New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial accounting

Accountancy Financial Accounting Part 1 Textbook For Class 11 1st Edition NCERT - Solutions

Describe each of the following methods for measuring assets and liabilities: a. Historical cost b. Price-level-adjusted historical cost.c. Market value d. Value in use e liquidation value.

Compare the concepts of value in use and value in exchange.

For each of items 1–5 listed below, state whether, in accordance with existing accounting standards and the Framework, it would be recognised as: a. An asset b. A liability c. A contingent liability d. Revenue e. An expense f. None of the above.Items: 1. A

Argue both for, and against, the following proposition: ‘Historical cost accounting is irrelevant to users’ decision-making.

The general manager of Telco Limited is considering spending $15 million on the development of a new mobile phone that can also be used as a television. What conditions would need to be met before the $15 million can be recognised as an asset on the balance sheet?

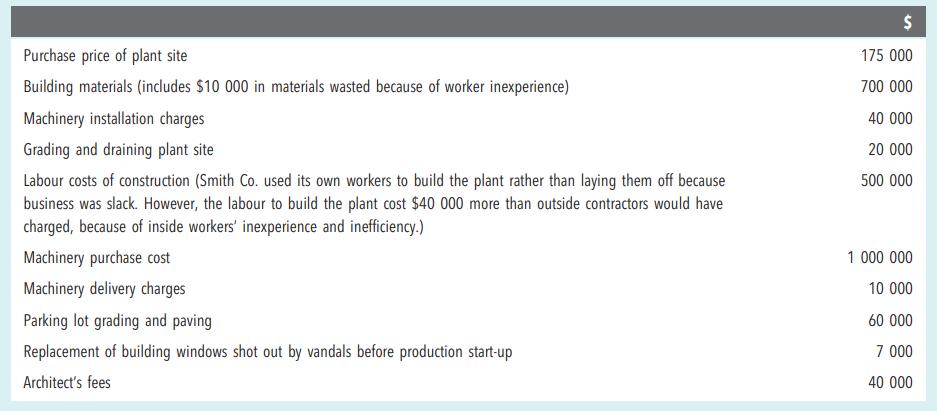

Determine the costs that would appear on the balance sheet of Smith Co. Ltd, in relation to land and a building, based on the following information: Purchase price of plant site Building materials (includes $10 000 in materials wasted because of worker inexperience) Machinery installation

Why is ethics so important to a profession? Is there really a necessity for ethical guidance for members of a profession?

The new accountant for Mactaggart Industries is wondering how to calculate the cost of a new machine the company has just installed. Explain briefly whether or not you think each of the following items should be part of the machine’s cost, and why: 1. The invoice price of the

State whether or not an asset should be recorded in the balance sheet of LMR Ltd as at 30 June 2019 in each of the following situations. Indicate the amount of the asset (if any) and any assumptions made. 1. On 15 May 2019, LMR Ltd paid $10 000 for an insurance premium. The premium covers

Go to the web page for a listed company, find its annual report and describe the contents of the CEO’s report.

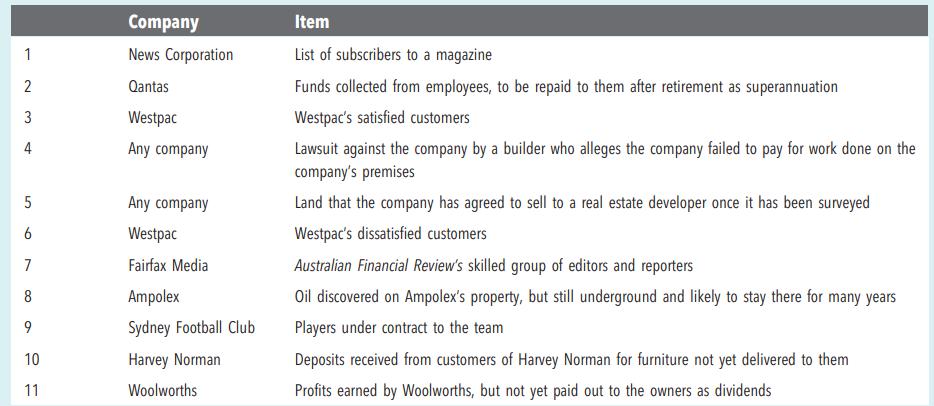

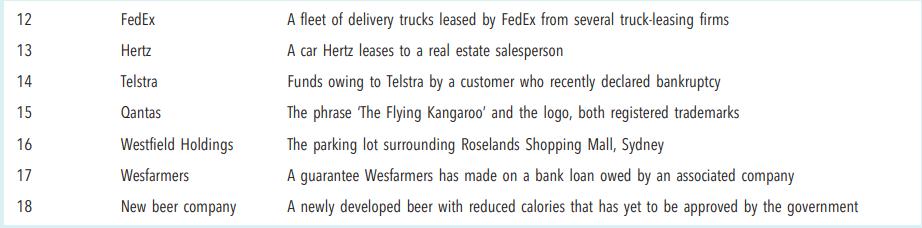

State whether or not, and why, each of the following items is likely to be an asset, a liability or an owners’ equity account (perhaps both an asset and a liability in some cases) of the company indicated: 1 2 3 4 5 6 7 8 9 10 11 Company News Corporation Qantas Westpac Any company Any

What purpose does the auditor’s report serve?

What are the types of audit reports, and what does each indicate to the users of financial statements?

Auditors play an important role in the financial reporting system, and their independence from their clients is an essential feature of this system. Why is such independence considered necessary? Why is it difficult to maintain?

Indicate whether each of the events described below results in a liability under the definitions and characteristics within the Framework. If so, show the amount of the liability. What would the liability be called? 1. A bank loan of $10 000 is obtained, with the company signing an agreement

Give examples of cases where there is a conflict of interest between preparers of financial statements and users of them.

Should a senior financial manager who works for a company, and is a professional accountant, have to meet the same standards of professional ethics as does a colleague who is an external auditor in public practice? Why, or why not?

Recently, there has been pressure to expand the role of auditors, because investors and other groups are demanding more forward-looking information. If these demands are met, auditors may be expected to review the plans and forecasts of a company that will be reporting to the public, and to

What is meant by the efficient market hypothesis?

Pat is the partner on the audit of Hardwood Emporium Ltd. Comment on whether or not, and why, each of the following may be a threat to Pat’s independence. 1. Pat and the chief financial officer of Hardwood Emporium play golf together every few weeks. 2. During the audit, Pat notices

What is the major purpose of a stock exchange?

For each of the following situations, state which of the fundamental principles have been breached: 1. Making a materially false statement 2. Two accountants on a plane after a few beers discussing future plans of a taxation client 3. Owning shares in an audit client 4.

Briefly describe two important implications capital market theory has for the use of accounting information.

It appears that some top managers attempt to manage their companies’ financial disclosure, including their financial accounting, to alter the story each disclosure tells. Why might managers be motivated to do this?

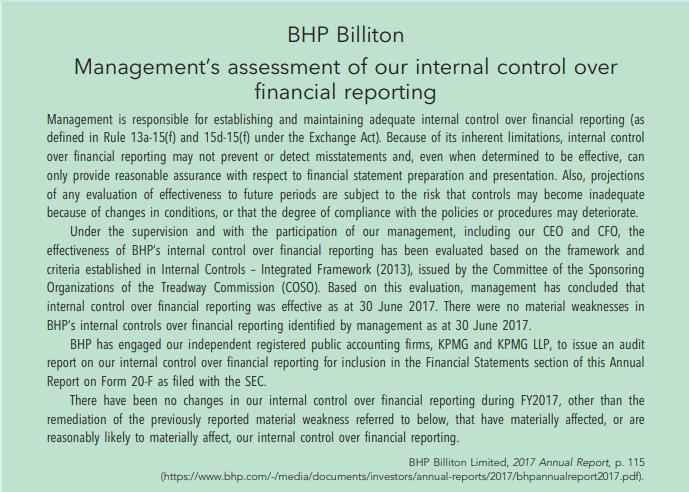

Following is an excerpt from the 2017 annual report of BHP Billiton.1. Who is responsible for internal control? 2. Why does BHP refer to the US Exchange Act? 3. Why can internal controls provide only reasonable assurance that business risks will be fully mitigated? BHP

Why should the shareholders of a large, publicly traded company want to have the company’s financial statements audited?

The auditor’s report is normally written using standard wording. The idea is that, if things are not all right, variations from the standard wording will alert users of the financial statements. Is that consistent, or inconsistent, with capital market theory?

Why is internal control over cash so critical?

What types of organisations need strong internal controls over inventory?

List four important internal controls over cash.

Provide three specific internal control procedures for: a cash b inventory c accounts receivable.

The proud owner of Beedle Ltd, a successful high-tech company, is very good at hiring and motivating excellent people to develop and sell products. Delegation is the key, says the owner. ‘Hire good people and get out of their way!’ As part of this philosophy, the owner hired the best

If a company is owed $100 000 by the bank, why would it appear as a DR in the company’s ledger accounts and a CR on the bank statement?

Why do outstanding (unpresented) cheques occur at month-end?

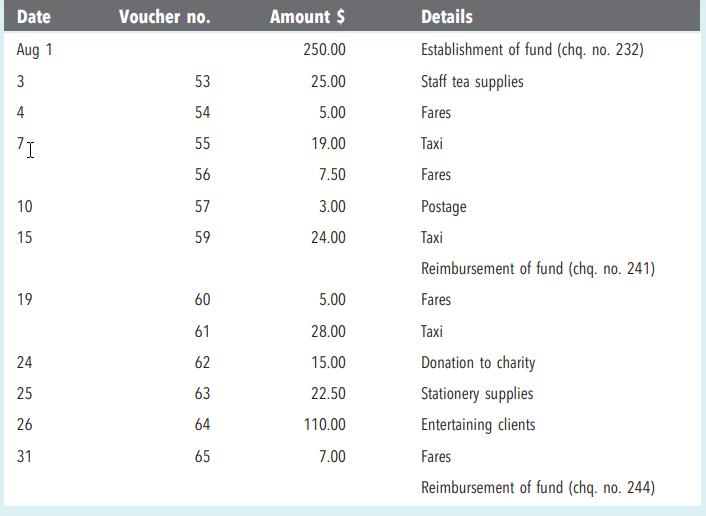

A petty cash fund of $250 was set up by Snodgrass Ltd on 1 August by drawing cheque no. 232. Transactions relating to petty cash in August were as follows:Prepare journal entries to record the transactions during August. Date Aug 1 3 4 ¹I 10 15 19 24 25 26 31 Voucher

‘No system of internal control is perfect. There are always inherent limitations.’ Discuss.

What does the concept of ‘reasonable assurance’ mean with respect to an internal control system?

ASB Limited received its bank statement for the month ending 30 June, and reconciled the statement balance to the 30 June balance in the cash account. The reconciled balance was determined to be $4800. The reconciliation included the following items:a. Deposits in transit were $2100. b.

The bank reconciliation of XYZ Ltd reveals a significant bank error in XYZ’s favour that will probably go undetected. As the accountant, you contact the general manager, who suggests that the bank has probably made errors in its favour in the past and that the bank should not be informed of its

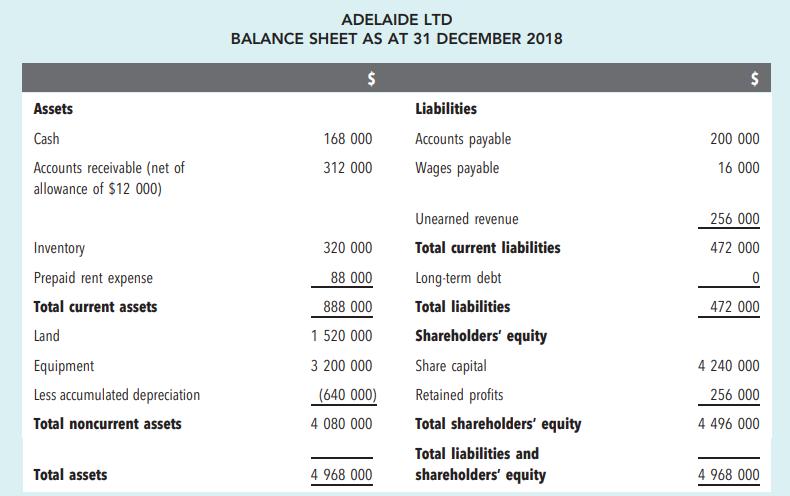

The following transactions occurred during the year ended 31 December 2019 for Adelaide Ltd: a. Issued share capital for $300 000 cash. b. Expiration of prepaid rent expense (i.e. prepaid rent expense balance to zero). c. Purchased $70 000 of inventory on credit. d. Paid $56 000

Discuss the relationship between the corporate manager’s responsibility for internal control and his or her responsibility to earn profit for the shareholders.

What effect would failure to make adjustments for accrued revenue have on the balance sheet and the income statement?

Provide examples of accounts that would be included under the heading ‘Receivables’ in the balance sheet.

A company has a $50 000 balance in the company’s accrued revenue account. Where would this account appear in the balance sheet?

Flimsy’s accounts receivable at the end of 2019 totalled $78 490. The allowance for doubtful debts had been $2310, but it was decided that this would be increased by $1560, then $1100 in unrecoverable accounts would be written off. i. What is the value of the receivables at the end of

Management of Sarah Limited are interested in the directional effect (i.e. increase, decrease or no effect) on net profit before tax and total assets for the year ended 30 June 2019, if the following occurred from January to June 2019. 1. Paying back a loan of $200 000. 2. Purchasing

Windjammer Technologies Ltd has been having difficulty collecting its accounts receivable. For the year 2019, the company increased the allowance for doubtful accounts by $53 000, bringing the balance to $74 000. At the end of 2019, accounts receivable equalled $425 000. When the year-end audit was

Why do companies have an allowance for doubtful debts?

Outline the income statement approach to calculating the bad debts expense.

OJ Ltd has been having difficulty collecting its accounts receivable. For the year 2019, the company increased the allowance for doubtful accounts by $48 000, bringing the balance to $70 000. At the end of 2019, accounts receivable equalled $425 000. When the year-end audit was being done, it was

Outline the balance sheet approach to calculating the allowance for doubtful debts. What is an important step to remember in this approach?

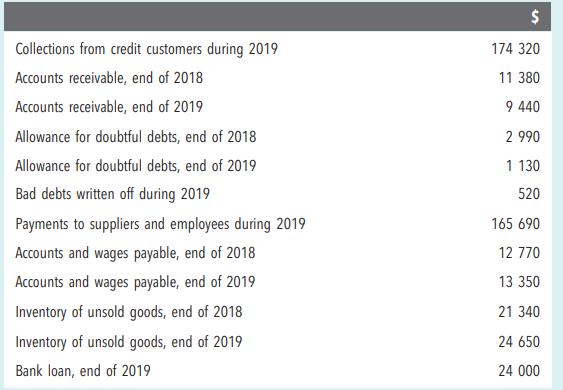

West Sonoma Ltd has just finished its 2019 financial year. From the following data, calculate net profit. The loan was taken out a month before the end of 2019 at an interest rate of 8 per cent. No interest has yet been paid, before tax, for 2019. Collections from credit customers during

What purposes are served by special journals? What control information could be made more readily available to management as a result of their use?

What considerations determine whether a special journal should be brought into use rather than placing entries in the general journal? Is the need for a general journal ever eliminated?

On what should you base your selection of the special analysis columns to be included in the cash payments journal?

Why should the sale of a fixed asset not be recorded in a simple sales journal?

If a customer’s account in the debtors’ ledger shows a credit balance, does this necessarily indicate that an error has been made?

Does the double-entry principle of an equal value of debits and credits in the system cease to apply when subsidiary ledgers are being employed?

Subsidiary ledgers involve unnecessary duplication, increase the opportunity for error and involve a breach of the double-entry principle. Under no circumstances can their use be justified.’ Comment critically.

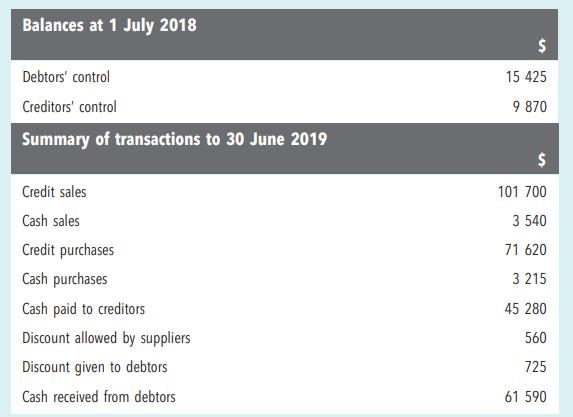

Prepare debtors’ and creditors’ control accounts for the year commencing 1 July 2018 from the following information: Balances at 1 July 2018 Debtors' control Creditors' control Summary of transactions to 30 June 2019 Credit sales Cash sales Credit purchases Cash purchases Cash paid to

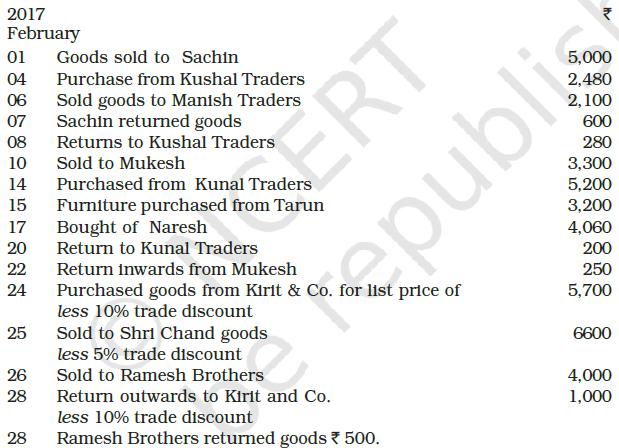

Prepare proper subsidiary books and post them to the ledger from the following transactions for the month of February 2017: 2017 February 01 04 06 07 08 10 14 15 17 20 22 24 25 26 28 28 Goods sold to Sachin Purchase from Kushal Traders Sold goods to Manish Traders Sachin returned goods Returns to

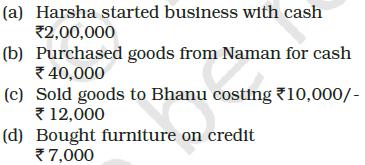

Prepare accounting equation on the basis of the following : (a) Harsha started business with cash *2,00,000 (b) Purchased goods from Naman for cash *40,000 (c) Sold goods to Bhanu costing *10,000/- 12,000 (d) Bought furniture on credit €7,000

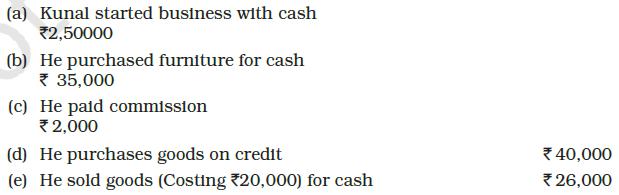

Prepare accounting equation from the following: (a) Kunal started business with cash *2,50000 (b) He purchased furniture for cash 35,000 (c) He paid commission 2,000 (d) He purchases goods on credit (e) He sold goods (Costing 20,000) for cash *40,000 *26,000

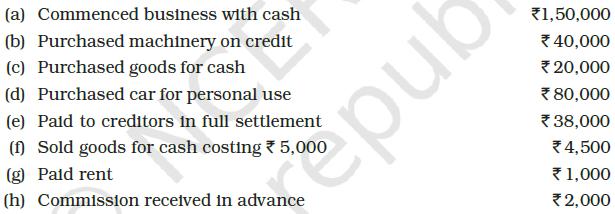

Rohit has the following transactions :Prepare the Accounting Equation to show the effect of the above transactions on the assets, liabilities and capital. (a) Commenced business with cash (b) Purchased machinery on credit (c) Purchased goods for cash (d) Purchased car for personal use (e) Paid to

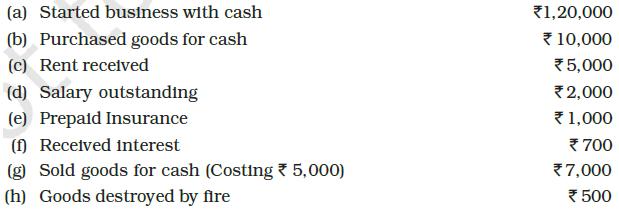

Use accounting equation to show the effect of the following transactions of M/s Royal Traders: (a) Started business with cash (b) Purchased goods for cash (c) Rent received (d) Salary outstanding (e) Prepaid Insurance (f) Received interest (g) Sold goods for cash (Costing 5,000) (h) Goods destroyed

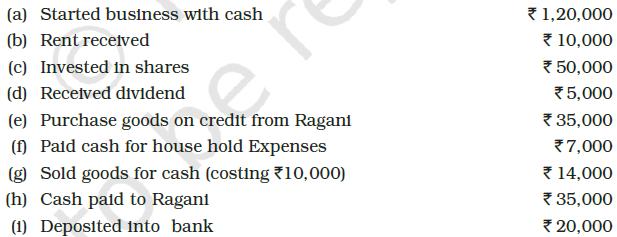

Show the effect of the following transactions on Assets, Liabilities and Capital through accounting equation: (a) Started business with cash (b) Rent received (c) Invested in shares (d) Received dividend 13 (e) Purchase goods on credit from Ragani (f) Paid cash for house hold Expenses (g) Sold

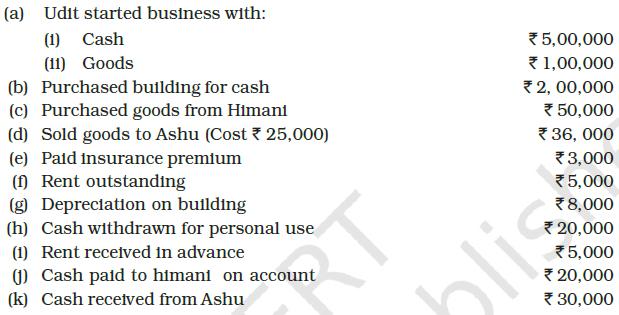

Show the accounting equation on the basis of the following transaction: (a) Udit started business with: (1) Cash (11) Goods (b) Purchased building for cash (c) Purchased goods from Himani (d) Sold goods to Ashu (Cost 25,000) (e) Paid insurance premium (f) Rent outstanding (g) Depreciation on

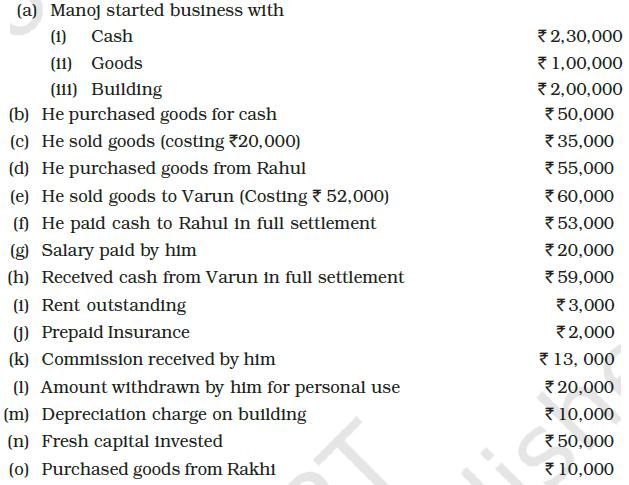

Show the effect of following transaction on the accounting equation: (a) Manoj started business with (1) Cash (11) Goods (111) Building (b) He purchased goods for cash (c) He sold goods (costing *20,000) (d) He purchased goods from Rahul (e) He sold goods to Varun (Costing * 52,000) (f) He paid

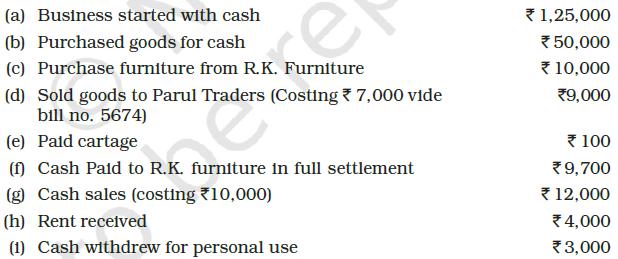

Transactions of M/s Vipin Traders are given below. Show the effects on Assets, Liabilities and Capital with the help of accounting Equation. (a) Business started with cash (b) Purchased goods for cash e coul (c) Purchase furniture from R.K. Furniture (d) Sold goods to Parul Traders (Costing *

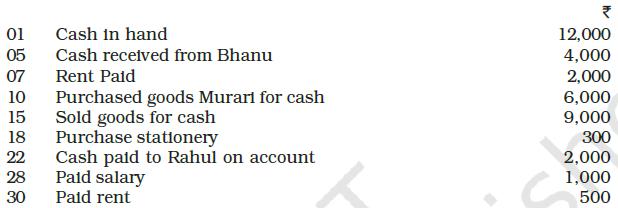

Enter the following transactions in a simple cash book for December 2016: 01 05 07 10 15 18 22 28 30 Cash in hand Cash received from Bhanu Rent Paid Purchased goods Murari for cash Sold goods for cash Purchase stationery Cash paid to Rahul on account Paid salary Paid

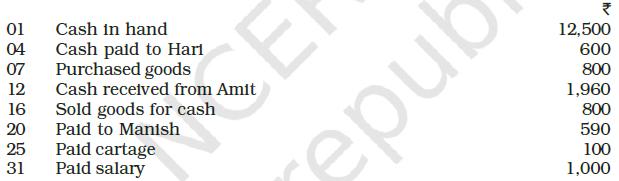

Record the following transaction in simple cash book for November 2016: 01 04 07 12 16 20 25 31 Cash in hand Cash paid to Hari Purchased goods E Cash received from Amit Sold goods for cash Paid to Manish Paid cartage Paid salary repub ₹ 12,500 600 800 1,960 800 590 100 1,000

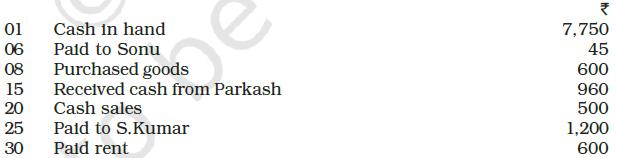

Enter the following transaction in Simple cash book for December 2017: 01 06 08 15 20 25 30 Cash in hand Paid to Sonu Purchased goods Received cash from Parkash Cash sales Paid to S.Kumar Paid rent ₹ 7,750 45 600 960 500 1,200 600

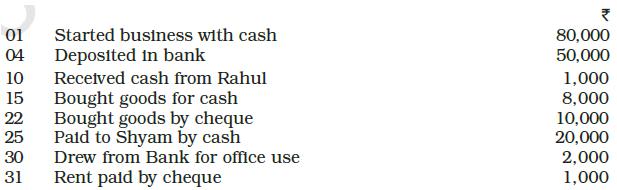

Record the following transactions in a bank column cash book for December 2016: 01 04 10 15 22 25 30 31 Started business with cash Deposited in bank Received cash from Rahul Bought goods for cash Bought goods by cheque Paid to Shyam by cash Drew from Bank for office use Rent paid by

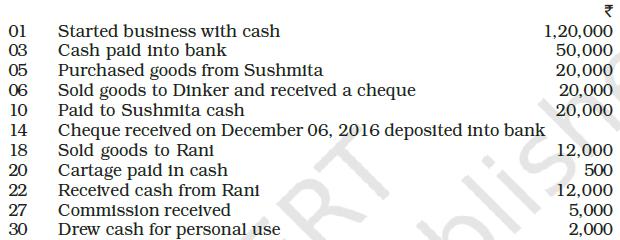

Prepare a double column cash book with the help of following information for December 2016: 01 Started business with cash Cash paid into bank 03 05 06 10 14 18 20 22 27 30 Purchased goods from Sushmita Sold goods to Dinker and received a cheque Paid to Sushmita cash Cartage paid in cash Received

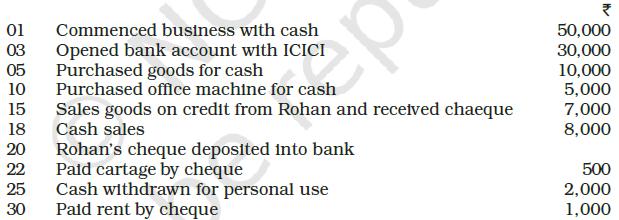

Enter the following transactions in double column cash book of M/s Ambica Traders for July 2017: P Sales goods on credit from Rohan and received chaeque Cash sales Rohan's cheque deposited into bank Paid cartage by cheque 25 Cash withdrawn for personal use 30 Paid rent by

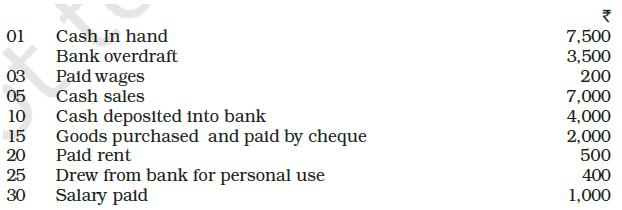

Prepare double column cash book from the following information for July 2017: 01 03 05 10 15 20 25 30 Cash In hand Bank overdraft Paid wages Cash sales Cash deposited into bank Goods purchased and paid by cheque Pald rent C Drew from bank for personal use Salary

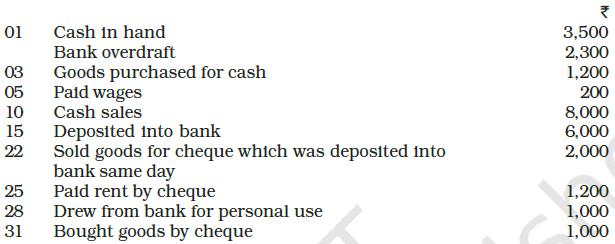

Enter the following transaction in a double column cash book of M/s.Mohit Traders for January 2017: Cash in hand Bank overdraft 03 Goods purchased for cash Paid wages Cash sales 01 05 10 15 22 25 28 31 Deposited into bank Sold goods for cheque which was deposited into bank same day Paid rent by

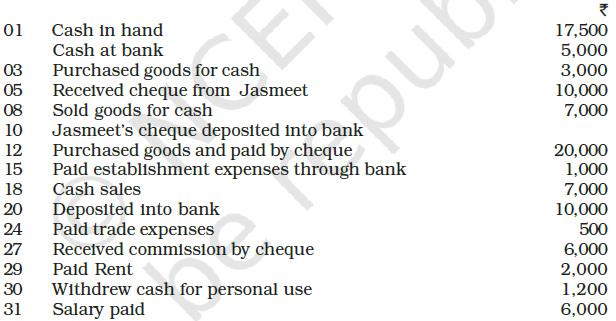

Prepare double column cash book from the following transactions for the year August 2017: 01 03 05 08 10 12 15 18 20 24 27 29 30 31 Cash in hand Cash at bank Purchased goods for cash Received cheque from Jasmeet Sold goods for cash Jasmeet's cheque deposited into bank Purchased goods and paid by

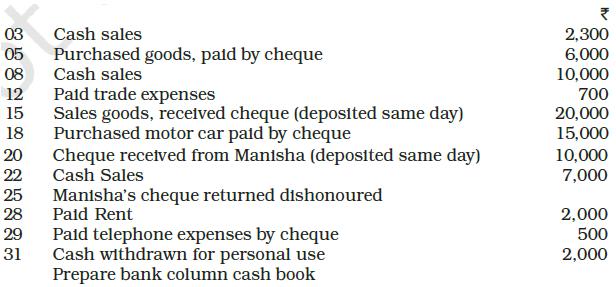

M/s Ruchi trader started their cash book with the following balances on July 2017: cash in hand ₹ 1,354 and balance in bank current account ₹ 7,560. He had the following transaction in the month of July 2017: 03 Cash sales 05 Purchased goods, paid by cheque 08 12 15 18 20 22 25 28 29 31 Cash

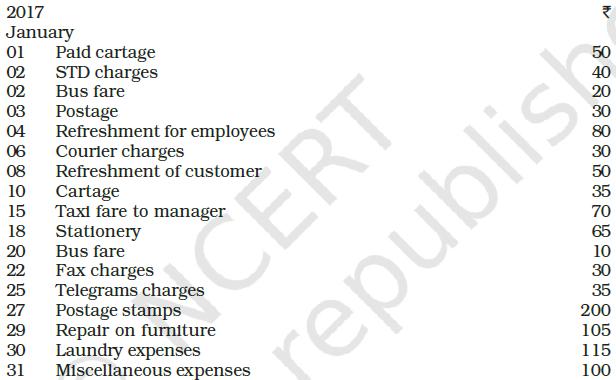

Prepare petty cash book from the following transactions. The imprest amount is ₹ 2,000. 2017 January 01 02 02 03 04 06 08 Refreshment of customer 10 15 18 20 22 25 27 29 Paid cartage STD charges Bus fare Postage Refreshment for employees Courier charges 30 31 Cartage Taxi fare to

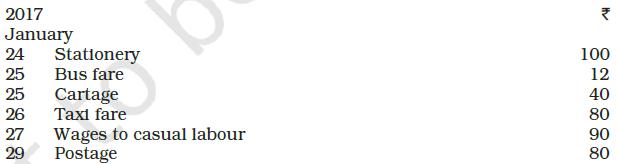

Record the following transactions during the week ending Dec.30, 2014 with a weekly imprest ₹ 500. 2017 January 24 Stationery Bus fare 25 25 26 27 29 Cartage Taxi fare Wages to casual labour Postage Itv 100 12 40 80 90 80

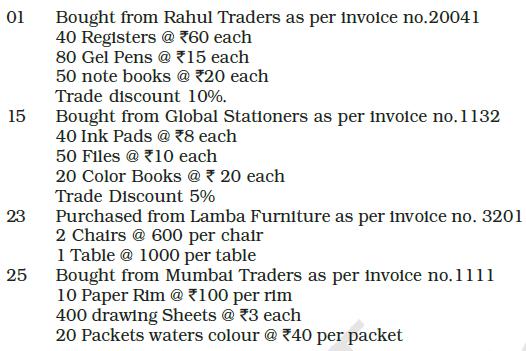

Enter the following transactions in the Purchase Journal (Book) of M/s Gupta Traders of July 2017: 01 15 23 25 Bought from Rahul Traders as per invoice no.20041 40 Registers @ ₹60 each 80 Gel Pens @ 15 each 50 note books @ ₹20 each Trade discount 10%. Bought from Global Stationers as per

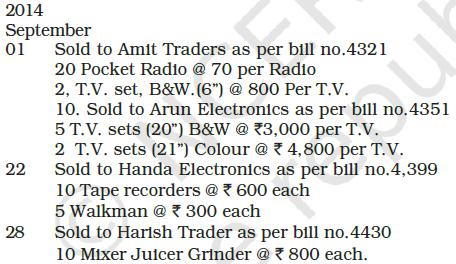

Enter the following transactions in sales (journal) book of M/s.Bansal electronics: 2014 September 01 22 28 Sold to Amit Traders as per bill no.4321 20 Pocket Radio @ 70 per Radio n 2, T.V. set, B&W. (6") @ 800 Per T.V. 10. Sold to Arun Electronics as per bill no.4351 5 T.V. sets (20") B&W @ 3,000

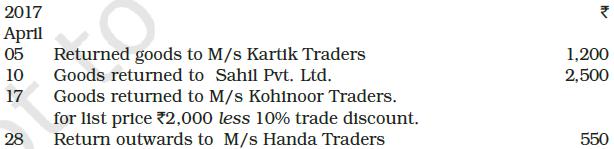

Prepare a purchases return (journal) book from the following transactions for April 2017. 2017 April 05 10 17 28 Returned goods to M/s Kartik Traders Goods returned to Sahil Pvt. Ltd. Goods returned to M/s Kohinoor Traders. for list price 2,000 less 10% trade discount. Return outwards to M/s Handa

Prepare Return Inward Journal (Book) from the following transactions of M/s Bansal Electronics for July 2017: 2017 July 04 M/s Gupta Traders returned the goods Goods returned from M/s Harish Traders M/s Rahul Traders returned the goods not as per 10 18 specifications Goods returned from Sushil

From the following particulars, prepare a bank reconciliation statement as at March 31, 2017.(i) Balance as per cash book ₹ 3,200(ii) Cheque issued but not presented for payment ₹ 1,800(iii) Cheque deposited but not collected upto March 31, 2014 ₹ 2,000(iv) Bank charges debited by bank ₹ 150

On March 31, 2017 the cash book showed a balance of ₹ 3,700 as cash at bank, but the bank passbook made up to same date showed that cheques for ₹ 700, ₹ 300 and ₹ 180 respectively had not presented for payment, Also, a cheque amounting to ₹ 1,200 deposited

The cash book shows a bank balance of ₹ 7,800. On comparing the cash book with passbook the following discrepancies were noted:(a) Cheque deposited in bank but not credited ₹ 3,000(b) Cheque issued but not yet present for payment ₹ 1,500(c) Insurance premium paid by the bank ₹

Bank balance of ₹ 40,000 showed by the cash book of Atul on December 31, 2016. It was found that three cheques of ₹ 2,000, ₹ 5,000 and ₹ 8,000 deposited during the month of December were not credited in the passbook till January 02, 2017. Two cheques of ₹ 7,000 and

On comparing the cash book with passbook of Naman it is found that on March 31, 2014, bank balance of ₹ 40,960 showed by the cash book differs from the bank balance with regard to the following:(a) Bank charges ₹ 100 on March 31, 2017, are not entered in the cash book.(b) On March 21,

Prepare bank reconciliation statement as on December 31, 2017. This day the passbook of Mr. Himanshu showed a balance of ₹ 7,000.(a) Cheques of ₹ 1,000 directly deposited by a customer.(b) The bank has credited Mr. Himanshu for ₹ 700 as interest.(c) Cheques for ₹

From the following particulars prepare a bank reconciliation statement showing the balance as per cash book on December 31, 2016.(a) Two cheques of ₹ 2,000 and ₹ 5,000 were paid into bank in October, 2016 but were not credited by the bank in the month of December.(b) A cheque of ₹ 800 which

Balance as per passbook of Mr. Kumar is 3,000.(a) Cheque paid into bank but not yet clearedRam Kumar ₹ 1,000Kishore Kumar ₹ 500(b) Bank Charges ₹ 300(c) Cheque issued but not presentedHameed ₹ 2,000Kapoor ₹ 500(d) Interest entered in the passbook but not entered in the cash book ₹ 100

The passbook of Mr. Mohit current account showed a credit Balance of ₹ 20,000 on dated December 31, 2016. Prepare a Bank Reconciliation Statement with the following information.(i) A cheque of ₹ 400 drawn on his saving account has been shown on current account.(ii) He issued two cheques of ₹

On 1st January 2017, Rakesh had an overdraft of ₹ 8,000 as showed by his cash book. Cheques amounting to ₹ 2,000 had been paid in by him but were not collected by the bank by January 01, 2017. He issued cheques of ₹ 800 which were not presented to the bank for payment up to that day. There

Prepare bank reconciliation statement.(i) Overdraft shown as per cash book on December 31, 2017 ₹ 10,000.(ii) Bank charges for the above period also debited in the passbook ₹ 100.(iii) Interest on overdraft for six months ending December 31, 2017 ₹ 380 debited in the passbook.(iv) Cheques

Kumar find that the bank balance shown by his cash book on December 31, 2017 is ₹ 90,600 (Credit) but the passbook shows a difference due to the following reason:A cheque (post dated) for ₹ 1,000 has been debited in the bank column of the cash book but not presented for payment. Also, a cheque

On December 31, 2017, the cash book of Mittal Bros. Showed an overdraft of ₹ 6,920. From the following particulars prepare a Bank Reconciliation Statement and ascertain the balance as per passbook.(1) Debited by bank for ` 200 on account of Interest on overdraft and ₹ 50 on account of charges

Prepare bank reconciliation statement of Shri Bhandari as on March 31, 2017(i) The Payment of a cheque for ₹ 550 was recorded twice in the passbook.(ii) Withdrawal column of the passbook under cast by ₹ 200(iii) A Cheque of ₹ 200 has been debited in the bank column of the Cash Book but it was

Overdraft shown by the passbook of Mr. Murli is ₹ 20,000. Prepare bank reconciliation statement on dated March 31, 2017.(i) Bank charges debited as per passbook ₹ 500.(ii) Cheques recorded in the cash book but not sent to the bank for collection ₹ 2,500.(iii) Received a payment directly from

Showing 2700 - 2800

of 7094

First

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

Last

Step by Step Answers