New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial accounting

Financial Accounting 9th Edition Craig Deegan - Solutions

What is a functional currency, and what is a presentation currency?

Why do we need to translate the financial statements of a foreign operation?

If we consolidate the financial statements of the parent entity with its subsidiaries, do all of the different entities’ financial statements have to be in the same presentation currency prior to consolidation? Why?

Explain why foreign currency gains or losses in relation to the translation of the accounts of a foreign operation into a particular presentation currency are not treated as part of the period’s profit or loss, but instead are included within other comprehensive income and then transferred to an

When translating the financial statements of a foreign operation, do we first translate the accounts into the functional currency and then into the presentation currency, or vice versa?

What is the difference between the presentation currency and the functional currency and how would an organisation determine the appropriate presentation currency?

For a foreign operation, will the functional currency necessarily be the same as the local/domestic currency?

On consolidation, will any non-controlling interests be allocated a share of any foreign currency translation reserve?

When translating a foreign operation’s financial statements into a functional currency, what rate do we apply to monetary assets?

At the end of the reporting period, when consolidation adjustments are made, will goodwill on acquisition of a foreign operation be adjusted to reflect any changes in exchange rates?

When translating a foreign operation’s financial statements from a functional currency into the presentation currency, what rate do we apply to the various income and expenses?

Explain what rates should be used for the assets, liabilities and equity items of a foreign entity when translating the financial statements from a functional currency to a particular presentation currency.

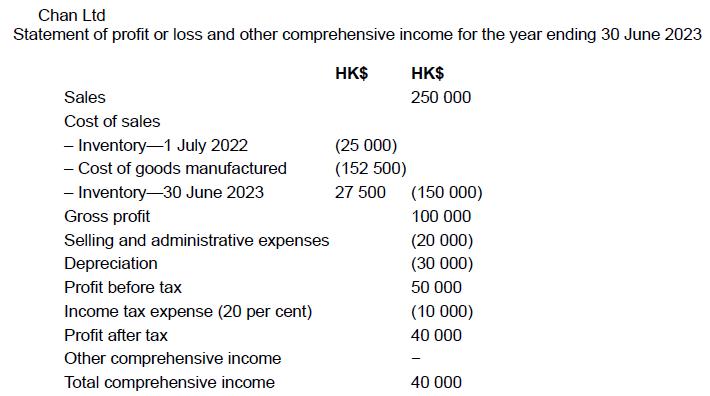

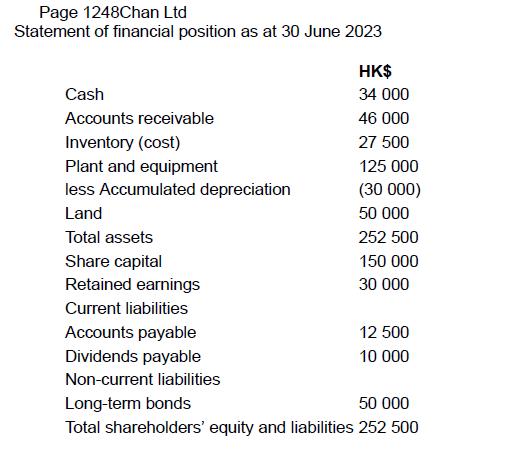

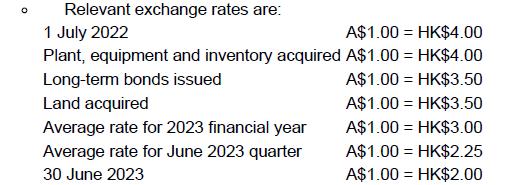

Bazza Ltd, an Australian company, acquires all of the shares of Chan Ltd, a Hong Kong company, on 1 July 2022. Chan Ltd had a $nil balance in retained earnings as at the date of acquisition. The financial statements for Chan Ltd are presented below:Additional InformationPlant, equipment and

What is social-responsibility reporting?

What is ‘corporate social-responsibility reporting’?

What is meant by the term ‘accountability’?

What does ‘sustainable development’ mean?

What is the relationship between ‘accountability’ and ‘accounting’?

What would you consider to be the social responsibilities of business?

What is the relationship, if any, between perceptions of organisational ‘responsibilities’ and ‘accounting’?

What is the Sustainability Accounting Standards Board?

If an organisation is concerned about its perceived legitimacy, is it more important for that organisation to actually do the right thing, or to communicate that it is doing the right thing? Give reasons for your answer.

What is an ‘externality’, and does financial reporting typically account for the externalities being generated by an organisation?

What are some of the central premises of Legitimacy Theory?

What is ‘integrated reporting’?

According to Legitimacy Theory, what are the implications for an organisation that fails to comply with the expectations held by society?

What is the IPCC?

In relation to schemes aimed at reducing carbon emissions, briefly explain how a ‘cap-and-trade’ system operates.

Legitimacy Theory relies upon the theoretical notion of a ‘social contract’. What is a ‘social contract’ and why is it linked to Legitimacy Theory?

Do the majority of large companies actually disclose information about their social and environmental performance?

Does an organisation have a responsibility to future generations?

What is sustainable development?

From the perspective of sustainable development, why is it important to consider both intergenerational and intragenerational equity?

Does AASB 116 have any requirements in relation to restoring land? If so, what are the requirements?

According to the GRI, what are the six principles for defining report quality, and are they similar to the qualitative identified in the Conceptual Framework for Financial Reporting?

What is the role of the United Nations’ Sustainable Development Goals?

In relation to the issue of ‘biodiversity’, what types of disclosures are suggested by GRI 304?

Explain the apparent rationale behind the Australian Government introducing the Modern Slavery Act.

What do ‘counter accounts’ represent, and would the incorporation of ‘counter accounts’ within corporate reports enhance the usefulness of corporate reports?

What are some of the motivations that might drive corporate managers to voluntarily disclose social and environmental performance information?

What is an externality and do reported profits incorporate a measure of the externalities generated by a reporting entity?

As used within this chapter, what does ‘full cost accounting’ involve?

What is personal social responsibility and what is the role of business educators in instilling the idea of personal social responsibility within students?

The following appeared in the 2018 Sustainability Report of BHP (p. 10):Our social licence is an informal set of enabling relationships that exist between BHP and our local, regional and global stakeholders. Our social licence is built on and sustained by the quality of our relationships, our

What is climate change and what are some of the accounting issues associated with climate change?

What implications would a failure to provide balanced, unbiased social and environmental performance data have for the perceived credibility of the other information provided in an annual report?

In this chapter it was stated:When we then review the Framework to see the perspective adopted with respect to the primary purpose of an integrated report we find (p. 7): The primary purpose of an integrated report is to explain to providers of financial capital how an organization creates value

What disclosures should an entity make in the notes to the financial statement in respect of each material category of non-adjusting event after the reporting period?

A major flood wipes out the principal place of operations of an organisation three weeks after the end of the reporting period. The flood loss is covered by insurance. Would this be an ‘adjusting event’ or a ‘nonadjusting event’? Why?

Determine whether the following events require adjustment to the financial statements, or disclosure by way of a note to the financial statements:a. Loss of a major customer after the end of the reporting period. No amount is owing at the end of the reporting period.b. A debtor owes a material

An organisation has five factories. One of the factories burns down two weeks after the end of the reporting period. Would this constitute an ‘adjusting event’ or a ‘non-adjusting event’? Why?

An organisation sells a significant proportion of its inventory two weeks after the reporting date. The inventory had been on hand for four months. Would this constitute an ‘adjusting event’? Why?

The managers of an organisation are provided with an annual bonus which is 1 per cent of profits. The profit of the organisation is not determined until 2 months after the reporting date. Would the determination of profit result in the recognition of an ‘adjusting event’? Why?

Events after the reporting period can be classified as either adjusting events or non-adjusting events. Describe each of these types of events, and explain the accounting treatment required for each. (For example, for which type of event is disclosure within the notes to the financial statements

If information relates to an event that occurs after the reporting period, when and why should it be detailed in the notes to the financial statements?

What is the rationale for the inclusion of information, within the notes to the financial statements, about material transactions and events that have occurred since the reporting date, but before the financial statements were authorised for issue?

What are the different types of events after the reporting date and how should they be disclosed?

If an event occurs ‘after the reporting period’, then from the perspective of accounting standards, it is considered that the event has occurred between the ‘end of the reporting period’ and the ‘date when the financial statements are authorised for issue’. What is the ‘date when the

In a newspaper article written by Carol Altmann and entitled ‘Cooking the books the Harris Scarfe way’ (The Australian, 7 August 2001, p. 1), the author discussed the collapse of the company known as Harris Scarfe. Specific commentary was given to how the senior accountant utilised ‘creative

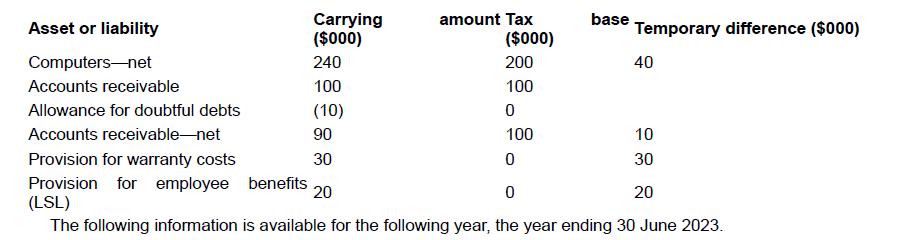

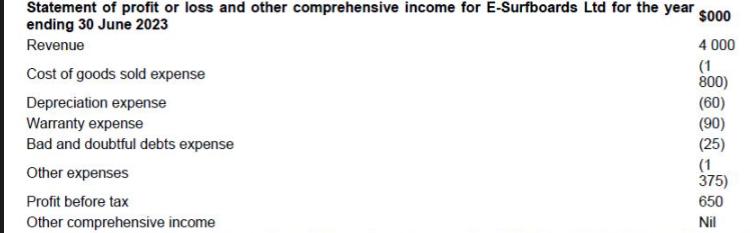

At 30 June 2022, E-Surfboards Ltd had the following temporary differences:E-Surfboards Ltd depreciates computers over five years in its accounting records but over three years for tax purposes. The straight-line method is used. During the year, E-Surfboards wrote off bad debts amounting to $15 000.

Buller Manufacturing Ltd issues 1000 share options to each of its 25 most senior employees. The options can be exercised at the end of a four-year period. Once exercised, the shares may not be sold to another party for another two years, after which time the employees may dispose of the

For an equity-settled share-based payment transaction that involves the purchase of inventory, how should the cost of the inventory be determined?

What are the three types of share-based transactions specifically addressed by AASB 2?

What is an ‘equity-settled share-based payment transaction’?

An article entitled ‘Parent loan puts Parmalat down $165m’ by Andrew Fraser, which appeared in The Australian on 8 June 2004, made reference to two extraordinary items, which at the time required separate disclosure. It stated:Parmalat Australia yesterday filed a net loss of $165.8 million,

What is a ‘share-based payment transaction’?

Pursuant to AASB 101, the statement of profit or loss and other comprehensive income can be presented by way of two alternative presentation formats. What are these formats?

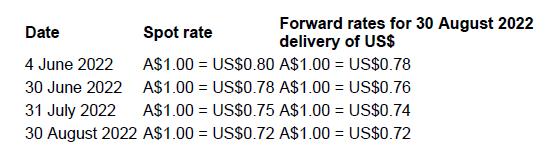

Melbourne Ltd manufactures electric skateboards. On 4 June 2022 Melbourne Ltd enters into a non-cancellable purchase commitment with Miami Ltd for the supply of wheels, with the wheels to be shipped on 30 June 2022. The total contract price was US$3 000 000 and the full amount was due for payment

AASB 7 is concerned primarily with ensuring extensive disclosure of financial instruments. Why do you think this is the case?

What is a compound financial instrument? Provide some examples.

On 1 July 2023 Cooloola Ltd provided 1 million options to its chief executive officer. The options were valued at $1.00 each allowed the chief executive officer to acquire shares in Cooloola Ltd for $7 each. The chief executive officer is not permitted to exercise the options before 30 June 2025

On 1 July 2023, Coastalwatch Ltd issued 5 million shares at $5.00 each. All of the shares were subscribed for. Coastalwatch Ltd incurred the following costs that were associated with the share issue:REQUIREDPrepare the journal entries necessary to account for the issue of the shares. Advertising of

On 1 July 2022, Mick Ltd invited Fanning Ltd to purchase 1 million shares at $3.00 per share. At the time of accepting the offer, Fanning Ltd which is an insurance company had cash resources available of only $2600000. The balance of the purchase price would be made up of insurance to be provided

What forms of preferential treatment can the holders of preference shares receive over and above the rights of holders of ordinary shares?

For many years Switches Ltd provided a defined benefit superannuation plan for its employees, but owing to concerns about its exposure to risk it has been phasing out the defined benefit superannuation plan and replacing it with a defined contribution superannuation plan. Most employees belong to

Australasia Ltd started operating on 1 July 2021 with 12 employees. Three years later all of those employees were still with the company. On 1 July 2023 the company hired 15 more people but by 30 June 2024 only 10 of those employed at the beginning of that year were still employed by Australasia

Alexandra Bay Ltd has five employees. According to their particular employment award, long-service leave can be taken after 12 years, at which time the employee is entitled to 10 weeks’ leave. If an employee were to leave before the completion of 12 years’ service, no entitlement would be

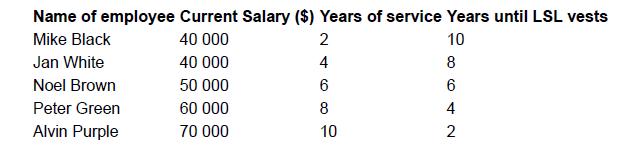

Surf School Ltd has six employees who are entitled to long-service leave (LSL). The LSL can be taken after 10 years of service, at which time the employee is entitled to 13 weeks’ leave. Entitlements to payment on departure arise after eight years of service. The following information about the

When would it be considered that income has arisen in relation to employee benefits?

Coolum Pty Ltd manufactures sunglasses that are sold to department stores, pharmacies, optical dispensers and optometrists. During the current year, Coolum Pty Ltd produced 60 000 pairs of sunglasses. Owing to increased competition and unseasonally wet weather affecting sales of sunglasses, the

Explain in which circumstances it would be appropriate to use the following cost-flow assumptions:a. Specific-identification assumptionb. Weighted-average cost assumptionc. First-in, first-out (FIFO) assumption

Explain how it is possible for profits to be manipulated through the use of the specific-identification and LIFO inventory cost-flow assumptions.

What is a joint arrangement and what are the two main classifications of joint arrangements?

When an investor acquires an interest in an associate:a. How is goodwill on acquisition calculated?b. Why is goodwill on acquisition calculated?c. How is goodwill on acquisition of the associate disclosed?

What is ‘fair value’ and why is it relevant to consolidation accounting?

Define:a. A legal entityb. An economic entityc. A parent entityd. A subsidiary.

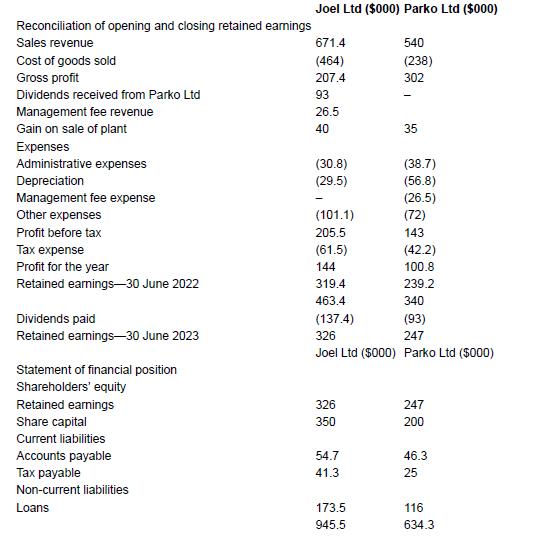

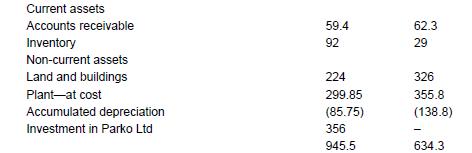

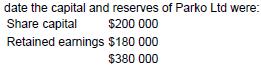

The following financial statements of Joel Ltd and its subsidiary Parko Ltd have been extracted from their financial records at 30 June 2023.Page 1053Other informationJoel Ltd acquired its 100 per cent interest in Parko Ltd on 1 July 2018, that is, five years earlier. At that At the date of

Do we make adjustments to the non-controlling interests’ share of profit when an intragroup transaction affects the subsidiary’s profit or loss, or the parent entity’s profit or loss, or both?

In the presence of non-controlling interests, if dividends are declared by a subsidiary and by a parent entity, which dividends payable will be shown in the consolidated balance sheet?

Do dividends declared and paid by a partly owned subsidiary reduce the non-controlling interest in that subsidiary?

How are non-controlling interests affected by intragroup transactions?

Could the non-controlling interests control, in total, more than 50 per cent of the total shareholding of a subsidiary?

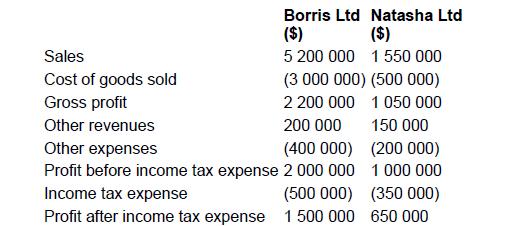

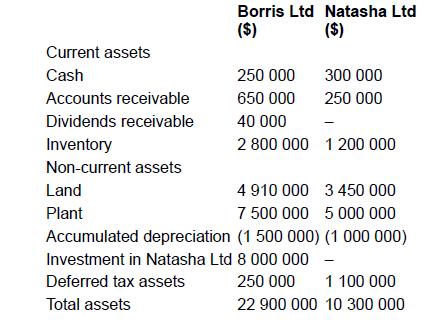

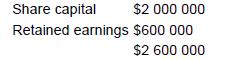

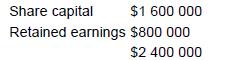

On 1 July 2021 Borris Ltd purchased 80 per cent of the shares of Natasha Ltd for $8 million. On 1 July 2021 the shareholders’ funds of Natasha Ltd were:Additional informationThe management of Borris Ltd measures any non-controlling interest in Natasha Ltd at fair value.At acquisition date, all

What is a direct ownership interest and what is an indirect ownership interest?

On consolidation, when we eliminate the parent entity’s investment in the subsidiary against the pre-acquisition capital and reserves of the subsidiary, do we take account of only the direct ownership interests of the parent entity, or both the direct and indirect ownership interests?

What is an indirect non-controlling interest in a subsidiary?

Why do we need to know which part of a non-controlling interest is direct, and which part is indirect?

Can an entity be considered a controlled entity (that is, a subsidiary) of another entity (the parent) even if that other entity (the parent) has no direct ownership interest in the subsidiary?

Where in the statement of financial position would indirect non-controlling interests be disclosed?

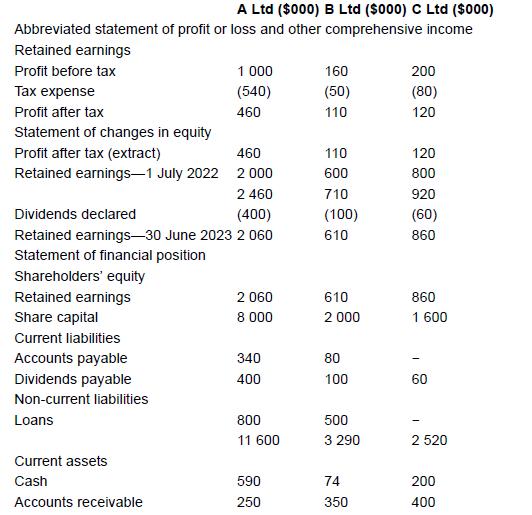

A Ltd acquires a 60 per cent interest in B Ltd on 1 July 2022 for a cost of $2 million representing the fair value of consideration transferred. The management of A Ltd values any non-controlling interest at acquisition date at the proportionate share of B Ltd’s net identifiable assets at

Showing 1100 - 1200

of 7094

First

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

Last

Step by Step Answers