New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing risk based approach

Auditing A Practical Approach 2nd Canadian edition Fiona Campbell, Robyn Moroney, Jane Hamilton, Valerie Warren - Solutions

When an audit test reveals an error or exception, the auditor should: (a) Try to understand why the error or exception has occurred. (b) Consider increasing the sample size. (c) Consider additional testing. (d) All of the above.

When testing payroll, the auditor: (a) Reviews that the hours on timecards are recorded in the payroll ledger in the correct period. (b) Uses only the number of employees at the end of the period as the predictor of total payroll expense. (c) Uses the list of employees who left

Searching for unrecorded liabilities: (a) Is not an important audit procedure. (b) Can be done by examining subsequent payments or unmatched invoices. (c) Is always performed by confirming accounts payable. (d) Is part of testing the mathematical accuracy of the payables

The following account is not an expense account that is ordinarily tested as part of the testing of asset balances: (a) Bad debts expense. (b) Purchases. (c) Interest received. (d) Depreciation.

Comparing the relationship of overhead costs in cost of sales to direct labour is an example of this type of auditing technique: (a) Vouching to original documents. (b) Tracing posting of original documents to the ledger. (c) Analytical procedures. (d) Confirmation.

Classification is an important assertion for expenses because: (a) There is often an incentive to overstate expenses. (b) Some expenses are subject to specific disclosure requirements. (c) Vouching is a useful audit technique for expenses. (d) Auditing assets gives no evidence

The important assertion(s) for revenue is (are): (a) Occurrence, because testing needs to ensure that recorded sales are genuine. (b) Never completeness, because a company would never want to understate its revenue. (c) Completeness when there could be pressure to defer sales

Delivery documentation for the sale of goods: (a) Is important because it provides evidence supporting the date of sale. (b) Is not important to audit because the invoice date is always the correct date of sale. (c) Is important because it shows how hard the personnel in the

Sales revenue is a significant account for an entity: (a) Because of the high volume of transactions that flow through the account. (b) Because of the overall inherent risk associated with revenue. (c) Except for a start-up company. (d) All of the above.

A key difference between auditing balance sheet accounts and income statement accounts is that: (a) Balance sheet accounts always have larger totals. (b) Balance sheet accounts are always more significant accounts. (c) Income statement accounts reflect the entire 12 months of

You are an auditor employed at B & B Accountants. On November 20, 2016, the partner in your firm sends you the following e-mail: Our firm has been reappointed auditors of Floral Impressions Ltd. (FIL) for the year ending December 31, 2016. I met with the president and major shareholder of FIL,

Your firm is the auditor of Newtown Ltd., and you have been asked to suggest audit work you will carry out in verifying accounts payable and accruals at the company’s year end of December 31, 2016. You attend the inventory count at the year end. The company operates from a single site and all

Securimax Limited has been an audit client of KFP Partners for the past 15 years. Securimax is based in Waterloo, Ontario, where it manufactures high-tech armour-plated personnel carriers. Securimax often has to go through a competitive market tender process to win large government contracts. Its

Juanita Rosa’s auditing firm is conducting an external audit of TYY Inc.’s financial statements (for the period ended December 31, 2016). The audit manager has assigned Juanita to analyze the replies for the confirmations sent to TYY’s accounts receivables, and also to prepare the aging of

You have been assigned to audit the sales and accounts receivable balances of Coppero Engineering Ltd. for the year ended September 30, 2016. Coppero Engineering is a major manufacturer of steel parts and fixtures for other manufacturers in the engineering field. The interim work was undertaken in

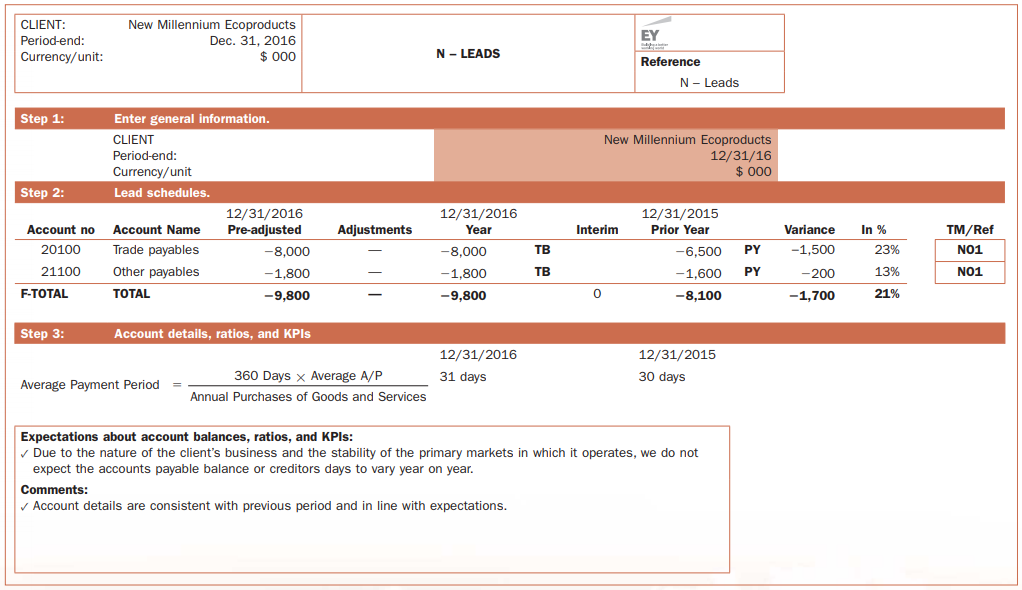

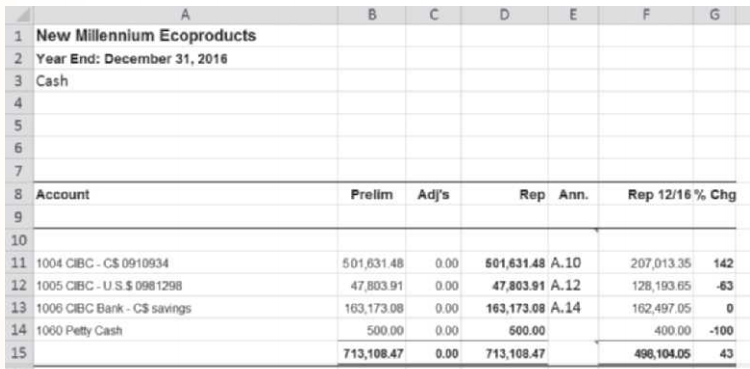

The following is a copy of the auditor’s working paper for auditing accounts payable for the client New Millennium Ecoproducts. Required (a) Explain the nature of the test being documented in the working paper. (b) Compare the information for the current year with the details for

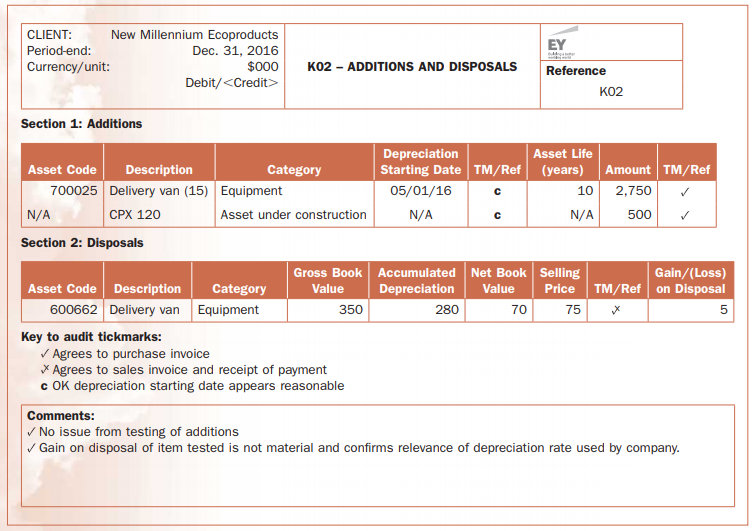

The following is a copy of the auditor’s working paper for auditing additions and disposals relevant to the balance of property, plant, and equipment (PPE) for the client New Millennium Ecoproducts. Required (a) What assertions are relevant to additions and disposals of PPE? (b)

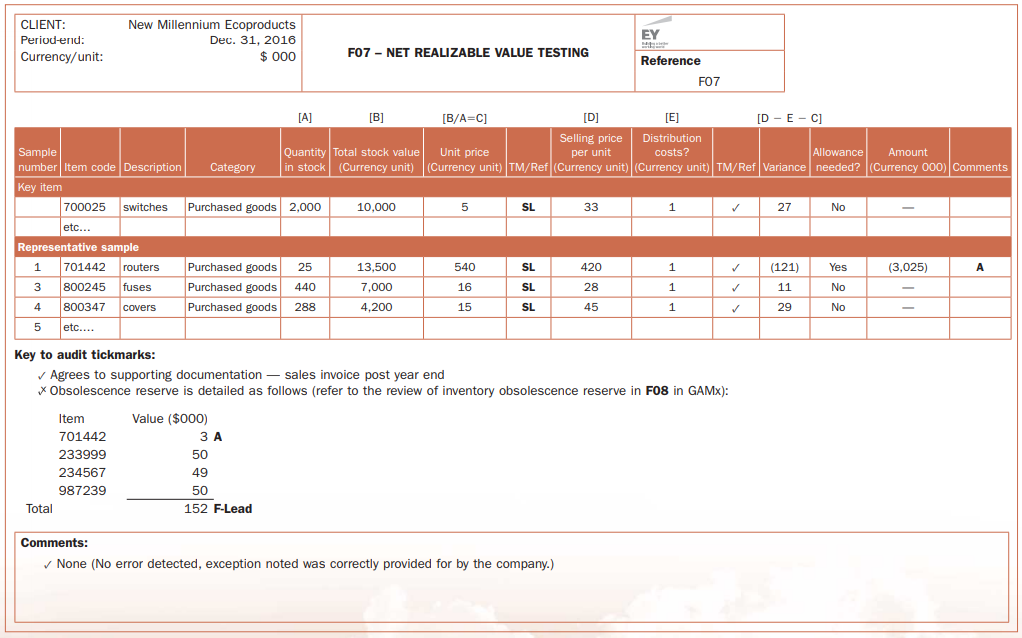

The following is a copy of the auditor’s working paper for auditing inventory balances for the client New Millennium Ecoproducts. It shows the details of the net realizable value (NRV) tests. Required (a) Why does an auditor test for NRV? (b) Find the details of the inventory items

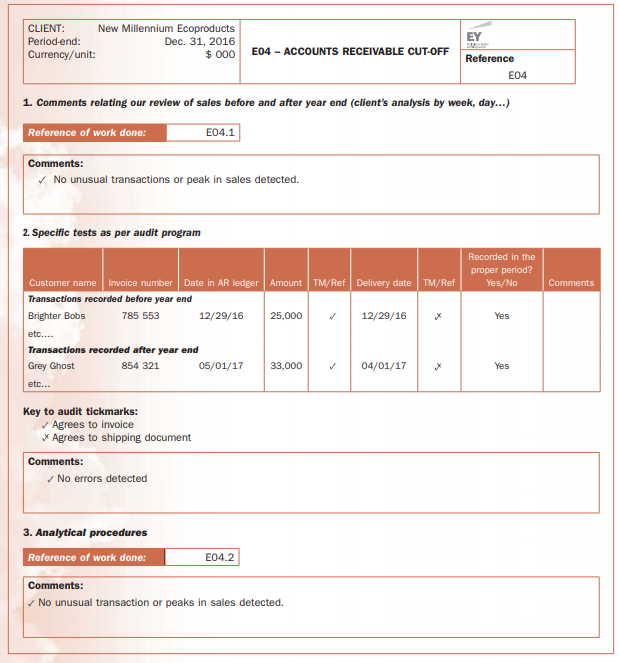

The following is a copy of the auditor’s working paper for auditing accounts receivable balances for the client New Millennium Ecoproducts. It shows the details of the cut-off tests. Required (a) Find the details of the transactions selected for cut-off tests. Why would these

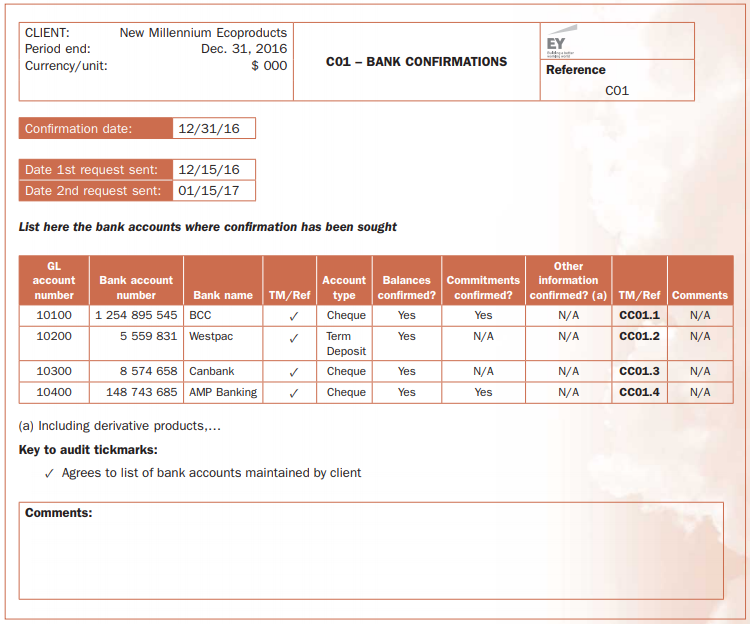

The following is a copy of the auditor’s working paper for auditing cash at bank balances for the client New Millennium Eco products. It shows the details of the bank confirmation requests. Required (a) Find the list of banks from which the auditor has sought bank confirmations. How

Fellowes and Associates Chartered Accountants is a successful mid-tier accounting firm with a large range of clients across Canada. During 2016, Fellowes and Associates gained a new client, Health Care Holdings Group (HCHG), which owns 100 percent of the following entities: Shady Oaks Centre,

The following items are documented in the audit working papers: 1. Sales transaction included in the year ended December 31, 2016, but evidence from the cut-off procedure suggests that the sale should be dated January 2, 2017 ($1,250,000). 2. Warranty expenses in the trial balance for the

Analysis is a substantive audit procedure that auditors use when they are performing financial statement audits. Required (a) Distinguish between analysis and analytical procedures. (b) Identify the three stages in the audit process at which analysis can be performed. (c) For each

Review your answers to the previous questions. Comment on the persuasiveness of evidence from each test. Explain any factors that would affect your assessment.

Inventory of various medical supplies and drugs is a material account on the Shady Oaks Centre audit engagement. You are planning to adopt a combined audit approach for existence of inventory and rely heavily on preventive control procedures (for example, access to the dispensary and the store room

Anna Mourani has the task of designing the audit program for the payroll area. There have been no recent changes to the payroll system, or its interface with the general ledger. Among other tests, Anna is considering using the following analytical procedures to gather evidence: 1. Compare

Seb Lee and Boris Shonkoff are discussing the audit program for the revenue account. Seb and Boris disagree about whether they should use procedure A or B below to test the occurrence assertion for the revenue account: A. Select a sample of sales from the sales journal and agree the details in

Boris Shonkoff has another suggestion for the audit program for the revenue account. This time he suggests: Select a sample of sales from the sales journal and agree the details in the journal to the sales invoices, delivery slips, and customer orders. Required Explain which assertion for

Boris Shonkoff suggests the following audit procedure should be included in the audit program to gather evidence on the cut-off assertion for the revenue account: Select a sample of sales from the sales journal and agree the dates on the invoices to the dates on the delivery documents signed by the

Misstatements: (a) Are documented in the audit working papers. (b) Can be categorized as errors or judgemental misstatements. (c) Must be considered for their effect on the financial statements both individually and in aggregate. (d) All of the above.

Roll-forward procedures: (a) Need to be responsive to the control risk assessment. (b) Are procedures done during the month after year end. (c) Have no effect on audit efficiency. (d) None of the above.

The primary advantage of selecting the largest transactions within a balance to test is: (a) It is an example of random sampling. (b) It is more interesting for the auditor because they see the most important transactions in detail. (c) That the auditor is able to draw a conclusion

Vouching is: (a) Not a useful audit procedure. (b) Agreeing a balance or transaction to supporting documentation. (c) The main audit procedure used to gather evidence on the completeness assertion. (d) Not designed to be used as a substantive audit procedure.

The reliability of data used for analytical procedures: (a) Affects the persuasiveness of the evidence from analytical procedures. (b) Is more useful on a consolidated basis than an individual business segment basis. (c) Is unaffected by inflation. (d) Is never affected by the

The following conditions make absolute data comparisons relatively less useful: (a) Multiple years of financial data available. (b) Single-location clients. (c) Changes in production methods. (d) Budgets that are carefully prepared.

We can conclude that analytical procedures provide persuasive evidence: (a) Always. (b) Never. (c) If they do not provide sufficient evidence by themselves to allow us to conclude that the account is free of material errors. (d) If we are able to conclude that no further

Analytical procedures: (a) Are used to test controls and are not substantive procedures. (b) Are substantive procedures and cannot be used at any other stage of the audit. (c) Are used at planning and substantive testing stages of the audit. (d) Can be used as substantive tests

The following factor(s) influences how much and when substantive procedures are performed: (a) The nature of the test. (b) The level of assurance necessary. (c) The type of evidence required. (d) All of the above.

Designing substantive procedures responds to: (a) The risk of material misstatement at the entity level. (b) The risk of material misstatement at the assertion level. (c) The risk of all types of misstatements at the assertion level. (d) The risk of all types of misstatements at

The lead auditor was reviewing the results of testing controls in the employee expense area. The documentation for the testing showed that there was one instance of a part-time staff member being paid an incorrect hourly rate. Required Explain why the result shows a control exception

The audit senior on the audit of Frankel Factors is preparing the audit plan for the year ended June 30, 2016. The following notes relate to the payroll application system that went live on January 1, 2016: 1. The new payroll application is more complex than the old system, but its reporting

Jintian Clothing Ltd. manufactures sportswear and sells it to large department stores in western Canada. The company records sales in a sales journal. When a customer orders merchandise, a sales clerk prepares a sales invoice. The credit manager must approve all sales to new customers, and a record

ABC is a company that purchases ski equipment from a European manufacturer and then sells the equipment to stores in eastern Canada. The company’s records include pre-numbered shipping and purchasing invoices, a sales journal, a purchases journal, and sub-ledgers for both payables and

The following procedures are used for EGO Company: EGO’s purchasing manager approves all purchases above $250. This allows the administrative staff to use the petty cash system to purchase minor items that are needed for the office and the manufacturing plant. When a supplier invoice is

The junior auditor on the engagement has suggested that, since there were no exceptions detected in previous years, no work on internal controls is required because last year’s evidence will be sufficient. Required Explain why the junior auditor’s suggestion is not appropriate and outline

Within the client’s IT system, supplier information is contained in a supplier master file (SMF). Each supplier has a unique supplier code. If the purchasing clerk attempts to place an order from a supplier not in the SMF, the order cannot be processed. Required Explain what type of control

The client company assigns each new employee a user profile and password for the computer system. The first time the new employee logs onto a company desktop computer, they are automatically forced to change their password. Passwords must be changed every 30 days. Required Explain what

What is the difference between entity level controls and transaction level controls?

Working papers: (a) Document the purpose of the test of the control identified and the results of the test, including a specific conclusion about whether the test results supported the overall purpose of the test. (b) Are necessary for the junior auditor to keep track of the daily work

A major change in the accounting system has taken place during the year. The effect on control testing is that: (a) The auditor should ensure controls testing is performed for periods both before and after the accounting change became effective. (b) The auditor can assume the accounting

Which of the following would require the auditor to increase the level of control testing for a particular control? (a) The control is performed monthly instead of daily.(b) There are several controls relating to a particular audit objective. (c) The WCGW addressed by the control is not

Inspection of physical evidence is a control test used by auditors. It: (a) Relies on questioning skills. (b) Is subject to a limitation because employees may be more diligent when they know they are being observed. (c) Relies on testing the physical evidence. (d) Requires the

Examples of application controls include: (a) Edit checks. (b) Validations. (c) Calculations. (d) All of the above.

ITGCs are important because they: (a) Prevent authorized personnel from having access to data and applications. (b) Impact the effectiveness of both application controls and IT-dependent manual controls. (c) Prevent the reliability of electronic audit evidence. (d) Allow client

Detective controls do not include: (a) Management level reviews. (b) Performance indicators. (c) Account coding. (d) Reconciliations.

Which is not a type of control? (a) Automated controls. (b) Substantive controls. (c) Manual controls. (d) IT-dependent manual controls.

The purpose of controls is to: (a) Prevent misstatements in the financial statements. (b) Detect misstatements in the financial statements. (c) Support automated parts of a business in the functioning of the controls. (d) All of the above.

The auditor decides which controls to test by considering: (a) The type of control. (b) The frequency of the control being performed. (c) The level of assurance the auditor wishes to gain. (d) All of the above.

Answer the following questions based on the information presented for Cloud 9 in Appendix B to this book and in the current and earlier chapters. You should also consider your answers to the case study questions in earlier chapters. Sharon Gallagher and Josh Thomas have assessed the internal

Lise Couture is documenting the purchasing and cash payments processes at Hardies Wholesaling. Hardies Wholesaling imports garden and landscaping items, such as pots, furniture, fountains, mirrors, and sculpture, from suppliers in Southeast Asia. All items are nonperishable; are made from materials

The following is the documentation of the payroll cycle at McQuarrie Enterprises, a ladies clothing wholesaler. There are approximately 50 staff members at McQuarrie Enterprises. Every employee has a payroll file that includes their offer letter, completed and signed tax deduction forms, a void

Fellowes and Associates Chartered Accountants is a successful mid-tier accounting firm with a large range of clients across Canada. During the financial year 2016, Fellowes and Associates gained a new client, Health Care Holdings Group (HCHG), which owns 100 percent of the following

Fellowes and Associates Chartered Accountants is a successful mid-tier accounting firm with a large range of clients across Canada. During the financial year 2016, Fellowes and Associates gained a new client, Health Care Holdings Group (HCHG), which owns 100 percent of the following

The following is a summary of the purchase process at McQuarrie Enterprises, a wholesaler of ladies clothing. Purchases are authorized and made by departmental managers. Sequential purchase orders are completed for all purchases and forwarded to the accounting department. Departmental managers may

Soak City Waterpark Ltd. is a family-owned business just outside of Winnipeg. The waterpark is only open for business from May to September. During the winter months, the waterpark undergoes repairs and maintenance upgrades. The capital assets for Soak City are signifi cant and the Waterpark

Required For each of the following statements of possible things that can go wrong, identify the audit objective and an internal control that should be implemented to prevent the WCGW. (a) Sales are made to customers that do not have approved credit. (b) Goods not ordered by the customer

A management letter: (a) Contains recommendations for improving internal control and discusses other issues discovered during the course of the audit. (b) Is written by management to the auditor at the start of the audit. (c) Lists only the significant deficiencies discovered during

Documenting internal controls: (a) Is always handled through the use of checklists and preformatted questionnaires. (b) Is done after internal controls are tested so that the results can be included in the documentation. (c) Can be handled with a combination of narratives and

Internal control in small entities: (a) Is always stronger because the owner-manager can supervise every activity. (b) Is likely to be less formal than in a larger entity. (c) Does not have the risk of management override. (d) Always results in an auditor placing a greater

Segregation of incompatible duties: (a) Is a guarantee that fraud cannot occur. (b) Is the same as performance review by a supervisor. (c) Means that different people are assigned responsibilities for authorizing transactions, recording transactions, and maintaining custody of

Performance reviews: (a) Are not relevant to internal controls. (b) Are applicable only to the chief executive officer in an organization. (c) Are part of control activities. (d) Can include financial data only.

Auditors are interested in an entity’s information systems: (a) Because they consist of procedures and records to deal with transactions and maintain accountability for related assets, liabilities, and equity. (b) Because their quality affects management’s ability to make appropriate

An entity’s risk assessment process: (a) Is the entity’s process for identifying and responding to business risks and the results thereof. (b) Is established only if the entity is subject to unusually high risk. (c) Is designed to help an entity think about risk in the same way

The control environment: (a) Is the economic environment in which the organization operates. (b) Is the combination of the culture, structure, and discipline of an organization. (c) Applies only to listed companies. (d) All of the above.

The objectives of internal controls include: (a) That fictitious transaction is not included in the organization’s records. (b) That correct amounts are assigned to transactions. (c) That transaction is recorded in the correct accounting period. (d) All of the above.

Internal control is a process: (a) Designed to provide reasonable assurance about the achievement of the entity’s objectives with regard to the reliability of financial reporting, effectiveness, and efficiency of operations, and compliance with applicable laws and regulations. (b) That

MICA is a regional credit union with 10 branches across the province. MICA leases its premises and buys furniture, such as waiting-area chairs and back-office desks, through a central asset purchasing department. All computer assets are acquired on finance leases. The furniture in the waiting area

BBB auditors have been the auditor on the Wild Ride Theme Park for the past two years. They have completed both the financial audit and the audit for the Department of Sport and Leisure, stating that the business has adhered to the Theme Park Regulations. Wild Ride Theme Park has requested that BBB

The controls at a retail store were assessed by the lead auditor as being effective and the auditor intended to rely on the operative effectiveness of controls around payroll in determining the nature, timing, and extent of substantive procedures. There is no evidence of fraud. The control

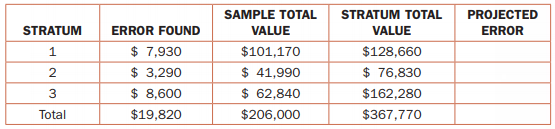

The results of substantive testing of sales invoices at City Electronics are shown in table 6.8. The three strata correspond to different departments and the overall tolerable error is set at $40,000. Required (a) Project the errors for each stratum and calculate the total projected error. Is

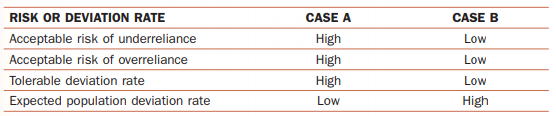

Patrizia Montani is considering the sample size needed for a selection of sales invoices relating to the test of internal controls of the Caistor Company. She is determining the acceptable risk and deviation rates, and is considering two possible scenarios as shown in table 6.7. Required In

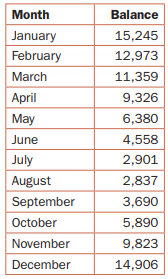

Rahim, a first-year auditor, is asked to select a sample of invoices to audit the utility expense account. Below is the account detail. The audit program asks to select a sample of four items. Required (a) Using systematic selection, determine which four months will be selected. (b)

Give an example of substantive testing where stratification would be appropriate.

The auditor has discovered errors when conducting substantive testing on a sample of invoices. If the total error discovered is $3,442, the dollar value of the sample is $25,136, and the population dollar value is $64,912, then the projected error is:(a) $3,442. (b) $8,889.(c) $1,885. (d)

Tolerable error:(a) is the maximum error an auditor is willing to accept within the population.(b) is positively related to sample size.(c) relates only to control testing.(d) is an amount prescribed by CAS 530.

Non-sampling risk:(a) Occurs only if you test every member of the population.(b) Applies only to samples taken for the purposes of control testing.(c) Is the risk that an auditor arrives at an inappropriate conclusion for a reason unrelated to sampling issues.(d) Does not occur if an auditor relies

Sampling risk:(a) Is the risk that the results of the test will be misinterpreted by the auditor.(b) Is the risk that the sample chosen by the auditor is not representative of the population of transactions.(c) Can be eliminated by taking a random sample.(d) Applies only to samples for substantive

If preliminary testing of controls reveals that the rate of deviation in controls is above the expected rate, the auditor will:(a) Reduce detection risk and increase reliance on detailed substantive testing at year end.(b) Increase detection risk and increase reliance on detailed substantive

The relationship between audit risk, reliance on substantive testing, and evidence persuasiveness is:(a) High audit risk, low reliance on substantive testing, low evidence persuasiveness required.(b) Low audit risk, high reliance on substantive testing, low evidence persuasiveness required.(c) High

Analytical procedures:(a) Are less efficient than substantive testing of details.(b) Place less reliance on the client’s accounting records than substantive testing of details.(c) Are relied on to a greater extent when a client’s internal controls are effective.(d) Are most useful when inherent

Deviations: (a) Are errors that affect account balances by a material amount. (b) Occur when controls do not operate as intended. (c) Are relevant only when they occur consistently throughout the accounting period. (d) Are caused by auditors choosing incorrect audit procedures.

When testing controls the auditor:(a) Is interested in assessing the effectiveness of controls.(b) Gathers evidence about the balances of the main accounts.(c) Does not have to have any prior knowledge of the client’s inherent risks and how the controls address those risks.(d) All of the above.

A detailed audit plan:(a) is based on the overall audit strategy.(b) contains a description of the control testing procedures.(c) lists the audit procedures to be used in substantive testing.(d) all of the above.

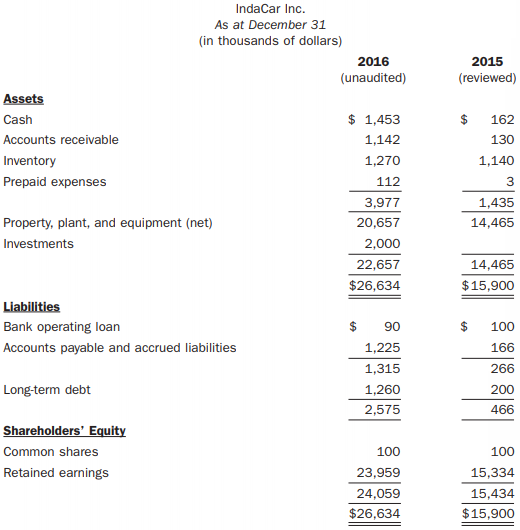

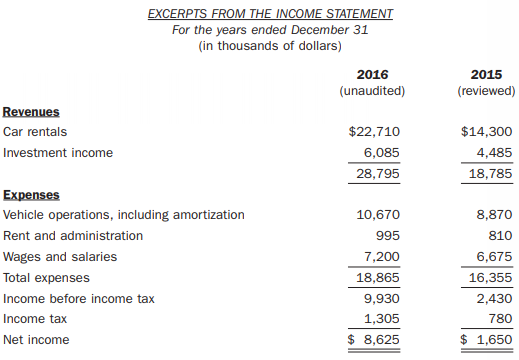

IndaCar Inc. (IC) operates a high-end car rental agency that specializes in the rental of unique vehicles and is located next to Lester B. Pearson International Airport in Toronto. IC is a private Canadian company that is wholly owned by Jake Bouvier. Daytona Lemans LLP, Chartered Professional

The working paper in figure 5.11 was prepared by James Parkhill, a first year accountant. Find seven errors that James made while completing this working paper. Figure 5.11 D. 1 New Millennium Ecoproducts 2 Year End: December 31, 2016 з Cash 8 Account Rep Ann. Prelim Adj's Rep 12/16 % Chg 10

For each of the following documents, state whether it would be located in the auditors’ permanent file or the current file.(a) Articles of incorporation(b) Bank confirmation for the current year(c) Management representation letter for the current year(d) Long-term debt agreement(e) Organization

Fellowes and Associates Chartered Accountants is a successful mid-tier accounting firm with a large range of clients across Canada. In 2016, Fellowes and Associates gained a new client, Health Care Holdings Group (HCHG), which owns 100 percent of the following entities: Shady Oaks Centre, a

Featherbed Surf & Leisure Holidays Ltd. is a resort company based on Vancouver Island. Its operations include boating, surfi ng, diving, and other leisure activities; a backpackers’ hostel; a family hotel; and a fi ve-star resort. Justin and Sarah Morris own the majority of the shares in the

The audit program for the Revenue account for a client has been drafted. The following item appears: Required (a) Does the procedure address the stated assertion? Explain. (b) If your answer to (a) is no, provide the correct assertion or suggest additional work.(c) Explain what type

The audit program for the Revenue account for a client has been drafted. The following item appears: Required (a) Does the procedure address the stated assertion? Explain. (b) If your answer to (a) is no, provide the correct assertion or explain what work would be required to address

Showing 300 - 400

of 537

1

2

3

4

5

6

Step by Step Answers