite various procedures auditors employ that might lead to the detection of an inadequate allowance for doubtful accounts receivable.

You have been assigned to the audit of Processing Solutions, Inc., a privately held corporation that develops and sells computer systems. The systems are sold under one- to five-year contracts that provide for a fixed price for licensing, delivery, and setup of the systems and maintenance and

Listed below are audit situations that may affect the audit of receivables and revenue.a. The audit of a machinery manufacturing company that engages in bill and hold transactions.b. The audit of a software company that engages in multiple element agreements that involve a fixed fee for software,

In their work on accounts receivable and elsewhere in an audit, the independent auditors often make use of confirmation requests.a. What is an audit confirmation request?b. What characteristics should an audit confirmation response possess if a CPA firm is to consider it to be valid evidence?c.

During the audit of Solar Technologies, Inc., the auditors sent confirmation requests to customers whose accounts had been written off as uncollectible during the year under audit. An executive of Solar protested, saying, “You people should be verifying that the receivables on the books are

Walter Conn, CPA, is engaged to audit the financial statements of Bingo Wholesaling for the year ended December 31, 20X0. Conn obtained and documented an understanding of the client and its environment, including internal control over the business processes relating to accounts receivable. He

An assistant auditor was instructed to “test the aging of accounts receivable as shown on the trial balance prepared by the client.” In making this test, the assistant traced all past-due accounts shown on the trial balance to the ledger cards in the accounts receivable subsidiary ledger and

Hale Nelson, CPA, is engaged to audit the financial statements of Hollis Manufacturing, Inc. Hollis engages in very complex sales agreements that create issues with respect to revenue recognition. As a result, Nelson has identified revenue recognition as an audit area of significant risk that

Multiple Choice QuestionsSelect the best answer for each of the following and explain fully the reason for your selection.a. Which of the following is least likely to be considered an inherent risk relating to receivables and revenues?(1) Restrictions placed on sales by laws and regulations.(2)

For each of the procedures described in the table below, identify the audit procedure performed and classification of the audit procedure using the following:Audit Procedures:(1) Analytical procedure(2) Confirmation(3) Inquiry(4) Inspection of records or documents(5) Inspection of tangible

You are involved with the audit of Jelco Company for year 1 and have been asked to consider the confirmation reply results indicated below. For each confirmation reply as to the proper action to be taken from the following possible actions:(1) Exception; propose an adjustment.(2) Send a second

An assistant on the Carter Company audit has been working in the revenue cycle and has compiled a list of possible errors and fraud that may result in the misstatement of Carter Company’s financial statements and a corresponding list of controls that, if properly designed and implemented, could

The auditors have determined that each of the following objectives will be part of the audit of SSC Corporation. For each audit objective, select a substantive procedure (see the list below) that would help to achieve that objective. Each of the procedures may be used once, more than once, or not

Halston Toy Manufacturing Co. introduced a number of new products in the last quarter of the year. The company has a liberal return policy allowing retail customers to return products within 120 days of purchase.a. Describe the audit problem indicated by this scenario.b. List audit procedures that

The following are typical questions that might appear on an internal control questionnaire for accounts receivable:1. Are sales invoices checked for proper pricing, terms, and clerical accuracy?2. Are shipping documents prenumbered and all numbers accounted for?3. Is customer credit approval

During your examination of the financial statements of Martin Mfg. Co., a new client, for the year ended March 31, 20X0, you note the following entry in the general journal dated March 31, 20X0:Your review of the contract for sale between Martin and Ardmore, your inquiries of Martin executives,

You are conducting an annual audit of Granite Corporation, which has total assets of approximately $1 million and operates a wholesale merchandising business. The corporation is in good financial condition and maintains an adequate accounting system. Granite Corporation owns about 25 percent of the

The July 31, 20X0, general ledger trial balance of Aerospace Contractors, Inc., reflects the following accounts associated with receivables. Balances of the accounts are after all adjusting journal entries proposed by the auditors and accepted by the client.Accounts receivable—commercial

Ming, CPA, is engaged to audit the financial statements of Wellington Sales, Inc., for the year ended December 31, 20X0. Ming obtained and documented an understanding of the client’s business and environment, including internal control over business processes relating to accounts receivable.

You are an assistant auditor with Zaird & Associates, CPAs. Universal Air (UA), your fifth audit client in your eight months with Zaird, is a national airline based in your hometown. UA has continued to grow while remaining healthy financially over the eight years of its existence. Indeed, as you

You have worked with Zaird & Associates, CPAs, for a little more than a year and are beginning your second audit of Universal Air (UA). This year you even have an assistant reporting to you—Jane McClain.Jane has come to you with a concern. She noticed that when sales are “booked” over the

Explain the difference between a customer’s order and a sales order, as these terms might be used by a manufacturing company making sales on credit.

State briefly the objective of the billing process. What important document is created by the billing department?

Criticize the following quotation: “A credit memorandum should be issued only when an account receivable is determined to be uncollectible.”

In the audit of an automobile agency, you find that installment notes received from the purchasers of automobiles are promptly discounted with a bank. Would you consider it necessary to confirm these notes by a communication with the bank? With the makers? Explain.

The confirmation of accounts receivable is an important auditing procedure. Should the formal request for confirmation be made by the client or by the auditors? Should the return envelope be addressed to the client, to the auditors in care of the client, or to the auditors’ office?Explain.

In selecting accounts receivable for confirmation, the auditors discover that the client company’s records show the addresses of many individual customers to be post office boxes. What should be the auditors’ reaction to this situation?

In the examination of credit memoranda covering allowances to customers for goods returned, how can the auditors ascertain whether the customer actually did return merchandise in each case in which accounts receivable were reduced?

Give an example of a type of receivable originating without arm’s-length bargaining. Comment on the presentation of such receivables in the balance sheet.

Describe a retrospective review of an accounting estimate. With respect to the audit of revenue, what is the purpose of performing this review?

During preliminary conversations with a new staff assistant, you instruct her to send out confirmation requests for both accounts receivable and notes receivable. She asks whether the confirmation requests should go to the makers of the notes or to the holders of the notes, in the case of notes

Lakeside Company has retained you to conduct an audit so that it will be able to support its application for a bank loan with audited financial statements. The president of Lakeside states that you will have unlimited access to all records of the company and may carry out any audit procedures you

You have been assigned to the audit of Utopia Industries, Inc., for the year ended December 31, 20X1. The company makes components for communications and defense applications. To obtain an understanding of the methods of revenue recognition used by such businesses and the risks involved, you decide

An auditor’s working papers include the following narrative description of the cash receipts and billing portions of Southwest Medical Center’s internal control. Evaluate each condition following the narrative as being either (1) a strength, (2) a deficiency, (3) not a strength or a deficiency.

An auditor may use confirmations of accounts receivable. Reply as to whether the following statements are correct or incorrect with respect to the confirmation process when applied to accounts receivable.a. The confirmation requests should be mailed to respondents by the CPAs.b. A combination of

Many auditors consider the substantiation of the figure for inventory to be a more difficult and challenging task than the verification of most other items on the balance sheet. List several specific factors that support this view.

What segregation of duties would you recommend to attain maximum internal control over purchasing activities in a manufacturing concern?

Do you believe that the normal review of purchase transactions by the auditors should include examination of receiving reports? Explain.

The client’s cost accounting system is often an important part of the CPAs’ audit of the financial statements of a manufacturing company. For what purposes do the auditors consider the cost accounting system?

Showing 3900 - 4000

of 10291

First

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

Last

Step by Step Answers

.png)

.png)

.png)

.png)

.png)

-1.png)

-2.png)

.png)

.png)