Question: Apply the same model sequence used in Example 6.2 to the extended velocity series (1869-1988) (e.g. Koop and Steel, 1994). This series is identified as

Apply the same model sequence used in Example 6.2 to the extended velocity series (1869-1988) (e.g. Koop and Steel, 1994). This series is identified as non-stationary (with significant probability that \(ho>1\) ) by Bauwens et al. (2000). The data for this series are included in Exercise 6.2. odc.

Data from Example 6.2

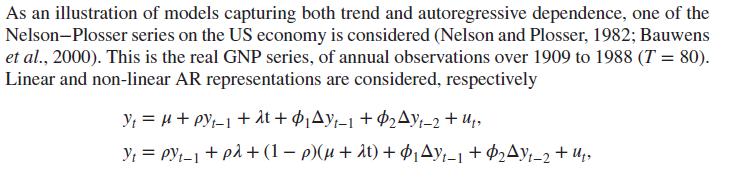

As an illustration of models capturing both trend and autoregressive dependence, one of the Nelson-Plosser series on the US economy is considered (Nelson and Plosser, 1982; Bauwens et al., 2000). This is the real GNP series, of annual observations over 1909 to 1988 (T = 80). Linear and non-linear AR representations are considered, respectively y = + pyt-1 +t + AY1 + $2y-2+u, y = pyt-1+p + (1 p)( + t) + $1yt-1 + $2y1-2+u

Step by Step Solution

3.47 Rating (150 Votes )

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts