During the course of an audit engagement, a CPA attempts to obtain satisfaction that there are no

Question:

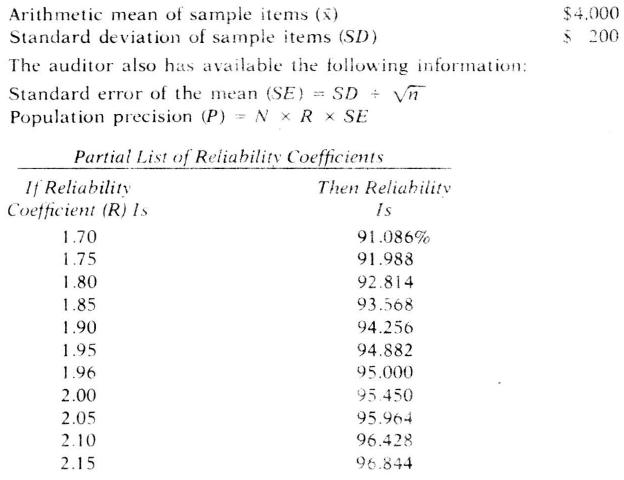

During the course of an audit engagement, a CPA attempts to obtain satisfaction that there are no material misstatements in the accounts receivable of a client. Statistical sampling is a tool that the auditor often uses to obtain representative evidence to achieve the desired satisfaction. On a particular engagement an auditor determined that a material misstatement in a population of accounts would be \(\$ 35,000\). To obtain satisfaction the auditor had to be \(95 \%\) confident that the population of accounts was not in error by \(\$ 35,000\). The auditor decided to use unrestricted random sampling with replacement and took a preliminary random sample of 100 items ( \(\mathbf{n}\) ) from a population of 1,000 items \((\mathrm{N})\). The sample produced the following data:

Required:

a. Define the statistical terms "reliability" and "precision" as appiied to auditing.

b. If all necessary audit work is performed on the preliminary sample items and no errors are detected, 1. What can the auditor say about the total amount of accounts receivable at the \(95 \%\) reliability level?

2. At what confidence level can the auditor say that the population is not in error by \(\$ 35,000\) ?

c. Assuming that the preliminary sample was sufficient, 1. Compute the auditor's estimate of the population total.

2. Indicate how the auditor should relate this estimate to the client's recorded amount.

Step by Step Answer:

Modern Auditing

ISBN: 9780471542834

5th Edition

Authors: Walter Gerry Kell, William C. Boynton, Richard E. Ziegler