New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing

Auditing A Business Risk Approach 8th edition Karla Johnstone, Audrey Gramling, Larry Rittenberg - Solutions

1. The auditor is auditing sales and accounts receivable and notes the following: (a) The company regularly does not follow its credit policies; rather it routinely overrides the credit policy when divisional management needs to meet its performance goals; and (b) The sales manager has the

Following is a portion of management's report on internal control by Milacron Inc. in 2004. Item 9A. Controls and Procedures Disclosure Controls and Procedures (Interim Analysis) Disclosure controls and procedures are controls and other procedures that are designed to ensure that information

The PCAOB allows the auditor to use the work of others, such as internal auditors or other company personnel, to alter the nature, timing, or extent of the auditor's own testing of internal controls. Client A has an internal audit department that reports to the CFO and audit committee. The

The introduction to this chapter contained the following quotes from an IMA paper:The requirement to report on internal control resulted from one particular type of internal control breakdown: senior management of some major public companies overrode their control systems and issued misleading

Assume that the auditor's tests of internal controls did not reveal any material weaknesses in controls. However, during the audit, a material misstatement in an important account was found. Does the auditor have to analyze the cause of the misstatement and report a material weakness in internal

Describe the major elements of PCAOB Auditing Standard No. 5 and how it has affected practice.

Review the external auditor's report on the integrated audit of Ford Motor Co. contained in the chapter material. What are the important elements in that report related to internal control?

Hermanson, D., & Ye, Z. (2009). Why Do Some Accelerated Filers with SOX Section 404 Material Weaknesses Provide Early Warning under Section 302? Auditing: A Journal of Practice & Theory 28(2): 247-271. 1. What is the issue being addressed in the paper? 2. Why is this issue important to practicing

In the overview of audit procedures, five different activities are identified in the evidence gathering and evaluation process. What are those activities and why is it important that each is considered and integrated into an overall assessment of audit evidence?

For audits under the jurisdiction of the PCAOB, auditors must document significant findings or issues and actions taken to address them. One of the significant findings that auditors are required to document and address are audit adjustments. What are audit adjustments? Why might the PCAOB care if

What are the purposes of an audit program? What are the major issues that should be addressed in an audit program?

Consider the "Earnings Management" example for Ford and General Motors in the chapter section "Auditing Account Balances Affected by Management's Estimates" as background. Why might it be difficult for auditors to disallow companies' preferences to decrease existing reserves? Explain the role of

1. The sufficiency of audit evidence is determined by: a. The reliability of the audit evidence. b. The quantity of evidence gathered. c. The risk of material misstatement of the assertion being examined. d. All of the above. 2. Regarding the auditor's reasoning process about an account balance,

Auditors routinely encounter client entries or financial accounting choices that are inconsistent with the financial statement assertions.Requireda. For each of the following, indicate what account balance assertion(s) is violated.1. Sales shipped FOB destination are recorded when shipped.Some of

You are planning the audit of the PageDoc Company's inventory. PageDoc manufactures a variety of office equipment. Required Describe how each of the following procedures could be used in the audit of inventory and the related assertion(s) it tests: Procedure ___________________How used

In this chapter, several different kinds of audit evidence were identified. The following questions concern the relevance and reliability of audit evidence.Requireda. Explain why confirmations are normally considered more reliable than inquiries of the client. Under what situations might the

Audit documentation represents the auditor's accumulation of evidence and conclusions reached on an audit engagement. Prior-year audit documentation can provide insight into an audit engagement that will be useful in planning the current year audit.Requireda. What are the purposes or primary

The following equipment schedule was prepared by the client and audited by Sam Staff, an audit assistant, during the calendar year 2011 audit of Roberta Enterprises, a continuing audit client. As engagement supervisor, you are reviewing the documentation.Required Identify the deficiencies in the

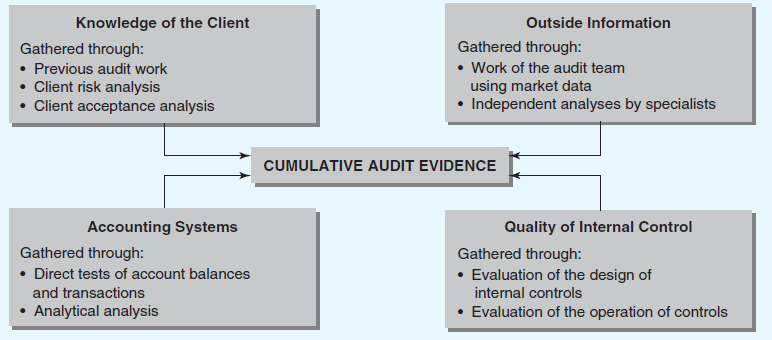

Exhibit 7.3 is a depiction of the sources of evidence. The auditor gathers:● Knowledge about the client● Information about internal controls● Accounting process information-tests of account balances and accounting processes● Outside information, including market informationRequireda.

The Professional Judgment in Context scenario at the beginning of the chapter introduced excerpts from the PCAOB inspection of Deloitte & Touche, LLP. The scenario is: On May 4, 2010, the PCAOB issued its public inspection of Deloitte & Touche, LLP covering their inspection of audits conducted

The International Standards on Auditing require the auditor to gather sufficient appropriate evidence to ensure that the auditor has a reasonable basis for an opinion regarding the financial statements. What are the characteristics of a. Sufficient audit evidence and b. Appropriate audit

Adecco SA is the world's largest temporary employment company. It lost several major accounts because customers felt it was not adequately serving their complex staffing needs. It announced that it was not able to deliver its financial statements on schedule. Their auditors had raised questions

As reported in the Wall Street Journal (September 11, 1989), MiniScribe, Inc., inflated its reported profits and inventory through a number of schemes designed to fool the auditors. At that time, MiniScribe was one of the major producers of disk drives for personal computers. The newspaper article

In Ford Motor Company's Annual Report, management disclosed the following risk factors that might affect the financial statements going forward. a. Continued decline in market share, and a market shift (or an increase in or acceleration of market shift) away from sales of trucks or sport utility

The purpose of this case is to provide you with an example of a decision setting in which we will explore the ethical issues involved in conducting audit procedures. This case is based on an actual situation that occurred in audit practice. However, names have been changed to achieve

To what extent are the concepts of sufficiency and relevance related to audit risk? Explain in terms of audits for which the auditor has determined that the level of audit risk will be low vs. an engagement in which the auditor has determined that the level of audit risk is higher.

ISA 200 identifies four major sources of audit evidence. What are these sources of evidence, and what are the components of each? Why is it important for the auditor to consider all four sources of evidence when auditing an organization?

Explain how information about the client, including previous audit work, client acceptance/continuance judgments, and the client's business risk are each relevant in developing comprehensive evidence used in assessing whether the financial statements are fairly presented.

Audit firms must be profitable and at the same time manage audit risk at a sufficient level to remain in business. Explain the tension between "making money" and managing the risk of the audit firm, and how the audit firm can minimize that tension. How might partner compensation affect audit risk?

Academic research addresses the conceptual issues outlined in this chapter. To help you consider the linkage between academic research and the practice of auditing, read the following research article and answer the questions below. Kaplan, S., O'Donnell, E., & Arel, B. (2008). The influence of

Identify the three main approaches the auditor might use to gather and evaluate audit evidence.

What information is needed to design a MUS sample? Where does the auditor gather such information?

All else being equal, what is the effect on a MUS sample size of an increase in: a. Tolerable misstatement? b. Expected misstatement? c. Detection risk? d. Population size?

An auditor evaluating a MUS sample of accounts receivable confirmations receives a confirmation response and has to determine whether the difference reported is due to (a) An error on the part of the client, (b) The customer's error, or (c) A timing difference. Explain how each would affect the

Explain how GAS can test for control effectiveness. For example, describe how an auditor could use GAS to identify whether a company has allowed credit to customers that do not meet its credit policies.

In which ways can GAS assist the auditor in planning and executing statistical sampling?

What is the relationship between the auditor's use of an analytical procedure and a client estimate?

Assume that the auditor concludes that detection risk must be very low. The auditor proposes that sales be audited by examining the relationship of sales and cost of sales to that of the previous two years, as adjusted for an increase in gross domestic product. Explain either why, or why not, this

Describe how each of the three approaches to gathering audit evidence discussed in this chapter can be used to test the five financial statement assertions: existence, completeness, rights, valuation, and presentation/disclosure. Provide examples of audit procedures for each of the approaches for

a. Sampling risk is 10%. Determine the sample size for each of the following controls:b. Explain why the sample sizes for controls 2 and 3 are different from those for control 1. c. What is the general effect on sample size of using a 10% sampling risk vs. a sampling risk of 5%? Explain. d. Under

The auditor uses MUS to select accounts receivables for confirmation. In confirming individual accounts receivable balances, your client's customers reported the exceptions listed below. Required Which of these exceptions should be considered misstatements for evaluation purposes, assuming that

The auditor must quantify the following parameters when using MUS sampling: 1. Tolerable misstatement 2. Expected misstatement 3. Risk of incorrect acceptance Required Describe each of these parameters and how they can be determined by the auditor.

The auditor is designing a MUS sample to determine how many accounts receivable confirmations to send. There are 2,000 customer accounts with a total book value of $5,643,200. The estimate of likely misstatement is estimated to be $40,000 and tolerable misstatement is set at $175,000.Requireda.

You are planning the confirmation of accounts receivable. There are 2,000 customer accounts with a total book value of $5,643,200. Tolerable misstatement is set at $175,000, expected misstatement is $40,000, and DR is 30%.Requireda. What is the sampling interval?b. What is the maximum sample

You are auditing the inventory of Husky Manufacturing Company for the year ended December 31, 2009. The book value is $8,124,998.66. Tolerable misstatement is $400,000 and expected misstatement is $10,000. Detection risk is 10% (confidence level of 90%). MUS sampling is to be used for a price

The auditor wishes to use GAS to assist in the audit of accounts receivable. The auditor's major objectives are to: • Evaluate existence by sending confirmations to customers. • Evaluate adequacy of allowance for doubtful accounts by: • Examining the file to determine if credit limits had

In your group, use the Internet to locate the financial statements for a company that you are familiar with. Identify specific account balances for which analytical procedures would be appropriate for conducting substantive tests of those balances.

Assume that you are a senior on an engagement and a member of your team has posed the following questions to you. How would you respond? Also discuss the relevance of professional skepticism. a. I have tested the first 25 items in the sample of 39. All 25 are free of misstatement. Do I need to test

A MUS sample results in a number of misstatements, the sum of which is not material. The auditor can project a most likely error and can compute an upper error limit. Which one is the most appropriate in determining whether there might be a material misstatement in the account balance? Explain your

Academic research addresses the conceptual issues outlined in this chapter. To help you consider the linkage between academic research and the practice of auditing, read the following research article and answer the questions below. Hall, T. W., Hunton, J. E., & Pierce, B. J. (2002). Sampling

What is professional skepticism? How is it applied when assessing the fraud risk of an organization, and then auditing that organization for the risk assessed by the auditor?

Which major oversight groups failed in their professional responsibilities in the Enron case? How did each group fail? What were the motivations that influenced each group that partially led to the failure? To what extent did Sarbanes-Oxley address many of the factors that caused the failures?

Fraud has always existed, but it seems that the attitude toward fraud may be changing. What are the major changes in the Josephson Institute's survey of high school students' attitudes toward lying or cheating?

What are some procedures the auditor can use to investigate the likelihood that fraud might exist in a company's accounts? The procedures should relate to identifying the potential existence of fraud, not to specifically identifying the fraud.

Explain the auditor's responsibility for reporting the following: • A defalcation that the client is willing to correct and portray in the financial statements • A defalcation that is material, but the client wishes to obscure by recording it in an "other expense" category • A financial

In your opinion, should auditors be required to report a material fraud (consider both a defalcation and preparation of fraudulent financial reporting) that was detected during the audit to: • Users of the company's financial statements? • Regulatory agencies, such as the SEC? • Law

Explain what procedures the auditor should employ upon identifying fraud risk factors.

Audit software can be very useful in analyzing data and identifying potential fraud. Identify the major fraud-related procedures that can be performed using audit software.

Professional skepticism has been emphasized as an important part of the audit process. However, the need to continually emphasize skepticism implies that auditors have a difficult time remaining skeptical.RequiredIn your groups address the following questions.a. What is professional skepticism? How

The text describes the Madoff Ponzi scheme, as well as other Ponzi schemes. All of the schemes require elements of both trust and greed. Since Madoff's Ponzi scheme was uncovered, many others have surfaced, including three in Minneapolis; one involving bank loans, another commodities trading, and a

Fraud continues to occur at smaller organizations at a rate higher than that of larger organizations. Explain why this is the case.

The following scenario and analytical information describe a company. Three sets of facts are presented about this company. Perform a brainstorming analysis identifying all the factors that will affect the planning and conduct of the audit. Specifically, discuss in your group the following: a.

Assume that your client possesses the following characteristics associated with the fraud triangle: Incentives: • Need to obtain additional debt or equity financing to stay competitive, including financing of major research and development or capital expenditures • Significant portions of

An auditor may consider a number of factors when identifying opportunities to commit fraud. The following represent areas that have often been associated with frauds. Situations Often Associated with Fraud 1. Related-party transactions 2. Industry dominance 3. Numerous subjective accounting

The following set of scenarios is adapted from "Test Your Ethical Judgment" by Kay Zekany, Strategic Finance November 1, 2007 and from the Institute of Management Accountants. Each of the scenarios is based on facts in the World Com fraud. Required For each scenario, decide which option (a) through

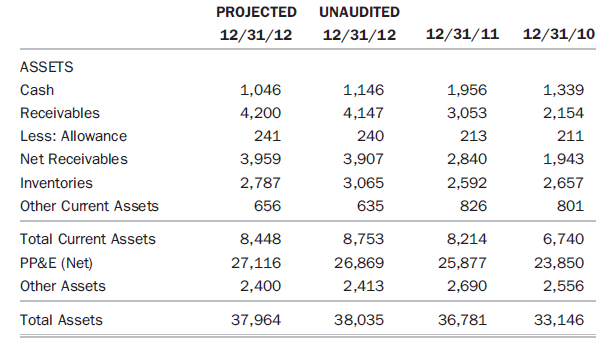

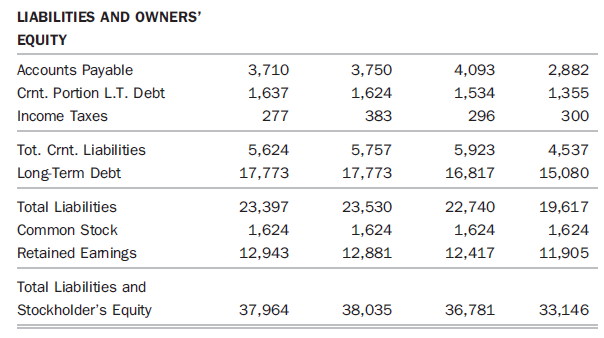

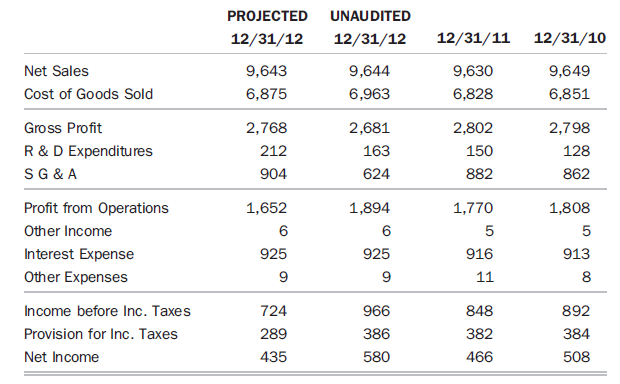

The following facts represent the audited financial statements of a public company for 2011 and 2010, along with management's representation regarding the unaudited amounts (i.e., the UNAUDITED column) and the auditors' projected amounts for 2012 (i.e., the PROJECTED column, which represents their

Hoffman, V. B., & Zimbelman, M. F. (2009). Do Strategic Reasoning and Brainstorming Help Auditors Change Their Standard Audit Procedures in Response to Fraud Risk? The Accounting Review 84(3):811-837. i. What is the issue being addressed in the paper? ii. Why is this issue important to practicing

What steps would the auditor take in performing an integrated audit?

How would the steps outlined in your answer to Review Question 10-10 differ if the auditor were not performing an integrated audit?

One of your audit clients manufactures fishing boats and sells them all over the country. Boats are sold to dealers who finance their purchases on a floor-plan basis with their banks. The banks usually pay your client within two weeks of shipment. The company's profits have been increasing over the

Stainless Steel Specialties (SSS) is a manufacturer of hot water-based heating systems for homes and commercial businesses. The company has grown about 10% in each of the past five years. The company has not made any acquisitions. Following are some of the statistics for the company during the past

Field, CPA, is auditing the financial statements of Miller Mailorder, Inc. (MMI) for the year ended January 31, 2012. Field has compiled a list of possible risks, including both errors and fraud, that may result in the misstatement of MMI's financial statements and a corresponding list of

In assessing the risks associated with revenue recognition, the auditor will likely consult criteria provided by the SEC. What criteria has the SEC used to help determine if revenue can be recognized? Why might the auditor need to do additional research and consider additional criteria on revenue

The following table includes a common risk in the revenue cycle that might be present at an audit client. For the risk, identify the relevant financial statement assertion and identify controls, including those related to the control activities and the control environment that the auditor might

Bert Finney, CPA, was engaged to conduct an audit of the financial statements of Clayton Realty Corporation for the month ending January 31, 2012. The examination of monthly rent reconciliation is a vital portion of the audit engagement. The following rent reconciliation was prepared by the

The following sales were selected for a cutoff test of Genius Monitors, Inc., for the December 31, 2012, financial statements. All sales are credit sales and are FOB shipping point. They are recorded on the billing dateRequired a. What adjusting journal entries, if any, would you recommend that the

As part of the audit of KC Enterprises, the auditor assessed control risk for the existence and valuation assertions related to accounts receivable at the maximum level. Katie, the staff person assigned to the engagement, sent positive confirmation requests to a sample of the company customers

You are auditing accounts receivable of HUSKY Corp. as of December 31, 2009. The accounts receivable general ledger balance is $4,263,919.52. The data files must be downloaded from the website www.cengage.com/ accounting/rittenberg. The files are labeled "HUSKY Unpaid Invoices 2009" (the

Review the Auditing in Practice feature focusing on the inappropriate actions of Robert A. Putnam, the engagement partner on the HBOC audit. In this case, we expand on the problems detected in the audit.Summarizing the facts from the SEC's Administrative Proceeding against Putnam dated April 28,

Academic research addresses the conceptual issues outlined in this chapter. To help you consider the linkage between academic research and the practice of auditing, read the following research article and answer the questions below. Callen, J. L., Robb, S. W. G., & Segal, D. (2008). Revenue

Describe some of the common fraud schemes that affect the inventory and cost of goods sold accounts. Discuss in small groups or in the class as a whole instances in which students have experienced or read about fraud schemes in their community or workplaces related to inventory. For example,

Compare worldwide professional guidance on auditing inventory accounts. What are the key requirements?

Why might a company understate expenses? Why might a company overstate expenses? How might a company accomplish these inaccuracies? For the auditor, how does professional skepticism play a role in considering these possibilities?

1. The auditor's inventory observation test counts are traced to the client's inventory listing to test for which of the following financial statement assertions? a. Completeness b. Existence c. Valuation d. Presentation and disclosure 2. Consider a nonpublic company where an opinion on internal

The SEC alleged that many deficiencies occurred during the audit of CMH, as discussed in the Auditing in Practice feature in this chapter. Among the complaints were the following:1. The audit firm "left the extent of various observation testing to the discretion of auditors, not all of whom were

Assume that you are conducting the audit of CollegeWare, a publicly held manufacturer and distributor of printed, embroidered, and embossed specialty clothing and gift items marketed to college students with school-specific logos. The company pays licensing fees and manufactures products in advance

The Professional Judgment in Context feature at the beginning of the chapter and the Auditing in Practice feature about CMH both describe scenarios whereby people with accounting or auditing responsibilities were lacking the appropriate training or knowledge to conduct their jobs. In a small group

Academic research addresses the conceptual issues outlined in this chapter. To help you consider the linkage between academic research and the practice of auditing, read the following research article and answer the questions below. Nigrini, M., & Mittermaier, L. (1997). The Use of Benford's Law as

Toyco, a retail toy chain, honors two bank credit cards and makes daily deposits of credit card sales in two credit card bank accounts (Bank A and Bank B). Each day, Toyco batches its credit card sales slips, bank deposit slips, and authorized sales return documents and send them to data processing

The following client-prepared bank reconciliation is being examined by Kautz, CPA, during an examination of the financial statements of Concrete Products, Inc.:Required Identify one or more audit procedures that should be performed by Kautz in gathering evidence in support of each of the items (a)

Aldhizer, G. R. & Cashell, J. D. (2006). Automating the Confirmation Process. The CPA Journal.76(4):28-32. Also available at www.nysscpa.org/cpajournal/2006/406/essentials/p28.htm. i. What is the issue being addressed in the paper? ii. Why is this issue important to practicing auditors? iii. What

Describe and compare worldwide professional auditing guidance on the use of subject-matter specialists/experts in auditing long-lived assets and related expense accounts.

In Terex Corporation's 2009 Annual Report, the company's CEO, Ronald Defeo, made this statement regarding the recessionary times that his company is facing: I like to say that, "when you are in a hurricane, you have to expect to get wet and blown around!" In 2009, many of our markets declined 70%

Your audit firm has been the auditor of Cowan Industries for a number of years. The company manufactures a wide range of lawn care products and typically sells to major retailers. In recent years, the company has expanded into ancillary products, such as recreation equipment, that use some of the

In the Professional Judgment in Context case at the beginning of this chapter, we reviewed some of the pertinent findings from the COSO (2010) study on fraudulent financial reporting. The study notes the many ways in which fixed assets can be fraudulently overstated including: ● Fictitious assets

Acito, A. A., Burks, J. J., & Johnson, W. B. (2009). Materiality Decisions and the Correction of Accounting Errors. The Accounting Review 84(3):659-688. i. What is the issue being addressed in the paper? ii. Why is this issue important to practicing auditors? iii. What are the findings of the

Explain how a bond amortization spreadsheet might be used to audit interest expense over the life of a bond.

In 2010, Nelson Communications purchased a controlling interest in Telnetco that resulted in goodwill in the 2010 consolidated financial statements of $4,500,000. There are no other intangible assets. Telnetco continues to be listed on NASDAQ. Near the end of 2011, Nelson estimated that the fair

One of the Auditing in Practice features in the chapter discusses Ford Motor Company's reducing a large portion of its other postretirement benefits by transferring its liability to the UAW Union through a one-time payment of $11.3 billion. However, Ford still has a sizeable liability for

Showing 9300 - 9400

of 10291

First

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

Last

Step by Step Answers

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

-1.png)

-2.png)

-3.png)

.png)