New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

business statistics communicating

Statistics For Business And Economics 10th Edition David R. Anderson, Dennis J. Sweeney, Thomas A. Williams - Solutions

24. LO.1, 6 To which of the following tax-exempt organizations may the UBIT apply?a. Red Cross.b. Salvation Army.c. United Fund.d. College of William and Mary.e. Rainbow, Inc., a private foundation.f. Louisiana State University.g. Colonial Williamsburg Foundation.h. Federal Land Bank.i. University

23. LO.6, 8 Second Church is going to operate a gift shop and bookshop that will include only religious articles in its inventory. The shop will be staffed by employees who are not church members. These employees will be paid the minimum wage except for the gift shop and bookshop manager, whose

22. LO.6 An exempt municipal hospital operates a pharmacy that is staffed by a pharmacist 24 hours per day. The pharmacy serves only hospital patients. Is the pharmacy an unrelated trade or business?

21. LO.6 What type of activity by a church is likely to be subject to the unrelated business income tax? What factors must be present for this activity to be classified as an unrelated trade or business?

20. LO.6 Less, Inc., a § 501(c)(3) organization, has unrelated business taxable income of$600,000 and total earnings of $1 million. Why is only the $600,000 subject to Federal income tax? What is the Federal income tax liability?

19. LO.6 Winston recently became the treasurer of Homeless, Inc., a § 501(c)(3) organization that feeds the homeless. One of the entity’s directors has proposed that Homeless purchase and operate a fast-food franchise as part of Homeless, Inc., to raise additional revenue (a projected increase

18. LO.4, 5 Really Welcome, Inc., a tax-exempt organization, receives 30% of its support from disqualified persons. Another disqualified person has agreed to match this support if Really Welcome will appoint him to the organization’s board of directors. What tax issues are relevant to Really

17. LO.5 Sunset, Inc., a § 501(c)(3) exempt organization that is classified as a private foundation, generates investment income of $600,000 for the current tax year. This amount represents 20% of Sunset’s total income.a. What type of tax is imposed on Sunset associated with its investment

16. LO.5What types of taxes may be levied on a private foundation? Why are the taxes levied?

15. LO.4 Describe the external support test and the internal support test for a private foundation.

14. LO.4 Which of the following exempt organizations could be private foundations?a. Bruton Parish Episcopal Church.b. Our Lady Catholic Church.c. Port Allen Community Hospital.d. National Football League (NFL).e. Southeastern Louisiana University Alumni Association.f. United Fund.g. Lee’s

13. LO.4, 5 What is a private foundation? What are the disadvantages of an exempt organization being classified as a private foundation?

12. LO.3 What types of activities are not subject to the tax imposed on feeder organizations?

11. LO.3 Service, Inc., an exempt organization, owns all of the stock of Blue, Inc., a retailer of boating supplies. Blue remits all of its profits to Service. According to a policy adopted by Service’s board, 60% of the amount received from Blue is to be spent annually in carrying out

10. LO.3 The IRS can impose intermediate sanctions on a public charity if its gross unrelated business income exceeds 50% of its gross income or if less than two-thirds of its net unrelated business income is used in carrying out its tax-exempt mission. Evaluate this statement.

9. LO.3 Under what circumstances can an exempt organization engage in lobbying activities?What types of exempt organizations are eligible for this treatment?

8. LO.3 Can a church make an election that will enable it to engage in lobbying on a limited basis without incurring any negative tax consequences? Explain.

7. LO.3 Good, Inc., a § 501(c)(3) exempt organization, engages in a § 503 prohibited transaction. What negative tax consequences may be associated with Good engaging in a§ 503 prohibited transaction?

6. LO.3 Walter contributes $3,000 to an exempt organization. Addie contributes $3,000 to a different exempt organization. Why might Addie be permitted a $3,000 charitable contribution deduction in calculating her itemized deductions when Walter is not?

5. LO.2 What are the common characteristics shared by many exempt organizations?

4. LO.1 Identify the statutory authority under which each of the following is exempt from Federal income tax.a. Kingsmill Country Club.b. Shady Lawn Cemetery.c. Amber Credit Union.d. Veterans of Foreign Wars.e. Boy Scouts of America.f. United Fund.g. Federal Deposit Insurance Corporation.h. Bruton

3. LO.1 Which of the following organizations qualify for exempt status?a. Tulane University (a private university).b. Virginia Qualified Tuition Program.c. Red Cross.d. Disneyland.e. Ford Foundation.f. Houston Chamber of Commerce.g. Colonial Williamsburg Foundation.h. Professional Golfers

2. LO.1 Why are certain organizations either partially or completely exempt from Federal income tax?

1. LO.1, 6 Eggshell, Inc., a C corporation, operates a rental clothing store, and its profits are subject to double taxation. First Church of the States operates a retail gift shop and bookshop and is not subject to taxation. What is the explanation for this difference in Federal income tax

3. Outline the Treasury Department’s tax reform proposal to treat passthrough entities as corporations. Summarize your findings in an e-mail to your instructor.

2. Sam is selling his S corporation, Superbody Fitness, Inc. He will receive 80% cash and 20% of another S corporation fitness center. As part of this transaction, should Sam liquidate Superbody Fitness? Outline your analysis in an e-mail to your instructor.

1. Bushong, Inc., a calendar year S corporation, has a “tax cash-flow” provision in its shareholder agreement. Bushong must make annual distributions by the December 31 following a tax year in which there is an income pass-through. Each distribution must be in an amount sufficient to enable

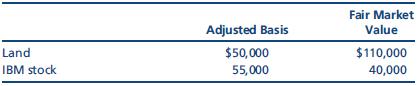

52. LO.10 Blue Corporation elects S status effective for calendar year 2011. As of January 1, 2011, Blue holds two assets.Blue sells the land in 2012 for $120,000. Calculate Blue’s recognized built-in gain, if any, in 2012. Land IBM stock Adjusted Basis $50,000 55,000 Fair Market Value $110,000

51. LO.11 Ruby is the owner of all of the shares of an S corporation. Ruby is considering receiving a salary of $80,000 from the business. She will pay 7.65% FICA taxes on the salary, and the S corporation will pay the same amount of FICA tax. If Ruby reduces her salary to $40,000 and takes an

50. LO.11 Friedman, Inc., an S corporation, holds some highly appreciated land and inventory and some marketable securities that have declined in value. It anticipates a sale of these assets and a complete liquidation of the company over the next two years.Arnold Schwartz, the CFO, calls you,

49. LO.5, 6, 11 Bonnie and Clyde each own one-third of a fast-food restaurant, and their 13-year-old daughter owns the other shares. Both parents work full-time in the restaurant, but the daughter works infrequently. Neither Bonnie nor Clyde receives a salary during the year, when the ordinary

48. LO.4, 10, 11 Sweetwater, Inc., is an S corporation in Sour Lake, Texas.a. In 2012, Sweetwater’s excess net passive income is $42,000. Sweetwater holds $31,000 of accumulated earnings and profits from a C corporation year. It reports $58,000 of taxable income and AMT adjustments of $17,000 for

47. LO.10 Rodeo, Inc., a cash basis S corporation in College Station, Texas, formerly was a C corporation. Rodeo records the following assets and liabilities on January 1, 2012, the date its S election is made.During 2012, Rodeo collects the accounts receivable and pays the accounts payable. The

46. LO.5, 6, 8 Emeline, Inc., of Auburn, Alabama, is an accrual basis S corporation with three equal shareholders. The three cash basis shareholders have the following stock basis at the beginning of the year: Andre, $12,000; Crum, $22,000; and Barbara, $31,000.Emeline reports the following income

45. LO.5, 6, 8, 9 A calendar year S corporation has an ordinary loss of $80,000 and a capital loss of $20,000. Ms. Freiberg owns 30% of the corporate stock and has a $24,000 basis in her stock. Determine the amounts of the ordinary loss and capital loss, if any, that flow through to Ms. Freiberg.

44. LO.6, 9 In Problem 43, how much of the Whitman loss belongs to Ann and Becky?Becky’s stock basis is $41,300.

43. LO.6, 9 At the beginning of the year, Ann and Becky own equally all of the stock of Whitman, Inc., an S corporation. Whitman generates a $120,000 loss for the year (not a leap year). On the 189th day of the year, Ann sells her half of the Whitman stock to her son, Scott. How much of the

42. LO.5, 6, 11 Red Lion, Inc., is an S corporation with a sizable amount of AEP from a C corporation year. The S corporation has $400,000 of investment income and $400,000 of investment expense in 2012. The company makes cash distributions to enable its sole shareholder to pay her taxes. What are

41. LO.8 Assume the same facts as in Problem 39, except that Jeff’s share of corporate taxable income is only $8,000 and there is no distribution. However, the corporation repays the $10,000 loan principal to Jeff. Discuss the tax effects. Assume that there was no corporate note (i.e., only an

40. LO.8 Assume the same facts as in Problem 39, except that there is no $15,000 distribution but the corporation repays the loan principal to Jeff. Discuss the tax effects.

39. LO.8 Jeff, a 52% owner of an S corporation, has a stock basis of zero at the beginning of the year. Jeff’s basis in a $10,000 loan made to the corporation and evidenced by a corporate note has been reduced to zero by pass-through losses. During the year, his net share of the corporate taxable

38. LO.8, 9 Assume the same facts as in Problem 37, except that a Reg. § 1.1367–1(g) election is made. How does your answer change?

37. LO.8, 9 At the beginning of 2011, Christine Wheat has a basis of $5,000 in her stock of a calendar year S corporation, Zhou, Inc. She holds no debt of the S corporation. During 2011, Wheat’s total share of Zhou’s losses and deductions is $16,000, consisting of$10,000 of ordinary loss and

36. LO.6, 7, 8 Assume the same facts as in Problem 35, except that the two shareholders consent to an AAA bypass election.

35. LO.6, 7, 8 Money, Inc., a calendar year S corporation in Denton, Texas, has two unrelated shareholders, each owning 50% of the stock. Both shareholders have a $400,000 stock basis as of January 1, 2012. At the beginning of 2012, Money has an AAA of$300,000 and AEP of $600,000. During 2012,

34. LO.6 Peres, Inc., a calendar year S corporation, holds an AAA balance of $767,050 at the beginning of 2012. During the year, the following items are recorded.Sales income $206,000 Loss from real estate operation (5,000)Officers’ life insurance proceeds 100,000 Premiums paid for officers’

33. LO.6 If the beginning balance in Strauder, Inc.’s OAA is $5,700 and the following transactions occur, what is Strauder’s ending OAA balance?Depreciation recapture income $22,700 Payroll tax penalty (4,200)Tax-exempt interest income 4,995 Nontaxable life insurance proceeds 50,000 Life

32. LO.6 Lonergan, Inc., a calendar year S corporation in Athens, Georgia, had a balance in AAA of $200,000 and AEP of $110,000 on December 31, 2012. During 2013, Lonergan, Inc., distributes $140,000 to its shareholders, while sustaining an ordinary loss of$120,000. Calculate the balance in

31. LO.6, 8, 9, 11 In 2012, Spence, Inc., a calendar year S corporation, generates an ordinary loss of $110,000 and makes a distribution of $140,000 to its sole shareholder, Storm Nelson. Nelson’s stock basis at the beginning of the year is $200,000. Write a memo to your senior manager, Aaron

30. LO.6, 7, 8 Tiger, Inc., a calendar year S corporation, is owned equally by four shareholders:Ann, Becky, Chris, and David. Tiger owns a piece of investment land that was purchased for $160,000 four years ago. On September 14, 2012, when the land is worth$240,000, it is distributed to David.

29. LO.5, 6 McLin, Inc., is a calendar year S corporation. Its AAA balance is zero.a. McLin holds $90,000 of AEP. Tobias, the sole shareholder, has an adjusted basis of$80,000 in his stock. Determine the tax aspects if a $90,000 salary is paid to Tobias.b. Same as part (a), except that McLin pays

28. LO.6 Noon, Inc., a calendar year S corporation, is equally owned by Ralph and Thomas. Thomas dies on April 1 (not a leap year), and his estate selects a March 31 fiscal year. Noon has $400,000 of income for January 1 through March 31 and $600,000 for the remainder of the year.a. Determine how

27. LO.6, 8, 9 Betty is a shareholder in a calendar year S corporation. At the beginning of the year, her stock basis is $10,000, her share of the AAA is $2,000, and her share of corporate AEP is $6,000. She receives a $6,000 distribution, and her share of S corporation items includes a $2,000

26. LO.5, 6 Who, Inc., is a calendar year S corporation. Who’s book income this year totals$172,000. Who is owned equally by four shareholders. From supplemental data, you obtain the following information about items included in book income.Tax-exempt interest income $ 3,200 Dividends received

25. LO.5, 6 Saul, Inc., a calendar year S corporation, incurred the following items.Tax-exempt bond interest income $ 7,000 Sales 130,000 Depreciation recapture income 12,000 Short-term capital gain 30,000§1231 gain 12,000 Cost of goods sold (42,000)Administrative expenses (15,000)Depreciation

24. LO.5, 6 A calendar year S corporation’s profit and loss statement shows net profits of$90,000 (book income). The corporation is owned equally by three shareholders. From supplemental data, you obtain the following information about items included in the book income.Tax-exempt interest income

23. LO.11 How does the alternative minimum tax affect an S corporation? Its shareholders?

22. LO.11 How can an S corporation avoid the passive investment income tax?

21. LO.1, 11 One of your clients is considering electing S status. Texas, Inc., is a six-yearold company with two equal shareholders, both of whom paid $30,000 for their stock.Going into 2012, Texas has a $110,000 NOL carryforward from prior years. Estimated income is $40,000 for 2012 and $25,000

20. LO.9 Sheila Jackson is a 50% shareholder in Washington, Inc., an S corporation. This year, Jackson’s share of the Washington loss is $100,000. Jackson has income from several other sources. Identify at least four tax issues related to the effects of the S corporation loss on Jackson’s tax

19. LO.8 For each of the following independent statements, indicate whether the transaction will increase (+), decrease (−), or have no effect (NE) on the adjusted basis of a shareholder’s stock in an S corporation.a. Expenses related to tax-exempt income.b. Short-term capital gain.c.

18. LO.6, 8 Scott Tyrney owns 21% of an S corporation. He is confused with respect to the amounts of the corporate AAA and his stock basis. Write a brief memo to Scott identifying the key differences between AAA and an S corporation stock basis.

17. LO.6, 11 Collette’s S corporation has a small amount of accumulated earnings and profits (AEP), requiring the use of the more complex distribution rules. Collette’s accountant tells her that this AEP forces maintenance of the AAA figure each year. Identify relevant tax issues facing

16. LO.6 Using the categories in the following legend, classify each transaction as a plus(+) or minus (−) on Schedule M–2 of Form 1120S. An answer might look like one of these: “+AAA” or “−OAA.”Legend AAA = Accumulated adjustments account OAA = Other adjustments account NA = No

15. LO.5 Indicate whether each of the following items is available to an S corporation.a. Amortization of organizational expenditures.b. Dividends received deduction.c. Standard deduction.d. Personal exemption.e. Section 179 expense deduction.

14. LO.4 Caleb Samford calls you and says that his two-person S corporation was involuntarily terminated in February 2011. He asks you if they can make a new S election now, in November 2012. Draft a memo for the file outlining what you told Caleb.

13. LO.2, 3 On March 2, 2012, the two 50% shareholders of a calendar year corporation decide to elect S status. One of the shareholders, Terry, purchased her stock from a previous shareholder (a nonresident alien) on January 18, 2012. Identify any potential problems for Terry or the corporation.

12. LO.2, 11 Bob Roman, the major owner of an S corporation, approaches you for some tax planning help. He would like to exchange some real estate in a like-kind transaction under § 1031 for other real estate that may have some environmental liabilities. Prepare a letter to Bob outlining your

11. LO.2 Which of the following can be a shareholder of an S corporation?a. Resident alien.b. Partnership.c. Charitable remainder trust.d. IRA.e. Estate.f. One-person LLC (disregarded entity).

10. LO.2 Which, if any, of these items would be considered a second class of stock for an S corporation?a. Short-term unwritten advances from a shareholder that do not exceed $10,000 in the aggregate at any time during the corporation’s taxable year.b. Debt that is held by shareholders in the

9. LO.2 Outline the characteristics of an S corporation’s straight debt.

8. LO.2 Which, if any, of these items would be considered a second class of stock for an S corporation?a. Voting preferred stock (with a preference on dividends).b. Treasury stock of another class.c. Phantom stock.d. Unexercised stock options.e. Warrants.f. Stock appreciation rights.g. Convertible

7. LO.2 What requirements must an entity meet to elect S corporation status?

6. LO.2 What is a qualified S corporation subsidiary (QSSS)? Elaborate.

5. LO.2 Which of the following are requirements to be an S corporation?a. Only one class of stock.b. Cannot have an estate as a shareholder.c. Cannot use a phantom stock plan.d. Cannot be a foreign corporation.e. Cannot have a resident alien.

4. LO.1 How can a C corporation mitigate its double taxation potential?

3. LO.1 Explain how the net operating loss rules apply to a new S corporation. To a new C corporation.

2. LO.1 The alternative minimum tax applies to an S corporation. Discuss the validity of this statement.

1. LO.1 Which of these characteristics are found with an S corporation?a. Limited liability to shareholder.b. Personal holding company.c. Liabilities affect the owner’s basis.d. Distributions of appreciated property are taxable at the corporate level.e. Treated as a corporation under state laws.

3. Use the search feature on your favorite news site on the Web (e.g., CNN, ABC News, or Fox News) and search for news on partnerships, LLCs, or limited partnerships. What entities did you find that are taking advantage of the partnership entity form? (Make sure these entities are truly legal

2. Barney, an individual, and Aldrin, Inc., a domestic C corporation, have decided to form BA, LLC. The new LLC will produce a product that Barney recently developed and patented. Barney and Aldrin, Inc., will each own a 50% capital and profits interest in the LLC. Barney is a calendar year

1. Your clients, Grayson Investments, Inc. (Ana Marks, President), and Blake Caldwell, each contributed $200,000 of cash to form the Realty Management Partnership, a limited partnership. Grayson is the general partner, and Blake is the limited partner. The partnership used the $400,000 of cash to

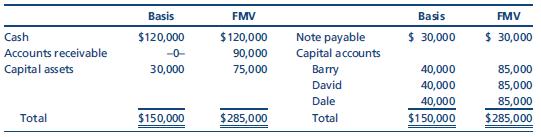

68. LO.15 RBP Partnership is a service-oriented partnership that has three equal general partners. One of them, Barry, sells his interest to another partner, Dale, for $90,000 of cash and the assumption of Barry’s share of partnership liabilities. On the sale date, the partnership’s cash basis

67. LO.14 In each of the following independent liquidating distributions in which the partnership also liquidates, determine the amount and character of any gain or loss to be recognized by each partner and the basis of each asset (other than cash) received. In each case, assume that distributions

66. LO.14 At the beginning of the tax year, Monica’s basis in the MIP LLC was $100,000, including Monica’s $50,000 share of the LLC’s liabilities. At the end of the year, MIP distributed to Monica cash of $20,000 and inventory (basis of $10,000, fair market value of$16,000). In addition, MIP

65. LO.14 Mark’s basis in his partnership interest is $39,000. In a proportionate nonliquidating distribution, Mark receives $30,000 of cash and two inventory items, each with a basis of $10,000 to the partnership. The values of the inventory items are $15,000 and$5,000.a. How much gain or loss,

64. LO.14 In each of the following independent cases in which the partnership owns no hot assets, indicate:• Whether the partner recognizes gain or loss.• Whether the partnership recognizes gain or loss.• The partner’s adjusted basis for the property distributed.• The partner’s outside

63. LO.14 When Melanie’s outside basis in the TMF Partnership is $200,000, the partnership distributes to her $40,000 of cash, an account receivable (fair market value of$80,000, inside basis to the partnership of $0), and a parcel of land (fair market value of$200,000, inside basis to the

62. LO.14 Greg’s outside basis in his interest in the GO Partnership is $360,000. In a proportionate nonliquidating distribution, the partnership distributes to him cash of$60,000, inventory (fair market value of $200,000, basis to the partnership of $160,000), and land (fair market value of

61. LO.13 Four GRRLs Partnership is owned by four sisters. Leah holds a 70% interest;each of the others owns 10%. Leah sells investment property to the partnership for its fair market value of $100,000 (Leah’s basis is $150,000).a. How much loss, if any, may Leah recognize?b. If the partnership

60. LO.7, 13 Nicole, a calendar year individual, owns 30% of Creole Cravings, Inc., a C corporation that was formed on February 1, 2012. She receives a $5,000 monthly salary from the corporation, and Creole Cravings generates $200,000 of taxable income (after accounting for payments to Nicole) for

59. LO.13 Continue with the facts presented in Problem 58. Assume that Burgundy, Inc.’s annual guaranteed payment is increased to $120,000 starting on January 1, 2013, and the LLC’s taxable income for 2012 and 2013 (after deducting Burgundy’s guaranteed payment)is the same (i.e., $80,000 and

58. LO.13 Burgundy, Inc., and Violet are equal partners in the calendar year BV, LLC.Burgundy uses a fiscal year ending April 30, and Violet uses a calendar year. Burgundy receives an annual guaranteed payment of $100,000 for use of capital contributed by Burgundy. BV’s taxable income (after

57. LO.10, 12 Jasmine Gregory is a 20% member in Sparrow Properties, LLC, which is a lessor of residential rental property. Her share of the LLC’s losses for the current year is$100,000. Immediately before considering the deductibility of this loss, Jasmine’s capital account (which, in this

56. LO.9, 10, 12, 17 The BCD Partnership plans to distribute cash of $20,000 to partner Brad at the end of the tax year. The partnership reported a loss for the year, and Brad’s share of the loss is $10,000. At the beginning of the tax year, Brad’s basis in his partnership interest, including

55. LO.3, 9, 10 Paul and Anna plan to form the PA General Partnership by the end of the current year. The partners will each contribute $80,000 of cash, and in addition, the partnership will borrow $240,000 from First State Bank. The $400,000 will be used to buy an investment property. The property

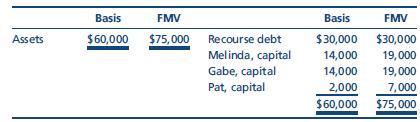

54. LO.10 The MGP General Partnership was created on January 1 of the current year by having Melinda, Gabe, and Pat each contribute $10,000 cash to the partnership in exchange for a one-third interest in partnership income, gains, losses, deductions, and credits. On December 31 of the current year,

53. LO.7, 9, 12 Continue with the facts presented in Problem 52. On the first day of the third tax year, the partnership sold the equipment for $150,000 and distributed the cash in accordance with the partnership agreement. The partnership was liquidated at this time.a. Calculate the partners’

52. LO.3, 7, 9, 12 Bryan and Cody each contributed $120,000 to the newly formed BC Partnership in exchange for a 50% interest. The partnership used the available funds to acquire equipment costing $200,000 and to fund current operating expenses. The partnership agreement provides that depreciation

51. LO.3, 7, 9, 10 Continue with the facts presented in Problem 49, except that Suz-Anna was formed as an LLC instead of a general partnership.a. How would Suz-Anna’s ending liabilities be treated?b. How would Suzy’s basis and amount at risk be different?

Showing 2700 - 2800

of 7675

First

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

Last

Step by Step Answers