New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing risk based approach

Auditing And Assurance Services An Integrated Approach 17th Edition Alvin A. Arens, Randal J. Elder, Mark S. Beasley - Solutions

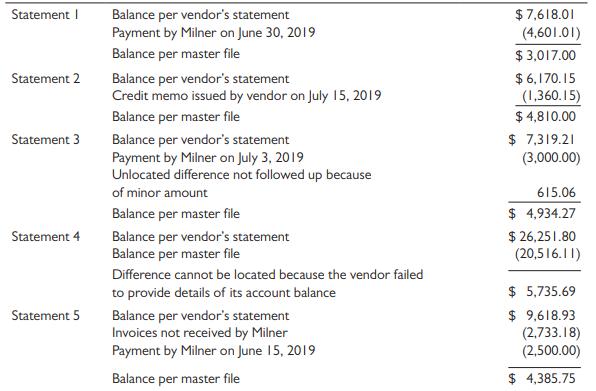

As part of the June 30, 2019, audit of accounts payable of Milner Products Company, the auditor sent 22 confirmations of accounts payable to vendors in the form of requests for statements. Four of the statements were not returned by the vendors, and five vendors reported balances different from the

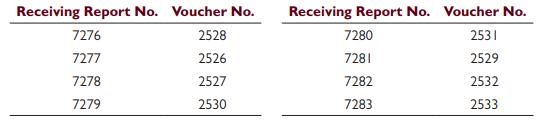

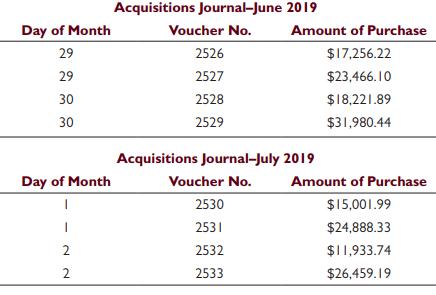

The Broughton Cap Company requires that prenumbered receiving reports be completed when purchased inventory items arrive in the receiving department. At the time of receipt, the receiving clerk writes the date of receipt on the receiving document. The last receipt in the fiscal year ended June 30,

The following are various audit procedures performed in the audit of the acquisition and payment cycle and accounts payable: 1. Foot the acquisitions journal for the month of August and trace postings to general ledger and accounts payable master file. 2. Determine that the amount of

The following audit procedures are included in the audit program for the audit of the financial statements of Golden State Overnight Express: 1. Select a sample of acquisitions from the acquisitions journal and perform the following: a. Vouch the transaction to the voucher package that

The following questions concern internal controls and accumulating evidence in the acquisition and payment cycle. Choose the best answer. a. While auditing a client’s purchase transactions, an auditor selects a sample of vouchers and then compares the dates on the vouchers to the dates on

The following questions concern internal controls in the acquisition and payment cycle. Choose the best response. a. An auditor traced a sample of purchase orders and the related receiving reports to the purchases journal and the cash disbursements journal. The purpose of this substantive

The CPA examines all unrecorded invoices on hand as of February 28, 2020, the last day of the audit. Which of the following misstatements is most likely to be uncovered by this procedure? Explain. a. Accounts payable are overstated at December 31, 2019. b. Accounts payable are understated

List one possible control for each of the seven transaction-related audit objectives for acquisitions. For each control, list a test of control to test its effectiveness.

List one possible internal control for each of the seven transaction related audit objectives for cash disbursements. For each control, list a test of control to test its effectiveness.

This problem requires the use of ACL software, which can be accessed through the textbook website. Information about downloading and using ACL and the commands used in this problem can also be found on the textbook website. You should read all of the reference material, especially the material on

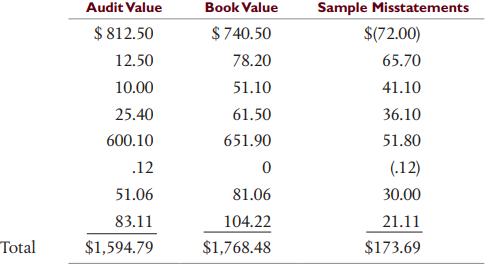

In auditing the valuation of inventory, the auditor, Claudette Perrier, decided to use difference estimation. She decided to select an unrestricted random sample of 80 inventory items from a population of 1,840 that had a book value of $175,820. Perrier decided in advance that she was willing to

The following questions relate to nonstatistical and monetary unit sampling. Choose the best response. a. A number of factors influence the sample size for a substantive test of details of an account balance. All other factors being equal, which of the following would lead to a larger sample

An auditor is determining the appropriate sample size for testing inventory valuation using MUS. The population has 3,140 inventory items valued at $19,325,000. The tolerable misstatement is $575,000 at a 10 percent ARIA. No misstatements are expected in the population. Calculate the preliminary

Describe why the use of MUS sampling provides little, if any, evidence related to the completeness balance-related audit objective.

How does stratifying an account balance population for sampling differ from using data analytics to audit the entire balance?

This problem requires the use of ACL software, which can be accessed through the textbook website. Information about downloading and using ACL and the commands used in this problem can also be found on the textbook website. You should read all of the reference material, especially the material on

You have been assigned to the first audit of the Chicago Company for the year ending March 31, 2019. Accounts receivable were confirmed on December 31, 2018, and at that date the receivables consisted of approximately 200 accounts with balances totaling $956,750. Fifty of these accounts, with

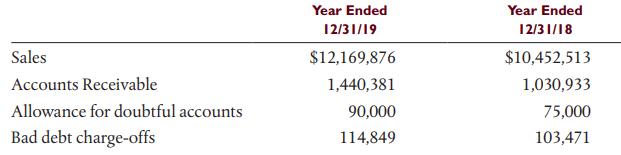

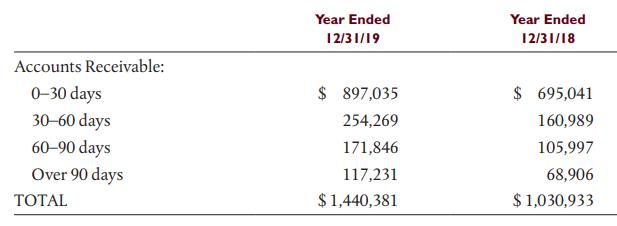

The Salah Company sells electronics equipment and has grown rapidly in the last year by adding new customers. The audit partner has asked you to evaluate the allowance for doubtful accounts at December 31, 2019. Comparative information on sales and accounts receivable is included

Chen, CPA, is auditing the financial statements of a manufacturing company with a significant amount of trade accounts receivable. Chen is satisfied that the accounts are correctly summarized and classified and that allocations, reclassifications, and valuations are made in accordance with GAAP.

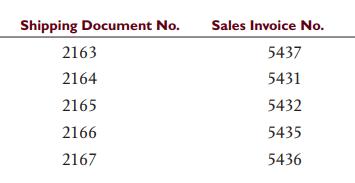

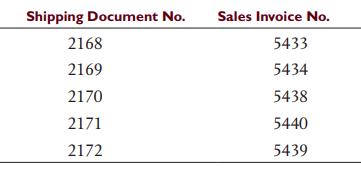

Makoto Auto Parts sells new parts for foreign automobiles to auto dealers. Company policy requires that a prenumbered shipping document be issued for each sale. At the time of pickup or shipment, the shipping clerk records the date on the shipping document. The last shipment made in the fiscal year

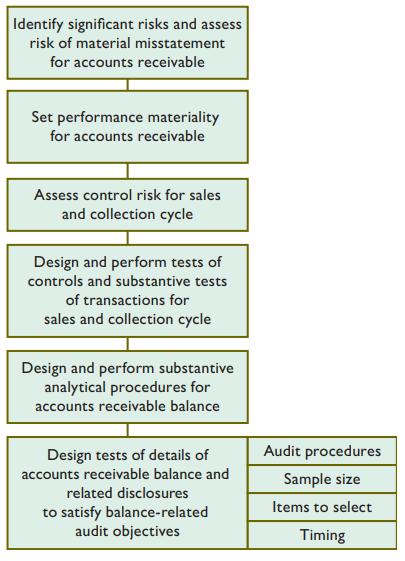

The following are the nine balance-related audit objectives, seven tests of details of balances for accounts receivable, and six tests of controls or substantive tests of transactions for the sales and collection cycle: Balance-Related Audit Objective Detail tie-in

With advances in technology, an increasing number of data analysis techniques are being used on audit engagements to increase both efficiency and effectiveness. In an article titled “Introduction to Data Analysis for Auditors and Accountants,” published in the CPA Journal (February 16, 2017),

You are responsible for designing the audit of notes receivable for Hickory Appliance Retailers, which sells appliances and electronics to consumers for their homes or small businesses. Hickory Appliance has eight store locations in different cities located in the upper Midwestern part of the

The following are common tests of details of balances or substantive analytical procedures for the audit of accounts receivable: 1. Select 20 customer accounts from the accounts receivable master file and trace to the aged accounts receivable listing to verify name and amount. 2. Select

The following questions concern auditor responsibilities related to the audit of accounts receivable. Choose the best response. a. The auditor sends out positive accounts receivable confirmations for a client. Assuming a second confirmation is sent out to a major customer who still fails to

The following questions deal with confirmation of accounts receivable. Choose the best response. a. The return of a positive confirmation of accounts receivable without an exception attests to the (1) Collectibility of the receivable balance. (2) Accuracy of the allowance for

Explain how unacceptable results from tests of controls and substantive tests of transactions might impact the auditor’s planned reliance on tests of details of balances.

Describe how auditors might use data visualization techniques to perform analytical procedures on disaggregate data for sales or accounts receivable. Provide a specific example.

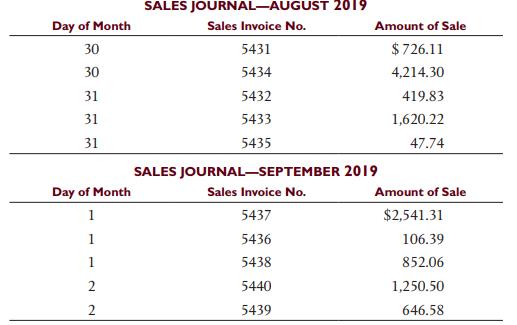

For the audit of Carbald Supply Company, Carole Wever, CPA, is conducting a test of sales for 9 months of the year ended December 31, 2019. Included among her audit procedures are the following: 1. Electronically re-add the sales journal and trace the balance to the general ledger. 2.

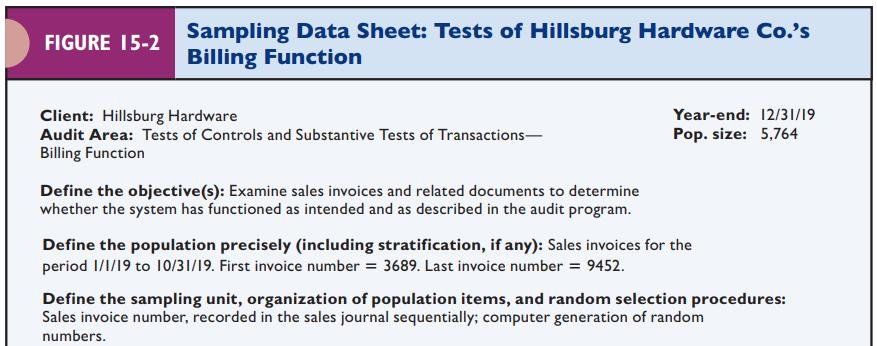

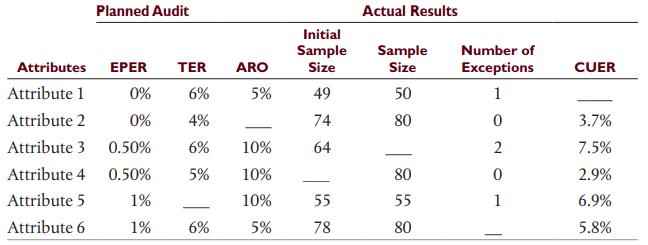

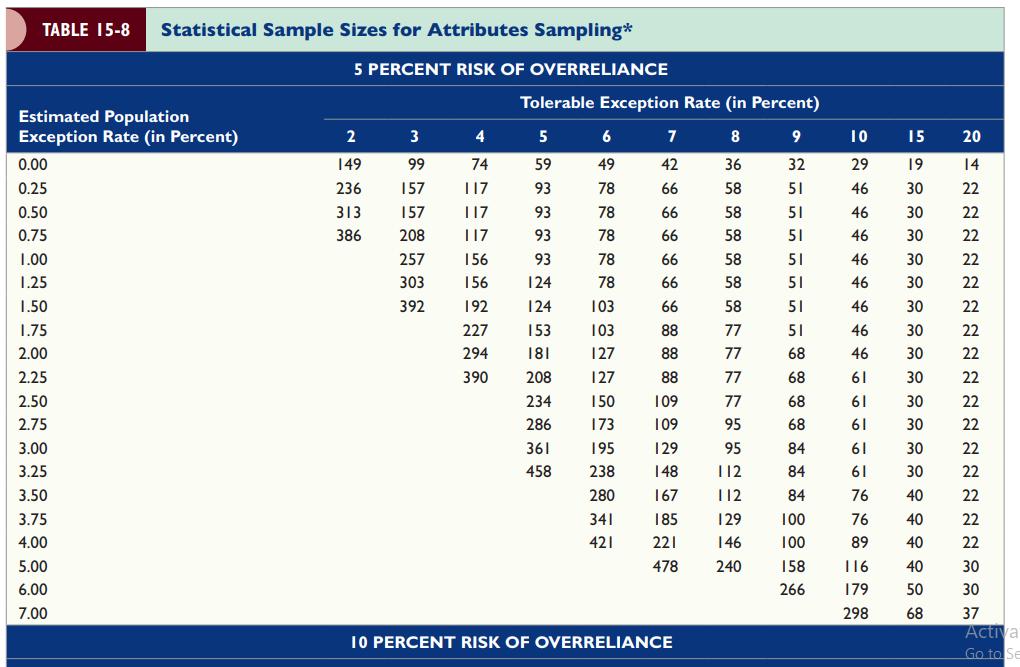

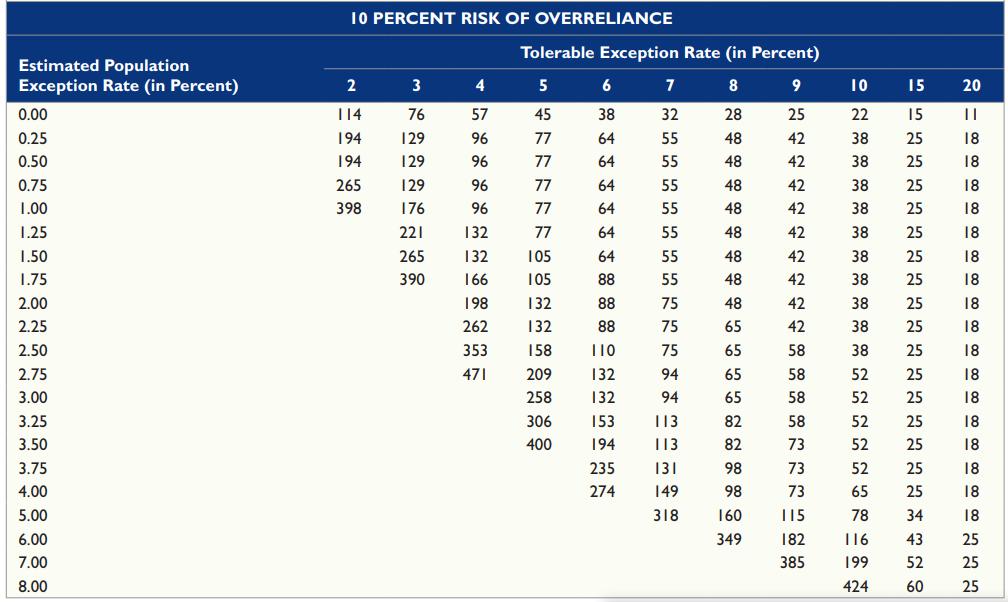

The sampling data sheet below is missing selected information for six attributes involving tests of transactions for the sales and collection cycle. Required:a. Use Table 15-8 (p. 519) and Table 15-9 (p. 521) to complete the missing information for each attribute. b. For which attributes

Auditing standards provide general guidance to auditors regarding audit sampling but do not require statistical versus nonstatistical sampling or specify which sampling method auditors should use. Search the Internet for “PCAOB Audit Sampling” or go to pcaobus.org to locate the PCAOB’s

The following items concern determining exception rates using random sampling from large populations using attributes sampling. Select the best response. a. The upper precision limit (CUER) in statistical sampling is (1) the percentage of items in a sample that possess a particular

List the major decisions that the auditor must make in using statistical attributes sampling. State the most important considerations involved in making each decision.

Define statistical attributes sampling. For which types of tests do auditors use attributes sampling?

Identify the factors an auditor uses to decide the appropriate ARO. Compare the sample size for an ARO of 10 percent with that of 5 percent, all other factors being equal.

Identify the factors an auditor uses to decide the appropriate TER. Compare the sample size for a TER of 7 percent with that of 4 percent, all other factors being equal.

Identify when an auditor would not use sampling to test the effectiveness of a control or perform a substantive tests of transactions. Explain circumstances when an auditor could test the entire population using a data analytic procedure using audit software.

Explain the difference between an attribute and an exception condition. State the exception condition for the audit procedure: The sales invoice has been approved, indicating the performance of internal verification.

Explain the difference between probabilistic and nonprobabilistic sample selection.

This problem requires the use of ACL software, which can be accessed through the textbook website. Information about downloading and using ACL and the commands used in this problem can also be found on the textbook website. You should read all of the reference material preceding the instructions

The PCAOB issues audit practice alerts to highlight new, emerging, or otherwise noteworthy circumstances. Revenue is the largest account in the financial statements for many companies, and many fraudulent financial reporting cases have involved the intentional overstatement of revenue. For these

The following is a list of possible errors or fraud (1 through 8) involving sales and controls (a. through k.) that may prevent or detect the errors or fraud: Possible Errors or Fraud 1. Invoices are sent for shipped goods, and are recorded in the sales journal, but are not posted to any

The following questions deal with internal control and audit evidence in the sales and collection cycle. Choose the best response. a. Tracing shipping documents to sales invoices provides evidence that (1) Sales billed to customers were actually shipped. (2) All goods ordered by

The following questions deal with audit evidence for the sales and collection cycle. Choose the best response. a. To determine whether internal control relative to the revenue cycle of a wholesaling entity is operating effectively in minimizing the failure to prepare sales invoices, an auditor

For each of the following types of misstatements (parts a. through c.), select the control that should have prevented the misstatement: a. Which of the following controls most likely will be effective in offsetting the tendency of sales personnel to maximize sales volume at the expense of high

Diane Smith, CPA, performed tests of controls and substantive tests of transactions for sales for the month of March in an audit of the financial statements for the year ended December 31, 2019. Based on the excellent results of both the tests of controls and the substantive tests of transactions,

Accounting standards require that companies provide footnote disclosures that enable a reader to understand the nature, timing, amount, and uncertainty surrounding revenue and cash flows arising from contracts with customers. Provide an example of an internal control that the client can use to

Describe the following documents and records and explain their use in the sales and collection cycle: a. Bill of lading, b. Credit memo, c. Remittance advice, d. Accounts receivable trial balance.

Both transaction-related and balance-related audit objectives include objectives related to presentation and disclosure. Visit the website of the United States Securities and Exchange Commission (SEC) and locate the Accounting and Auditing Enforcement Release (AAER) No. 3850 issued on January 18,

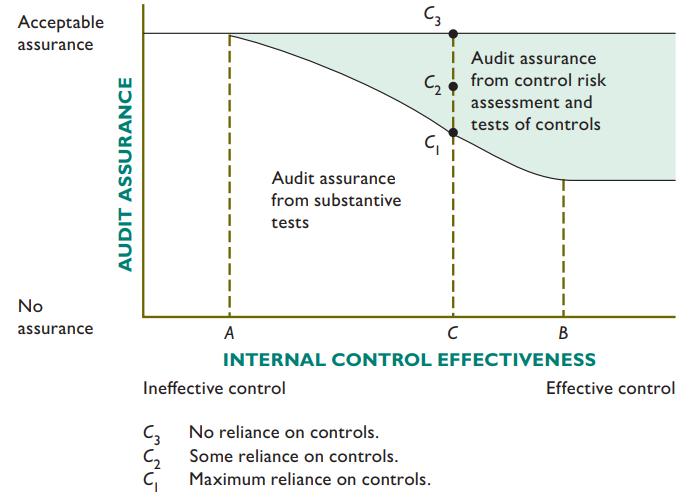

Following are evidence decisions for the three audits described in Figure 13-4 on page 426: Audit A Ineffective client internal controls Audit B Very effective client internal controls Audit C Somewhat effective client internal controls.Evidence Decisions 1. The auditor decided it was possible

The following questions concern the overall audit strategy and audit program, including selection of the type of test to perform. Choose the best response. a. In the financial statement audit of a nonpublic company, the auditor decides to perform tests of the controls related to the occurrence

The following questions deal with tests of controls. Choose the best response. a. To support the auditor’s initial assessment of control risk below maximum, the auditor performs procedures to determine that internal controls are operating effectively. Which of the following audit procedures

How might the performance of test of controls provide evidence related to the presentation transaction-related audit objective?

List the nine balance-related audit objectives in the verification of the ending balance in inventory and provide one useful audit procedure for each of the objectives.

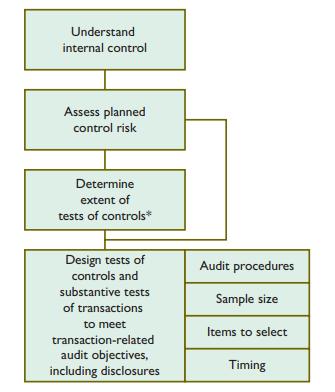

Explain the relationship between the methodology for designing tests of controls and substantive tests of transactions in Figure 13-5 (p. 429) and the methodology for designing tests of details of balances in Figure 13-7. Figure 13-5Figure 13-7 Understand internal control Assess planned

Section 404(a) of the Sarbanes–Oxley Act requires management of a public company to issue a report on internal control over financial reporting (ICOFR) as of the end of the company’s fiscal year. Visit the website for MetLife (www.metlife.com) and search for the 2017 annual report under

AU-C 265, “Communicating Internal Control Related Matters Identified in an Audit,” provides guidance to auditors on communicating deficiencies in internal control to management and those charged with governance when performing an audit under AICPA auditing standards. Visit the AICPA website

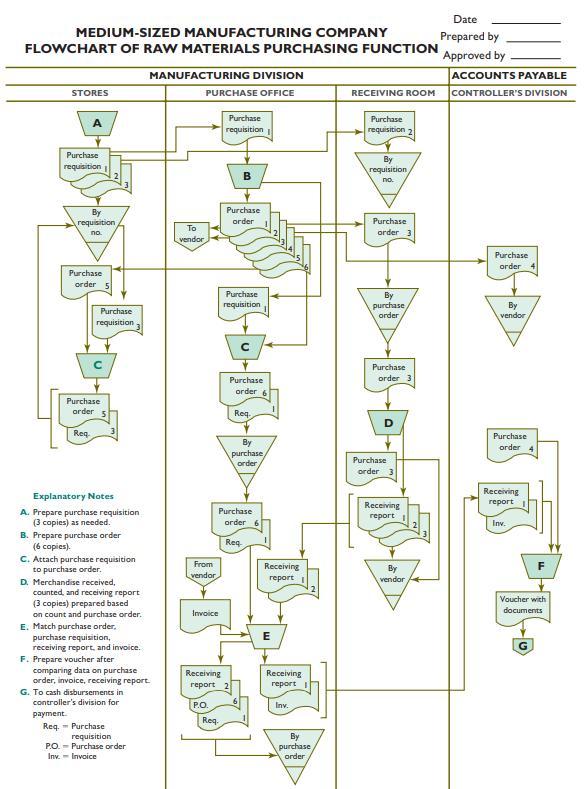

Anthony Liu, CPA, prepared the flowchart on the next page that portrays the raw materials purchasing function of one of Anthony’s clients, Medium-Sized Manufacturing Company, from the preparation of initial documents through the vouching of invoices for payment in accounts payable. Assume that

Internal controls 1 through 5 were tested in prior audits. Evaluate each internal control independently and determine which controls must be tested in the current year’s audit of the December 31, 2019, financial statements. Be sure to explain why testing is or is not required in the current

The following internal controls were identified by the auditor while gaining an understanding of internal control for the sales cycle. 1. Access to the customer master file is restricted to authorized personnel. Customers are added to the master file only after appropriate approval, including

Siva Kumar and Vera Collier are friends who are employed by different CPA firms. One day during lunch they are discussing the importance of internal control in determining the amount of audit evidence required for an engagement. Kumar expresses the view that internal control must be evaluated

The following are general questions about assessing control risk, testing controls, and reporting on internal controls. Choose the best response. a. During the planning stage of an audit, the auditor initially assessed both inherent risk and control risk at a high level. Further testing of the

The following questions concern auditing IT systems. Choose the best response. a. As general IT controls weaken, the auditor is most likely to (1) Reduce testing of automated application controls done by the computer. (2) Increase testing of general IT controls to conclude whether

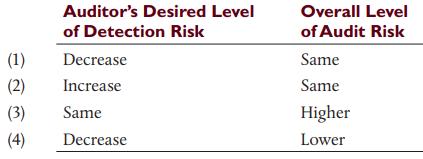

The following questions deal with assessing control risk in a financial statement audit. Choose the best response. a. On the basis of audit evidence gathered and evaluated, an auditor decides to increase assessed control risk from that originally planned. To achieve an audit risk level (AcAR)

Explain what is meant by auditing through the computer, and describe the challenges and benefits of this approach in an audit of a client that uses IT extensively to process accounting information.

The SEC issues Accounting and Auditing Enforcement Releases (AAERs) summarizing SEC actions concerning civil lawsuits brought by the SEC in federal court and related settlements from administrative proceedings. Visit the SEC’s website (www.sec.gov) and locate the link to Accounting and Auditing

The following are general questions about internal control. Choose the best response. a. Which of the following situations is not an example of an inherent limitation of internal control? (1) A programming error in the design of an automated control allows an employee to give himself an

Explain how the effectiveness of general controls impacts the effectiveness of automated application controls.

What is the primary focus of the monitoring component of internal control?

What is meant by the control environment? What is the relationship between the control environment and the other four components of internal control?

The following audit procedures are included in the audit program of Holland Equipment, Inc. 1. Use audit software to examine journal entries in the sales, cash receipts, purchases, cash disbursements, payroll, and general journals for any amounts exceeding $1 million and for any entries with

Public companies are required to file restated financial statements with the SEC when they discover after the audited financial statements have been issued that the financial statements are materially misstated. The misstatements may have been the result of fraudulent actions on the part of

The Art Appreciation Society operates a museum for the benefit and enjoyment of the community. When the museum is open to the public, two clerks who are positioned at the entrance collect a $10.00 admission fee from each nonmember patron. Members of the Art Appreciation Society are permitted

The following questions concern auditor responsibilities related to the identification and assessment of fraud risk. Choose the best response. a. While performing a preliminary assessment for a new client audit, the auditor determines that the client has had excessive growth over the past

The following questions address fraud risks in specific audit areas and accounts. a. Which of the following internal controls will best detect the theft of valuable items from an inventory that consists of hundreds of different items selling for $1 to $10 and a few items selling for hundreds

The following questions address fraud risk factors and the assessment of fraud risk. a. Which action regarding fraud is an activity related to performance of risk assessment procedures? (1) Document the results of procedures used to address the risk of fraud. (2) Discussions among

Whitehead, CPA, is planning the audit of a newly obtained client, Henderson Energy Corporation, for the year ended December 31, 2019. Henderson Energy is regulated by the state utility commission, and because it is a publicly traded company the audited financial statements must be filed with the

This problem is based on the JA Tires data that was first introduced in problem 6-35. If you have not already accessed the data, it can be downloaded from the textbook website. As part of risk assessment procedures, you have been asked to perform some preliminary data analytics on the sales file to

Mark Hopper is planning the audit of the investments account for audit client Garden Supply Co. (GSC). GSC invests excess cash at the end of the summer sales season through an investment manager who invests in equity and debt securities for GSC’s account. Hopper has assessed the following risks

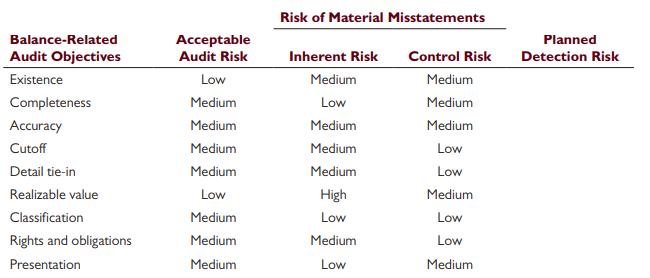

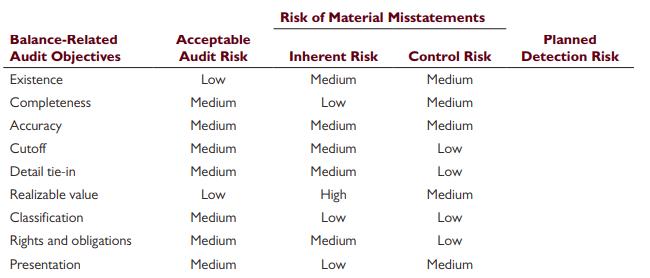

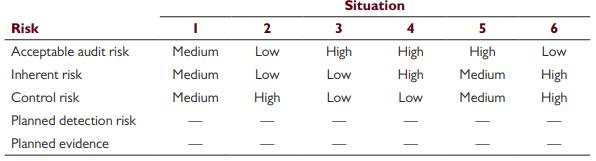

Following are six situations that involve the audit risk model as it is used for planning audit evidence requirements in the audit of inventory. Required:a. Explain what low, medium, and high mean for each of the four risks and planned evidence. b. Fill in the blanks for planned detection

Listed below are various risks identified during audit planning that you have been asked to evaluate to assess whether they are significant risks. 1. Fernandez Wholesalers sells energy drinks to various distributors. As they have expanded sales to additional customers, there has been some increase

This problem requires you to access PCAOB Auditing Standard AS 2110, Identifying and Assessing Risks of Material Misstatements (pcaobus.org). Use this standard to answer each of the questions below. For each answer, document the paragraph(s) in AS 2110 supporting your answer. Required:a. What

The following questions concern auditor responsibilities related to the assessment of risks of material misstatement. Choose the best response. a. Which of the following procedures would a CPA most likely perform during the planning stage of the audit? (1) Evaluate the reasonableness of

Define what is meant by inherent risk. Identify four factors that are associated with higher inherent risk in audits.

This problem requires the use of ACL software, which can be accessed through the textbook website. Information about downloading and using ACL and the commands used in this problem can also be found on the textbook website. You should read all of the reference material preceding the instructions

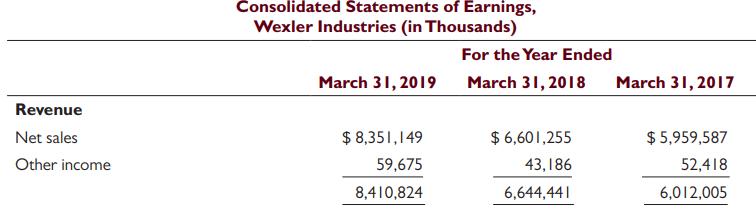

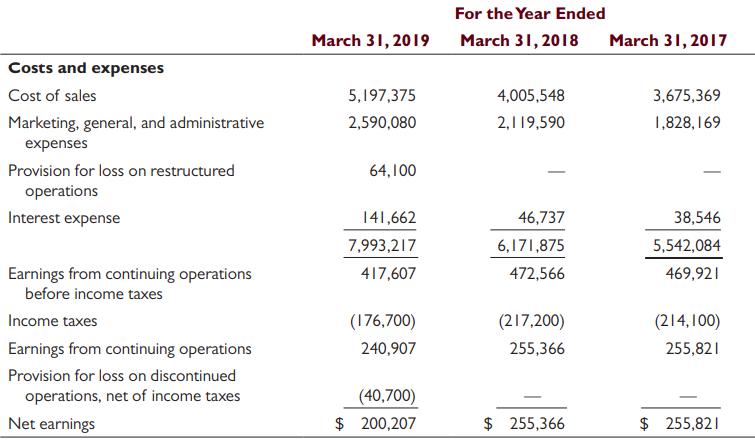

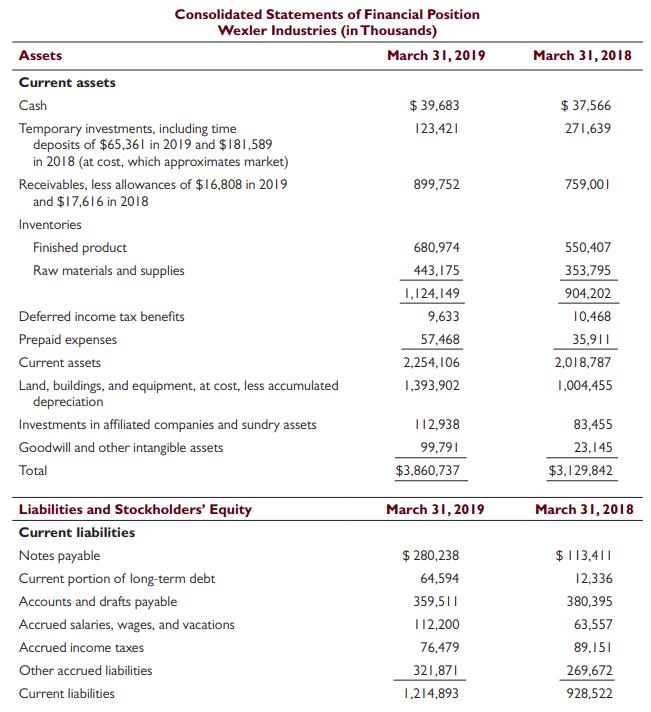

Following are statements of earnings and financial position for Wexler Industries. Required:a. Use professional judgment in deciding on the preliminary judgment about materiality for earnings, current assets, current liabilities, and total assets. Your conclusions should be stated in terms of

In the audit of the Worldwide Wholesale Company, you did extensive ratio and trend analysis as part of preliminary audit planning. Your analytical procedures identified the following: 1. Commission expense as a percent of sales was constant for several years but has increased significantly in

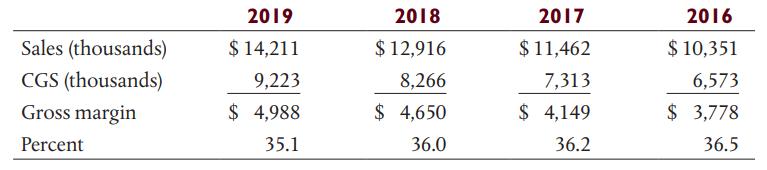

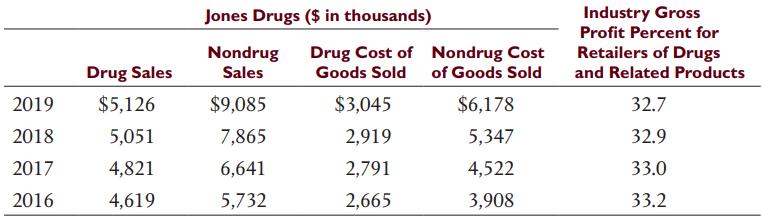

Your comparison of the gross margin percent for Jones Drugs for the years 2016 through 2019 indicates a significant decline. This is shown by the following information: A discussion with Tanvi Anand, the controller, brings to light two possible explanations. She informs you that the industry

Your audit firm was recently engaged to conduct the financial statement audit for BBH Automotive, an original equipment manufacturer (OEM) in the automotive industry. As the senior manager on the engagement, you are performing initial audit planning and developing an understanding of BBH’s

The following questions deal with client acceptance, audit planning, and materiality. Choose the best response. a. In which of the following circumstances would an auditor of an issuer be least likely to reevaluate established materiality levels? (1) The materiality level was established

Assume a company with the following balance sheet accounts: You are concerned only about overstatements of owner’s equity. Set performance materiality for the three relevant accounts such that the preliminary judgment about materiality does not exceed $5,000. Justify your answer. Account

Assume that Xinran Wang, CPA, is using 5 percent of net income before taxes, current assets, or current liabilities as her major guideline for evaluating materiality. What qualitative factors should she also consider in deciding whether misstatements may be material?

Gale Gordon, CPA, has found ratio and trend analysis relatively useless as a tool in conducting audits. For several engagements, he computed the industry ratios for his clients and compared them with industry averages. For most engagements, the client’s business was significantly different from

In recent years, globalization of business and factors such as technological disruption, tax reform, trade policies, and changing demographics in the workforce cause uncertainty and volatility in stock and bond markets. Why might it be important for you to consider current economic and other events

Regulators are taking advantage of advances in technology to fulfill their oversight responsibilities. Visit the website of the Securities and Exchange Commission (SEC) (www.sec.gov) to locate the speech given at the OpRisk North America 2017 Conference by Scott W. Bauguess, Acting Director and

As the in-charge senior auditor on the audit engagement for JA Tire Manufacturing for the year ended December 31, 2019, you are responsible for performing risk assessment procedures related to the sales cycle. JA Tire has four sales divisions within the U.S. and sells primarily to large tire

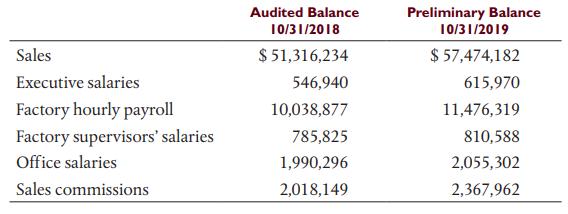

You are auditing payroll for the Morehead Technologies company for the year ended October 31, 2019. Included next are amounts from the client’s trial balance, along with comparative audited information for the prior year. You have obtained the following information to help you perform

This problem requires the use of ACL software, which can be accessed by following the instructions available on the textbook website. Information about downloading and using ACL and the commands used in this problem can also be found on the textbook website. You should read all of the reference

The following are examples of documentation typically obtained by auditors: 1. Duplicate sales invoices 2. Receiving reports 3. Minutes of the board of directors 4. Signed W-4s 5. Subsidiary accounts receivable records 6. Vendors’ invoices 7. General ledgers 8. Title

The following questions concern audit evidence and audit documentation. Choose the best response. a. According to PCAOB audit standards, audit documentation must be retained for b. Which of the following types of audit evidence is generally the most reliable? (1) One year. (2)

Showing 100 - 200

of 537

1

2

3

4

5

6

Step by Step Answers