New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial reporting

Financial Reporting 4th Edition Janice Loftus, Ken Leo, Sorin Daniliuc, Belinda Luke, Hong Nee Ang, Mike Bradbury, Dean Hanlon, Noel Boys, Karyn Byrnes - Solutions

Identify four corporate stakeholders and explain how they affect a business’s operations.

Identify why you would expect the finance sector — and investment funds in particular — to have an interest in climate change.

Identify how ethical investment can affect corporate decision making regarding sustainable business operations.

Explain why governance reporting regulations and principles were introduced.

Explain what governance reporting regulations and principles aim to achieve.

Explain how emissions trading schemes are likely to affect financial reporting.

The manager of Gladstone Ltd is not convinced of the scientific evidence behind climate change, and does not consider it necessary to adopt changes in the company’s operations which would decrease its greenhouse gas emissions. Gladstone Ltd’s accountant, however, has argued that if the company

Darwin Ltd wants to focus on ‘people, profits, planet’. The board of directors has proposed linking top managers’ pay to broad measures of environmental sustainability, and worker and customer satisfaction. The board proposes that bonuses for management will be linked to targets such as the

The report Net Zero Momentum Tracker: Superannuation Sector examines 20 of the largest superannuation funds in Australia, and looks at these organisations’ different investment styles and environmental implications. The report is considered to have a significant impact on the investment

Green, or sustainable finance, is an important part of ethical investment. In many jurisdictions, including Australia and New Zealand, green bonds are becoming an important source of funding.Required What are green bonds? How do they differ from normal bonds?

Find a recent sustainability report. Good reports can be found at the Australian Reporting Awards website; however, it might be useful to compare these to other firms’reports.Required Prepare a report that addresses the following issues.1. The firm’s core values, and how these relate to ESG

This chapter has identified a range of stakeholders that managers should consider when determining sustainability performance and reporting. Determine how managers should engage with each of these stakeholders and document what ESG issues they would be likely to discuss during this engagement

Explain the purpose of the Dow Jones Sustainability Indices.

Some of the traditional sustainability reports are an integrated report, a triple bottom line report, and a CSR report. Research the background of these reports and explain the difference between them. What are some of the benefits and limitations of each?

There are no IFRS accounting standards for the reporting of social and environmental activities. Evaluate what issues this presents for the preparation of financial reports.

You are the accountant of a company that is considering expanding its operations to a developing country. The CEO has asked for a report outlining what issues the company should consider from an ESG perspective when making this decision. Outline some of the key issues to be included in the report.

Explain why rotation (change) of the lead auditor is important.

Explain why composition of the Board of Directors is important.

Explain the difference between an emissions trading scheme and a carbon tax. What are some of the benefits and limitations of each?

Research and prepare a report on the different approaches for accounting for carbon emissions under the EU ETS.

Explain double materiality. Do you think stakeholders are interested in the impact of climate-related risks on the firm or the impact of the firm on climate? Which stakeholders would they be? If you were a standard setter (e.g. XRB), which materiality would you focus on?

Obtain and read the joint AASB–AUASB 2019 statement on climate-related and other emerging risks. What specific AASB/IFRS accounting standards might be affected by climate change risks?

In this chapter we have touched on several important developments in sustainability reporting. Describe any recent developments by visiting the following websites.• GRI, www.globalreporting.org• ISSB, www.ifrs.org/groups/international-sustainability-standards-board/• VRF,

AASB 8/IFRS 8 applies to the financial statements whose debt or equity instruments are traded in a public market. Whereas, most accounting standards apply to all reporting entities. Why do you think segment reporting has a limited scope?

Distinguish between an operating segment and a reportable segment.

Describe how an entity determines its chief operating decision maker.

The 75% threshold relating to revenue refers to ‘external revenue’. Explain what is meant by external revenue and how a segment could generate revenue that is not external.

Explain why the disclosure requirements of AASB 8/IFRS 8 are said to be less prescriptive compared with those of other standards.

AASB 8/IFRS 8 requires entities to disclose information about products and services, geographical areas and major customers. Discuss why such information may benefit users of financial statements.

The controversy of segment reporting is that it is based on information provided to the CODM. Some argue that this makes segment reporting non-comparable. Others argue that it is valuable because investors can see how the business is run 'through the eyes of management'. It is much lower cost

Download the document Post-implementation Review: Operating Segments. Referring to page 7 of this document, prepare a brief report that summarises the key issues identified in the feedback received by the IASB with respect to areas for improvement and amendment to IFRS 8.

AASB 8/IFRS 8 sets out three criteria that need to be followed in order to identify an operating segment.Required List and briefly explain the three criteria.

Kaikoura Ltd is a listed manufacturing company with only one main product line:scientific equipment. A second but very small product line is the data analysis software, which customers typically purchase with the equipment. It manufactures almost all of its products in New Zealand and exports

Using the information from Exercise 21.2, identify Kaikoura Ltd’s operating segments.Exercise 21.2Kaikoura Ltd is a listed manufacturing company with only one main product line:scientific equipment. A second but very small product line is the data analysis software, which customers typically

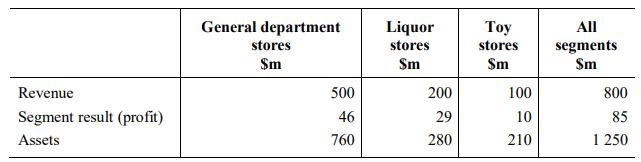

Parattah Ltd is a listed diversified retail company. Its stores are located mainly in Australia.It has three main types of stores: general department stores, liquor stores and specialist toy stores. Each of these stores has different products, customer types and distribution processes.In accordance

Using the information provided about Parattah Ltd, analyse the relative profitability and contribution of the reportable segments.

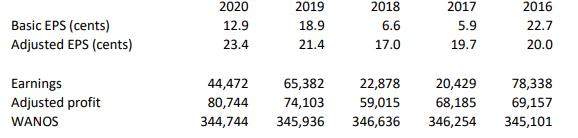

The following is taken from a 5 year review in the annual report of Esperance:A new chair of the audit committee seeks your advice. Write a report with your advice on the following issues:Required A new chair of the audit committee seeks your advice. Write a report with your advice on the

An entity may report significant profits and negative net cash flows from its operating activities or significant accounting losses and positive net cash flows from its operating activities. How can this happen?

How are the techniques for preparing a consolidated statement of cash flows adjusted when the group has obtained or lost control of a subsidiary during the period?

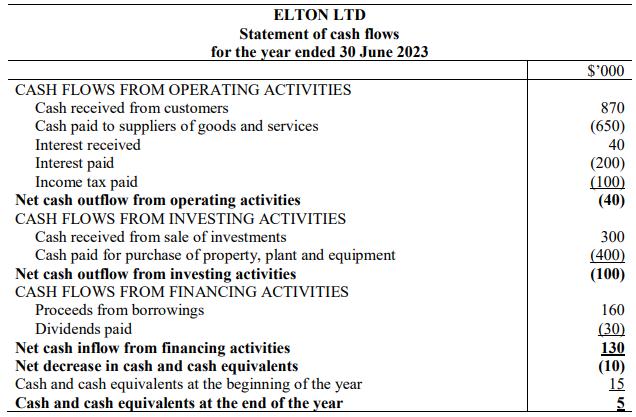

The accountant for Elton Ltd prepared the following statement of cash flows.The managers were worried that investors would be displeased by the negative operating cash flow and that the company’s share price might fall as a result. One manager suggested that the interest paid and interest

Mauve Ltd has the following balances.For the year to 30 June 2023, Sales amounted to \($3\) 500 000, doubtful debts expense was \($75\) 000, discount allowed was \($45\) 000, and cost of sales was \($2\) 400 000.Required 1. Determine cash received from customers of Mauve Ltd for the year ended 30

At 30 June 2022, Tangerine Ltd had accounts receivable of \($200\) 000. At 30 June 2023, accounts receivable was \($240\) 000 and sales for the year amounted to \($2\) 100 000. Bad debts amounting to \($50\) 000 had been written off during the year, and discounts of

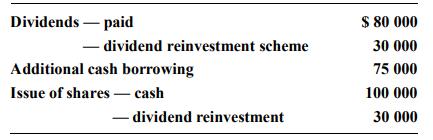

The following information has been compiled from the accounting records of Benji Ltd for the year ended 30 June 2023 in relation to its financing activities.Required Determine the amount of net cash flow from financing activities that Benji Ltd would report in its statement of cash flows for the

What disclosures are required by AASB 101/IAS 1 regarding accounting policies?

Why might there be a change in an entity’s accounting policy?

How should a change in an entity’s accounting policy be applied?

Why would an accounting estimate change and how is the change accounted for?

What is a prior period error? How and when is it corrected?

What is the difference between ‘retrospective application’ and ‘retrospective restatement’?

When is it impracticable to make a retrospective change in an accounting policy or a retrospective restatement to correct an error?

Outline the concept of materiality as it applies to financial reporting.

Explain the difference between adjusting and non-adjusting events occurring after the end of the reporting period. Describe the difference in the way such events impact on the preparation of financial statements.

The board of directors of Gazelle Ltd has resolved to change the company’s accounting policy for capitalising gains or losses on its cash flow hedges recognised in other comprehensive income. To date, such gains or losses were capitalised to hedged items, but the directors now believe that taking

Assume the change in the accounting policy for capitalising hedge gains or losses was due to the issue of a revised accounting standard, AASB 9/IAS 9 Financial Instruments, which requires all hedge gains or losses to be taken to profit or loss, thereby removing the choice to

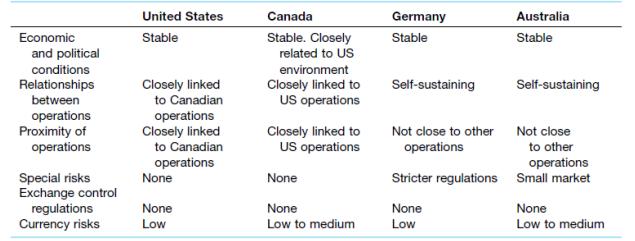

Aardvark Ltd is a catering company specialising in providing catering services to remote area mine sites. The company has operations in Australia but during the current year it acquired significant long-term contracts in China and Japan. AASB 8/IFRS 8 Operating Segments requires entities to

The statement of financial position of Waterbuck Ltd as at 30 June 2023 includes an asset ‘Debenture money receivable \($500\) 000’ and a liability ‘Debentures \($500\) 000’. Note 12 to the accounts reveals that the issue of the debentures to a private investor was approved by the board of

Assume, however the contract was signed with the private investor on 29 June 2023 to issue the debt on 17 July.Required Comment on the accounting treatment of the debenture issue in accordance with the requirements of AASB 110/IAS 10.

The directors of an Australian company, Moose Ltd, have formed a view that compliance with a particular AASB standard will mean the company’s financial statements will not provide a true and fair view, which is contrary to the Corporations Act.Required Advise the directors how this problem can

Yak Ltd estimates its future liability for repairs to products sold with a 12-month warranty as a percentage of its net credit sales. Warranty expense and actual repair costs for the last 2 years ending 30 June were as follows.Required Comment on Yak Ltd’s accounting method for warranty

Macaw Ltd operates a fleet of fishing trawlers. The following events took place after the end of the reporting period, 30 June 2023, but before the date the accounts were authorised, 15 September 2023.(a) On 17 July 2023, Macaw Ltd’s main fishing fleet was sunk during a freak storm.Insurance will

The following relate to Dog Ltd.(a) The useful life of depreciable plant is determined as being 5 years.(b) Dog Ltd depreciates non-current assets.(c) Dog Ltd uses straight-line depreciation.(d) Dog Ltd determines that it will calculate its warranty provision using past experience of products

The annual audit of the accounting records and draft financial statements of Mole Ltd as at 30 June 2023 revealed the following errors and omissions.(a) Credit notes totalling $75 000 relating to June sales were posted against sales made in July.(b) The purchase price of $106 800 for a new vehicle

In order to comply with AASB 108/IAS 8, determine whether the following changes should be accounted for prospectively or retrospectively.1. A change in accounting estimate.2. A voluntary change in an accounting policy.3. A change in accounting policy required by a new or revised accounting

On 1 July 2017, Swan Ltd acquired a building for $12 500 000 with an estimated life of 25 years and a residual value of nil. Swan Ltd uses the straight-line method of depreciation. Based on expert advice provided to Swan Ltd in 2023, it was decided the building should be depreciated over a total

What is the earnings per share ratio used for?

Jonty states that "Tamar Limited is a better investment than Rapid Limited because it has a higher EPS". Evaluate.

How is diluted EPS affected by issued options where the exercise price is above the average market price?

How is diluted EPS affected by issued options where the exercise price is below the current market price?

When calculating EPS, the directors of Pique Limited are not sure how to, or if they need to, include ordinary shares that would be issuable under employee share‐based payment schemes. They argue that the issuing of such shares will be contingent upon the company meeting certain profitability

Visit the websites of two Australian companies in the same industry and access their latest annual reports.Required Extract information on the use of EPS and 1. Describe how many times and where in the annual report EPS is reported, 2. Calculate how much diluted EPS is lower (in percentage terms)

If an entity presents both consolidated and separate financial statements, which statements are used for the calculation of basic EPS? Give reasons for your answer.

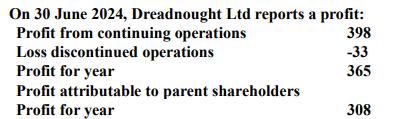

There was no non-controlling interest in the discontinued operations.At the beginning of the reporting period the company had 1 000 ordinary shares outstanding.The company had no share issues during the period and had no potential ordinary shares Required Calculate Dreadnought Ltd’s 2023 basic

Dumbarton Ltd has 80 000 ordinary shares on issue. The company announced a 1-for-4 rights issue with an exercise price of \($5\) for each right. The market price of one ordinary share immediately before the exercise of the rights was $6.Required Determine the theoretical ex-rights value per share.

Assume that in exercise 20.4 Dumbarton Ltd announced the rights issue at the beginning of its reporting period (1 July 2023) and the last date for exercising the rights was 1 October 2023. Dumbarton Ltd announced profit attributable to ordinary shareholders of $9 175 for the full reporting

An entity announces a share split to occur in the current reporting period. There is no consideration payable by existing shareholders and therefore no corresponding increase in the entity’s resources.Required Should the entity recognise the additional shares in the weighted average number of

On 31 December 2024, Caradoc Ltd has 50 000 ordinary shares outstanding. The only change in share outstanding during this period was a 1 for 2 bonus issue on 1 March 2023.Caradoc Ltd’s profit attributable to ordinary shareholders was $15 000 (2023: $14 000, 2022; $11

Amphion Ltd determines its profit attributable to ordinary shareholders for the reporting period ended 30 June 2024 as \($52\) 180.The company has calculated its weighted average number of ordinary shares on issue during the period as 140 000. Amphion has issued options for 60,000 shares.The

Temeraire Ltd has 100 000 ordinary shares outstanding during the reporting period ended 30 June 2024. The profit attributable to parent shareholders (there are no discontinued operations or non-controlling shareholders) was \($7\) 250. The average market price of its ordinary shares during the

At the beginning of the current reporting period (1 January 2023) Atropos Ltd has 60 000 ordinary shares on issue. The company announced a 1‐for‐5 rights issue on 1 January 2023.The exercise price is \($2\) and the last date to exercise the rights is 1 April 2023. The market price of one

Papillion Ltd operates an executive performance share plan. Under this plan, the company grants rights to employees which are convertible into ordinary shares of the company. It also grants options under the plan. The options have a term of 5 years and are converted into ordinary shares when the

Discuss whether warranties that accompanying a sale of goods is a performance obligation of the contract with the customer and how it affects the sales recognition.

Sahara Ltd sells goods to Jackson Ltd. The agreement between the two parties states that Jackson Ltd pays for the goods in advance of delivery which will occur in 12 months’ time. Control of the goods passes to Jackson Ltd at the date of delivery. Jackson Ltd pays $40 000 to Sahara Ltd on 1 July

State whether each of the following is true or false.1. ‘Income’ means the same as ‘revenue’.2. All ‘revenue’ is ‘income’.3. ‘Gains’ are always recognised net under IFRSs.4. ‘Revenue’ must always be in respect of an entity’s ordinary operations.5. ‘Gains’ must always

State whether each of the following is true or false.1. Revenue is measured at the fair value of the consideration given by the seller.2. Revenue is measured at the transaction price that is allocated to that performance obligation.3. If payment for the goods or services is deferred, the fair value

On 1 February 2024, FastNet Ltd entered into an agreement with Smith Ltd to develop a new database system (both hardware and software) for Smith Ltd. The agreement states that the total consideration to be paid for the system will be \($430\) 000. FastNet Ltd expects that its total costs for the

In each of the following situations, state at which date, if any, revenue will be recognised.1. A contract for the sale of goods is entered into on 1 May 2024. The goods are delivered on 15 May 2024. The buyer pays for the goods on 30 May 2024. The contract contains a clause that entitles the buyer

All Star Ltd provides a bundled service offering to Bruce Ltd. It charges Bruce Ltd $28 000 for initial connection to its network and two ongoing services — access to the network for 1 year and ‘on-call troubleshooting’ advice for that year.Bruce Ltd pays the $28 000 upfront, on 1 July 2024.

Swablu Ltd sells office equipment to Chantelle Ltd. Rather than paying in cash, Chantelle Ltd will transfer some furniture to Swablu Ltd. The furniture is recorded in Chantelle Ltd's account at a cost of \($23\) 000 and with accumulated depreciation of \($4\) 000. The fair value of the furniture is

Logistics Ltd provides professional advisory services to develop internal and external reporting systems to facilitate the integration of various forms of capital (financial, mechanical, human, intellectual, natural and social) in the business models of their clients. The contracts take up to 18

What is the purpose of a statement of financial position? Discuss the factors to consider when assets and liabilities are classified into current and non-current.

What is the purpose of statement of profit or loss? Why other comprehensive income is presented separately from the profit or loss?

Statement of profit or loss can be presented either by nature or by function of the expenses. Explain the difference between these classifications.

Review the published financial reports of the following companies and report on the information applicable to the statement of profit or loss and other comprehensive income.Determine whether the expenses are classified by nature or function. Give some possible reasons for the different methods of

A first-time shareholder has approached you requesting some advice. The shareholder has received the company’s annual report and noticed the following statement in the summary of significant accounting policies:The financial report has been prepared on the basis of historical cost, except for the

Any judgements made by management when applying the entity’s accounting policies that have significant effect on amounts recognised in the financial statements must also be disclosed. What judgements do you think are made by management?

Marsha Ltd has recently hired a trainee who is unsure of the presentation of income and expense items recognised in a period and what items to be presented in other comprehensive income.Required Assume you are the accountant responsible for preparing the statement of profit or loss, you need to

The directors of an Australian company that is required to prepare financial reports under the Corporations Act conclude that applying the requirements of AASB 136/IAS 36 Impairment of Assets would not provide a fair presentation because the resulting $120 000 impairment loss is

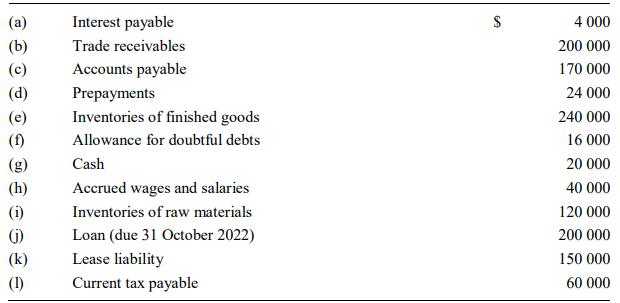

The general ledger trial balance of David Ltd at 30 June 2022 includes the following asset and liability accounts. • The lease liability (k) includes an amount of \($26\) 000 for lease payments due before 30 June 2023.• The company classifies assets and liabilities using a currenton-current

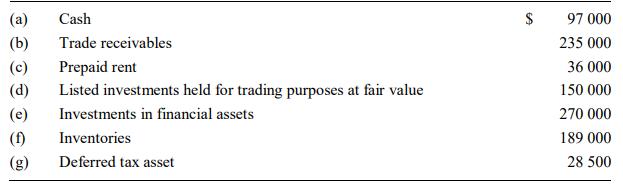

The general ledger trial balance of Jojoba Ltd includes the following asset accounts at 30 June 2023.• Jojoba Ltd’s investments are part of a long-term investment strategy.• The company classifies assets and liabilities using a currenton-current basis.Required Prepare the current asset

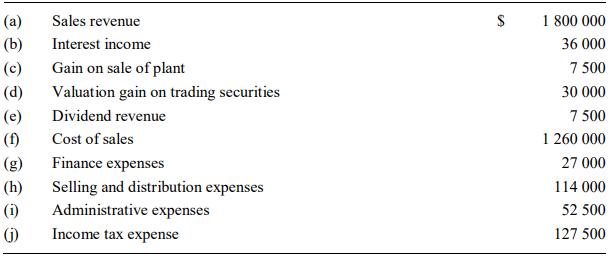

The general ledger trial balance of DEF Ltd includes the following accounts at 30 June 2023.• DEF Ltd recognised a loss on valuation of \($1500\) net of tax for financial assets recognised at fair value through other comprehensive income. No financial assets were sold during the year.• A gain

Showing 3800 - 3900

of 4482

First

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

Step by Step Answers