Question: If the r.v.s X and Y have the Bivariate Normal distribution with parameters μ 1 , μ 2 in R,0 < Ï 1 , Ï

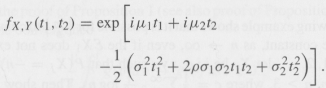

If the r.v.s X and Y have the Bivariate Normal distribution with parameters μ1, μ2in R,0 < σ1, σ2< ˆž. and p ˆˆ [-1, 1], show that their joint ch.f. is given by

For this purpose, do the following:

(i) Assume first that μ1 = μ2 = 0 and σ1 = σ2 = 1, and use Exercises 12 (ii) in Chapter 9 and 13 (ii) in this chapter to show that:

(ii) For the general case, use the transformations U = (X €“ μ1)/σ1, V = (Y €“ μ2)/σ2 and verify that ÔU = ÔV = 0, Var(U) = Var(V) = 1, p(U, V) = p(X, Y) = p. Then use Exercise 15 in Chapter 9 and part (i) here to arrive at the desired expression for the ch.f. fX.Y.

fx,Y (t1, 12) = exp iuiti +iuzt2 (oi + 2po102112 + oik)| + 2p0102t|12 +

Step by Step Solution

3.35 Rating (158 Votes )

There are 3 Steps involved in it

i For 1 2 0 and 1 2 1 we have so that However the second integral on the right... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

742-M-S-P (6964).docx

120 KBs Word File