Question: Sapphire Ltd has a complex capital structure that includes both ordinary shares and potential ordinary shares. Sapphire Ltd reported the following net profit and dividends

Sapphire Ltd has a complex capital structure that includes both ordinary shares and potential ordinary shares.

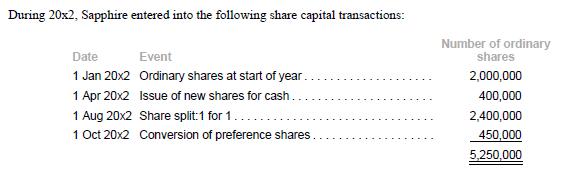

Sapphire Ltd reported the following net profit and dividends information for the current year ended 31 December 20x2.

The following information relates to potential ordinary shares issued by Sapphire Ltd:

(a) On 1 July 20x1, Sapphire issued 1,000,000 convertible preference shares at $1 per share. On 1 October 20x2, 450,000 preference shares were converted to ordinary shares. Under the issue agreement, the shares bear a tax exempt coupon rate of 6% on a non-cumulative basis. The dividends are paid on a pro-rated basis for the period that the shares are outstanding. Prior to the share split, the conversion ratio was two preference shares to one ordinary share. After the share split, the conversion ratio is on a one-to-one basis.

(b) On 31 December 20x2, Sapphire had 600,000 units of outstanding stock options. These options were issued on 1 April 20x2 and none were exercised during 20x2. Each stock option entitles the holder to purchase one ordinary share at the exercise price of $2.60 per share. The average market price for the period from 1 April 20x2 to 31 December 20x2 was $3.00 per share. All prices were adjusted for share splits.

(c) On 1 July 20x2, Sapphire issued convertible bonds. Under IAS 32, the bonds were recognized separately from the equity options. The fair value of the bonds was $6,000,000. Each dollar of bond was convertible to one ordinary share after adjustment for share split. There were no conversions in 20x2. The effective interest rate of the bonds was 5% per annum.

(d) Tax rate applicable to 20x2 was 20%. Preference dividends are tax-exempt.

Required

1. Determine the basic earnings per share of Sapphire Ltd for the year ended 31 December 20x2.

2. Determine the earnings per incremental share for each potential ordinary share for the year ended 31 December 20x2.

3. Determine the diluted earnings per share for the year ended 31 December 20x2.

Net profit after tax. Less preference dividends. Net profit attributable to ordinary shareholders.. $6,900,000 (53,250) $6,846,750

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts