New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial reporting

Financial Reporting 4th Edition Janice Loftus, Ken Leo, Sorin Daniliuc, Belinda Luke, Hong Nee Ang, Mike Bradbury, Dean Hanlon, Noel Boys, Karyn Byrnes - Solutions

Gold Ltd classifies its exploration and evaluation assets as intangible assets. A new accountant has just been employed and has suggested that Gold Ltd should change its accounting policy for exploration and evaluation assets from its existing cost model to the fair value model under AASB 138/IAS

Oil Sands Ltd is a company involved in the search for, production of and sale of oil and gas resources. The company has been following an accounting policy of expensing its exploration and evaluation costs as incurred since adoption of AASB 6/IFRS 6. However, its most significant competitor follows

Mining Ltd has acquired a licence to explore a new area of interest and its accounting policy is to capitalise its exploration and evaluation expenditures on an area of interest basis. During the period, costs have been incurred in relation to:(a) the acquisition of speculative seismic data in

During the year ended 30 June 2024, the management of LPG Ltd has been analysing its engineering reports for a specific area of interest, which indicate that sample drilling has not resulted in any findings that confirm the existence of oil and gas in that area. As a result, LPG Ltd is reluctant to

Distinguish between a direct and an indirect acquisition.

Distinguish between a business combination and a non-business acquisition.

What constitutes a business?

What key conditions must be satisfied in order for a business combination to occur?

What is the acquisition date?

How are the identifiable assets and liabilities acquired in a business combination measured?

What is meant by ‘deferred consideration’ and how is it accounted for?

What are acquisition-related costs and how are they accounted for?

Hikoi Ltd has recently undertaken a negotiations to acquire 70% of shares of Hapu Ltd.At the start of negotiations, Hikoi Ltd owned 30% of the shares of Hapu Ltd. The negotiations began on 1 January 2023 and enough shareholders in Hapu Ltd agreed to the deal by 30 September 2023. The agreement was

Ataahua Ltd has acquired a major manufacturing division from Yemba Ltd. The accountant, Mr Zhen, has shown the board of directors of Ataahua Ltd the financial information regarding the acquisition. Mr Zhen calculated a residual amount of $45 000 to be reported as goodwill in the accounts. The

What are the consolidated financial statements?

What is a group, a parent and a subsidiary?

How many parents can a group have?

Why do the regulators require the parent entity to prepare consolidated financial statements for a group?

What are the key elements of control over an investee?

What are the four characteristics of power according to AASB 10/IFRS 10?

What are ‘relevant’ activities related to the existence of power over an investee?

Give examples of the rights of an investor that determine the existence of power over the investee.

What is the link between voting rights, ownership interest (i.e. percentage of shares held by the investor in the investee) and control?

Give examples of factors to consider in determining the existence of power when the investor holds less than 50% of the voting shares of an investee.

What are substantive rights and protective rights?

What are variable returns?

What is an agent and a principal?

Describe the consolidation process.

Which entities are required to prepare consolidated financial statements and which entities are exempted?

What is an investment entity?

What needs to be disclosed according to AASB 12/IFRS 12 for each subsidiary where a non-controlling interest exists?

What needs to be disclosed according to AASB 12/IFRS 12 in relation to structured entities?

When does a parent need to prepare separate financial statements according to AASB 127/IAS 27?

What needs to be disclosed in the separate financial statements prepared by a parent according to AASB 127/IAS 27?

Briefly describe the consolidation process in the case of a parent that has a wholly owned subsidiary.

Explain the initial adjustments that may be required before undertaking the consolidation process.

Explain the adjustments that may be required as part of the consolidation process.

If the parent assesses that some of the subsidiary’s identifiable assets and liabilities are not recorded by the subsidiary at acquisition date, explain why adjustments to these assets and liabilities are required in the preparation of the consolidated financial statements.

Explain what the business combination valuation reserve is.

Explain the impact on the acquisition analysis of a previously held investment by the parent in the subsidiary.

If the subsidiary has recorded goodwill in its records at acquisition date, how does this affect the acquisition analysis, the business combination valuation entries and the pre-acquisition entries?

Explain why and how the business combination valuation entries for inventories will be adjusted in subsequent periods after the acquisition date.

Explain why and how the business combination valuation entries for non-current assets will be adjusted in subsequent periods after the acquisition date.

Explain why and how the business combination valuation entries for liabilities will be adjusted in subsequent periods after the acquisition date.

Explain why and how the pre-acquisition entries will be adjusted in subsequent periods after the acquisition date.

Using an example, explain how the business combination entries affect the preacquisition entries, both at acquisition date and in the subsequent periods.

Explain the choices that may be available to revalue the identifiable assets recorded by the subsidiary at carrying amounts different from fair value at the acquisition date

At acquisition date, the subsidiary may have the choice to revalue or not in its own accounts the identifiable assets previously recorded at carrying amounts different from fair value. Discuss how the business combination entries and the pre‐acquisition entries will be affected by this choice.

Tiwi Ltd has acquired all the shares of Boon Ltd. The accountant for Tiwi Ltd, Ms Gupta, having studied the requirements of AASB 3/IFRS 3 Business Combinations, realises that all the identifiable assets and liabilities of Boon Ltd must be recognised in the consolidated financial statements at fair

The accountant for Birrarung Ltd, Ms Wei, has sought your advice on an accounting issue that has been puzzling her. When preparing the acquisition analysis relating to Birrarung Ltd’s acquisition of Kakadu Ltd, she calculated that there was a gain on bargain purchase of $25 000. Being unsure of

Wiradjuri Ltd is a Queensland software developer that specialises in software that controls mining operations. To exploit opportunities in the US market, Wiradjuri Ltd has established a foreign operation, Opencut Inc., in Austin, Texas. The operations of Opencut Inc. essentially involve the

Dharug Ltd is an Australian company with two foreign operations, one in Indonesia and the other in South Korea. The Indonesian operation has as its major activity the distribution in Indonesia of Dharug Ltd’s products. It has been agreed that the Indonesian operation will, for a period of time,

Explain the financial reporting issue that arises when a company enters into foreign currency transactions. Provide examples of various foreign currency transactions and indicate whether each transaction involves the initial recognition of a monetary item or non-monetary item or both.

Explain how the items that arise from foreign currency transactions are translated into the functional currency on initial recognition in the accounting records.

Describe how the transaction date is determined for the purpose of initially recognising items arising from foreign currency transactions.

Provide an overview of the accounting requirements of AASB 121/IAS 21 in relation to foreign currency transactions and exchange differences.

Describe how monetary items designated in a foreign currency are subsequently remeasured under AASB 121/IAS 21? At what dates does the remeasurement occur?

Describe the conditions under which non-monetary items designated in a foreign currency are subsequently remeasured under AASB 121/IAS 21?

Explain what is meant by the term ‘qualifying asset’ in the context of foreign currency transactions. Describe the accounting treatment for exchange differences that relate to qualifying assets.

Describe the accounting treatment for exchange differences that relate to revalued assets.

How can forward exchange contracts be used to manage foreign exchange risk?

Describe the accounting treatment for a forward exchange contract where there is no hedging relationship.

Explain how the fair value of a forward contract is measured at inception date, at the end of the reporting period and at settlement date.

Distinguish between a fair value hedge and a cash flow hedge that uses a forward exchange contract as the hedging instrument. Describe the accounting treatment of any gains or losses on a forward contract that qualifies for hedge accounting.

Describe the disclosures relating to foreign currency transactions required in the financial report.

You are the technical accounting consultant of a professional accounting firm. One of your clients is an Australian travel company that arranges package tours to overseas destinations. The client states: ‘When we arrange accommodation in foreign hotels we recognise a liability at the spot rate.

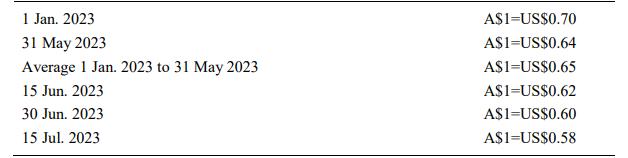

Koala Ltd is an Australian company that receives management consulting services from Spin Incorporated. On 15 June 2023, Koala Ltd received an invoice from Spin Incorporated amounting to US\($4\) million for services provided over the period 1 January 2023 to 31 May 2023. On 15 July 2023, Koala Ltd

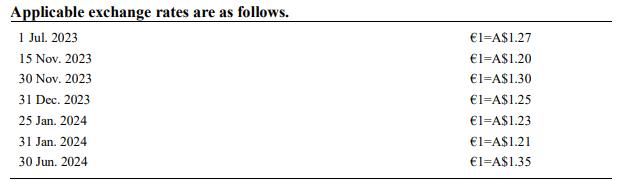

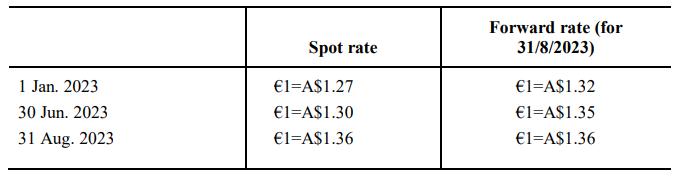

Mara Ltd is an Australian company. The functional currency of Mara Ltd is A$. It has reporting periods ending on 31 December and 30 June. During the year ended 30 June 2024, Mara Ltd entered into various foreign currency transactions in Euros (€) as follows.(a) On 15 November 2023, Mara Ltd

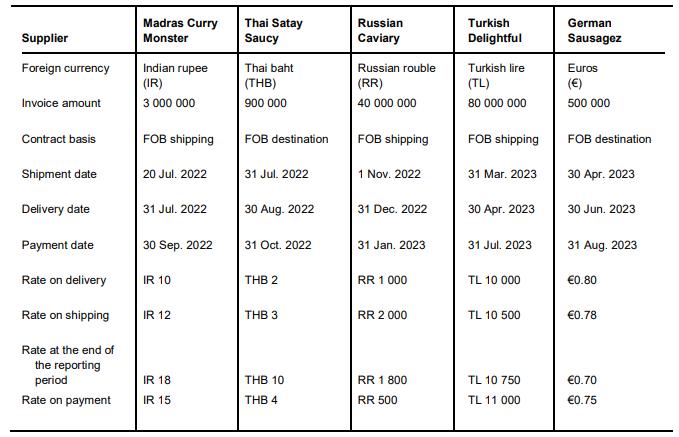

You are the financial controller of Waru Ltd, an Australian company listed on the ASX that distributes imported food products in the local market. The functional currency of Waru Ltd is A\($.\) Waru Ltd’s purchases of inventories in foreign currency during the year ended 30 June 2023 are set out

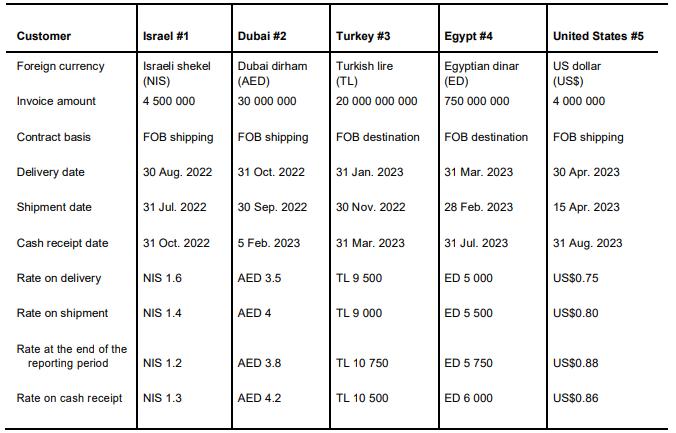

You are the financial controller of Garla Ltd, an Australian company listed on the ASX that sells premium Australian wines into overseas markets. Garla’s sales of inventories in foreign currency during the year ended 30 June 2023 are set out below. Exchange rates at delivery date, shipment date,

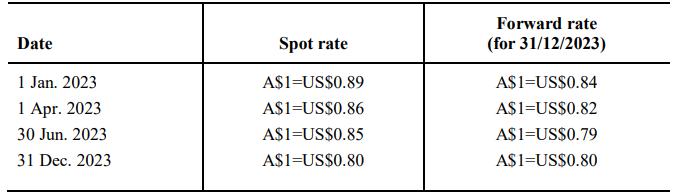

On 1 July 2023, Yananga Ltd, an Australian company that has A$ as its functional currency, enters a loan agreement with a lender in Hong Kong to borrow HK\($700\) 000 and uses the funds to acquire components for construction of a warehouse. By 31 December 2023, when the warehouse is ready to

On 1 January 2023, Bunji Ltd, an Australian company that has A$ as its functional currency, enters into a forward exchange contract to sell €300 000 on 31 August 2023. The forward contract is designated as a hedge for a sales transaction of €300 000 that Bunji Ltd expects to have with a German

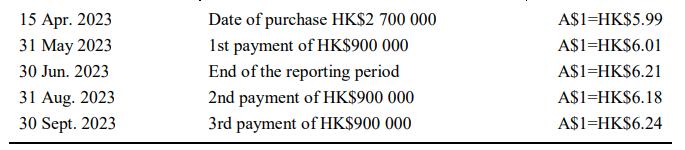

You are the finance director of the Australian listed company, Yidaki Ltd that has A$ as the functional currency. Yidaki Ltd purchases goods from Hong Kong and has borrowings from a US bank. The company’s financial year ends on 30 June2023. . Yidaki Ltd entered the following transactions during

Why are financial statements translated from one currency to another?

Discuss the primary economic indicators used to determine the functional currency of an entity?

Discuss the financing indicators used to determine the functional currency of an entity?

Discuss the activity indicators used to determine the functional currency of an entity?

What are the two possible translation processes that may be necessary to translate a foreign operation’s financial statements?

Why does an exchange difference arise and how it is recognised under the temporal method of translation used to translate financial statements of foreign operations?

What is meant by ‘presentation currency’?

Discuss the disclosures required by AASB 121/IAS 21 with regards to exchange differences, functional currency and the currency used by an entity to present its financial information.

Related party transactions are an every-day occurrence. What is so special about them that standard setters formulate rules for the disclosure?

Laura states "Our company's transactions with related parties are all at arm's length prices, so I do not see why we need to have related party disclosures".

Why is a company controlled by a person who is a key management personnel considered a related party?

Choose the most recent annual report of two Australian or New Zealand publicly listed companies (other than Woolworths Group Ltd). Locate the remuneration report and the financial statement notes dealing with related party disclosures. Compare the details provided by each company. Do you consider

A partner in your firm has just been offered an appointed to the board of a public listed company that is significantly owned by an overseas shareholder. She has asked you to write her some notes about the Mainzeal court case. Specifically, she has asked you:(1) Briefly, what are the facts of the

Elaine Chan is a newly appointed director of Elite Sports Ltd, a listed company that organises major sporting events. Elaine has provided consultancy services to Elite Sports Ltd for the past 3 years. In the most recent financial year these services amounted to $50 000.Required Determine whether

The Golden Pairs Company operates a pension scheme that offers defined benefit pensions for the benefit of the company’s employees and their spouses. At the end of the reporting period, the present value of the defined benefit obligation is \($90\) million and the fair value of the defined

Hasan holds 100% of the shares in Behmoth Ltd and he is also a director of Lion Ltd. All of the shares in Lion Ltd are held by Singa Ltd.Required Determine the related party relationships for each company.

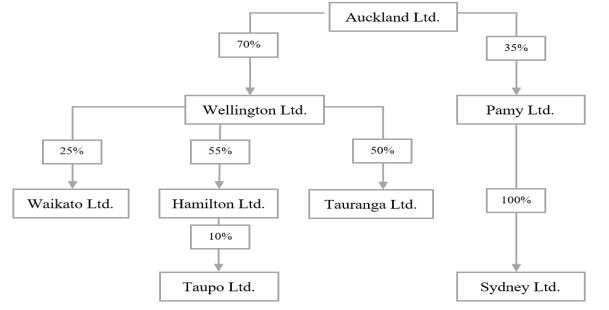

Consider the following corporate structure diagram and the additional information which follows.The entities engaged in the following financial transactions during the period under consideration:• Auckland Ltd. made sales worth $ 25,000 to Pamy Ltd. on account, the amount is still receivable.•

Which of the following is a related party transaction and, under AASB 124/IAS 24, requires disclosure in the annual financial statements?(a) A performance-related amount paid to the directors of the entity.(b) A loan for $100 000 that was made to a retired director of an entity, and which was

Explain, with reasons, whether or not each of the following is a disclosable related party transaction of Alpha Ltd under NZ IAS 24:• Alpha Limited stores inventory in a warehouse that is leased from the wife of its directors. The lease rentals are at arm’s length.• A performance-related

During the period ended 30 June 2023, Ru Li, an employee of Westshore Company, purchased goods from the company on normal commercial terms and conditions. Li receives remuneration consisting of cash and other short-term benefits amounting to $240 000.During the 30 June 2023 financial year, Li

Wilderness Windfarms is a government organisation which directly controls another entity — Steam Energy Ltd. Through this investment it indirectly controls Blades Construction Ltd and Zepher Farms Ltd.Required Blades Construction Ltd competes for outside tenders and would rather not disclose to

Explain the meaning of sustainability reporting.

What reasons might an entity provide for adopting ESG practices?

Identify what information entities are likely to provide if they adopt ESG reporting.

Explain the difference between ESG reporting and traditional financial reporting.

What benefits should entities expect from preparing sustainability reports?

What is the TCFD, and what is its purpose?

Showing 3700 - 3800

of 4482

First

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

Step by Step Answers