New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting 11th

Intermediate Accounting IFRS International Adaptation 5th Edition Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield - Solutions

18. What is the difference between a lease receivable and a net investment in the lease?

17. Explain which of the following would result in the lessor classifying the lease as a finance lease.a. The lease is for a major part of the economic life of the asset.b. The lease term is 12 months or less.c. The lease transfers ownership of the asset at the end of the lease.

16. Identify the lease classifications for lessors and the criteria that must be met for each classification. What is the relevance of revenue recognition criteria for lessor accounting for leases?

15. Describe the effect on the lessee of a “bargain purchase option” in accounting for a finance lease transaction.

14. What is a short-term lease? Describe lessee accounting for a short-term lease.

13. What is a low-value lease? Describe lessee accounting for low-value leases.

12. Describe the accounting procedures involved in applying the finance lease method by a lessee.

11. Harcourt Company enters into a lease agreement with Brunsell Inc. to lease office space for a term of 72 months. Lease payments during the first year are $5,000 per month. Each year thereafter, the lease payments increase by an amount equivalent to the percentage increase in a price index. For

10. Identify the amounts included in the measurement of the rightof-use asset.

9. Wonda Stone read somewhere that a residual value guarantee is used for computing the present value of lease payments. Is Wonda correct in her interpretation? Explain.

8. What payments are included in the lease liability?

7. Explain the following concepts: (a) bargain purchase option and(b) bargain renewal option.

6. Describe the following terms: (a) residual value, (b) guaranteed residual value, and (c) initial direct costs.

5. Paul Singer indicated that “all leases must now be capitalized on the statement of financial position.” Is this statement correct? Explain.

4. Morgan Handley and Tricia Holbrook are discussing the new leasing standard. Morgan believes the standard requires that the lessee use the implicit rate of the lessor in computing the present value of its lease liability. Tricia is not sure if Morgan is correct. Explain the discount rate that the

3. What are the major advantages to a lessor for becoming involved in a leasing arrangement?

2. Bradley plc is expanding its operations and is in the process of selecting the method of financing this program. After some investigation, the company determines that it could (1) issue bonds and with the proceeds purchase the needed assets, or (2) lease the assets on a long-term basis. Without

1. What are the major lessor groups? What advantage does a captive leasing subsidiary have in a leasing arrangement?

CA19.6 (LO 1, 3, 4) Ethics (Non-Vested Employees—An Ethical Dilemma) Cardinal Technology recently merged with College Electronix (CE), a computer graphics manufacturing firm. In performing a comprehensive audit of CE’s accounting system, Richard Nye, internal audit manager for Cardinal

CA19.5 (LO 1) Writing (Implications of International Accounting Standard No. 19) Ruth Moore and Carl Nies have to do a class presentation on the pension pronouncement “Employee Benefits.”In developing the class presentation, they decided to provide the class with a series of questions related

CA19.4 (LO 1) Writing (Major Pension Concepts) Lyons plc is a medium-sized manufacturer of paperboard containers and boxes. The company sponsors a non-contributory, defined benefit pension plan that covers its 250 employees. Tim Shea has recently been hired as president of Lyons plc. While

CA19.3 (LO 1) (Basic Terminology) In examining the costs of pension plans, Leah Hutcherson, public accountant, encounters certain terms. The components of pension costs that the terms represent must be dealt with appropriately if IFRS is to be reflected in the financial statements of entities with

CA19.2 (LO 1) Writing (Pension Terminology) The following items commonly appear in a company’s financial statements.1. Under the caption Assets:Pension asset/liability.2. Under the caption Liabilities:Pension asset/liability.3. Under the caption Equity:Asset loss as a component of Accumulated

CA19.1 (LO 1) (Pension Terminology and Theory) Since the late 1800s, many business organizations have been concerned with providing for the retirement of their employees. During recent decades, a marked increase in this concern has resulted in the establishment of pension plans in most large

P19.14 (LO 6) (Postretirement Benefit Worksheet—2 Years) Elton AG has the following postretirement benefit plan balances on January 1, 2025.Defined postretirement benefit obligation €2,250,000 Fair value of plan assets 2,250,000 The discount (interest) rate applicable to the plan is 10%. On

P19.13 (LO 6) Groupwork (Postretirement Benefit Worksheet) Hollenbeck Foods Inc.sponsors a postretirement medical and dental benefit plan for its employees. The following balances relate to this plan on January 1, 2025.Plan assets $200,000 Defined postretirement benefit obligation 200,000 As a

P19.12 (LO 2, 4, 5) (Pension Worksheet) Chen Group sponsors a defined benefit pension plan for its employees. On January 1, 2025, the following balances related to this plan (amounts in thousands).Plan assets (fair value) ¥270,000 Defined benefit obligation 340,000 Pension asset/liability 70,000

P19.11 (LO 2, 4, 5) (Pension Worksheet) The following data relate to the operation of Kramer Co.’s pension plan in 2026. The pension worksheet for 2025 is provided in P19.10.Service cost $59,000 Actual return on plan assets 32,000 Annual contributions 51,000 Benefits paid retirees 27,000 For

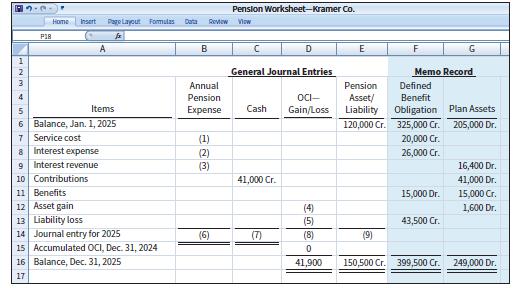

P19.10 (LO 2, 4) (Pension Worksheet—Missing Amounts) Kramer Co. has prepared the following pension worksheet (amounts in $). Unfortunately, several entries in the worksheet are not decipherable.The company has asked your assistance in completing both the worksheet and the accounting tasks related

P19.9 (LO 2, 3, 4) Groupwork (Comprehensive 2-Year Worksheet) Hobbs AG has the following defined benefit pension plan balances on January 1, 2025.Defined benefit obligation €4,600,000 Fair value of plan assets 4,600,000 The discount (interest) rate applicable to the plan is 10%. On January 1,

P19.8 (LO 2, 4, 5) Groupwork (Comprehensive 2-Year Worksheet) Lemke SA sponsors a defined benefit pension plan for its employees. The following data relate to the operation of the plan for the years 2025 and 2026.2025 2026 Defined benefit obligation, January 1 R600,000 Plan assets (fair value),

P19.7 (LO 2, 4) (Pension Worksheet) Hanson Ltd. sponsors a defined benefit pension plan for its employees. On January 1, 2025, the following balances related to this plan.Plan assets (fair value) £520,000 Defined benefit obligation 700,000 Pension asset/liability 180,000 Cr.Accumulated net loss

P19.6 (LO 1, 4) (Pension Expense, Journal Entries, and Net Gain or Loss) Aykroyd Inc. has sponsored a non-contributory, defined benefit pension plan for its employees since 1995. Relevant information about the pension plan on January 1, 2025, is as follows.1. The company has 200 employees. All

P19.5 (LO 4) (Computation of Pension Expense, Journal Entries for 3 Years) Hiatt Toothpaste SA initiates a defined benefit pension plan for its 50 employees on January 1, 2025. The insurance company which administers the pension plan provided the following selected information for the years 2025,

P19.4 (LO 2, 4) (Pension Expense, Journal Entries for 2 Years) Gordon Company sponsors a defined benefit pension plan. The following information related to the pension plan is available for 2025 and 2026 (no benefits were paid in either year).2025 2026 Plan assets (fair value), December 31 $699,000

P19.3 (LO 3, 4, 5) (Pension Expense, Journal Entries) Gottschalk plc sponsors a defined benefit plan for its 100 employees. On January 1, 2025, the company’s actuary provided the following information.Pension plan assets (fair value) £200,000 Accumulated benefit obligation 260,000 Defined

P19.2 (LO 2, 3, 4, 5) Groupwork (3-Year Worksheet, Journal Entries, and Reporting) Jackson Company adopts acceptable accounting for its defined benefit pension plan on January 1, 2024, with the following beginning balances: plan assets $200,000 and defined benefit obligation $250,000. Other data

P19.1 (LO 2, 4, 5) (2-Year Worksheet) On January 1, 2025, Harrington SA has the following defined benefit pension plan balances.Defined benefit obligation €4,500,000 Fair value of plan assets 4,200,000 The interest rate applicable to the plan is 10%. On January 1, 2026, the company amends its

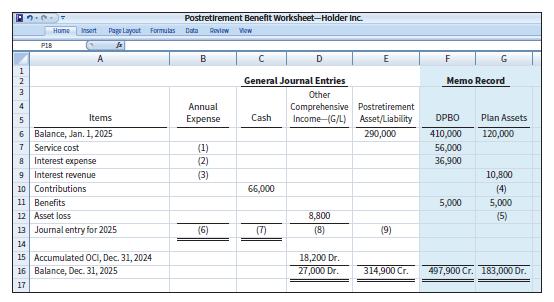

E19.21 (LO 6) (Postretirement Benefit Worksheet—Missing Amounts) The accounting staff of Holder Inc. has prepared the following postretirement benefit worksheet (amounts in €). Unfortunately, several entries in the worksheet are not decipherable. The company has asked your assistance in

E19.20 (LO 6) (Postretirement Benefit Worksheet) Using the information in E19.19, prepare a worksheet inserting the January 1, 2025, and December 31, 2025, balances, and the journal entry recording postretirement benefit expense.

E19.19 (LO 6) (Postretirement Benefit Expense Computation) Englehart AG provides the following information about its postretirement benefit plan for the year 2025.Service cost € 90,000 Contribution to the plan 56,000 Actual return on plan assets 62,000 Benefits paid 40,000 Plan assets at January

E19.18 (LO 6) (Postretirement Benefit Expense Computation) Garner Inc. provides the following information related to its postretirement benefits for the year 2025.Defined postretirement benefit obligation at January 1, 2025 $710,000 Actual return on plan assets (at 10%) 34,000 Discount (interest)

E19.17 (LO 6) (Postretirement Benefit Worksheet) Using the information in E19.16, prepare a worksheet inserting January 1, 2025, balances, and showing December 31, 2025, balances. Prepare the journal entry recording postretirement benefit expense.

E19.16 (LO 6) (Postretirement Benefit Expense Computation) Kreter Concepts provides the following information about its postretirement benefit plan for the year 2025.Service cost P 45,000 Contribution to the plan 10,000 Actual return on plan assets (at 8%) 8,800 Benefits paid 20,000 Plan assets at

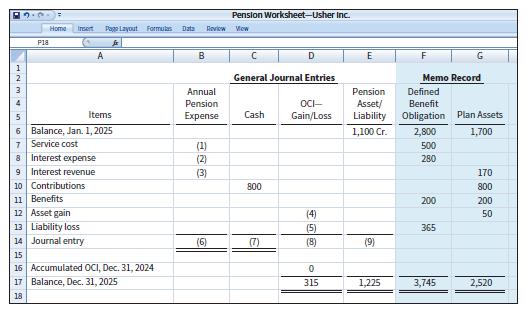

E19.15 (LO 2, 5) (Pension Worksheet—Missing Amounts) The accounting staff of Usher Inc.has prepared the following pension worksheet (amounts in $). Unfortunately, several entries in the worksheet are not decipherable. The company has asked for your assistance in completing the worksheet and the

E19.14 (LO 2, 5) (Pension Expense, Journal Entries) Latoya Company provides the following selected information related to its defined benefit pension plan for 2025.Pension asset/liability (January 1) $ 25,000 Cr.Accumulated benefit obligation (December 31) 400,000 Actual return on plan assets

E19.13 (LO 2, 4, 5) (Worksheet for E19.12) Using the information in E19.12 about Erickson plc’s defined benefit pension plan, prepare a 2025 pension worksheet with supplementary schedules of computations. Prepare the journal entries at December 31, 2025, to record pension expense and related

E19.12 (LO 1, 4, 5) (Computation of Actual Return, Gains and Losses, and Pension Expense)Erickson plc sponsors a defined benefit pension plan. The company’s actuary provides the following information about the plan.January 1, 2025 December 31, 2025 Vested benefit obligation £1,500 £1,900

E19.11 (LO 1, 2, 4, 5) (Pension Expense, Journal Entries, Statement Presentation) Ferreri SpA received the following selected information from its pension plan trustee concerning the operation of the company’s defined benefit pension plan for the year ended December 31, 2025.January 1, 2025

E19.10 (LO 1, 4, 5) (Pension Expense, Journal Entries, Statement Presentation) Henning plc sponsors a defined benefit pension plan for its employees. The following data relate to the operation of the plan for the year 2025.1. The actuarial present value of future benefits earned by employees for

E19.9 (LO 2, 4) (Pension Worksheet and Remeasurement) Webb Corp. sponsors a defined benefit pension plan for its employees. On January 1, 2025, the following balances relate to this plan.Plan assets $480,000 Defined benefit obligation 600,000 Pension asset/liability 120,000 Accumulated OCI

E19.8 (LO 2, 4, 5) (Disclosures: Pension Expense and Other Comprehensive Income) Taveras Enterprises provides the following information related to its defined benefit pension plan.Balances or Values at December 31, 2025 Defined benefit obligation €2,729,907 Fair value of plan assets 2,278,329

E19.7 (LO 2, 4, 5) (Pension Worksheet, Gains and Losses) Kennedy Company had a defined benefit obligation of $6,300,000 and plan assets of $4,900,000 at January 1, 2025. Kennedy has the following data related to the plan during 2025.Discount (interest) rate 7%Service cost $120,000 Actual return on

E19.6 (LO 2, 3) (Basic Pension Worksheet, Past Service Costs) The following defined pension data of Yang Ltd. apply to the year 2025 (amounts in thousands).Defined benefit obligation, 1/1/25 (before amendment) ¥560,000 Plan assets, 1/1/25 546,200 Pension liability 13,800 On January 1, 2025, Yang

E19.5 (LO 1) (Computation of Actual Return, Asset Gain and Loss) Gingrich Importers provides the following pension plan information.Fair value of pension plan assets, January 1, 2025 2,400,000 Fair value of pension plan assets, December 31, 2025 2,725,000 Contributions to the plan in 2025 280,000

E19.4 (LO 2) (Basic Pension Worksheet) The following facts apply to the pension plan of Boudreau plc for the year 2025.Plan assets, January 1, 2025 £490,000 Defined benefit obligation, January 1, 2025 490,000 Discount (interest) rate 8%Service cost 40,000 Contributions (funding) 25,000 Actual

E19.3 (LO 2) (Preparation of Pension Worksheet) Using the information in E19.2, prepare a pension worksheet inserting the January 1, 2025 and December 31, 2025, balances, and the journal entry recording pension expense.

E19.2 (LO 1) (Computation of Pension Expense) Veldre SpA provides the following information about its defined benefit pension plan for the year 2025.Service cost € 90,000 Contribution to the plan 105,000 Benefits paid 40,000 Plan assets at January 1, 2025 640,000 Defined benefit obligation at

E19.1 (LO 1) (Pension Expense, Journal Entry) The following information is available for the pension plan of Radcliffe Company for the year 2025.Interest revenue on plan assets $ 15,000 Benefits paid to retirees 40,000 Contributions (funding) 90,000 Discount (interest) rate 10%Defined benefit

BE19.12 (LO 6) For 2025, Benjamin plc computed its annual postretirement expense as £240,900.Benjamin’s contribution to the plan during 2025 was £160,000. Prepare Benjamin’s 2025 entry to record postretirement expense.

BE19.11 (LO 6) Caleb Corporation has the following information available concerning its postretirement medical benefit plan for 2025.Service cost $40,000 Interest expense 52,400 Interest revenue 26,900 Compute Caleb’s 2025 postretirement expense.

BE19.10 (LO 5) At December 31, 2025, Conway SA had a defined benefit obligation of €510,000 and plan assets of €322,000. Prepare a pension reconciliation schedule for Conway.

BE19.9 (LO 5) Tevez AG experienced an actuarial loss of €750 in its defined benefit plan in 2025. For 2025, Tevez’s revenues are €125,000, and expenses (excluding pension expense of €14,000) are €85,000.Prepare Tevez’s statement of comprehensive income for 2025.

BE19.8 (LO 2, 4, 5) Hemera SA had a defined benefit obligation of R$3,100,000 and plan assets of R$2,900,000 at January 1, 2025. Hemera’s discount rate is 6%. In 2025, actual return on plan assets is R$160,000. Hemera contributed R$200,000 to the pension fund and paid benefits of

BE19.7 (LO 4) Refer to the information for Villa SpA in BE19.6. Compute the gain or loss on pension plan assets for Villa SpA and indicate the accounting and reporting for the asset gains or losses.

BE19.6 (LO 2, 4) Villa SpA has experienced tough competition, leading it to seek concessions from its employees in the company’s pension plan. In exchange for promises to avoid layoffs and wage cuts, the employees agreed to receive lower pension benefits in the future. As a result, Villa amended

BE19.5 (LO 2) Duesbury Corporation amended its pension plan on January 1, 2025, and granted$120,000 of past service costs to its employees. The employees have an average time to vesting of 4 years.Current service cost for 2025 is $23,000, and net interest expense is $8,000. Compute pension expense

BE19.4 (LO 2) For 2025, assume that Wm Morrison Supermarkets plc (GBR) had pension expense of £61 million and contributed £52 million to the pension fund. Prepare Morrison’s journal entry to record pension income and funding.

BE19.3 (LO 2) At January 1, 2025, Uddin Company had plan assets of $250,000 and a defined benefit obligation of the same amount. During 2025, service cost was $27,500, the discount rate was 10%, actual return on plan assets was $25,000, contributions were $20,000, and benefits paid were $17,500.

BE19.2 (LO 2) For Becker AG, year-end plan assets were €2,000,000. At the beginning of the year, plan assets were €1,680,000. During the year, contributions to the pension fund were €120,000, and benefits paid were €200,000. Compute Becker’s actual return on plan assets.

BE19.1 (LO 2) Assume that Cathay Pacific Airlines (HKG) reported the following in a recent annual report (in millions).Service cost HK$316 Interest on defined benefit obligation 342 Interest revenue on plan assets 371 Compute Cathay Pacific’s pension expense.

28. What are the major differences between postretirement healthcare benefits and pension benefits?

27. What are postretirement benefits other than pensions?

26. Of what value to the financial statement reader is the schedule reconciling the funded status of the plan with amounts reported in the employer’s statement of financial position?

25. Explain the meaning of the following terms.a. Contributory plan.b. Vested benefits.c. Retroactive benefits.

24. At the end of the current year, Joshua plc has a defined benefit obligation of £335,000 and pension plan assets with a fair value of£345,000. The amount of the vested benefits for the plan is £225,000.Joshua has a liability gain of £8,300. What amount and account(s)related to its pension

23. At the end of the current period, Jacob AG has a defined benefit obligation of €125,000 and pension plan assets with a fair value of€98,000. The amount of the vested benefits for the plan is €95,000.What amount and account(s) related to its pension plan will be reported on the company’s

22. Bill Haley is learning about pension accounting. He is convinced that in years when companies record liability gains and losses, total comprehensive income will not be affected. Is Bill correct? Explain.

21. If pension expense recognized in a period exceeds the current amount funded by the employer, what kind of account arises, and how should it be reported in the financial statements? If the reverse occurs—that is, current funding by the employer exceeds the amount recognized as pension

20. What are “liability gains and losses,” and how are they accounted for?

19. How does an “asset gain or loss” develop in pension accounting?

18. Sarah is a finance major who has taken only one accounting course. She asserts that pension remeasurements, like many other accounting adjustments, are recorded in net income. Is Sarah correct?Explain.

17. What is a pension plan curtailment? Explain the accounting for pension plan curtailments.

16. What is meant by “past service cost”? When is past service cost recognized as pension expense?

15. Explain the difference between service cost and past service cost.

13. What is net interest? Identify the elements of net interest and explain how they are computed.14. Given the following items and amounts, compute the actual return on plan assets: fair value of plan assets at the beginning of the period $9,200,000; benefits paid during the period

12. What is service cost, and what is the basis of its measurement?

11. Identify the components of pension expense. Briefly explain the nature of each component.

9. What is the net benefit obligation (asset)? How is the net benefit obligation (asset) reported in the financial statements?10. What elements comprise changes in the net benefit obligation(asset)? How are these changes reported in the financial statements?

8. Explain how cash-basis accounting for pension plans differs from accrual-basis accounting for pension plans. Why is cash-basis accounting generally considered unacceptable for pension plan accounting?

7. Name three approaches to measuring benefits from a pension plan and explain how they differ.

6. What factors must be considered by the actuary in measuring the amount of pension benefits under a defined benefit plan?

5. What is the role of an actuary relative to pension plans? What are actuarial assumptions?

4. The meaning of the term “fund” depends on the context in which it is used. Explain its meaning when used as a noun. Explain its meaning when used as a verb.

3. Differentiate between “accounting for the employer” and“accounting for the pension fund.”

2. Differentiate between a defined contribution pension plan and a defined benefit pension plan. Explain how the employer’s obligation differs between the two types of plans.

1. What is a pension plan? How does a contributory pension plan differ from a non-contributory plan?

CA18.7 (LO 1, 2) Ethics (Deferred Taxes, Income Effects) Stephanie Delaney, a public accountant, is the newly hired director of company taxation for Acme Incorporated, which is a publicly traded company. Ms. Delaney’s first job with Acme is the review of the company’s accounting practices on

CA18.6 (LO 1, 2, 3) (Explain Future Taxable and Deductible Amounts, How Carryforward Affects Deferred Taxes) Maria Rodriquez and Lynette Kingston are discussing accounting for income taxes. They are currently studying a schedule of taxable and deductible amounts that will arise in the future as a

CA18.5 (LO 1, 2) (Explain Computation of Deferred Tax Liability for Multiple Tax Rates) At December 31, 2025, Higley Corporation has one temporary difference which will reverse and cause taxable amounts in 2026. In 2025, a new tax act set taxes equal to 45% for 2026, 40% for 2025, and 34% for 2027

Showing 200 - 300

of 3960

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers