New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial accounting

Financial Accounting 9th Edition Craig Deegan - Solutions

Outline arguments for and against the use of the lower of cost and net realisable value rule.

What costs should be included as part of the ‘cost’ of inventory?

What does unearned revenue represent, and when shall it be recorded?

Which financial assets shall be measured at amortised cost?

In accordance with AASB 9, the recognition of a financial asset or financial liability will be influenced by considerations as to whether there is a contractual right to exchange financial assets or financial liabilities with another entity under conditions that are potentially favourable, or

If equity investments have been made in another entity (for example, shares have been acquired), and the investments were made for trading purposes, how shall any gain or loss on the investments be treated?

At the time of initial recognition, on what basis shall financial instruments be measured?

Surfside Ltd is marketing a ‘surfing bundle’ in which, for $1100, it provides customers with a surfboard (which retails separately for $850), a wetsuit (which retails separately for $250) and five lessons (which retail separately for $200). You are required to determine:a. Whether separate

Eddie Ltd sells to Mass Marketer Ltd an item of machinery that manufactures identical surfboards. Included in the sale was a put option that gives Mass Marketer Ltd the right to require Eddie Ltd to buy back the machine for a specified price on a specified date. When should Eddie Ltd recognise the

When amounts to be received from customers are to be discounted (for example, the amount to be received for a sale of goods or services will be received beyond 12 months), what discount rate is to be applied?

If an organisation receives a large donation from a particular benefactor, would this donation represent income to the organization? Explain your answer.

If an entity recognises the revenue associated with a contract with a customer over time (rather than at a point in time), would this approach be considered more conservative than an approach that defers profit recognition until the completion of the contract (that is, at a future point in time)?

In accounting for a long-term construction contract, if the billings on a construction in progress exceed the costs assigned to the construction in progress (contract asset), then how should this be disclosed in the statement of financial position?

If an entity is performing its responsibilities under a contract to a customer in a manner where the performance obligations are being satisfied ‘over time’ (rather than at a ‘point in time’), what are the alternative approaches to measuring the level of progress that depict the transfer of

Noosa Ltd owns a pie shop on Hastings Street. The carrying amount of the shop in the accounts of Noosa Ltd is $1.2 million. Because it needs some funds it has decided to sell the shop to Leaseco Ltd. Leaseco Ltd buys the shop for $1.5 million and then immediately leases the shop back to Noosa Ltd

For several years the IASB and the FASB had been developing an accounting standard entitled Revenue from Contracts with Customers. An original Discussion Paper was released in 2008 but the ultimate accounting standard AASB 15 was not released until 2014. What might be some reasons for the lengthy

A firm believes that it is subject to scrutiny by particular interest groups because it is earning excessive profits. Do you think that this might influence whether the firm prefers to recognise revenue over time for its construction contracts, or whether it would prefer to defer profit recognition

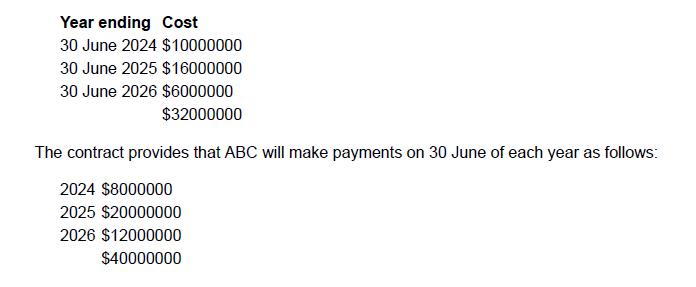

XYZ signs a contract on 30 June 2023, agreeing to build a bridge for ABC at a contract price of $40 million. ABC will be in control of the asset throughout the construction process. XYZ estimates that construction costs will be as follows:The contract is completed as expected on 30 June 2026.

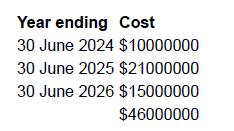

Assume the same facts as in Challenging Question 28, except that XYZ now estimates at the beginning of the 2025 financial year that construction costs will be as follows:Provide the journal entries for each year, assuming that cost (an input measure) is used as the basis for assessing progress on

In the presence of the following contractual arrangements, would you expect a firm to prefer to recognise revenue over time (that is, throughout the term of a contract) or to defer profit recognition until the completion of the contract (that is, at a future point in time?a. A management

We have a separate accounting standard, AASB 138, that specifically deals with intangible assets and which provides different requirements from those for property, plant and equipment (the rules for which appear in AASB 116). What is it about intangible assets that requires them to have a separate

Will the balance sheet report the economic value of all of an organisation’s intangible assets?

Explain the difference in how you measure intangible assets that are individually acquired compared with those that are acquired as part of a business combination.

Explain the difference between tangible assets and intangible assets. Is it necessary to have different accounting rules for tangible and intangible assets?

Explain the change in requirements for accounting for research and development costs resulting from adopting International Financial Reporting Standards. Do the current requirements provide a better representation of the financial performance and financial position of the entity?

What is the difference between an unidentifiable intangible asset and an identifiable intangible asset?

How is the value of goodwill determined for accounting purposes?

Would goodwill be considered an ‘asset’ according to the Conceptual Framework for Financial Reporting?

For each class of intangible assets, a reporting entity is required to disclose a reconciliation of the opening and closing carrying amount. What items are to be included within this reconciliation?

Why did many Australian reporting entities oppose the mandatory amortisation of goodwill that was prescribed under Australian accounting standards prior to international convergence in 2005?

What are possible arguments for and against the prohibition of recognition of internally generated goodwill?

What is an ‘active market’, and is an active market likely to exist for intangible assets such as brand names or development-related expenditures? Explain your answer.

Tamarama Ltd acquires 100 per cent of Bronte Ltd on 1 July 2021. Tamarama Ltd pays the shareholders of Bronte Ltd the following consideration:On 1 July 2021 Bronte Ltd’s statement of financial position shows total assets of $700 000 and liabilities of $300 000. The fair value of the assets is

Nat Ltd purchases a 100 per cent interest in Angourie Ltd. The cost of the acquisition is $1 400 000 plus associated legal costs of $70 000. As at the date of acquisition, the statement of financial position of Angourie Ltd shows:Additional informationThe assets and liabilities of Angourie Ltd are

Energy Ltd is involved in the research and development of a new type of three-finned surfboard. For this R & D it has incurred the following expenditure:$50 000 obtaining a general understanding of water-flow dynamics$30 000 on understanding what local surfers expect from a surfboard$90 000 on

Describe the amortisation requirements for certain identifiable intangible assets and the changes to accounting for goodwill introduced as part of the convergence with international accounting standards. How have these changes affected reported profit?

Inglis Ltd has a number of taxi licences that are shown in the financial statements at cost. Can these licences be revalued to fair value and, if so, do they also need to be subject to periodic amortisation?

State whether the following assets may be revalued. Prepare journal entries for any revaluations permitted by accounting standards (you can ignore taxation effects). Assume that each item listed below represents a separate class of assets.a. A company has developed a masthead for its newspaper to

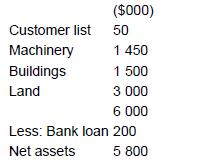

Mam Ltd acquired Bo Ltd on 1 July 2022 for $7 000 000 in cash. At that date, Bo Ltd’s net identifiable assets had a fair value of $5 800 000. The fair value of the net identifiable assets of Bo Ltd are determined as follows:At the end of the reporting period of 30 June 2023, the management of Mam

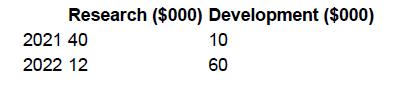

In 2021 McGoy Ltd decided to develop a surfboard out of a new type of material that was resistant to damage. The material to be used was more like plastic than the fibreglass traditionally used on surfboards. In 2021 McGoy Ltd spent $510 000 on research aimed at understanding the properties of

What is goodwill, and how is it measured for financial reporting purposes?

What activities should be included in the cost of research and development? In your answer, differentiate between research activities and development activities.

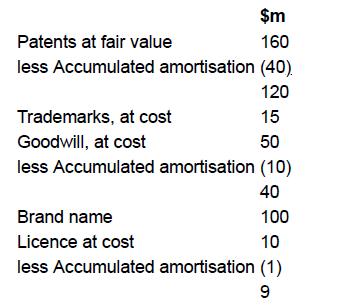

IP Ltd reports the following intangible assets:Patents were acquired at a cost of $80 million and were revalued soon afterwards. They have an estimated life of 16 years, of which 12 years remain.The trademark can be renewed indefinitely, subject to continued use. The cost represents registration

In a 2018 media release from ASIC (18-310MR ‘Premier Investments writes down brand name assets’, http://www.asic.gov.au/about-asic/news-centre/find-a-media-release/2018-releases/18-310mr-premier-investments-writes-downbrand-name-assets/), it is noted that:ASIC notes the decision by Premier

a. If an accounting standard is introduced that requires certain types of expenditures to be expensed rather than capitalised, and that type of expenditure is discretionary, would you expect management to change their expenditure patterns from what they would have been in the absence of the

When an organisation acquires another organisation as part of a business combination, what impact on recognised goodwill will occur if greater value is attributed to identifiable intangible assets acquired as part of the acquisition?

In a report by KPMG (Key Audit Matters: Auditor’s Report Snapshot, 20 September 2017), it was noted that calculating and suggesting adjustments to the value of an organisation’s reported goodwill (and also to brand names) is the issue that takes up most of financial statement auditors’ time.

Should computer software be classified as an intangible asset or as part of property, plant and equipment?

In 1999 the Group of 100 (G100), an Australian group representing senior executives from large Australian companies, made a submission to the Australian Accounting Standards Board. They were worried about the ‘strict’ rules incorporated in IAS 38 and were concerned that similar rules might be

At its September 2000 meeting, the AASB decided to provide interested parties with access to the document Strategy Paper—Intangible Assets through its website, www.aasb.gov.au. In a section entitled ‘Key issues’ the document states:Some argue that if accounting standards were to not

In a newspaper article by Bridget Carter and Scott Murdoch (‘Myer write down on cards’, The Australian, 12 February 2018) it was reported that the total market value of Myer shares was $480.45 million at the same time as its intangible assets primarily the value of its brand names and goodwill

Innovator Ltd incurred expenditure researching and developing a cure for a common disease found in turnips. At the end of 2021, management determined that the research and development project was unlikely to succeed because trials of the prototype had been unsuccessful. During 2022 a breakthrough

As explained within the chapter, accounting standards prohibit goodwill from being subject to amortisation. Rather, there is a requirement that goodwill be subject to impairment testing. In relation to impairment testing of goodwill, Petersen and Plenborg (2010, p. 420) state:Many argue that an

Bloom (2009) notes how a great deal of the market value of a listed company relates to the value of its goodwill much of which has been internally generated and which is prohibited from being recognised. In this regard he states:Paragraph 48 of AASB 138 states that ‘internally generated goodwill

In an article by Sue Mitchell entitled ‘Undies, sheets key to Pacific recovery’ that appeared in The Australian Financial Review on 27 August 2014 (p. 15), it was reported that:Pacific Brands’ fourth chief executive in seven years is counting on higher sales of Bonds underwear and Sheridan

ASIC issued a media release in January 2019 (19-014MR) in which it noted that numerous large Australian organisations are not properly accounting for the possible impairment of their intangible assets. Specifically, ASIC noted some entities as not having sufficient regard to impairment indicators,

In an article by Paul Smith entitled ‘Telstra takes $500m hit’ that appeared in The Australian Financial Review on 3 February 2018 (p. 25), it was reported that Telstra was writing down the value of its investment in a video-streaming firm (named Ooyala) it bought for more than $500 million to

If the managers of an organisation that acquires another organisation either do not recognise previously unrecorded intangible assets of the acquired company, or underestimate their fair value, how could this potentially impact future reported profits?

An article that appeared in The Australian on 23 November 2005 by Blair Speedy, entitled ‘Aussie firms quick to adopt new regime’, included the following extract. Read the extract and evaluate the comments made by Sir David Tweedie, Chairperson of the IASB. Under the International Financial

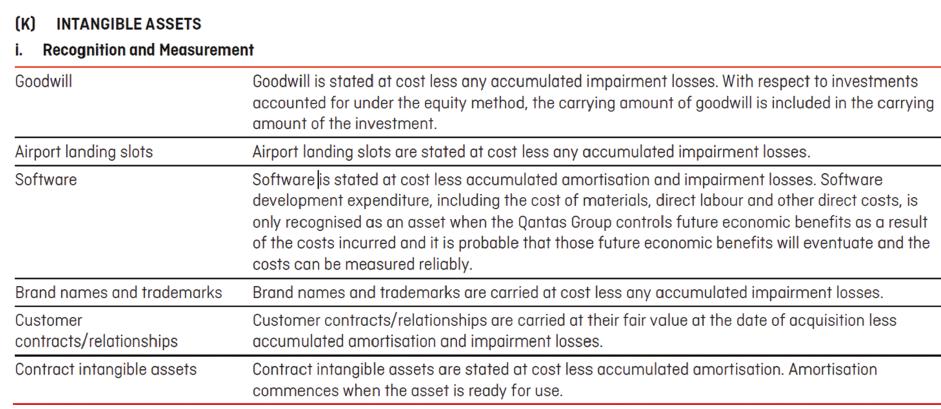

The following information appeared in the notes to the financial statements as reported in the 2019 Annual Report of Qantas Airways. You are required to explain the nature of each of these intangible assets and to evaluate whether the accounting treatment appears to be in compliance with accounting

As goodwill is not to be amortised, does this mean that the balance of goodwill can be carried forward indefinitely?

In an article by Carrie La Frenz entitled ‘Hastie auditor rejects PPB concerns’ that appeared in The Australian Financial Review on 22 January 2013 (p. 16) and which is adapted here, it was reported that:In 2012 Hastie Group collapsed and there were wide-ranging job losses (2,100). PPB Advisory

What is a heritage asset?

What are some of the characteristics of a heritage asset?

Is there general agreement within the ‘accounting community’ that heritage assets should be measured in monetary terms?

What are some of the differences between heritage assets and assets that are typically held by privatesector entities?

Do heritage assets seem to comply with the definition of assets provided within the Conceptual Framework?

What attributes of heritage assets would support the notion that they need to be accounted for differently from other assets?

Do you think that heritage assets should be classified as assets pursuant to the Conceptual Framework for Financial Reporting? Explain your answer with particular reference to the definition and recognition criteria embodied within the Conceptual Framework.

Carnegie and West (2005) state that ‘full accrual accounting systems are now being applied to a range of public-sector institutions that have no profit making nor financial wealth maximisation objective’. You are required to explain whether believe this application of financial accounting

Because heritage assets typically generate negative net cash flows, some authors have argued that they should be treated as liabilities and not as assets. Do you agree with such a view? Why?

AASB 116 permits ‘heritage and cultural assets’ to be revalued. What would be some potential problems in revaluing heritage assets?

Explain and contrast the valuation suggestions made by Carnegie and Wolnizer in relation to national parks that are considered to be heritage assets and the valuation suggestions of Roberts, Staunton and Hagan (1995) for forest reserves held for the purposes of milling.

How would you value a biological asset used within, or generated by, agricultural activities, and how are changes in valuation to be treated for the purposes of an entity’s profit or loss?

What types of non-financial disclosures are required by AASB 141?

Would you consider that the accountability of managers of heritage assets is best demonstrated by requiring them to provide up-to-date valuations of the ‘assets’ under their control? Explain your answer.

Do you think that we should have different asset definitions for not-for-profit organizations and for-profit organizations? Explain your answer.

Do you consider that lack of consistency across entities in the accounting treatment of particular items (for example, the measurement of biological assets) is sufficient justification for the development of an accounting standard Explain your answer.

Roberts, Staunton and Hagan (1995) suggest that increases in the valuation of livestock can be broken down into two components:1. Changes in current market value as a result of biological factors, for example, growth, quality, ageing and changes in composition (volume changes)2. Changes in market

Briefly explain how the method of valuation known as the contingent-valuation method is applied.

Briefly explain how the method of valuation known as the travel-cost method is applied.

Apart from the disclosures specifically required by AASB 141, what sustainability/environmentally-related disclosures would you suggest that a company with, for example, large herds of dairy cattle should make?

Evaluate the following comment:Some cultural or heritage assets are so important that their ‘worth’ should not be reflected by any form of monetary valuation. That is, they are beyond pricing and it would be inappropriate to try to value them in monetary terms.

In an article that appeared in The Australian Financial Review on 15 December 2018 entitled ‘Australian Museum collection hits $1 billion mark’ (by Elouise Fowler, p. 3), it was reported that Kim McKay who took up the position of director of the Australian Museum almost five years ago was of

A recent annual report of the City of Sydney Council did not include library books on the statement of financial position, notwithstanding the existence of a substantial library collection. The City of Sydney Council’s accounting policy for library books is to expense them at the time of

In the April 1998 edition of Charter, an article appeared on self-generating and regenerating (biological) assets. In the article it is noted that:The main criticism against net market value accounting is that it does not reflect actual events. It’s accounting for what’s going to happen in the

Carnegie and West (Reprinted from CARNEGIE, G.D. & WEST, B.P., 2005, ‘Making Accounting Accountable in the Public Sector’, Critical Perspectives on Accounting, vol. 16, p 910, with permission from Elsevier.) state:The consequences of the weak definitional basis for the monetary valuation of

It was reported within the chapter that some years ago the chairperson of Australia’s biggest wine producer, Southcorp Ltd, was critical of the requirements incorporated within AASB 141 because it would lead to the recognition of income in advance of when the company believed it should be

How would you value a museum collection of ancient Aboriginal artefacts?

Carnegie and Wolnizer (1995, ‘The Financial Value of Cultural, Heritage and Scientific Collections: An Accounting Fiction’, Australian Accounting Review, vol. 5, no) argue that quantifying heritage assets in financial terms is an ‘accounting fiction’. Explain what they mean. Do you agree

What types of information do you believe a government-funded museum should provide to reflect its performance, and what could be the purpose of providing the information you suggest?

Read the following adaptation of an article entitled ‘CBA in payout on “toxic” products’ by Leo Shanahan that appeared in The Australian on 4 April 2015.In 2012 a claim was lodged in the Federal Court against the Commonwealth Bank by Gloucester Council and an investment company, Clurname,

Read the following extract from an article entitled ‘Tanks to go at old refinery’ by Cameron England that appeared in The Advertiser on 17 September 2012.The demolition of the Port Stanvac oil refinery has begun, nine years after the site was abandoned. Site owner Exxon Mobil says it will take

In an article entitled ‘Nailed. Father’s discovery sparks punching bag recall’ by Angus Thompson which appeared in The Advertiser on 11 March 2015 it was reported that:father’s claims that he found nails, broken glass and medical waste in a punching bag bought for his sons has led to a full

Read the extract below from an article entitled ‘Suits overshadow the Ts at American Apparel’ by Joann Lublin that appeared in The Australian on 28 May 2015. Nearly a year after moving to oust chief executive Dov Charney, American Apparel continues to fight with its controversial founder

Elwood Chemicals Ltd has, as a result of its ongoing operations, contaminated the land on which it operates. There is no legal requirement to clean up the land.REQUIREDShould Elwood Chemicals Ltd recognize a liability?

Sandringham Mining Ltd has been mining in a particular coastal area. A requirement of the local Environmental Protection Authority is that the area be restored to a state that is beneficial to the local fauna.REQUIREDDoes a liability exist and, if so, when should a provision for restoration be

In an article entitled ‘Berry nasty’ that appeared in the Courier Mail on 15 February 2015 (by Greg Stolz), it was reported that people who had eaten a well-known brand of frozen berries were warned to watch for symptoms of hepatitis A. This followed at least five cases of people contracting

In a newspaper article of 8 November 2018 entitled ‘BHP faces $9b dam lawsuit’ (in The Australian Financial Review, by Will Willitts, p. 19), it was reported that BHP faces a £5 billion ($9 billion) lawsuit over the failure of the Samarco dam in Brazil in November 2015. Waste and sludge from

All things being equal, the managers of an organization would generally prefer to disclose a transaction as part of equity, rather than debt. Why?

Showing 1500 - 1600

of 7094

First

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

Last

Step by Step Answers