New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing

Auditing The Art and Science of Assurance Engagements 13th Canadian edition Alvin A. Arens, Randal J. Elder, Mark S. Beasley, Joanne C. Jones - Solutions

What are the legal tests for auditor negligence?

Why is duty of care so important for third party lawsuits but not client lawsuits?

How can auditors defend themselves against such suits?

Explain why some experts argue that the best defense against legal liability is careful client acceptance and continuance processes?

Helmut & Co., a public accounting firm, was the new auditor of Mountain Ltd., a private company in the farm equipment and supply business. In early February 2015, Helmut & Co. began the audit for the year ended December 31, 2014. The audit was to be run by Frost, a senior who had just joined Helmut

The public accounting firm of André, Mathieu, & Paquette (AMP) was expanding very rapidly. Consequently, it hired several junior accountants, including Small. The partners of the firm eventually became dissatisfied with Small's production and warned him that they would be forced to terminate

Jan Sharpe recently joined the public accounting firm of Spark, Watts, and Wilcox. On her third audit for the firm, Sharpe examined the underlying documentation of 200 disbursements as a test of purchasing, receiving, vouchers payable, and cash disbursement procedures. In the process, she found 12

In confirming accounts receivable on December 31, 2014, the auditor found 15 discrepancies between the customer's records and the recorded amounts in the subsidiary ledger. A copy of all confirmations that had exceptions was turned over to the company controller to investigate the reason for the

In this chapter, we discussed the major sources of an auditor's legal liability as well as the five defences that auditors can use when faced with a lawsuit. Now, it's time for you to find out how these concepts are applied to real-life situations. In 2009, the Honourable Daniel W. Payette of the

Bryan Longview's ethical dilemma involves a situation in which he is asked to work without regarding the time, which is sometimes called kitchen-tabling or eating time. One of the concerns with eating time is that it can lead to a more severe problem known as premature signoff, in which a staff

What are the four steps of the professional judgment framework and how is a useful tool? What are some common judgment traps?

Why is professional skepticism considered essential to the proper exercise of professional judgment?

Describe an ethical dilemma. How can you apply the ethical reasoning framework to an ethical dilemma?

Why are ethical decisions so difficult? Consider the role of rationalizations and ethical blind spots.

Explain the need for a code of professional ethics for PAs.

What is meant by the statement, "The rules of professional conduct of a professional accounting organization should be regarded as a minimum standard?"

What are the five threats to independence? Describe each and provide an example.

List three categories of safeguards to independence. Provide an example of each.

How does communication with the predecessor auditor improve audit quality?

Zaspa Inc. is a public company that manufactures and sells tennis racquets. The company has expanded internationally and its auditors have resigned due to the fact that they have insufficient staff to meet the needs of the expanding business. In light of this fact, Zaspa has approached your firm,

Diane Harris, a PA, is the auditor of Fine Deal Furniture, Inc. In the course of her audit for the year ended December 31, 2015, she discovered that Fine Deal had serious going-concern problems. Henri Fine, the owner of Fine Deal, asked Diane to delay completing her audit. Diane is also the auditor

The following situations involve the provision of non-audit services. a. Providing bookkeeping services to a listed entity. The services were preapproved by the audit committee of the company. b. Providing internal audit services to a listed entity that is not an audit client. c. Designing and

Each of the following scenarios involves a possible violation of the rules of conduct. a. John Brown is a PA, but not a partner, with three years of professional experience with Lyle and Lyle, Public Accountants, a one-office public accounting firm. He owns 25 shares of stock in an audit client of

Explain how "framing the problem" can help overcome judgment traps when auditing subjective areas such as fair value estimates.

Each of the following situations involves possible violations of the rules of conduct that apply to professional accountants. a. Martha Painter, PA, was appointed as the trustee of the So family trust. The So family trust owned the shares of the So Manufacturing Company, which is audited by another

The following are situations that may violate the general rules of conduct of professional accountants. Assume in each case that the PA is a partner. a. Simone Able, a PA, owns a substantial limited partnership interest in an apartment building. Juan Rodriquez is a 100 percent owner in Rodriquez

Donna, a PA, is approached by the owner of one of her clients, for whom she normally compiles monthly and annual financial statements, to perform an audit of the company's inventories. The client, Fantastic Fashions Ltd., is a chain of retail clothing stores that operates in several local shopping

Aqua Inc. was a privately owned company that operated a marina business from two lakefront properties in northern Ontario. The company was started by two brothers. The company provided boat docking, sold gasoline and boating supplies, and was very successful. Aqua's accountant, John Purd, was a PA

Barbara Whitley had great expectations about her future as she sat at her graduation ceremony in May 2015. She was about to receive her Master of Accountancy degree, and the following week she would begin her career on the audit staff of Green, Thresher & Co., a public accounting firm. Things

Refer to the opening vignette regarding the Livent case. REQUIRED a. Explain how this case illustrates the importance of framing the issue. b. The ICAO disciplinary committee argues that professional judgment requires a correct conclusion. How do you reconcile this view with the common view that

The national assurance service line leader at Grant Thornton, Jeremy Jagt, commenting on the deficiencies the CPAB found in audits of companies in emerging markets, suggested that issues around cultural difference could account for differences in professional judgment.Below is a summary of the

Why is an auditor's independence so essential? How can judgment traps affect auditors' independence?

What consulting or non-audit services are prohibited for auditors of public companies? Explain why it is generally agreed that prohibitions on consulting and non-audit services will improve auditors' professional judgment and professional skepticism.

Explain why documentation can improve auditors' professional and/or ethical judgment.

We discussed various audit quality initiatives. An example of an audit quality initiative is the Standards Working Group of the Global Policy Committee (comprising BDO, Deloitte Touche Tomatsu, Ernst & Young, Grant Thornton, KPMG, and PricewaterhouseCoopers). The Global Policy Committee is a

Is it possible for the auditor to conduct the audit without reliance on management? Why or why not?

What are the three different types of audit objectives? Provide an example of each for the completeness audit objective.

How do presentation and disclosure-related objectives differ from transaction-related and balance-related audit objectives?

What is the relationship between risk assessment and risk response during the financial statement audit?

When is quality control conducted during the audit? How does this affect risk assessment?

What are the responsibilities of those in charge of governance regarding fraud and illegal acts?

How do indirect-effect illegal acts affect the financial statements?

Why does the audit process use cycle?

What are entity-wide controls and what is their significance to the audit process?

What are management assertions about financial information?

How does the auditor use management assertions during the financial statement audit?

Distinguish between the existence and completeness balance-related audit objectives. State the effect on the financial statements (overstatement or understatement) of a violation of each in the audit of accounts payable. Discuss.

Explain why existence is a relevant assertion for fixed assets. How does identifying relevant assertions affect audit objectives and evidence accumulation?

Identify the management assertion and presentation and disclosure-related audit objective for the specific presentation and disclosure-related audit objective: Read the fixed asset footnote disclosure to determine that the types of fixed assets, depreciation methods, and useful lives are clearly

Identify the eight phases of the audit. What is the relationship of the eight phases to the objective of the audit of financial statements?

The following general ledger accounts are included in the trial balance for an audit client, Jones Wholesale Stationery Store. Accounts receivable Accrued sales salaries Accumulated amortization of furniture and equipment Advertising expense Allowance for doubtful accounts Amortization

Jane was the audit supervisor in charge of the audit of an advertising agency. Unfortunately, two other audit supervisors in the office resigned and moved on to other positions. Rather than hiring or promoting another supervisor, the firm reallocated clients. Jane was asked to take on some of the

Renée Ritter opened a small grocery and related products convenience store in 1993 with the money she had saved working as a Loblaws store manager. She named it Ritter Dairy and Fruits. Because of the excellent location and her fine management skills, Ritter Dairy and Fruits grew to three

The following information was obtained from several accounting and auditing enforcement releases issued by the Securities and Exchange Commission (SEC) after its investigation of fraudulent financial reporting involving Just for Feet, Inc.: • Just for Feet, Inc., was a national retailer of

Distinguish between the terms "errors" and "fraud and other irregularities." What is the auditor's responsibility for finding each?

Access a copy of the CPAB's 2013 Annual Inspection Report at www.cpab-ccrc.ca/Documents/Topics/Public%20 Reports/2013_Public_Report_EN.pdf . Refer to Appendix D of the report, which summarizes the most common inspections findings and groups them by category. REQUIRED 1. Read the examples provided

Many of Canada's larger public companies are listed on American stock exchanges. Auditors who conduct these audits are required to follow PCAOB auditing standards. In that type of audit, in addition to issuing an opinion on the financial statements, the auditors also issue an opinion on internal

The Canadian Securities Administrators (CSA) regularly perform reviews of the quality of interim and annual information filed with the provincial securities regulators. Part of this review includes the quality of financial statements presentation and disclosure. In their July 2014 review, the CSA

Arthur Andersen partner Michael Jones, in his documentation of the critical meeting attended by key Andersen partners to discuss their client continuance decision, recorded the following: We discussed Enron's dependence on transaction execution to meet financial objectives, the fact that Enron

How does brainstorming regarding fraud risk improve auditors' professional judgment? Explain how it helps to mitigate potential judgment traps.

Identify four types of information in the client's minutes of the board of directors' meetings that are likely to be relevant to the auditor. Explain why it is important to read the minutes early in the engagement.

For the audit of Radline Manufacturing Company, the audit partner asks you to carefully read the new mortgage documents from Green Bank and extract all pertinent information. List the information in a mortgage that is likely to be relevant to the auditor.

During the planning phase of every audit, Roger Morris, CPA, calculates a large number of ratios and trends for comparison with industry averages and prior-year calculations. He believes the calculations are worth the relatively small cost of doing them because they provide him with an excellent

An auditor performs various procedures during audit planning. For each procedure, indicate which of the first four parts of audit planning the procedure primarily relates to: (1) accept the client and perform initial audit planning; (2) understand the client's business and industry; (3) assess the

The minutes of the board of directors of the Tetonic Metals Company for the year ended December 31, 2014, were provided to you. MEETING OF MARCH 5, 2015 The meeting of the board of directors of Tetonic Metals was called to order by James Cook, the chair of the board, at 8:30 a.m. The following

You are auditing payroll for the Morehead Technologies company for the year ended October 31, 2015. Included next are amounts from the client's trial balance, along with comparative audited information for the prior year.You have obtained the following information to help you perform preliminary

Your comparison of the gross margin percent for Jones Drugs for the years 2012 through 2015 indicates a significant decline. This is shown by the following information:A discussion with Nandini Sharma, the controller, brings to light two possible explanations. She informs you that the industry

The internet has dramatically increased global ecommerce activities. Both traditional "bricks and mortar" businesses and new dot-com businesses use the internet to meet business objectives. However, in order to continue to succeed, dot-com businesses are pressured to change their business models.

Winston Black was an audit partner at Maharajah, Davis, LLP. He was in the process of reviewing the audit files for the audit of a new client, McMullan Resourcing. McMullan was in the business of heavy construction. Winston was conducting his first review after the field work had been substantially

Kent, CPA, is the engagement partner on the financial statement audit of Super Computer Services Co. (SCS) for the year ended April 30, 2015. On May 6, 2015, Smith, the senior auditor assigned to the engagement, had the following conversation with Kent concerning the planning phase of the audit:

Assessing Risk at Niko Resources Refer to Auditing in Action 6-3 . a. Based upon the facts presented related to Niko, explain how they impact the risk of material misstatement. Explain if it has an overall impact on financial reporting risk and identify the related account balances and/or

INTRODUCTIONThis case study focuses on the risk assessment stage of the audit. Each of the four parts deals largely with the material in the chapter to which that part relates. However, the parts are connected in such a way that in completing all four, you will gain a better understanding of how a

Planning is one of the most demanding and important aspects of an audit. A carefully planned audit increases auditor efficiency and provides greater assurance that the audit team addresses the critical issues. Auditors prepare audit planning documents that summarize client and industry background

What is the difference between overall materiality and performance materiality? How does the use of performance materiality affect the audit process?

Why do auditors use specific performance materiality?

Using the audit risk model, holding all factors equal, what happens to detection risk if control risk goes down? Why?

Why should the auditor consider client business risk when determining audit risk?

Describe the risk of material misstatement using parts of the audit risk model.

How would the complexity of information systems affect inherent risk?

How can general rule of thumbs and past experience with the client create judgment traps for auditors' risk assessments? Provide an example for inherent risk and control risk assessments.

Define materiality as it is used in accounting and auditing. What is the relationship between materiality and the phrase "obtain reasonable assurance" used in the auditor's report?

Some countries, such as the United Kingdom,require that the auditor's report include a statement of materiality level and risk of material misstatement. Some accountants suggest that the audit risk that the auditor used in conducting the audit should also be disclosed. REQUIRED a. The proponents of

Statements of earnings and financial position for Prairie Stores Corporation are shown.REQUIRED a. Use professional judgment in determining overall materiality based on revenue, net income before taxes, total assets, and shareholders' equity. Your conclusions should be stated in terms of

You are evaluating audit results for current assets in the audit of Quicky Plumbing Co. You set the specifi c performance materiality for current assets at $12 500 for overstatements and at $20 000 for understatements. The estimated and actual misstatement ranges are shown below.REQUIREDa. Justify

Following are six situations that involve the audit risk model as it is used for planning audit evidence requirements in the audit of inventory. REQUIRED a. Explain what low , medium , and high mean for each of the four risks and planned evidence. b. Fill in the blanks for planned detection risk

Bohrer, CPA, is considering the following factors in assessing audit risk at the fi nancial statement level in planning the audit of Waste Remediation Services (WRS), Inc.'s fi nancial statements for the year ended December 31, 2015. WRS is a privately held company that contracts with municipal

Joanne Whitehead is planning the audit of a newly obtained client, Henderson Energy Corporation, for the year ended December 31, 2015. Henderson Energy is regulated by the provincial utility commission and, because it is a publicly traded company, the audited fi nancial statements must be fi led

You are the senior auditor in charge of the December 31, 2015, year-end audit for Cleo Patrick Cosmetics Inc. (CPCI). CPCI is a large, privately held Canadian company that was founded in 1996 by one of Canada's best known hair stylists, Cleo Patrick. Cleo Patrick is a famous celebrity hair stylist

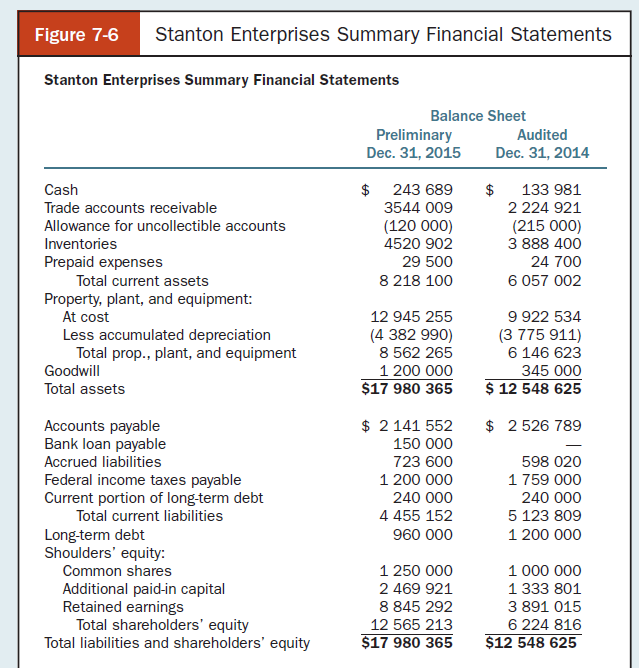

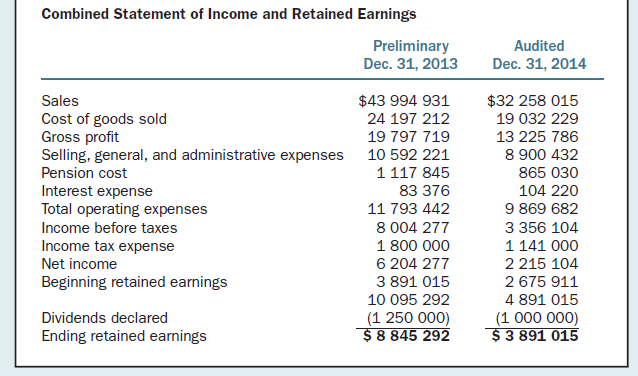

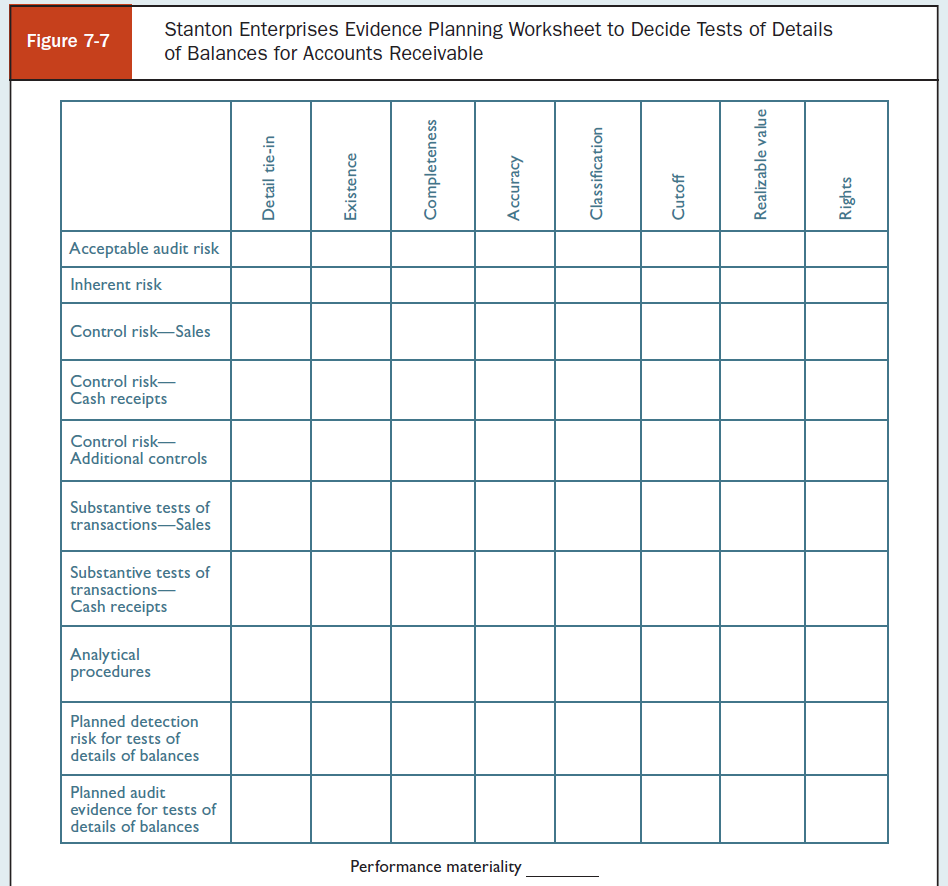

Pamela Albright is the manager of the audit of Stanton Enterprises, a public company that manufactures formed steel subassemblies for other manufacturers. Albright is planning the 2015 audit and is considering an appropriate amount for overall financial statement materiality, what performance

How does engagement risk affect the audit process?

Explain why inherent risk is estimated for specifi c accounts rather than for the overall audit. What is the effect on the amount of evidence the auditor must accumulate when inherent risk is increased from medium to high for a segment?

Explain the relationship between audit risk and the legal liability of auditors.

What is meant by acceptable audit risk ? What is its relevance to evidence accumulation?

In the opening vignette and Auditing in Action 7-1 , we referred to the Financial Reporting Council ("FRC"), the United Kingdom's independent regulator responsible for promoting high-quality corporate governance and reporting to foster investment. The council sets standards for corporate reporting,

Explain the impact on the audit if the client relies upon outsourced systems that process material transactions.

What are entity-level controls and why are they so important?

What are general controls? Explain how they are similar to entity-level controls.

What are control activities? Explain their role in the financial reporting process.

What are the accounting information and communication controls? How are they distinct from business process controls?

How is management's risk assessment relevant to the audit?

Showing 9500 - 9600

of 10291

First

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

Step by Step Answers

.png)

-1.png)

-2.png)

-1.png)

-2.png)

.png)

.png)