New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial institutions management

Financial Institutions Management A Risk Management 4th Edition Helen Lange, Anthony Saunders, Marcia Millon Cornett - Solutions

1.What are the three major sources of DI liquidity? What are the two major uses?

1.Go to the Reserve Bank of Australia’s website and update Tables 13.1 and 13.3 . Be prepared to discuss any changes in either the size and/or the maturity structures of the foreign exchange exposures.

1.Two multinational corporations enter their respective debt markets to issue $100 million of two-year notes. Firm A can borrow at a fixed annual rate of 11 per cent or a floating rate of LIBOR plus 50 basis points, repriced at the end of the year. Firm B can borrow at a fixed annual rate of 10 per

1.An FI has made a loan commitment of SF10 million that is likely to be taken down in six months. The current spot rate is $0.60/SF.Is the FI exposed to the dollar depreciating or the dollar appreciating? Why?If it decides to hedge using SF futures, should it buy or sell SF futures?If the spot rate

1.An FI must make a single payment of 500 000 Swiss francs (SF) in six months at the maturity of a CD. The FI’s in-house analyst expects the spot price of the franc to remain stable at the current $0.80/SF. But the analyst is concerned that it could rise as high as $0.85/SF or fall as low as

1.An FI has a $100 million portfolio of six-year Eurodollar bonds that have an 8 per cent coupon. The bonds are trading at par and have a duration of five years. The FI wishes to hedge the portfolio with T-bond options that have a delta of −0.625. The underlying long-term Treasury Bonds for the

1.An FI is planning to hedge its one-year $100 million Swiss franc (SF)-denominated loan against exchange rate risk. The current spot rate is$0.60/SF. A one-year SF futures contract is currently trading at $0.58/SF. SF futures are sold in standardised units of SF125 000.Should the FI be worried

1. An FI has assets denominated in UK pound sterling of A$125 million and sterling liabilities of A$100 million.What is the FI’s net exposure?Is the FI exposed to an A$ appreciation or depreciation?How can the FI use futures or forward contracts to hedge its FX rate risk?What is the number of

1. What technique is commonly used to estimate the hedge ratio? What statistical measure is an indicator of the confidence that should be placed in the estimated hedge ratio? What is the interpretation if the estimated hedge ratio is greater than one? Less than one? LO 13.8

1. What does the hedge ratio measure? Under what conditions is this ratio valuable in determining the number of futures contracts necessary to hedge fully an investment in another currency? How is the hedge ratio related to basis risk? LO 13.8

1. What is meant by ‘tailing the hedge’? What factors allow an FI manager to tail the hedge effectively? LO 13.8

1. An FI has an asset investment in euros. The FI expects the exchange rate of $/€ to increase by the maturity of the asset.Is the dollar appreciating or depreciating against the euro?To fully hedge the investment, should the FI buy or sell euro futures contracts?If there is perfect correlation

1. What factors may make the use of swaps or forward contracts preferable to the use of futures contracts for the purpose of hedging long-term foreign exchange positions? LO 13.8

1. A US money market mutual fund manager is looking for some profitable investment opportunities and observes the following one-year interest rates on government securities and exchange rates: r US = 12 per cent, r UK = 9 per cent, S = $1.50/£1, f = $1.6/£1, where S is the spot exchange rate and

1. An FI has $100 000 of net positions outstanding in UK pounds (£) and −$30 000 in Swiss francs (SF). The standard deviation of the net positions as a result of exchange rate changes is 1 per cent for the £ and 1.3 per cent for the SF. The correlation coefficient between the changes in

1. What is economic integration? What impact does the extent of economic integration of international markets have on the investment opportunities for FIs? LO 13.4, 13.5

1. What is the relationship between the real interest rate, the expected inflation rate and the nominal interest rate on fixed-income securities in any particular country? Refer to Table 13.6 . What factors may be the reasons for the relatively high correlation coefficients? LO 13.7

1. How does the lack of perfect correlation of economic returns between international financial markets affect the risk–return opportunities for FIs holding multicurrency assets and liabilities? LO 13.5

1. Assume that annual interest rates are 8 per cent in Australia and 4 per cent in Germany. An FI can borrow (by issuing one-year securities) or lend (by purchasing one-year securities) at these rates. The spot rate is $0.60/€1.If the forward rate is $0.64//€1, how could the FI arbitrage using

1. Explain the concept of interest rate parity. What does this concept imply about the long-run profit opportunities from investing in international markets? What market conditions must prevail for the concept to be valid? LO 13.7

1. Suppose that the current spot exchange rate of US dollars for Australian dollars, SUS$/ A $ , is .7590 (i.e. 0.759 dollars or 75.9 cents can be received for A$1). The price of Australian-produced goods increases by 5 per cent (i.e. inflation in Australia, IPA , is 5 per cent), and the US price

1. What is the purchasing power parity theorem? LO 13.7

1.How does the lack of perfect correlation of economic returns between international financial markets affect the risk–return opportunities for FIs holding multicurrency assets and liabilities? Refer to Table 13.6 . Which country pairings seem to have the highest correlation of equity and bond

1.A bank purchases a six-month $1 million Eurodollar deposit at an annual interest rate of 6.5 per cent. It invests the funds in a six-month Swedish krona bond paying 7.5 per cent per year. The current spot rate is $0.18/SK1.The six-month forward rate on the Swedish krona is being quoted at

1.Brumby Bank has been borrowing in the Australian markets and lending abroad, thus incurring foreign exchange risk. In a recent transaction, it issued $2 million in one-year securities at 6 per cent and funded a loan in euro at 8 per cent. The spot rate for the euro was €1.45/$1 at the time of

1.What are the two primary methods of hedging FX risk for an FI? What two conditions are necessary to achieve a perfect hedge through on-balancesheet hedging? What are the advantages and disadvantages of off-balance-sheet hedging in comparison to on-balance-sheet hedging? LO 13.6

1.What motivates FIs to hedge foreign currency exposures? What are the limitations to hedging foreign currency exposures? LO 13.6

1.Highlanders Bank recently made a one-year NZ$10 million loan that pays 10 per cent interest annually. The loan was funded with a eurodenominated one-year deposit at an annual rate of 8 per cent. The current spot rate is €1.60/$1.What will be the net interest income in dollars on the one-year

1.Sun Bank of Byron Bay has purchased a €16 million one-year loan that pays 12 per cent interest annually. The spot rate for euro is €1.60/$1. Sun Bank has funded this loan by accepting a UK pound- (GBP) denominated deposit for the equivalent amount and maturity at an annual rate of 10 per

1.City Bank issued $200 million of one-year CDs in the United States at a rate of 6.50 per cent. It invested part of this money, $100 million, in the purchase of a one-year bond issued by an Australian firm at an annual rate of 7 per cent. The remaining $100 million was invested in a one-year

1.What are the four FX trading activities undertaken by FIs? How do FIs profit from these activities? What are the reasons for the slow growth in FX profits at major banks? LO 13.4

1.The following are the foreign currency positions of an FI, expressed in dollars.What is the FI’s net exposure in euros?What is the FI’s net exposure in UK pounds?What is the FI’s net exposure in Japanese yen?What is the expected loss or gain if the € exchange rate appreciates by 1 per

1.What two factors directly affect the profitability of an FI’s position in a foreign currency? LO 13.4

1.X-IM Bank has SF14 million in assets and SF23 million in liabilities and has sold SF8 million in foreign currency trading. What is the net exposure for X-IM? For what type of exchange rate movement does this exposure put the bank at risk? LO 13.2

1.On 16 July 2015, you convert $500 000 Australian dollars to Japanese yen in the spot foreign exchange market and purchase a one-month forward contract to convert yen into dollars. How much will you receive in US dollars at the end of the month if the forward rate is 0.010603? Use the data in

1.What is the spot market for FX? What is the forward market for FX? What is the position of being net long in a currency? LO 13.1

1.What are the four FX risks faced by FIs? LO 13.2

1.What are two ways in which an FI manager can control FX exposure?

1.The cost of one-year Australian dollar securities is 8 per cent, one-year Australian dollar loans yield 10 per cent, and UK sterling loans yield 15 per cent. The dollar/pound spot exchange is $1.50/£1, and the one-year forward exchange rate is $1.48/£1. Are one-year Australian dollar loans more

1.Suppose in Table 13.8 that the Australian bank had agreed to make floating payments of BBSW + 1 per cent instead of BBSW + 2 per cent. What would its net payment have been to the UK bank over the four-year swap agreement?

1.Referring to the fixed–fixed currency swap in Table 13.6 , if the net cash flows on the swap are zero why does either FI enter into the swap agreement?

1.If an FI has to hedge a $5 million liability exposure in Swiss francs (SF), what options should it purchase to hedge this position?

1.What is the difference between options on foreign currency and options on foreign currency futures?

1.In running a regression of ΔSt on Δft , the regression equation is ΔSt = 0.51 + 0.95 Δft and R 2 = 0.72. What is the hedge ratio? What is the measure of hedging effectiveness?

1.Circle an observation in Figure 13.5 that shows futures price changes exceeding spot price changes.Suppose the R 2 = 0 in a regression of ΔSt . Would you still use futures contracts to hedge? Explain your answer.

1.What are two ways in which an FI manager can control FX exposure?

1.The cost of one-year Australian dollar securities is 8 per cent, one-year Australian dollar loans yield 10 per cent, and UK sterling loans yield 15 per cent. The dollar/pound spot exchange is $1.50/£1, and the one-year forward exchange rate is $1.48/£1. Are one-year Australian dollar loans more

1.What is the interest rate parity condition? How does it relate to the existence or non-existence of arbitrage opportunities?

1.What is purchasing power parity?

1.What is the source of most profits and losses on FX trading? What foreign currency activities provide a secondary source of revenue?\

1.In which trades do FIs normally act as agents and in which trades as principals?

1.What are the four major FX trading activities?

1.A bank has £10 million in assets and £7 million in liabilities. It has also bought £52 million in foreign currency trading. What is its net exposure in pounds? (£55 million)

1.If a bank is long in UK pounds (£), does it gain or lose if the dollar appreciates in value against the pound?

1.How is the net foreign currency exposure of an FI measured?

1.What is the difference between a spot and forward foreign exchange market transaction?

1.Go to the World Bank website (www.worldbank.org ) and find the number of bank loans outstanding in Brazil and China. To do this, click on ‘data and research’. Under ‘data programs’, click on ‘joint external debt hub’. Click ‘go’ and then click ‘creditor/market’. Under

1.Go to the Heritage Foundation website (www.heritage.org ) and find the most recent Economic Freedom Index for Australia, by clicking on ‘explore the data’. This will download a file that contains the relevant data. What factors led to this rating? LO 12.3

1.A bank was expecting to receive $100 000 from its customer based in Singapore. Since the customer has problems repaying the loan immediately, the bank extends the loan for another year at the same interest rate of 10 per cent. However, in the rescheduling agreement, the bank reserves the right to

1.A $20 million loan outstanding to the Nigerian government is currently in arrears with City Bank. After extensive negotiations, City Bank agrees to reduce the interest rate from 10 per cent to 6 per cent and to lengthen the maturity of the loan to 10 years from the present five years remaining to

1.A bank is in the process of renegotiating a three-year non-amortising loan. The principal outstanding is $20 million, and the interest rate is 8 per cent.The new terms will extend the loan to 10 years at a new interest rate of 6 per cent. The cost of funds for the bank is 7 per cent for both the

1.A bank is in the process of renegotiating a loan. The principal outstanding is $50 million and is to be paid back in two instalments of $25 million each, plus interest of 8 per cent. The new terms will stretch the loan out to five years with no principal payments except for interest payments of 6

1.How would the restructuring, such as rescheduling, of sovereign bonds affect the interest rate risk of the bonds? Is it possible that such restructuring would cause the FI’s cost of capital not to change? Explain. LO 12.6

1.Which variables typically are negotiation points in an LDC multi-year restructuring agreement (MYRA)? How do changes in these variables provide benefits to the borrower and to the lender? LO 12.6

1.What is ‘concessionality’ in the process of rescheduling a loan? LO 12.6

1.Zlick Company plans to invest $20 million in Chile to expand its subsidiary’s manufacturing output. Zlick has two options. It can convert the $20 million at the current exchange rate of 410 pesos to a dollar (i.e. P410/$1), or it can engage in a debt-for-equity swap with its bank City Bank by

1.Chase Bank holds a $200 million loan to Argentina. The loans are being traded at bid–offer prices of 91–93 per 100 in the London secondary market.If Chase has an opportunity to sell this loan to an investment bank at a 7 per cent discount, what are the savings after taxes compared to the

1.What are the risks to an investing company participating in a debt-for-equity swap? LO 12.6

1.Identify and describe the four market segments of the secondary market for LDC debt. LO 12.5

1.Who are the primary sellers of LDC debt? Who are the buyers? Why are FIs often both sellers and buyers of LDC debt in the secondary markets? LO 12.5

1.What are the benefits and costs of rescheduling to the following:a borrower a lender. LO 12.2

1.What is systematic risk in terms of sovereign risk? Which of the variables often used in statistical models tend to have high systematic risk? Which variables tend to have low systematic risk? LO 12.3

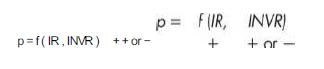

1.Explain the following relation:where:p = Probability of rescheduling IR = Total imports/Total foreign exchange reserves INVR = Real investment/GNP LO 12.3 , 12.4 p=f(IR, INVR) ++ or - p = F(IR, INVR) + +or

1.The average σ ER 2 (or VAREX = variance of export revenue) of a group of countries has been estimated at 20 per cent. The individual VAREX of two countries in the group, Holland and Singapore, has been estimated at 15 per cent and 28 per cent, respectively. The regression of individual country

1.How do price and quantity risks affect the variability of a country’s export revenue? LO 12.3 , 12.4

1.What shortcomings are introduced by using traditional CRA models and techniques? In each case, what adjustments are made in the estimation techniques to compensate for the problems? LO 12.3

1.Countries A and B have exports of $2 billion and $6 billion, respectively. The total interest and amortisation on foreign loans for both countries are $1 billion and $2 billion, respectively.What is the debt service ratio (DSR) for each country?Based only on this ratio, to which country should

1.An FI manager has calculated the following values and weights to assess the credit risk and likelihood of having to reschedule a loan. From the Zscore calculated from these weights and values, is the manager likely to approve the loan? Validation tests of the Z-score model indicated that scores

1.What types of variables normally are used in a CRA Z-score model? Define the following ratios and explain how each is interpreted in assessing the probability of rescheduling.Debt service ratio Import ratio Investment ratio Variance of export revenue Domestic money supply growth LO 12.3 , 12.4

1.What three country risk assessment models are available to investors? How is each model compiled? LO 12.3

1.Identify and explain at least four reasons why rescheduling debt in the form of loans is easier than rescheduling debt in the form of bonds. LO 12.2

1.What is the difference between debt rescheduling and debt repudiation and why is this distinction important? LO 12.2

1.What risks are incurred in making loans to borrowers based in foreign countries? Explain. LO 12.1 , 12.2

1.How does the secondary market for LDC debt improve the liquidity of LDC funding?

1.How can the secondary market for LDC debt assess sovereign risk?

1.Which sovereign risk indicators are the most important for a large FI: those with a high or those with a low systematic element?

1.What are the major problems involved with using traditional CRA models and techniques?

1.What variables are most commonly included in sovereign risk prediction models? What does each one measure?

1.Are the credit ratings of countries in the Institutional Investor rating scheme forward looking or backward looking?

1.Provide four reasons why we see sovereign loans being rescheduled rather than repudiated.

1.What is the difference between debt repudiation and debt rescheduling?

1.In deciding to lend to a party residing in a foreign country, what two considerations must an FI weigh?

1.What is the difference between credit risk and sovereign risk?

1.Go to your central bank’s website to see how recommendations from the BIS are being implemented in your country. LO 11.5MC Financial does not want to deviate from the national average by more than 12.25 per cent.Loan loss ratio-based model Based on regression analysis on historical loan losses,

1.Go to the BIS website and review any recent papers dealing with the implementation of risk-based models for measuring loan portfolio risk. LO 11.5

1.An FI has a loan portfolio of 10 000 loans of $10 000 each. The loans have a historical average default rate of 4 per cent and the severity of loss is 40 cents per $1.Over the next year, what are the probabilities of having default rates of 2, 3, 4, 5 and 8 per cent?What would be the dollar loss

1.How does the Credit Risk3 model of Credit Suisse Financial Products differ from the CreditMetrics model of JPMorgan Chase?

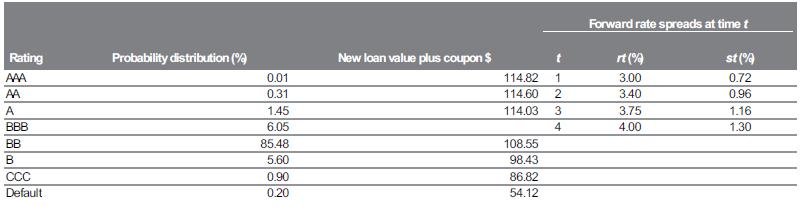

1.A five-year fixed-rate loan of $100 million carries a 7 per cent annual interest rate. The borrower is rated BB. Based on hypothetical historical data, the probability distribution given below has been determined for various ratings upgrades, downgrades, status quo and default possibilities over

1.Refer to the example information in Appendix 11A.From Table 11A.1, what is the probability of a loan upgrade? A loan downgrade?What is the impact of a rating upgrade or downgrade?How is the discount rate determined after a credit event has occurred?Why does the probability distribution of

1.An FI has a concentration of home mortgages and is feeling exposed to increasing interest rates and the impact that this may have on the default characteristics of the mortgage portfolio. How may loan sales and/or securitisation assist the FI to diversify their portfolio? LO 11.12 The following

Showing 1900 - 2000

of 4618

First

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

Last

Step by Step Answers