New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial statement analysis

Financial Statement Analysis 10th edition K. R. Subramanyam, John J. Wild - Solutions

What are management’s objectives in determining a company’s investment in inventories and receivables?

What is the justification for including prepaid expenses in current assets?

Certain installment receivables are not collectible within one year. Why are these receivables sometimes included in current assets?

What is the forecast horizon?

A current exposure draft requires companies to recognize the fair value of employee stock op-tions as an operating expense. Options pricing models are used to estimate the fair value of the options. Under current GAAP, companies have the choice to provide footnote disclosure of pro forma effects on

Accounting for earnings per share has certain weaknesses that our analysis must consider for interpreting EPS data. Identify and discuss at least two weaknesses.

EPS can affect a company’s stock prices. Can a company’s stock prices affect EPS?

What is the purpose underlying the reporting of diluted EPS?

What factors cause the effective tax rate to differ from the statutory rate?

Analysts often refer to the core income of a company. What is meant by the term core income?

Although comprehensive income is the bottom line income number, it is rarely reported in the income statement. Where will you typically find details regarding comprehensive income?

Explain how accountants measure income.

Describe the analysis procedure available to adjust an income statement using pooling accounting so as to be comparable with an income statement using purchase accounting.

Describe the accounting treatment for speculative derivatives.

When does a derivative security qualify for hedge accounting under SFAS 133?

What is a hedge transaction?

Describe a swap contract. How are swaps typically used by companies?

Describe a futures contract.

Distinguish between hedging and speculative activities with regard to derivatives.

Distinguish between a “hard asset” and a “soft asset.” Cite several examples.

Explain when an expenditure should be capitalized versus when it should be expensed.

One means for a corporation to generate long-term financing is through issuance of noncurrent debt instruments in the form of bonds.Required:a. Describe how to account for proceeds from bonds issued with detachable stock purchase warrants.b. Contrast a serial bond with a term (straight) bond.c.

Identify what items are treated as prior period adjustments.

Explain how off-balance-sheet financing items should be treated for financial analysis purposes.

Define off-balance-sheet financing and provide three examples.

Define the term big bath. Explain when a manager would consider “taking a big bath” and how analysis of current financial position and future profitability might be adjusted if one suspects that a company has taken a big bath.

Discuss how the lessor reflects the benefits of leasing in the income statement under (a) an operating lease and (b) a capital lease.

Discuss how the lessee reflects the cost of leased equipment in the income statement for (a) assets leased under operating leases and (b) assets leased under capital leases.

Explain how analysis of financial statements is used to evaluate a company’s liabilities, both existing and contingent.

Debt contracts usually place restrictions on the ability of a company to deploy resources and to pursue business activities. These are often referred to as debt covenants.a. Identify where information about such restrictions is found.b. Define margin of safety as it applies to debt contracts and

Describe the major disclosure requirements for long-term liabilities.

Explain how the issuance of convertible debt and warrants can affect the valuation analysis conducted by current and potential stockholders.

Both convertibility and warrants attached to debt aim at increasing the attractiveness of debt securities and lowering their interest cost. Describe how the costs of these two features affect income and equity.

Describe the conditions necessary to demonstrate the ability of a company to refinance its short-term debt on a long-term basis.

Identify the major disclosure requirements for financing-related current liabilities.

Identify and describe the two major sources (as linked with business activities) of current liabilities.

Public accounting firms are being implored to assess a company’s reported earnings per share relative to the market expectation of earnings per share (e.g., consensus analysts’ forecast) when establishing the level of misstatement that is considered acceptable (the materiality threshold).

Explain why financial statements are important to the decision-making process in financial analysis. Also, identify and discuss some of their limitations for analysis purposes.

Citigroup is currently audited by KPMG. Who pays KPMG for its audit of Citigroup? To whom is KPMG providing assurance regarding the fair presentation of the Citigroup financial statements? List two market forces faced by KPMG that increase the probability that the firm effectively performed an

What are some circumstances suggesting higher audit risk? Explain.

What does the auditor’s reference to generally accepted accounting principles imply for our analysis of financial statements?

An auditor does not prepare financial statements but instead samples and investigates data to render a professional opinion on whether the statements are “fairly presented.” List the potential implications of the auditor’s responsibility to users that rely on financial statements.

What are some implications to financial analysis stemming from the audit process?

What does the opinion section of the auditor’s report usually cover?

What are auditing procedures? What are some basic objectives of a financial statement audit?

What are generally accepted auditing standards?

What gives rise to accounting distortions? Explain.

Discuss the advantages and disadvantages of fair value accounting.

What adjustments would you make to net income to determine economic income?

Explain how accountants measure income.

Describe alternative information sources beyond statutory financial reports that are available to investors and creditors.

Describe forces that serve to limit the ability of management to manage financial statements.

Who has the main responsibility for ensuring fair and accurate financial reporting by a company?

Describe the U.S. financial reporting environment including the following:a. Forces that impact the content of statutory financial reportsb. Rule-making bodies and regulatory agencies that formulate GAAP used in financial reportsc. Users of financial information and what alternative sources of

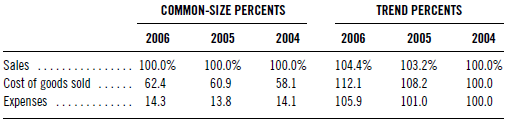

Common-size and trend percents for JBC Company’s sales, cost of goods sold, and expenses follow:Determine whether net income increased, decreased, or remained unchanged in this three-year period. COMMON-SIZE PERCENTS TREND PERCENTS 2004 100.0% 58.1 14.1 2005 2006 2004 2005 2006 100.0% 60.9 13.8

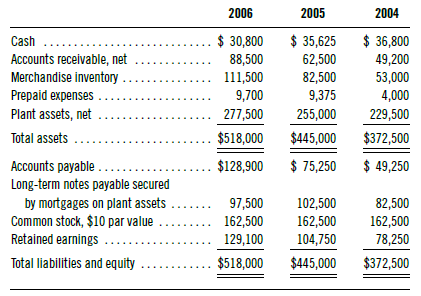

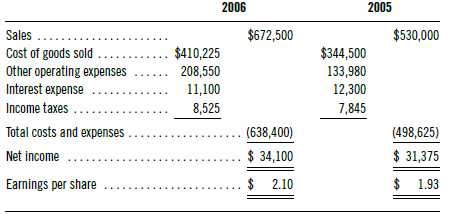

Refer to the information in Exercises 1–3 and 1–5 about Mixon Company. Compare the long-term risk and capital structure positions of the company at the end of 2006 and 2005 by computing the following ratios:(a) Total debt ratio(b) Times interest earned. Comment on these ratio results.In

Showing 5600 - 5700

of 5656

First

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

Step by Step Answers