New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

equity asset valuation

Managing Investment Portfolios A Dynamic Process Workbook 1st Edition John L. Maginn, Donald L. Tuttle, Dennis W. McLeavey, Jerald E. Pinto - Solutions

10. A trader decided to sell 30,000 shares of a company. At the time of this decision, the quoted price was ¤53.20 to ¤53.30. Because of the large size of the order, the trader decided to execute the sale in three equal orders of 10,000 shares spread over the course of the day. When she placed

9. A client of a broker evaluates the broker’s performance by measuring transaction costs with a specified price benchmark. The broker has discretion over the timing of his trades for the client. Discuss what the broker could do to make his performance look good to the client (even though the

8. Able Energy, Inc., is a company listed on NASDAQ (symbol: ABLE). A trader sold 100 shares of this company onMay 10, 2004 at 15:52:59 at a price of $2.66 per share. All the trades that occurred in Able Energy on that day are listed below.Time Trade Price ($) Shares Traded 10:00:39 2.71 200

7. An asset management firm wants to purchase 500,000 shares of a company. It decides to shop the order to various broker/dealer firms to see which firm can offer the best service and lowest cost. Discuss the potential negatives of shopping the order.

6. A portfolio manager would like to buy 5,000 shares of a very recent initial public offering(IPO) stock. However, he was not able to get any shares at the IPO price of £30. The portfolio manager would still like to have 5,000 shares, but not at a price above £45 per share. Should he place a

5. An investment manager placed a limit order to buy 500,000 shares of Alpha Corporation at $21.35 limit at the opening of trading on February 8. The closing market price of Alpha Corporation on February 7 was also $21.35. The limit order filled 40,000 shares, and the remaining 460,000 shares were

4. For each of the following, discuss which of the two orders in shares of Sunny Corporation will have a greater market impact. Assume that all other factors are the same.A. i. An order to buy 5,000 shares placed by a trader on the NYSE.ii. An order to buy 50,000 shares placed by the same trader on

3. E-Crossnet is an electronic crossing network that operates in Europe. It runs a total of 14 crosses every day at half-hour intervals. After a cross is run, there are some stocks for which there are unmatched buy quantities and some stocks with unmatched sell quantities.Discuss whether E-Crossnet

2. In a report dated December 15, 2004, the Office of Economic Analysis of the U.S.Securities and Exchange Commission (SEC) compared trade execution quality on the NYSE and NASDAQ using a matched sample of 113 pairs of firms. The comparison is based on six months of data from January to June 2004.

1. An analyst is estimating variousmeasures of spread for Airnet Systems, Inc. (NYSE: ANS).On page 98 is a sample of quotes in ANS on the New York Stock Exchange on March 10, 2004, between 10:49:00 and 10:57:00.A buyer-initiated trade in ANS was entered at 10:50:06 and was executed at 10:50:07 at a

18. Following are four methods for calculating risk-adjusted performance: the Sharpe ratio, risk-adjusted return on capital (RAROC), return over maximum drawdown (RoMAD), and the Sortino ratio. Compare and contrast the measure of risk that each method uses.

17. Tony Smith believes that the price of a particular underlying, currently selling at $96, will increase substantially in the next six months, so he purchases a European call option expiring in six months on this underlying. The call option has an exercise price of $101 and sells for $6.A. How

16. Ricardo Col´on, an analyst in the investment management division of a financial services firm, is developing an earnings forecast for a local oil services company. The company’s income is closely linked to the price of oil. Furthermore, the company derives the majority of its income from

15. Indicate which of the following statements about credit risk is (are) false, and explain why:A. Because credit losses occur often, it is easy to assess the probability of a credit loss.B. One element of credit risk is the possibility that the counterparty to a contract will default on an

14. An organization’s 5 percent daily VaR shows a number fairly consistently around ¤3 million. A backtest of the calculation reveals that, as expected under the calculation, daily portfolio losses in excess of ¤3 million tend to occur about once a month. When such losses do occur, however,

13. A. A firm runs an investment portfolio consisting of stocks as well as options on stocks.Management would like to determine the VaR for this portfolio and is thinking about which technique to use. Discuss a problem with using the analytical or variance–covariance method for determining the

12. Consider a $10 million portfolio of stocks. You perform a Monte Carlo simulation to estimate the VaR for this portfolio. You choose to perform this simulation using a normal distribution of returns for the portfolio, with an expected annual return of 14.8 percent and a standard deviation of

11. You invested $25,000 in the stock of Dell Computer Corporation in early 2002. You have compiled the monthly returns on Dell’s stock during the 1997–2001 period, as given below.1997 1998 1999 2000 2001 0.2447 0.1838 0.3664 −0.2463 0.4982 0.0756 0.4067 −0.1988 0.0618 −0.1627−0.0492

10. An analyst would like to know the VaR for a portfolio consisting of two asset classes:long-term government bonds issued in the United States and long-term government bonds issued in the United Kingdom. The expected monthly return on U.S. bonds is 0.85 percent, and the standard deviation is 3.20

9. Suppose you are given the following sample probability distribution of annual returns on a portfolio with a market value of $10 million.Return on Portfolio Probability Less than −50% 0.005 −50% to −40% 0.005 −40% to −30% 0.010 −30% to −20% 0.015 −20% to −10% 0.015 −10% to

8. Each of the following statements about VaR is true except:A. VaR is the loss that would be exceeded with a given probability over a specific time period.B. Establishing a VaR involves several decisions, such as the probability and time period over which the VaR will be measured and the technique

7. A. An organization’s risk management function has computed that a portfolio held in one business unit has a 1 percent weekly VaR of £4.25 million. Describe what is meant in terms of a minimum loss.B. The portfolio of another business unit has a 99 percent weekly VaR of £4.25 million(stated

6. Ford Credit is the branch of Ford Motor Company that provides financing to Ford’s customers. For this purpose, it obtains funding from various sources. As a result of its interest rate risk management process, including derivatives, Ford Credit’s debt reprices faster than its assets. This

5. A large trader on the government bond desk of a major bank loses ¤20 million in a year, in the process reducing the desk’s overall profit to ¤10 million. Senior management, on looking into the problem, determines that the trader repeatedly violated his position limits during the year. They

4. Sue Ellicott supervises the trading function at an asset management firm. In conducting an in-house risk management training session for traders, Ellicott elicits the following statements from traders:• Trader 1. ‘‘Liquidity risk is not a major concern for buyers of a security as opposed

3. NatWest Markets (NWM) was the investment banking arm of National Westminster Bank, one of the largest banks in the United Kingdom. On February 28, 1997, NWM revealed that a substantial loss had been uncovered in its trading books. During the 1990s, NatWest was engaged in trading interest rate

2. Stewart Gilchrist follows the automotive industry, including Ford Motor Company.Based on Ford’s 2003 annual report, Gilchrist writes the following summary:Ford Motor Company has businesses in several countries around the world. Ford frequently has expenditures and receipts denominated in

1. Discuss the difference between centralized and decentralized risk management systems, including the advantages and disadvantages of each.

19. Critique the following statement: ‘‘When the economy has been faltering and may be going into recession, it is typically a good time to invest in distressed securities.’’

18. Formulate a description of the results of a prepackaged bankruptcy with reference to(a) ‘‘prebankruptcy’’ creditors of the company, (b) ‘‘prebankruptcy’’ shareholders, and(c) vulture investors.

17. Evaluate the role of investors in both the private equity and relative-value strategies—specifically, with respect to investing in distressed securities.

16. Contrast ‘‘fallen angels’’ to high-yield debt.

15. List and discuss the sources of return available to managed futures programs through the use of derivative trading strategies.

14. Cassano asks: ‘‘If managed futures strategies are often momentum based, how do they achieve excess returns differently from traditional stock or bond investment vehicles?’’Formulate an answer to Cassano’s question.

13. Andrew Cassano, CIO of a large charitable organization, ismeeting with his senior analyst, Lori Wood, to discuss managed futures. Cassano believes that it would be beneficial to evaluate this alternative investment category before making a final decision with respect to hedge fund

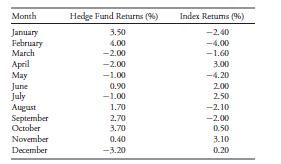

12. A. Compute the annualized downside deviations for the hedge fund and the index, and contrast them to the standard deviation. The annualized standard deviations for the hedge fund and the index are, respectively, 8.64 percent and 9.19 percent.B. Compute the Sortino ratio and, based on this

11. A. Calculate the average rolling returns for the hedge fund if the investor’s investment horizon is nine months.B. Explain how rolling returns can provide additional information about the hedge fund’s performance.

10. Jane Farkas tells Susan DiMarco that she has seen exciting data on the performance of market-neutral, convertible arbitrage, and global macro hedge funds. Farkas states: ‘‘The Sharpe ratios of all of these hedge fund strategies are much higher than for traditional equities or bonds, which

9. Susan DiMarco is evaluating a hedge fund that has a high level of portfolio turnover and a short investment record. The hedge fund makes a contractual stipulation with limited partners regarding a lock-up period that is quite common in the hedge fund industry.A colleague, Jane Farkas, who has

8. Interpret a ‘‘1 and 20’’ fee structure with reference to high-water marks and drawdowns.

7. Ian Parkinson, as chief pension officer of a large defined-benefit plan, is considering presenting a recommendation that the pension plan make its first investments in three different types of hedge funds: (1) market-neutral, (2) convertible arbitrage, and (3) global macro.An analyst who works

6. Explain the practical effects of the following possible characteristics of a hedge fund index:A. Survivorship bias B. Value weighting C. Stale price bias

5. Capital market analysts John Lake and Julie McCoy are reviewing the information in Exhibit 8-2. Lake and McCoy note that the Sharpe ratio for the GSCI is significantly lower than that of the S&P 500 and the Lehman Government/Corporate Bond indices.They also note that the minimummonthly returns

4. RogerGuidry, chief investment officer (CIO) of a university endowment fund, is reviewing investment data related to the endowment’s investment in energy commodities.GSCI Total GSCI Collateral GSCI Roll GSCI Spot Year Annual Return Yield Yield Annual Return 1 29.1% 9.6% ? 6.1%2 −30.5% ?

3. The board trustees of Elite Corporation’s US$50 million pension fund are meeting to discuss a presentation they recently received from their pension consultant, who is recommending that they diversify their current 50/50 stock/bond asset allocation to include a 10 percent allocation to real

2. A. Summarize the major categories of direct and indirect investment in real estate.B. Using the data in Exhibit 8-1, evaluate the historical relative diversification benefits of both forms of investment when added to a 50 percent stock/50 percent bond portfolio. Use the National Council of Real

1. Compare the relative liquidity characteristics of direct versus indirect investment in real estate. Discuss three factors that affect the liquidity of both forms of investment.

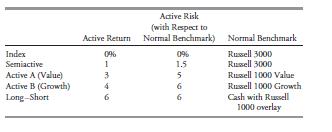

11. Stephanie Whitmore is evaluating several alternatives for the U.S. equity portfolio of her company’s pension plan, involving the following managers:Active A’s misfit risk is 7.13 percent. In all of the questions below, assume that the active returns are uncorrelated. The overall equity

10. Karen Johnson is responsible for the U.S. equity portion of her company’s pension plan.She is thinking about trying to boost the overall alpha in U.S. equities by using an enhanced index fund to replace her core index fund holding.A. The U.S. equity portion of the pension plan currently

9. Mike Smith is a consultant evaluating a market neutral long–short strategy for his client.Based on the holdings data he receives from the client, Smith notices a small but persistent difference between the alphas generated on the long side and those generated on the short side. State which of

8. Yoko Suzuki manages an enhanced index portfolio benchmarked to the index for Kyushu Motors’ pension fund. The strategy has a target alpha of 1.5 percent annually with an annualized active risk of 2 percent. Her client is quite pleased that the portfolio has met its stated objective for the

7. Simon Hayes is a long–short portfolio manager with Victoria Investment Management in London. His expertise lies in building market-neutral long–short strategies using U.K.equities. After meeting with his most important client, Hayes learns that the client is planning to hire an investment

6. Explain the principal benefit of a market-neutral long–short portfolio. What risks are inherent in such a portfolio that a long-only equity portfolio lacks?

5. Shawn Miller plans to use returns-based style analysis to analyze his global portfolio. He will use style indices as a proxy for style in the analysis and is debating whether to use indices like Dow Jones (which categorizes stocks as value, growth, or neutral) or like MSCI (which categorize

4. Phillipa Jenkins has been asked to manage internally a FTSE 100 index fund. Because the index’s 10 largest stocks make up more than 50 percent of its weight, Jenkins is considering using optimization to build the portfolio using many fewer than 100 stocks. All 100 stocks in the index are

3. David Burke is considering investing in a mutual fund that is classified generically under the term growth and income. In preparation for his CFA exams, Burke studied style investing. Using publicly available data sources, he gathered the following information about the mutual fund in question.

2. Juan Varga is concerned about the performance and investment positions of an investment firm he hired five years ago. The firm, Galicia Investment Management, has been tasked with managing an active portfolio with a developed market mandate (MSCI World countries). Galicia is a well-known value

1. Katrina Lowry works for the pension department of National Software. Her supervisor has asked her to evaluate the different style alternatives for a large-cap mandate and to highlight their differences.A. State the three main large-cap styles.B. Describe the basic premise and risks of each style

14. A British fixed-income fund has substantial holdings in U.S. dollar–denominated bonds.The fund’s portfolio manager is considering whether to leave the fund’s exposure to the U.S. dollar unhedged or to hedge it using a U.K. pound–U.S. dollar forward contract.Assume that the short-term

13. A portfolio manager of a Canadian fund that invests in the yen-denominated Japanese bonds is considering whether or not to hedge the portfolio’s exposure to the Japanese yen using a forward contract. Assume that the short-term interest rates are 1.6 percent in Japan and 2.7 percent in

12. Assume that the spread between U.S. and German bonds is 300 bps, providing German investors who purchase a U.S. bond with an additional yield income of 75 bps per quarter.The duration of the German bond is 8.3. If German interest rates should decline, how much of a decline is required to

11. Assume that a U.S. bond investor has invested in Canadian government bonds. The duration of a 12-year Canadian government bond is 8.40, and the Canadian country beta is 0.63. Interest rates in the United States are expected to change by approximately 80 bps. How much can the U.S. investor

10. Assume that the rates shown in the table below accurately reflect current conditions in the financial markets.Dollar/Euro Spot Rate 1.21 Dollar/Euro 1-Year Forward Rate 1.18 1-Year Deposit Rate:Euro 3%U.S. 2%In the table, the one-year forward dollar–euro exchange rate is mispriced, because it

9. Consider a collateralized debt obligation (CDO) that has a $250 million structure. The collateral consists of bonds that mature in seven years, and the coupon rate for these bonds is the seven-year Treasury rate plus 500 bps. The senior tranche comprises 70 percent of the structure and has a

8. The current credit spread on bonds issued by Great Foods Inc. is 300 bps. The manager of More Money Funds believes that Great Foods’ credit situation will improve over the next few months, resulting in a smaller credit spread on its bonds. She decides to enter into a six-month credit spread

7. The trustees of a pension fund would like to examine the issue of protecting the bonds in the fund’s portfolio against an increase in interest rates using options and futures.Before discussing this with their external bond fund manager, they decide to ask four consultants about their

6. The market value of the bond portfolio of a French investment fund is ¤75 million.The duration of the portfolio is 8.17. Based on the analysis provided by the in-house economists, the portfolio manager believes that the interest rates are likely to have an unexpected decrease over the next

5. Your client has asked you to construct a £2 million bond portfolio. Some of the bonds that you are considering for this portfolio have embedded options. Your client has specified that he may withdraw £25,000 from the portfolio in six months to fund some expected expenses. He would like to be

4. You are the manager of a portfolio consisting of three bonds in equal par amounts of$1 million each. The first table below shows the market value of the bonds and their durations. (The price includes accrued interest.) The second table contains the market value of the bonds and their durations

3. The table below shows the spread duration for a 70-bond portfolio and a benchmark index based on sectors. Determine whether the portfolio or the benchmark is more sensitive to changes in the sector spread by determining the spread duration for each. Given your answer, what is the effect on the

2. A portfolio manager decided to purchase corporate bonds with a market value of ¤5 million. To finance 60 percent of the purchase, the portfolio manager entered into a 30-day repurchase agreement with the bond dealer. The 30-day term repo rate was 4.6 percent per year. At the end of the 30 days,

1. The table below shows the active return for six periods for a bond portfolio. Calculate the portfolio’s tracking risk for the six-period time frame.Period Portfolio Return Benchmark Return Active Return 1 14.10% 13.70% 0.400%2 8.20 8.00 0.200 3 7.80 8.00 −0.200 4 3.20 3.50 −0.300 5 2.60

19. (Adapted from the 1993 CFA Level III exam)The Medical Research Foundation (MRF) has just learned that it will receive a$45 million cash gift in three months. The gift will greatly increase the size of the foundation’s endowment from its current $10 million. The foundation’s

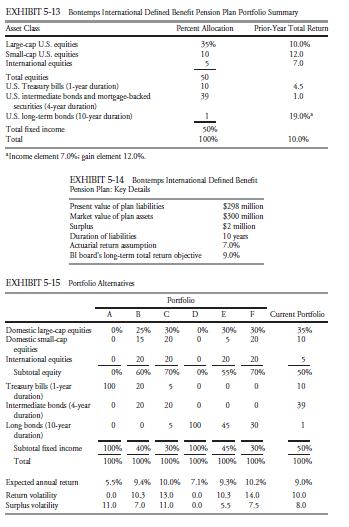

18. (Adapted from the 1995 CFA Level III Exam)Bontemps International (BI) is a financially healthy, rapidly growing import/export company with a young workforce. Information regarding the company’s Employee Retirement Income Security Act (ERISA)-qualified defined-benefit pension plan appears in

17. (Adapted from the 2000 CFA Level III Exam)Hugh Donovan is chief financial officer (CFO) of LightSpeed Connections (LSC), a rapidly growing U.S technology company with a traditional defined-benefit pension plan.Because of LSC’s young workforce, Donovan believes the pension plan has no

16. Wendy Willet is chief investment officer of the Allright University Endowment (AUE)based in the United States. The strategic asset allocation of AUE is as follows, where percentages refer to proportions of the total portfolio:Global equities 60%U.S. Equities 30%Ex-U.S. equities 30%Global fixed

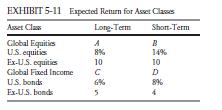

15. Exhibit 5-10 shows William Smith’s financial and human capital in constant dollars terms at 30, 50, and 65 years of age.Smith’s target asset allocation for total wealth is 60/40 stocks/bonds. Assume that his human capital is approximately risk free and uncorrelated with stock returns.

14. For the following types of investors, appraise the importance of using the specified asset class for strategic asset allocation.A. Long-term bonds for a life insurer and for a young investor.B. Common stock for a bank and for a young investor.C. Domestic tax-exempt bonds for an endowment and

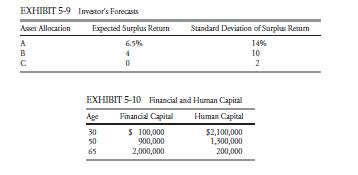

13. The Inner Life Insurance Company (ILIC) is considering the asset allocation shown in Exhibit 5-9 below. ILIC has risk aversion (RA) of 5 using the scale presented in the text.A. Recommend an asset allocation for ILIC.B. Recommend a statistical method that ILIC should use to obtain information

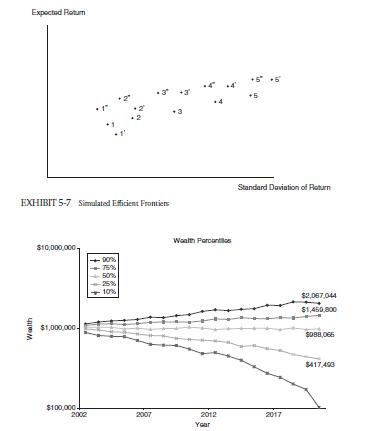

12. John Stevenson retired at the end of 2002 at age 65. His $1 million portfolio is invested 70 percent in common stocks and 30 percent in bonds. He anticipates liquidating $50,000 a year from the portfolio during retirement. Exhibit 5-8 gives the results of a Monte Carlo simulation showing the

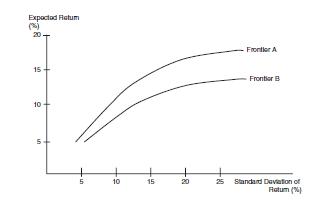

11. A. Identify the scatter of points in Exhibit 5-7.B. Describe how to compute a resampled efficient frontier from the scatter of points shown in Exhibit 5-7. Expected Retur 20- 15 10 5 10 15 20 B- Frontier A Frontier B 25 Standard Deviation of Ratum (%)

10. A. In Exhibit 5-6, if Frontier B is a mean–variance efficient frontier in which the efficient portfolios’ portfolio weights reflect perfect knowledge of the true return parameters, discuss whether Frontier A could be i. the conventional mean–variance efficient frontier ii. the resampled

9. Claudine Robert is treasurer and vice chair of the Investment Committee of Le Fonds de Recherche des Maladies du Coeur (FRMC), a French foundation with ¤95 million in assets that supports medical research relating to heart diseases and treatments. For the annual asset allocation review, Robert

8. Compare and contrast the global minimum variance portfolio with the minimum surplus variance portfolio.

7. Contrast the elements in the strategic asset allocation process that are relatively stable to those that frequently change.

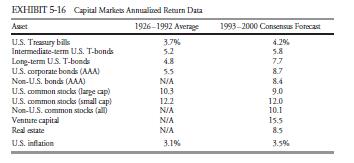

6. The Ingo Fund is a Swedish foundation currently invested in Swedish equities and government bonds. The portfolio has a Sharpe ratio of 0.40. The fund is considering adding U.S. real estate to its portfolio. U.S. real estate as represented by the NACREIF(National Council of Real Estate Investment

5. Critique the following specifications of asset classes:A. U.S. equities, world equities, U.S. bonds.B. Canadian equities, Canadian bonds, alternative assets.C. Small-cap U.S. equities, large-cap U.S. equities, real estate, private equity, ex-U.S.developed market equities, emerging market

4. William Ernst needs to spend 5 percent from his portfolio annually. He anticipates that inflation will be 2.4 percent annually. Ernst incurs expenses of 60 basis points a year in investing his portfolio. Which asset allocations satisfy Ernst’s return requirement?

3. The Garrett Foundation would like to choose an asset allocation that minimizes the probability of returns below its annual spending rate of 3.5 percent. Recommend an asset allocation for the foundation.

2. On the scale discussed in the text, Robert Langland’s risk aversion (RA) is 5. Recommend an asset allocation for him.

1. Paula Williams is chair of the Investment Committee of the Robinson Furniture Manufacturing (RFM) defined-benefit pension plan. The committee has established the strategic asset allocation given in Exhibit 5-1. The RFM pension liability can be modeled approximately as a short position in a

19. Fap is a small country whose currency is the fip. Ten years ago, the exchange rate with the Swiss franc (CHF) was 3 fips per 1 CHF, the inflation indices were equal to 100 in both Switzerland and Fap, and the exchange rate reflected purchasing power parity (PPP).Now, the exchange rate is 2 fips

18. Looking independently at each of the economic observations below, indicate the country where an analyst would expect to see a strengthening currency for each observation.Observation Canada United Kingdom Expected inflation over next year 2.0% 3.0%Real (inflation-adjusted) government 10-year

17. Discuss four approaches to forecasting exchange rates.

16. J. Wolf is an individual investor who intends to make an additional investment in various South Korean–based assets based on the outcome of your capital market expectationssetting framework analysis. Your analysis should use the data provided in the table below.However, each measure should be

15. Other than changes in the rate of inflation, specify two factors that impact the yields available on inflation-indexed bonds.

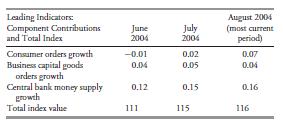

14. In late 2004, K.C. Sung is planning an asset allocation strategy but would first like to assess Australia’s current economic environment, then make a forecast for the economic conditions expected over the succeeding six- to nine-month period. Sung has learned that the leading indicator

13. Identify four differences between developed economies and emerging market economies.

12. A. List five general elements of a pro-growth government structural policy.B. For each of the variables given below, describe the change or changes in the variable that would be pro-growth and determine the element of a pro-growth government structural policy that would best describe the change

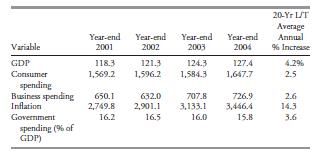

11. Plim Ltd. Is a manufacturing company in Finland that is a defined-benefit pension plan sponsor. Plim intends to increase its overall plan diversification by making an investment in Brazil. The table below provides Brazilian data for indices representing various economic variables.Based only on

Showing 200 - 300

of 1717

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers